We're scrambling for equity and competing in infrastructure—South Korea’s crypto institutions are in a full-blown melee.

- Core Viewpoint: South Korean financial institutions are accelerating their push into the crypto market through partnership signings and exchange equity acquisitions, but most projects remain in the preliminary stage, with a low rate of actual implementation. The strategic focus of institutions has shifted from competing for retail investors to seizing the high ground in infrastructure such as stablecoins, STOs, and custody services, thereby influencing the formulation of future regulatory frameworks.

- Key Elements:

- Low Partnership Implementation Rate: According to a study by Tiger Research, of the 196 collaborations involving 150 institutions, most are still in the letter of intent stage, with very few actual commercial projects materializing.

- Exchange Equity Scramble: Giants like Hana Bank, Hanwha Investment & Securities, and Samsung are aggressively acquiring stakes in exchanges such as Upbit and Korbit, aiming to control the gateway for digital financial traffic.

- Uneven Track Development: Asset custody has seen the most implementation, while RWA/STO and stablecoins are progressing slowly due to regulatory lags. Corporations are either allying with local partners or turning to overseas markets.

- Rise of Local Infrastructure: Companies like LG CNS, DSRV, and Altus are focusing on building South Korea-specific financial infrastructure, reducing reliance on overseas technology and becoming core pillars for institutions.

- Shift in Market Focus: With retail trading volume declining by about 48% year-over-year, the market is transitioning from being retail-driven to institution-driven. Overseas public chain strategies are also pivoting toward partnerships with local financial giants.

Original Authors: Henry Kim, Ryan Yoon

Original Compiled by: Chopper, Foresight News

South Korean financial institutions are accelerating their partnerships and equity acquisitions in the crypto space, but the industry landscape remains complex. While various cooperation agreements are frequently announced, few commercial projects have actually materialized. This article will analyze the reasons behind the low implementation rate of these collaborations and why institutions continue to increase their布局.

TL;DR

- Institutional crypto businesses in Korea have moved from the letter of intent stage to substantive operations and exchange equity acquisitions.

- Major institutions are vying for control over key financial infrastructure, including security token offering (STO) standard-setting, stablecoin payment channels, and the asset custody market.

- Local infrastructure service providers are emerging as core pillars for institutional businesses. Companies are building proprietary technological chains based on the Bank of Korea's central bank digital currency (CBDC) framework and local regulations, reducing dependence on overseas technology.

- The Korea strategy of overseas Web3 public chain foundations has completely shifted. Traditional finance is gradually dominating the market, with overseas institutions no longer focusing on retail community operations but seeking partnerships with large corporations and financial institutions.

Proliferation of Letters of Intent: The Industry Enters a "Signing Contest"

