Tiger Research: South Korea's Retail Crypto Investors Are Disappearing — Who Will Sustain the Market in 2026?

- Key Insight: South Korea's crypto market is shifting from retail-led to institution-led. As regulatory clarity remains pending, traditional financial institutions are accelerating their capture of key infrastructure in stablecoins, STOs, and custody through Memorandums of Understanding (MOUs) and equity acquisitions, aiming to seize the front end of digital asset finance.

- Key Elements:

- Institutional activity has moved beyond the stage of cooperative intent into actual business operations and exchange equity acquisitions. For instance, multiple banks and securities firms have acquired stakes in exchanges like Upbit and Korbit to secure user access points.

- The current competition is unfolding across three fronts: stablecoins (delayed by the central bank's 51% rule regulation), STOs (legislation passed but lacking commercial infrastructure), and custody (businesses active but requiring more institutional capital).

- Domestic infrastructure providers (such as LG CNS, DSRV, and Altus) are building localized tracks aligned with the Bank of Korea's CBDC framework to reduce reliance on overseas technology, positioning themselves to gain critical market share when capital inflows accelerate.

- The strategy of overseas Web3 foundations entering South Korea has shifted from building retail community engagement to collaborating with large enterprises and financial institutions, as traditional finance takes over the market.

This article is written by Tiger Research. The Korean crypto market is undergoing a power shift. The era dominated by retail investors is ending. Even before regulations are fully clarified, traditional financial institutions have already begun aggressively competing to secure key infrastructure, including the power to set STO (Security Token Offering) standards, stablecoin payment rails, and the custody market. Behind this seemingly calm MOU competition lies a battle for control over the front-end of digital asset finance in the future – whoever masters this infrastructure gains the customer gateway for the next decade.

Partnerships and equity acquisitions between Korean institutions and securities companies are accelerating simultaneously in the crypto market. However, the overall landscape remains difficult to discern at a glance. Many partnerships have been announced, but actual commercial deployment remains rare. This report explores why the conversion rate is so low and why institutions continue to push forward.

Core Highlights

- Institutional crypto activity in Korea has moved beyond MOUs (Memorandums of Understanding) into concrete business operations and exchange equity acquisitions.

- Institutions are implicitly intensifying competition for key financial infrastructure, including STO standard-setting, stablecoin payment rails, and the custody market.

- Domestic infrastructure builders are becoming the core pillars of institutional business, constructing Korean-native rails that align with the Bank of Korea's CBDC framework and local regulatory requirements, reducing reliance on foreign technology.

- The strategy for overseas Web3 foundations entering Korea has completely shifted from retail community building to partnering with large corporations and financial institutions, as traditional finance accelerates its takeover of the market.

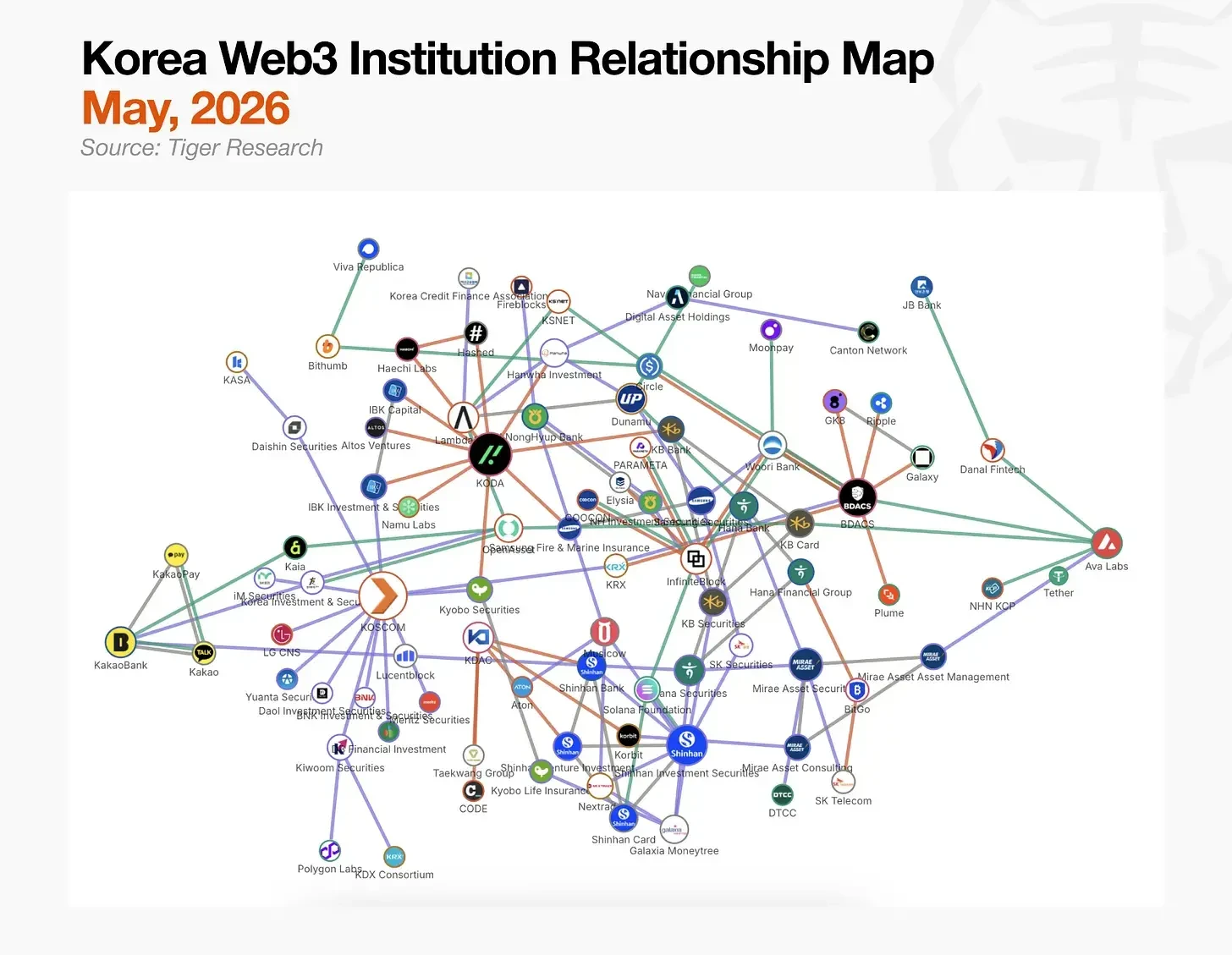

1. The MOU Arms Race

The chart above, compiled by Tiger Research, maps the connections within the Korean institutional crypto landscape. But this structure is not easily discernible. It is difficult to distinguish which lines represent active business operations and which are merely MOUs; the boundaries between central hubs and peripheral players remain blurred.

Notably, this complexity itself accurately reflects the current state of the Korean institutional crypto market. As confirmed by Tiger Research’s dataset – 150 institutions and 196 partnerships – no single hub has yet achieved dominant control over the market.

Domestic institutions are establishing their positions across the entire market simultaneously, even before regulations are fully clarified. The competition currently revolves around three fronts: Stablecoins, STOs, and Custody.

Equally noteworthy is the sustained acquisition of exchange equity by financial institutions, interpreted as a confidence-driven move to secure a foothold before regulatory clarity.