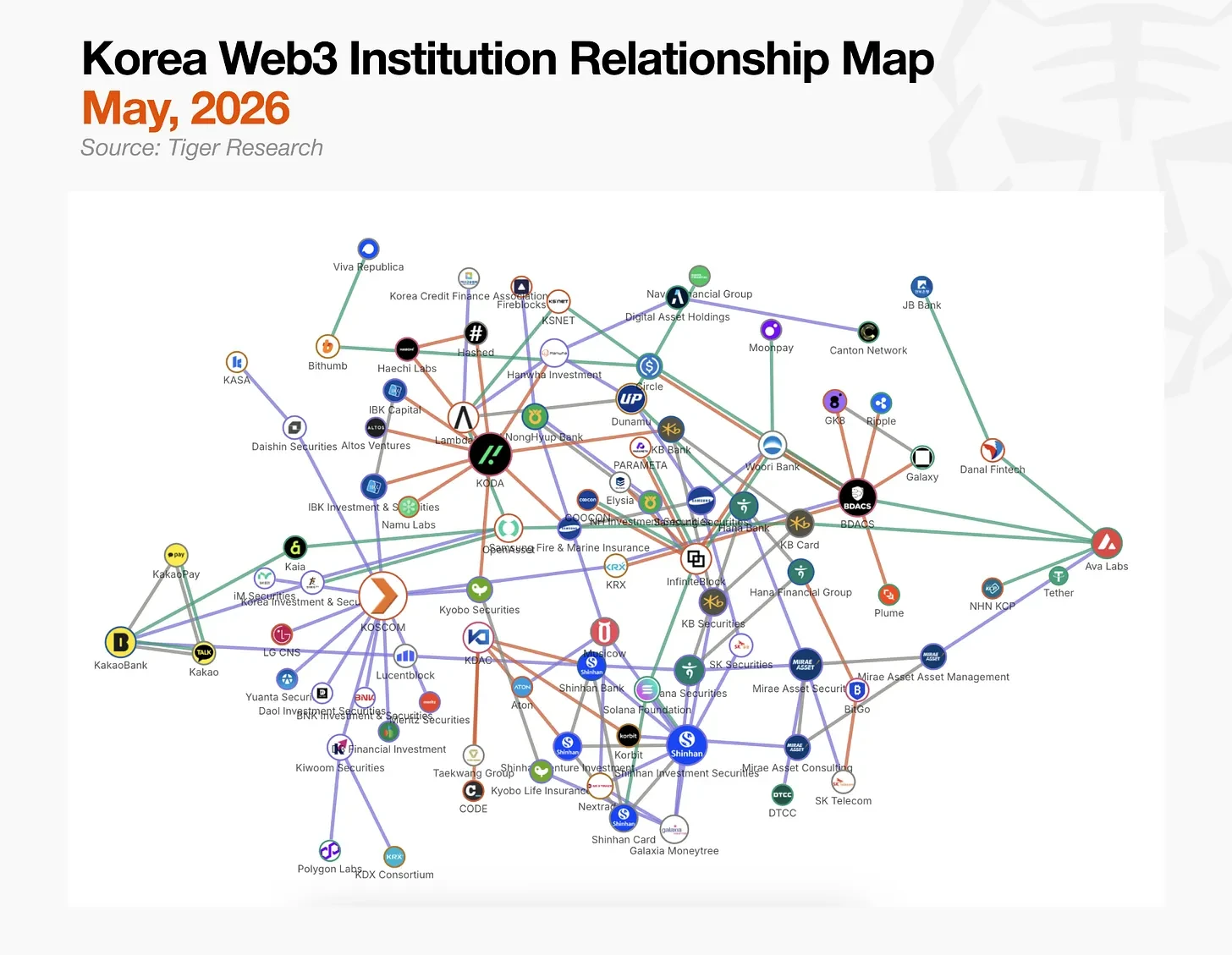

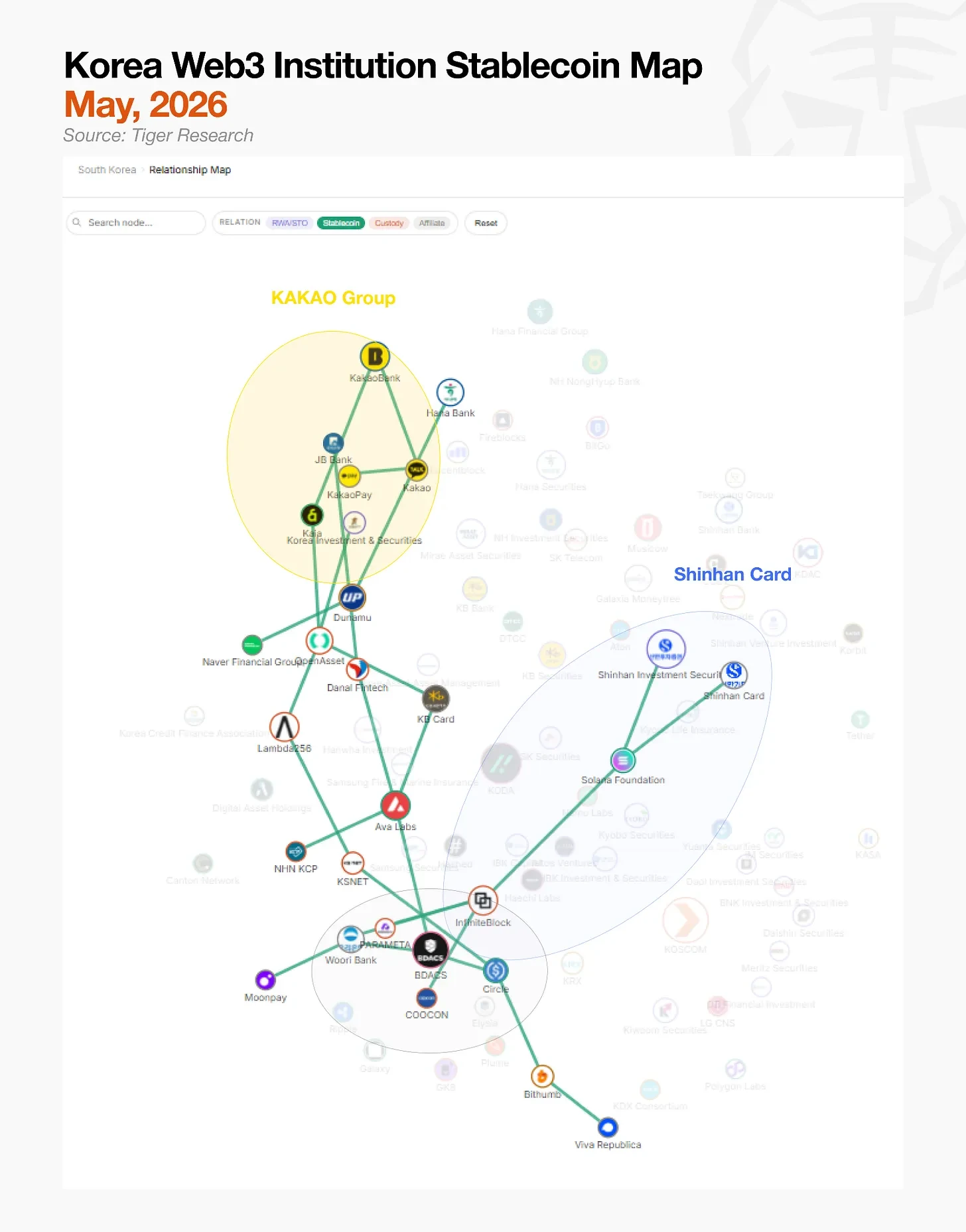

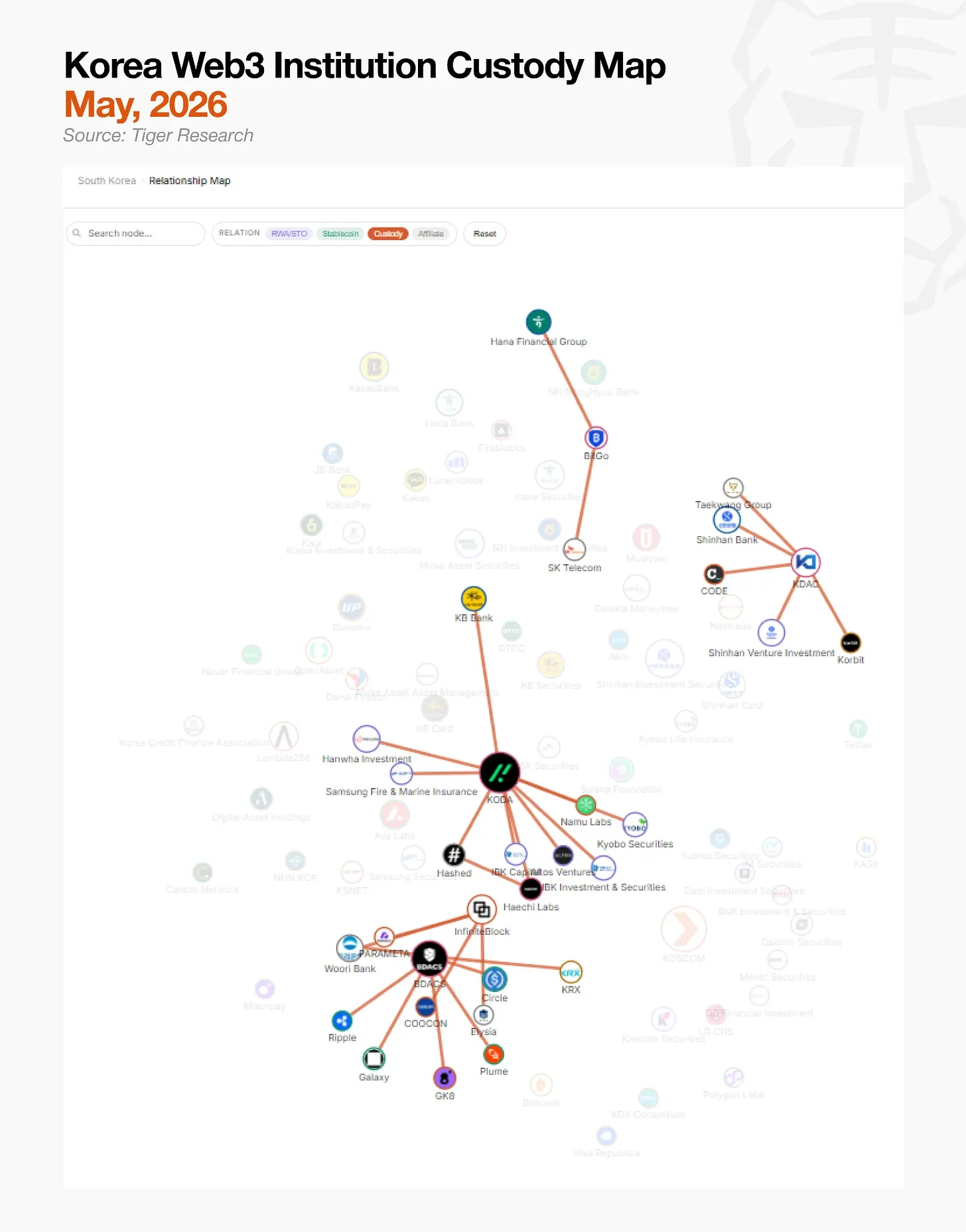

The above image, compiled by Tiger Research, maps the partnership networks of various institutions in Korea's crypto market. The entire landscape is deeply interwoven, making it difficult for outsiders to distinguish which collaborations are operational and which remain at the intent stage. The boundary between core industry players and peripheral participants is also very blurred.

This complex landscape accurately reflects the current state of Korea's institutional crypto market. Tiger Research analyzed 150 institutions and 196 collaboration cases, finding that no single entity has achieved absolute dominance.

Before relevant regulations are formally enacted, local Korean institutions are racing to establish their positions and secure market sectors. The current competition is primarily concentrated in three areas: stablecoins, security token offerings (STOs), and crypto asset custody.

Another notable trend is the intensive acquisition of crypto exchange equity by financial institutions. Industry insiders view this as institutions seizing market positions ahead of regulatory clarity and signaling long-term bullish sentiment.