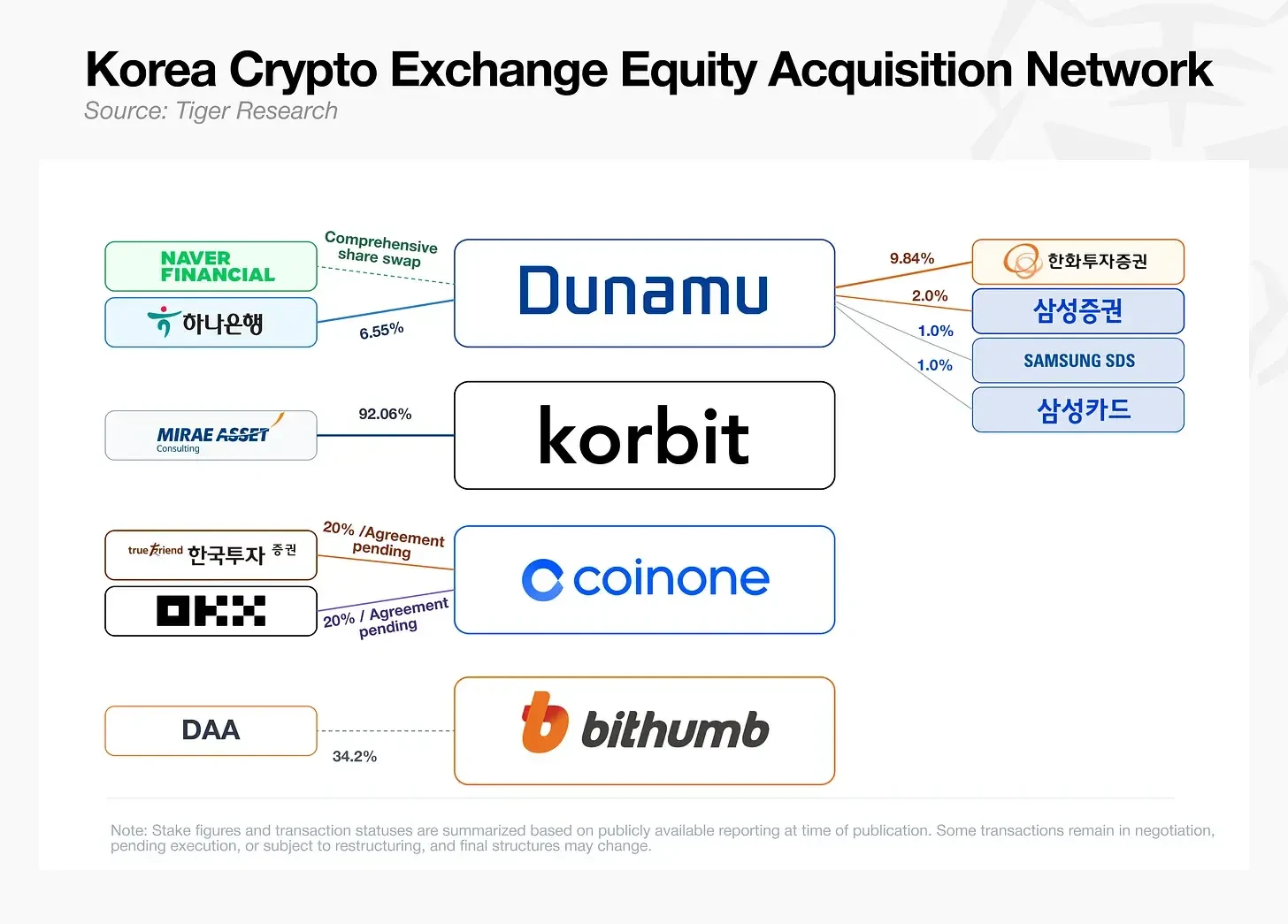

2. The Battle for Exchange Equity

Less than 10 days after Hana Bank announced the acquisition of a 6.55% stake in Dunamu (operator of Upbit) for approximately KRW 1 trillion (approx. USD 720 million), Hanwha Investment & Securities approved an additional 3.90% acquisition. On May 28 of the same month, Samsung Securities, Samsung SDS, and Samsung Card jointly announced a collective acquisition of 4.0%. Mirae Asset Consulting had already signed an agreement in February to acquire a 92.06% stake in Korbit, and there are reports that Korea Investment & Securities and global exchange OKX are discussing a joint acquisition of Coinone.

This competition reflects a revaluation of crypto exchanges, which are now seen not merely as platforms for trading fees, but as critical customer touchpoints for distributing stablecoins, custody services, security tokens, and RWA products.

Banks and securities firms gain indirect access to licenses like VASP registration while securing the exchange's user base and liquidity. The current equity battle is ultimately a race to control the front-end of digital asset finance.

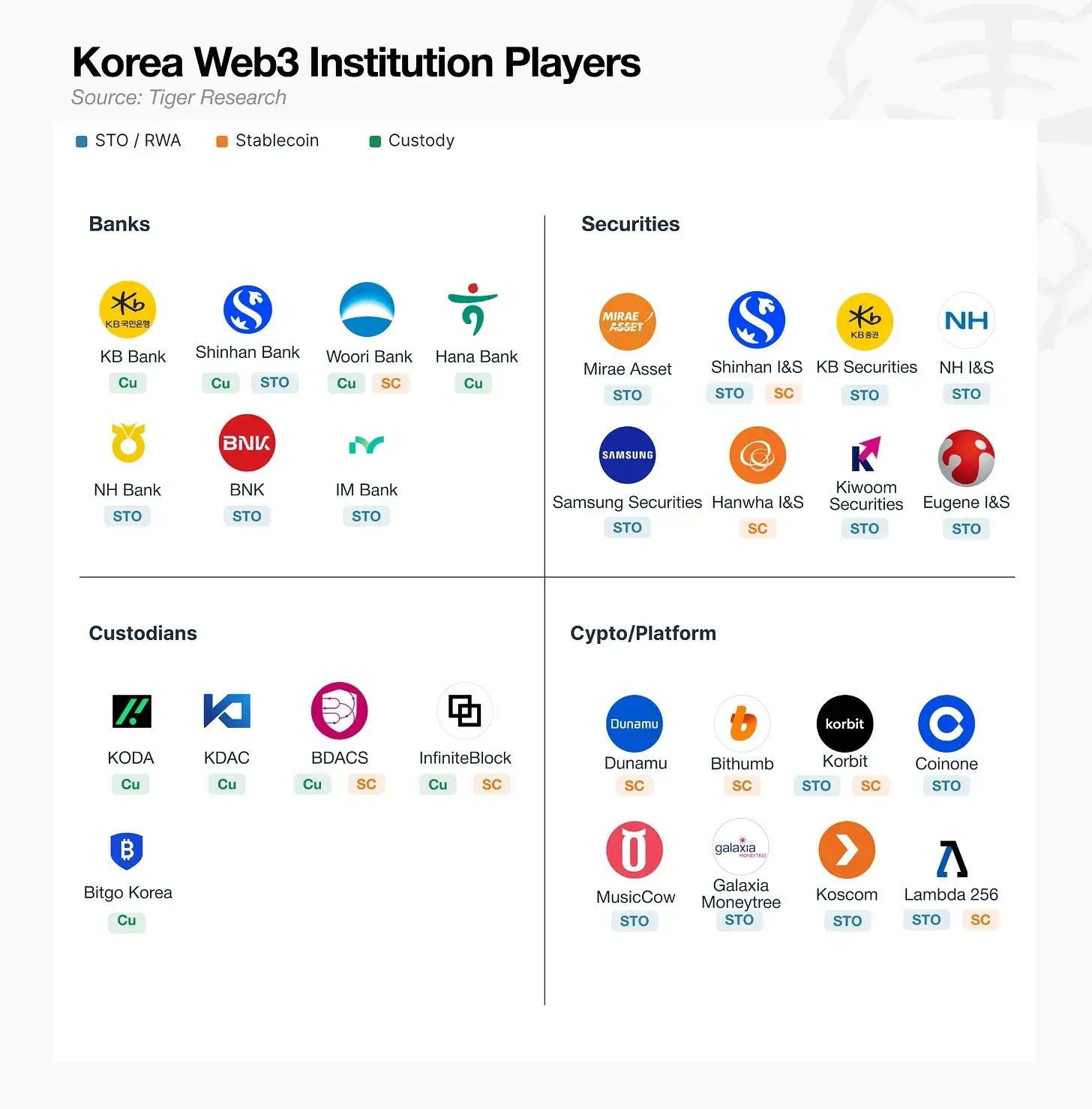

3. The Korean Crypto Market by Sector

A sector-by-sector analysis of the relationship map reveals an uneven landscape. The custody sector shows the most active operations, with many participants running live services after clearing regulatory hurdles. In contrast, RWA and STO remain largely in the contract or MOU stage, awaiting relevant legislation. Stablecoins face a similar stalemate, with no clear standard-setter positioned to dominate the market.

Given the differing nature of barriers across sectors, breakthrough strategies also vary. Some players are consolidating domestic alliances, waiting for regulatory openings. Others are pivoting to overseas markets with faster regulatory progress, forging alternative paths. The following sections explore the specific hurdles and player strategies for each sector.

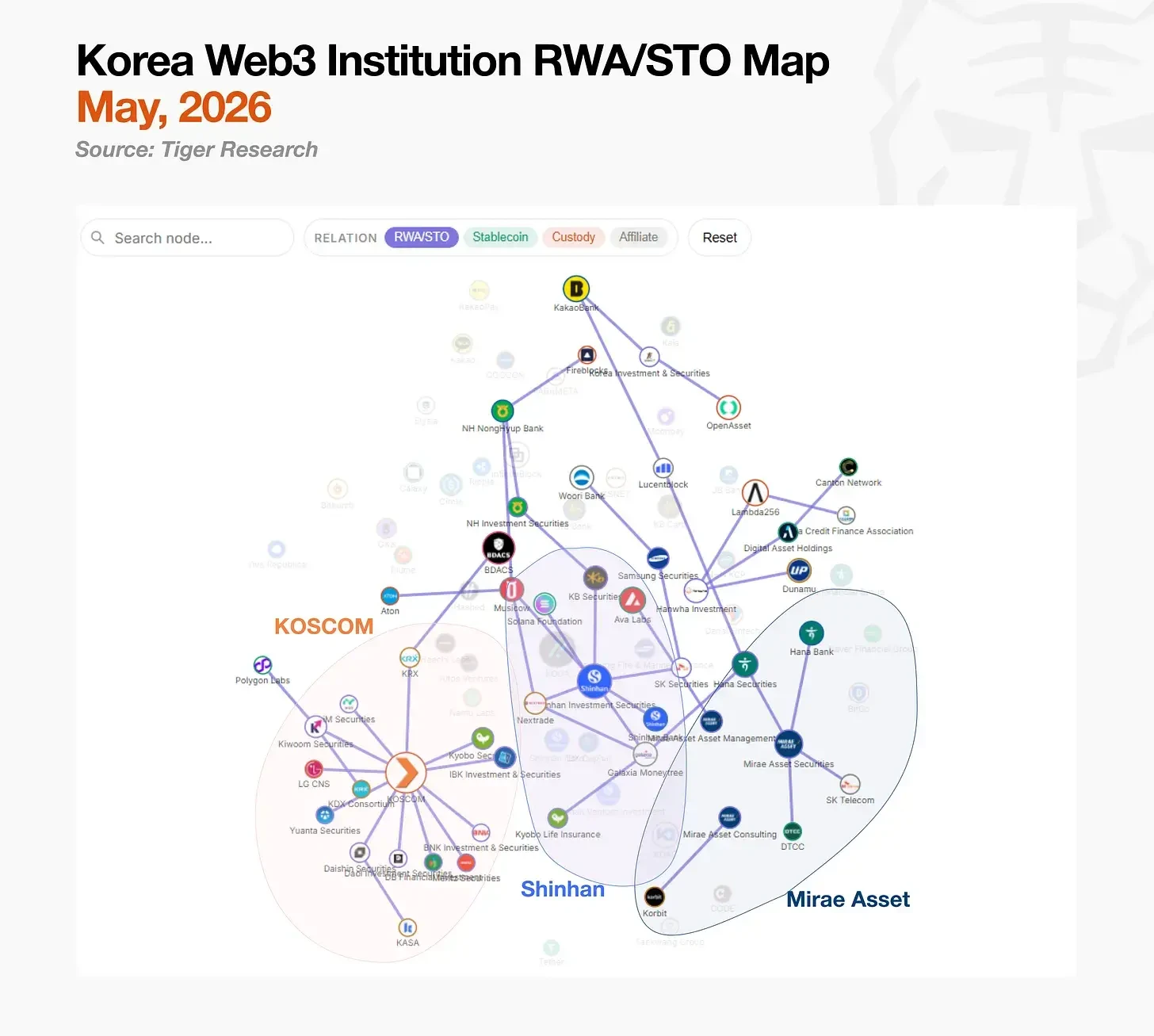

3.1. RWA/STO: Legislation Passed, Commercialization Infrastructure is the Bottleneck

The domestic STO market is divided into two camps: the KOSCOM-led consortium and the fragmented investment consortium led by Shinhan Investment & Securities. Mirae Asset Securities has taken an independent path, leveraging overseas operations rather than waiting for domestic infrastructure.