The Battle for Exchange Equity Intensifies

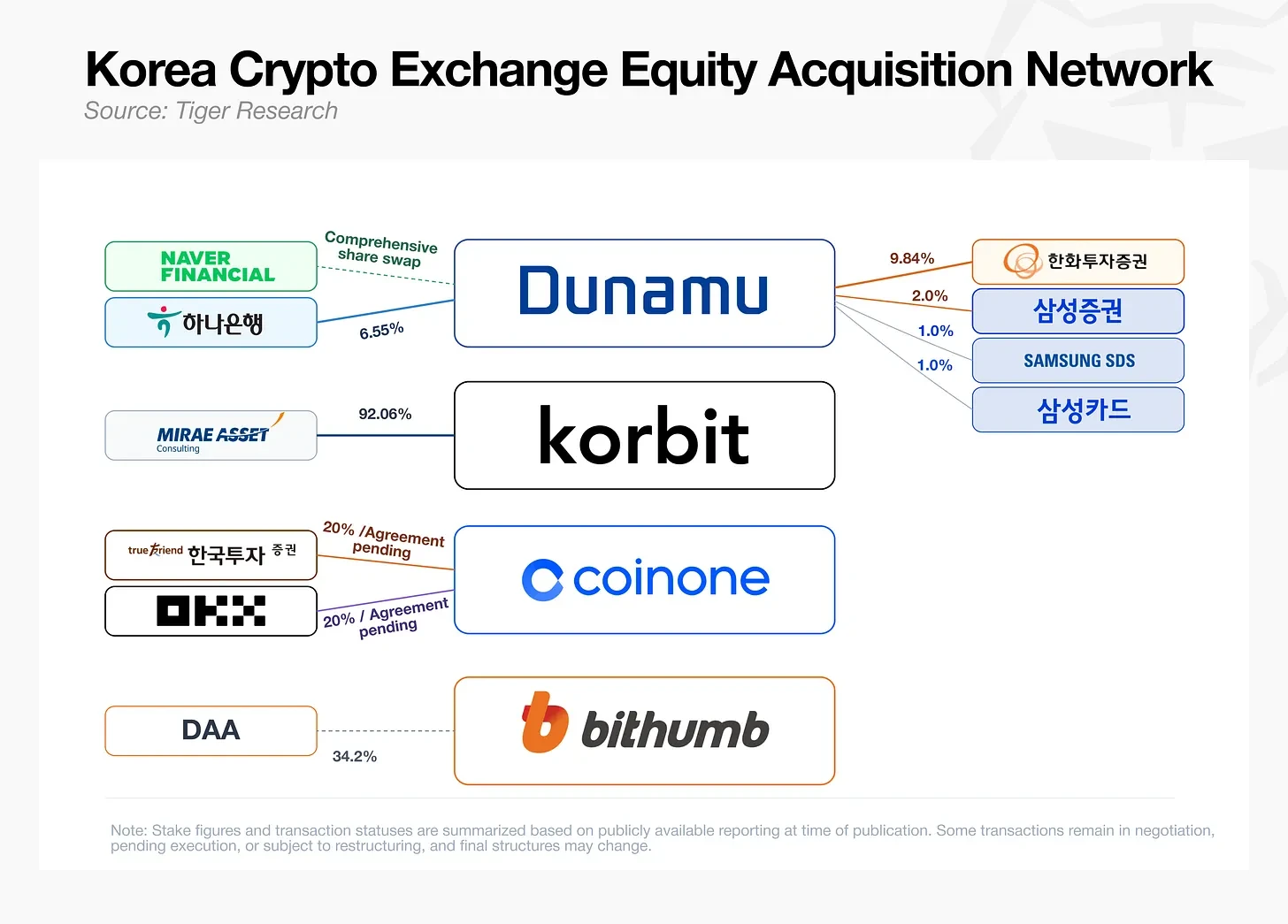

Hana Bank announced it would spend approximately 1 trillion Korean won (about $720 million) to acquire a 6.55% stake in Dunamu, the operator of Upbit. Just ten days later, Hanwha Investment & Securities received approval to increase its stake by an additional 3.90%. On the 28th of the same month, Samsung Securities, Samsung SDS, and Samsung Card jointly acquired a 4.0% stake in the platform.

Mirae Asset Consulting signed an agreement back in February to acquire a 92.06% stake in Korbit exchange. There are also reports that Korea Investment & Securities is in talks with global exchange OKX to jointly acquire Coinone.

The valuation logic for crypto exchanges in capital markets has changed. Exchanges are no longer just platforms for earning transaction fees; they are becoming core traffic gateways for distributing stablecoins, custody services, security tokens, and real-world asset tokenization (RWA) products.

By holding equity in exchanges, banks and brokerages can indirectly acquire relevant Virtual Asset Service Provider (VASP) qualifications while gaining firm control over the platform's user base and liquidity. This equity battle is fundamentally a contest for control over digital financial front-end traffic and distribution channels.