KOSCOM, a core financial network operator in which the Korea Exchange holds a 76.6% stake, is pursuing a neutral infrastructure model aligned with its founding mission, providing shared infrastructure for securities firms. Rather than signing exclusive deals with individual issuers, it integrates 11 securities firms onto its platform, aiming to set technical standards for issuance and distribution and ensure interfaces compatible with the integrated custody management requirements of the Korea Securities Depository.

Shinhan Investment & Securities has rapidly built its own STO ecosystem. Starting with a proof of concept with Lambda 256 in 2022, it launched the joint platform PULSE in 2024 and officially introduced its multi-platform account integration service in 2025. In 2025 alone, it participated as an account manager in 10 investment contract security token issuances and acquired a controlling stake in the OTC exchange NXT, establishing an end-to-end pipeline from issuance to distribution within its own ecosystem.

Mirae Asset Securities bypassed domestic infrastructure development entirely, moving directly overseas. It issued digital bonds in Hong Kong, secured a digital asset retail license from the Hong Kong Securities and Futures Commission, and plans to launch MTS for retail investors in the market in June. In the US, it is the only Korean securities firm to join the DTCC-led tokenization working group, which includes JPMorgan, Goldman Sachs, and BlackRock, participating in global standard-setting discussions. This strategy positions Mirae Asset favorably in terms of regulatory alignment and negotiation leverage when domestic STO infrastructure eventually connects with global standards.

3.2. Stablecoins: Legislation, Not Technology, is the Bottleneck

The stablecoin market features a more diverse set of participants than other sectors. Card companies, exchanges, fintech firms, and infrastructure providers are all entering via different routes, leveraging their respective strengths.