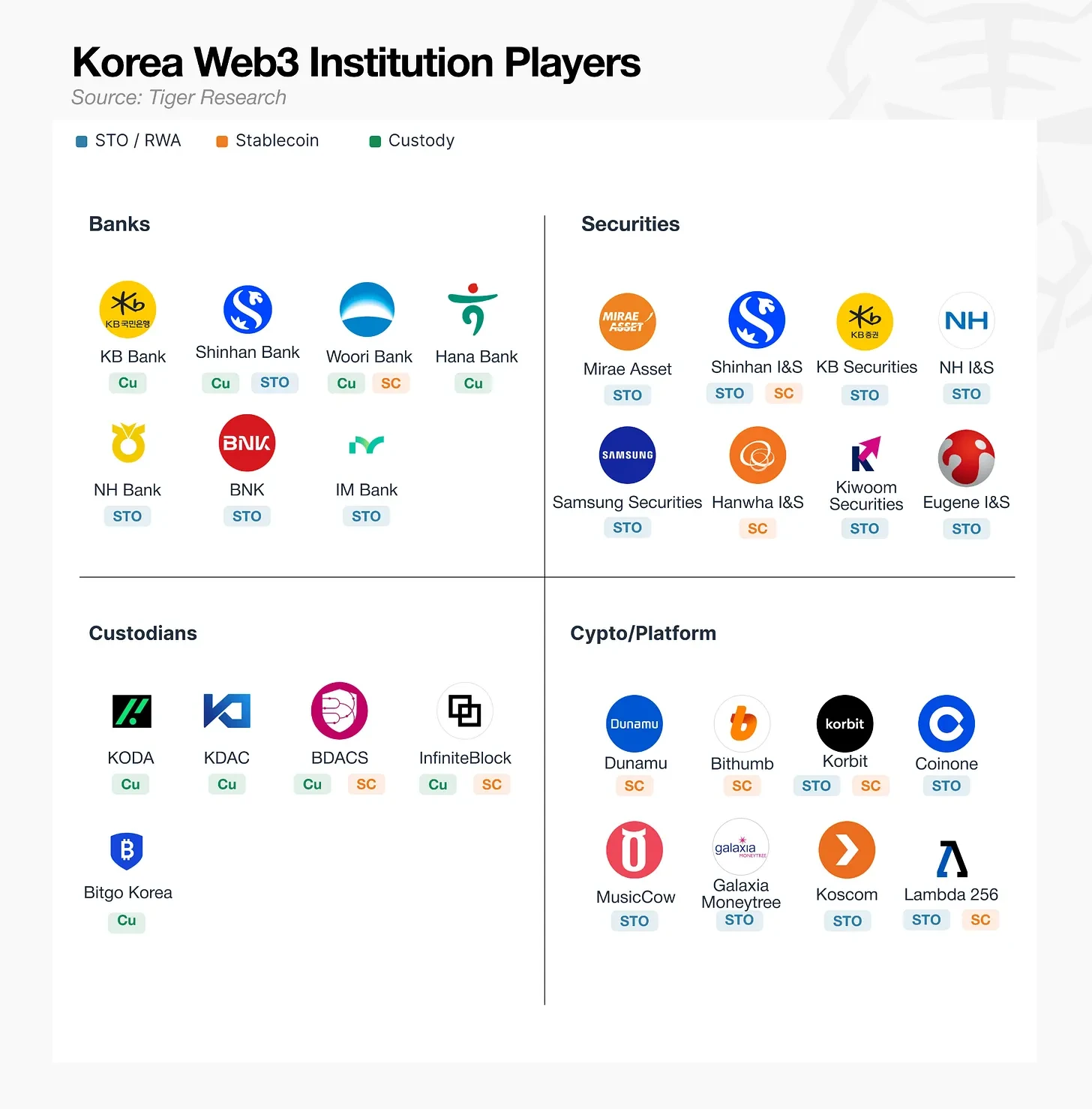

Current State of Korea's Crypto Sub-Sectors

From the partnership network, it is clear that the development progress of various crypto sub-sectors is uneven. The asset custody sector has the most implemented projects, with several players having overcome regulatory hurdles and officially launched services. The RWA/STO sector mostly remains at the signing or intent stage, awaiting supporting legislation. The stablecoin sector is also progressing slowly, with no company yet establishing industry standards or leading the market.

The development obstacles differ for each sub-sector, leading to divergent strategies among institutions. Some companies are partnering with local allies and waiting for regulatory easing, while others are pivoting to more mature overseas markets. The following sections analyze the bottlenecks and player strategies for each sector.

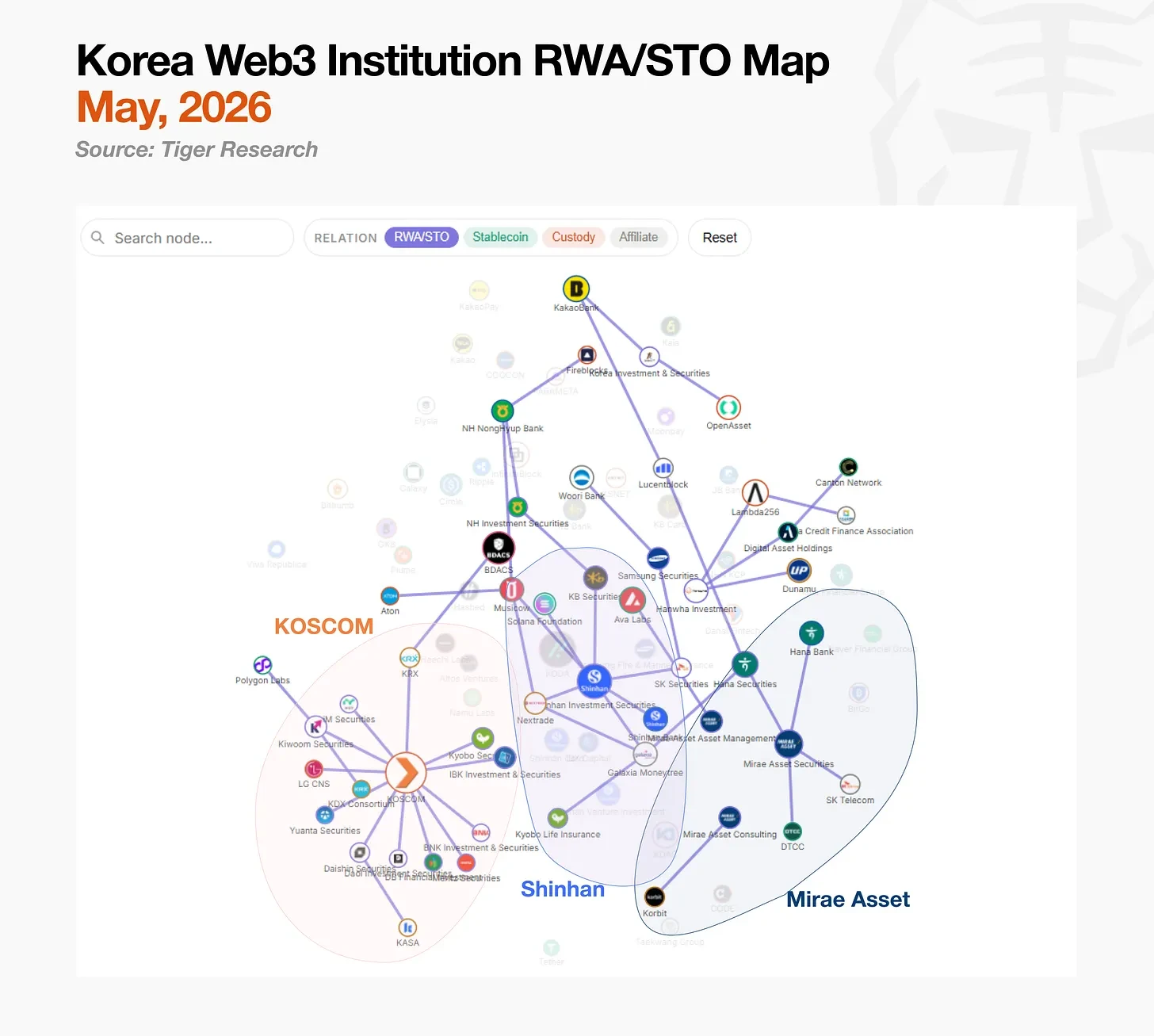

Real World Assets / Security Token Offerings (RWA/STO): Legislation Enacted, Commercial Infrastructure Remains Biggest Shortcoming

Korea's local STO market has split into two main camps: the alliance led by the Korea Securities Computing Corporation (KOSCOM) and the fractional investment alliance led by Shinhan Investment & Securities. Mirae Asset Securities is taking a different path, bypassing local infrastructure development and directly expanding into overseas markets.

KOSCOM, in which the Korea Exchange holds a 76.6% stake, is the operator of Korea's core financial network. Its positioning is to build neutral, shared infrastructure serving all securities firms. Instead of signing exclusive agreements with single issuers, it has onboarded 11 securities firms to its platform. Its goal is to standardize STO issuance and circulation technology and connect with the centralized custody system of the Korea Securities Depository.

Shinhan Investment & Securities has rapidly built its own STO ecosystem. It completed a proof of concept with Lambda 256 in 2022, launched the integrated platform PULSE in 2024, and introduced a multi-platform account aggregation service in 2025. In 2025 alone, it participated as an account manager in 10 investment contract-type security token issuances and acquired a controlling stake in the OTC exchange NXT, establishing a channel from token issuance to circulation.

Mirae Asset Securities is entirely bypassing local infrastructure to focus on overseas expansion. The firm has issued digital bonds in Hong Kong, obtained a virtual asset retail license from the Hong Kong Securities and Futures Commission, and plans to launch a smart trading system for local retail investors in June. In the US, it is the only Korean securities firm to join the Depository Trust & Clearing Corporation (DTCC) tokenization working group, participating in global standard-setting alongside institutions like JPMorgan, Goldman Sachs, and BlackRock. This布局 will give it a compliance and negotiation advantage when Korea's future STO system aligns with global standards.

Stablecoins: Technology Mature, Regulation is the Key Barrier

The stablecoin sector features the most diverse participants, including credit card companies, exchanges, fintech firms, and infrastructure providers, each leveraging their strengths to enter the market.

The Kakao Group represents the largest camp. Kakao, KakaoBank, and Kakao Pay have formed a joint task force aimed at creating a "super wallet" encompassing stablecoins, cryptocurrencies, and local currencies. The team's core advantage stems from the infrastructure capabilities accumulated through years of operating the Kaia public chain, which has already launched USDT and is conducting real-world payment tests.