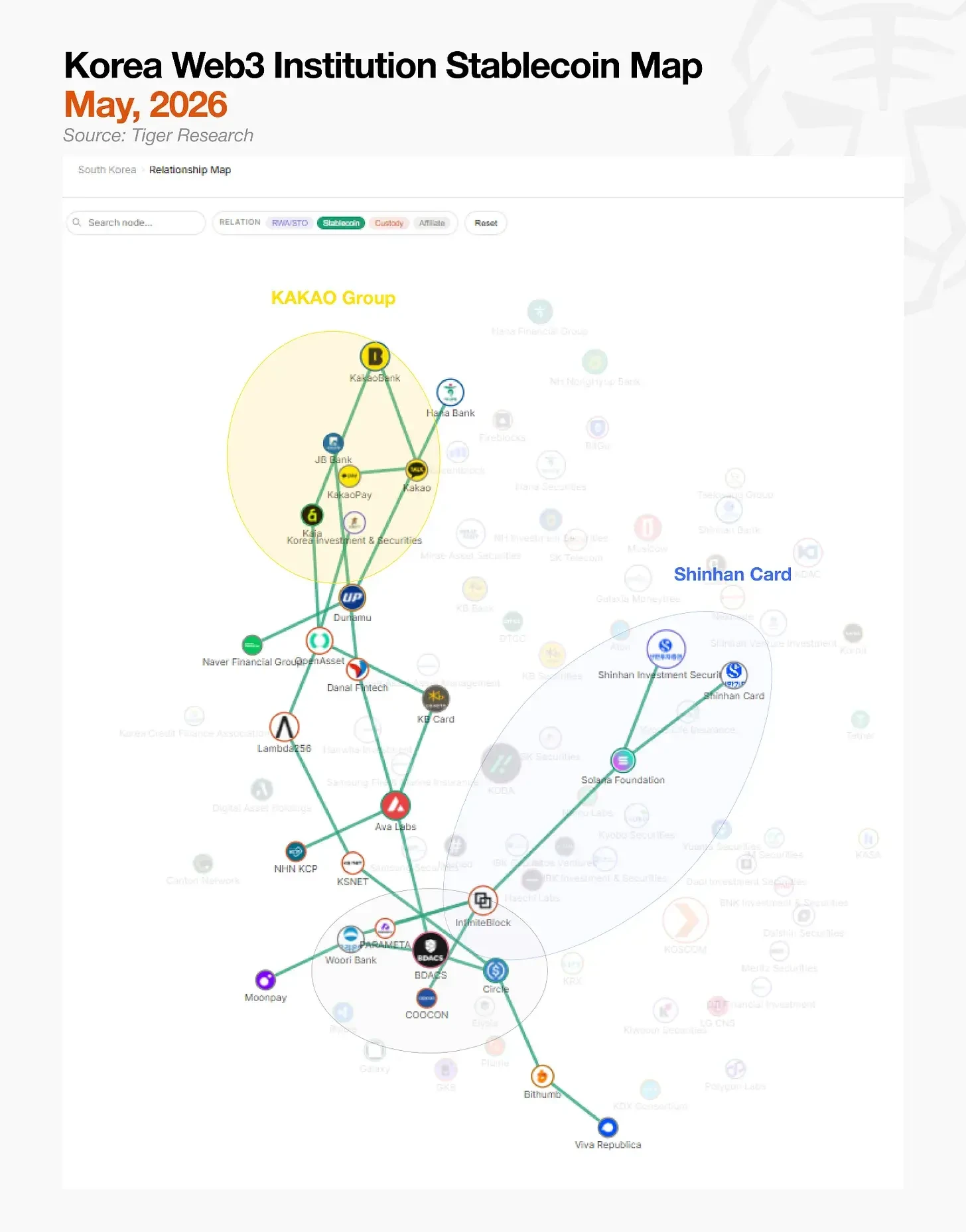

The largest camp is the Kakao Group. Kakao, KakaoBank, and Kakao Pay have formed a joint task force to build a "super wallet" covering stablecoins, cryptocurrencies, and local currencies. Their key asset is the infrastructure accumulated from operating the Kaia public chain since the Ground X era. Kaia has already deployed Tether (USDT) on its network and is conducting real-time payment tests.

Shinhan Card is focused on migrating its existing payment network to blockchain rails. Shinhan Card signed an MOU with Solana in April, although the technical groundwork preceded the agreement. The company has completed initial proofs of concept with Solana, Visa, Mastercard, and Fireblocks, and is now conducting advanced testing in six areas, including wallets and smart contracts.

The exchange camp is bypassing the delay in Korean won stablecoins by using USD stablecoins. Dunamu is developing a Korean won stablecoin business with Naver Financial based on its proprietary blockchain, GIWA. Facing regulatory delays for Korean won stablecoins, Bithumb is opting to first secure a USD stablecoin distribution network through partnerships with Circle and WLF. A joint Korean won stablecoin initiative with Toss is also under discussion, though progress is slow.

All camps are active but face the same regulatory barrier. The Bank of Korea is pushing for a "51% rule," requiring only bank-majority consortia to be allowed to issue stablecoins, while fintech companies are lobbying for access, delaying government-ruling party consultations. Once issuance guidelines are released, the camp with the most comprehensive public touchpoints is expected to achieve market leadership.

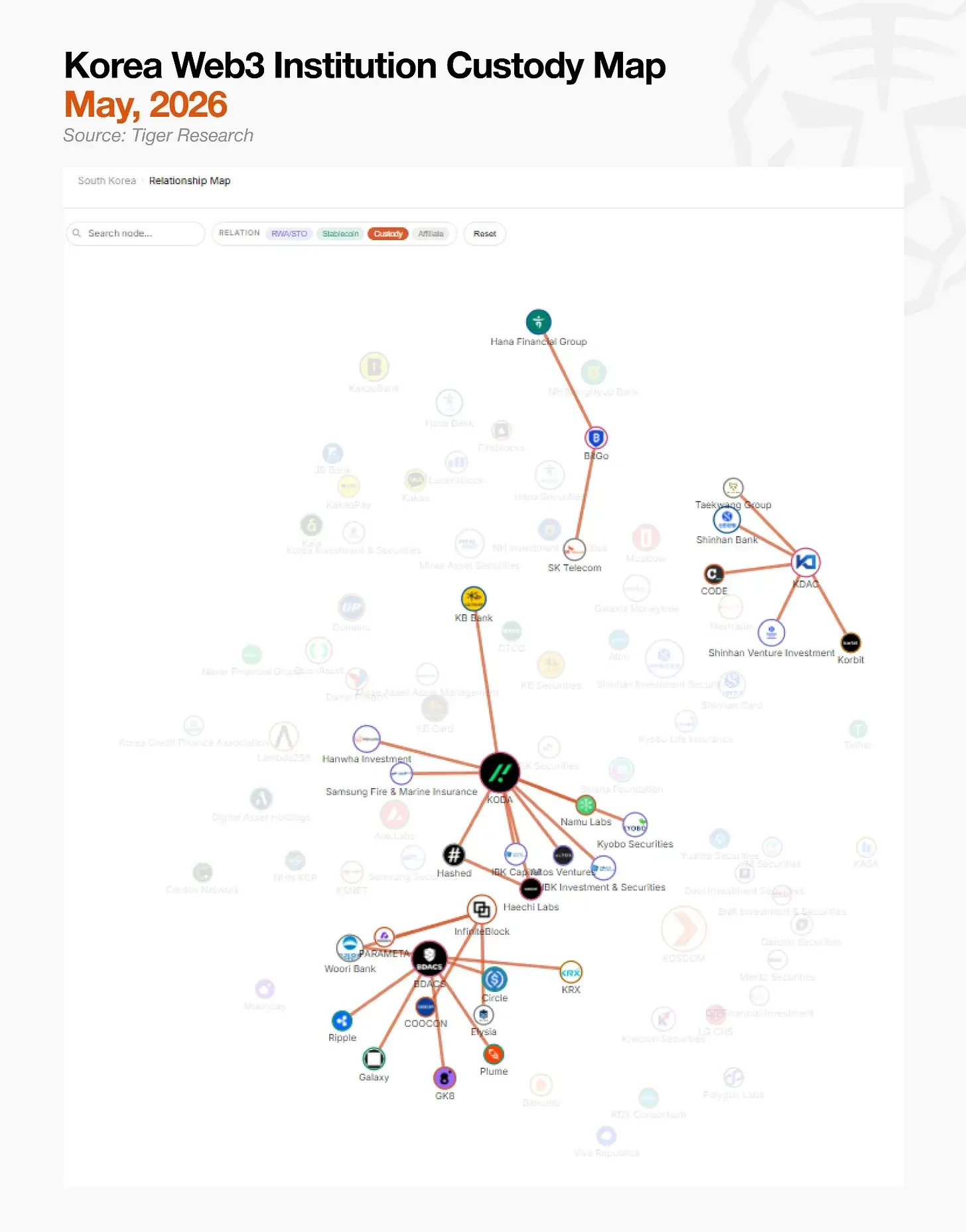

3.3. Custody: Need for More Institutional Capital

The custody market is structurally simpler than other sectors. The four major custodians have each secured domestic and international financial and technology partners to establish their market positions.

KODA, co-founded by KB Kookmin Bank, Hashed, and Haechi Labs, combines traditional financial capital with crypto-native VC. Hanwha Investment & Securities, IBK Capital, and Kyobo Securities subsequently joined as investors, and a dedicated custody insurance agreement with Samsung Fire & Marine Insurance further enhances its stability.

KDAC is a traditional finance-led custodian, with Shinhan Bank and NH Nonghyup Bank as major shareholders. NH Nonghyup Bank, initially an investor in another custodian, Kardo, became a KDAC shareholder post-merger. After the merger, KDAC's shareholder base includes two of Korea's top five banks.

BDACS has taken a unique approach centered on technology and partnership development. Expanding its custody and payment infrastructure through partnerships with Woori Bank and international digital asset infrastructure companies like Galaxy and GK8, it also signed an MOU with Circle to issue the KRW1 won stablecoin on Circle's Arc blockchain, and it is the sole VASP and key custody partner in the KRX-led KDX consortium. BDACS is currently conducting a proof of concept for KRW1, positioning itself as a custodian targeting both custody and payment infrastructure.

BitGo Korea entered the domestic market backed by the technological prowess of its global parent company. BitGo headquarters custodies over $70 billion in assets and handles approximately 20% of global Bitcoin on-chain transactions. Domestically, Hana Financial Group and SK Telecom each hold stakes, making it a custodian supported by financial and telecommunications capital.

Institutions have entered the market through their respective custody relationships. However, all major custodians reportedly recorded net losses last year, indicating they are building ahead of the institutional capital inflows needed to sustain operations.

Taken together, the infrastructure buildout across STOs, stablecoins, and custody reveals a clear common constraint: domestic institutions have constructed the business frameworks, but the underlying technical infrastructure still relies heavily on overseas solutions.

4. Infrastructure Builders

Reliance on overseas solutions carries structural costs: as the market grows, a significant portion of revenue will flow overseas in the form of technology licensing fees. If overseas partners change policies or raise costs, domestic infrastructure also faces disruption risks.

More fundamentally, areas requiring alignment with Korea's specific regulatory environment – such as Korean won stablecoin issuance, STO distribution rules, and domestic corporate account integration – cannot simply apply global solutions directly. This is precisely why, once relevant legislation is finalized and capital begins to flow seriously, domestic technology companies capable of directly designing and controlling the underlying rails according to the Korean regulatory framework will be indispensable.

Domestic companies that have already identified this technology gap and are building Korea-specific financial infrastructure are already in motion. The leading technology providers are as follows.

4.1. LG CNS

Among traditional IT service companies, LG CNS has the most distinct stance. Since launching its own blockchain platform "Monachain" in 2018, it has accumulated operational experience by providing services to over 220 local governments through the Korea Minting and Security Printing Corporation's local currency platform.

This permissioned chain experience translated into orders for CBDC and STO projects. As the main contractor for the Bank of Korea's CBDC project "Hangang," LG CNS is developing a government subsidy distribution system using deposit tokens. Through this process, it has built the system architecture capability to run institutional CBDCs and private digital currencies on a single network, effectively transplanting traditional financial security standards and procedures onto the blockchain.

Developing the KOSCOM joint STO issuance platform and Mirae Asset Securities' STO platform follows the same logic. Rather than issuing assets directly, LG CNS targets three directions: building issuance and distribution platforms for banks, providing SaaS to payment operators including credit card companies, payment gateways, and simple payment services, and developing digital asset payment platforms for securities firms. Once the regulatory framework is finalized, it appears to be the most likely candidate to secure the market for infrastructure contracts.

4.2. DSRV

Among blockchain infrastructure companies, DSRV stands out for directly assisting financial institutions in accessing on-chain infrastructure. As a validator and infrastructure company operating on over 70 blockchain networks, DSRV manages over KRW 4 trillion (approx. USD 2.9 billion) in assets, ranking first in Ethereum staking in Korea and among the top ten globally.

A key development is its expansion from node operations to full-stack institutional on-chain infrastructure. Through the DSRV Portal, financial institutions can access wallet, payment, tokenization, custody, and staking functions via API and dashboard interfaces. Without building their own node and security infrastructure, financial companies can integrate user wallets, institutional wallets, recurring payments, token issuance, burning, transfer and locking, custody, and staking capabilities.

Trust mechanisms are also in place. DSRV was the first to obtain VASP, ISMS, and SOC 1 Type 1 certifications, directly meeting the regulatory, security, and operational control requirements of financial institutions. In practice, this means the external infrastructure provider bears the wallet security, internal controls, and operational risks that financial companies find most burdensome when deploying on-chain services.

Its partnerships are oriented towards payment rail construction. DSRV is jointly developing remittance infrastructure compliant with Korean and Japanese regulations with SBI Ripple Asia. It is working with Circle to develop an institutional USDC issuance, redemption, and settlement framework that bypasses exchanges. It signed an agreement with BC Card for stablecoin payment infrastructure connecting traditional card payment networks to the blockchain.

DSRV recently completed a KRW 30 billion (approx. USD 21.7 million) Series B funding round to accelerate technology development.

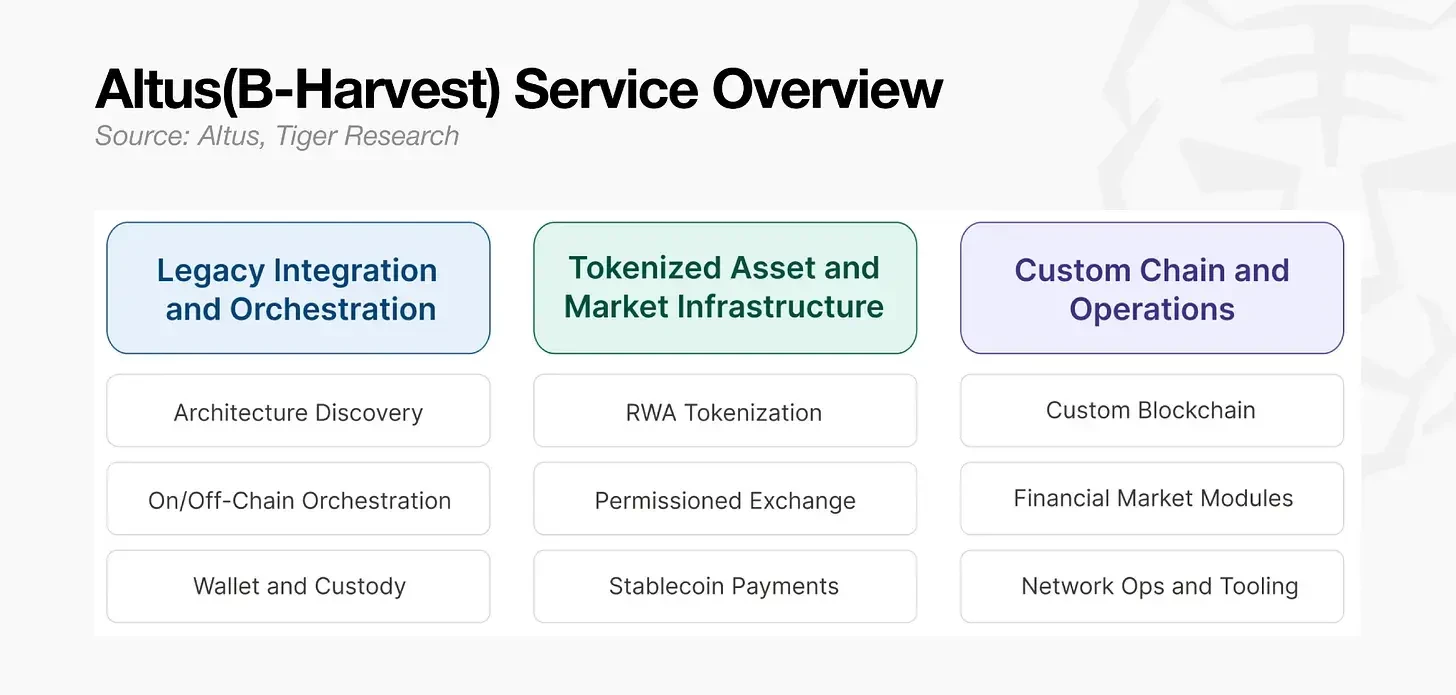

4.3. Altus (formerly B-Harvest)

Altus (formerly B-Harvest) operates in the integration layer between financial institutions' legacy systems and the blockchain environment. Founded in 2018, the company has contributed to the development of Cosmos SDK-based EVM chains and is an organization of over 40 engineers and researchers who have directly built multiple production networks including Canto, Crescent, Stable, and Ault.

Altus handles protocol engineering and core architecture for Ault Blockchain, an institutional L1 focused on RWA, trading, and payments. In 2025, it contributed EVM integration, performance improvements, and security audits for the Bitcoin staking L1 Babylon, supporting its production readiness.

Its financial institution solutions stem from the same layer. Altus built from scratch according to financial industry requirements: an on-chain/off-chain orchestration layer connecting legacy systems and blockchain execution environments, RWA tokenization, permissioned exchanges, stablecoin payment and settlement, and institutional wallet and custody infrastructure.

Current internal R&D proceeds in parallel: the Canton Network architecture supporting selective data disclosure between institutions, and