Shinhan Card is migrating its existing payment network to a blockchain platform. The firm signed a letter of intent with Solana in April this year, but related technology R&D had already been implemented earlier. It previously completed proofs of concept with Solana, Visa, Mastercard, and Fireblocks, and is now conducting in-depth testing across six modules, including wallets and smart contracts.

Due to regulatory delays for Korean won stablecoins, the exchange camp is prioritizing the U.S. dollar stablecoin track. Dunamu, in partnership with Naver Financial, is developing Korean won stablecoin business based on its proprietary GIWA public chain. Bithumb has paused Korean won stablecoin efforts, first partnering with Circle and WLF to build a USD stablecoin distribution network. It is also in talks with payment platform Toss regarding a joint Korean won stablecoin issuance, but overall progress is slow.

Despite frequent moves by various camps, they are all constrained by the same regulatory hurdle. The Bank of Korea proposed a 51% ownership rule, requiring that the issuing entity for a Korean won stablecoin be a consortium where a bank holds a majority stake. Fintech companies have objected to this proposal, and the resulting tug-of-war has prevented the government from finalizing issuance details. Whichever camp holds the most extensive front-end traffic channels is likely to dominate the market once formal rules are established.

Asset Custody: Business Launched, but Still Needs Institutional Capital Inflows

Compared to other sectors, the custody market landscape is clearer. The four major custody institutions have all solidified their market positions by partnering with domestic and international financial and tech partners.

KODA was co-founded by KB Kookmin Bank, crypto venture capital firm Hashed, and Haechi Labs. Subsequently, Hanwha Investment & Securities, IBK Capital, and Kyobo Securities acquired stakes. KODA has also signed an exclusive custody insurance agreement with Samsung Fire & Marine Insurance, providing a robust risk control system.

KDAC is a traditional finance-led custodian, with Shinhan Bank and NongHyup Bank as its two major shareholders. NongHyup Bank had previously invested in another custodian, Kardo; after a merger, it was formally integrated into KDAC. Two of Korea's top five banks are now among its shareholders.

BDACS focuses on technology and ecosystem partnerships, collaborating with domestic and international institutions like Woori Bank, Galaxy, and GK8 to expand custody and payment infrastructure. It also partnered with Circle to issue the Korean won stablecoin KRW1 based on Circle's Arc public chain, which is currently undergoing proof of concept. BDACS is also the designated VASP and core custody partner for the KDX alliance led by the Korea Exchange (KRX), simultaneously developing custody and payment businesses.

BitGo Korea entered the market leveraging its parent company's global technology. Its headquarters custodies over $70 billion in assets and handles approximately 20% of global Bitcoin on-chain transactions. With shareholdings from Hana Financial Group and SK Telecom, BitGo Korea benefits from both financial and telecommunications capital backgrounds.

Numerous financial institutions conduct business through these custodians. However, reports indicate that all four major custodians were operating at a loss last year. This suggests that while the industry infrastructure has been built in advance, it has yet to attract the large-scale institutional capital inflows needed to sustain operations.

Looking across the STO, stablecoin, and custody sectors, a common issue emerges: while Korean local institutions have built a complete business framework, the underlying technology remains highly dependent on overseas solutions.

The Rise of Local Infrastructure Service Providers

Long-term reliance on overseas technology creates structural risks. As the industry scales, a significant portion of revenue will flow overseas in the form of technology licensing fees. Furthermore, if overseas partners adjust policies or raise fees, local businesses could face vulnerabilities.

A deeper contradiction lies in the fact that scenarios like Korean won stablecoin issuance, STO circulation rules, and local enterprise account connectivity require deep alignment with Korean regulatory requirements, making it impossible to directly apply global solutions. Consequently, once relevant legislation is enacted and capital flows in on a large scale, local tech companies capable of independently designing and controlling the underlying technology chain will become essential.

A cohort of local companies has already identified this technological gap and is focusing on developing Korea-specific financial infrastructure. Key players include:

LG CNS

Among traditional IT service providers, LG CNS has the most prominent layout. The company launched its proprietary blockchain platform, Monachain, in 2018. Leveraging local currency services from the Korea Minting and Security Printing Corporation, it provides on-chain services to over 220 local governments, accumulating substantial operational experience.

Building on this technical expertise, LG CNS has secured key projects, including the Bank of Korea's CBDC project, Hangang, and various STO-related projects. As the general contractor for the central bank's CBDC project, it is responsible for building a government subsidy distribution system based on deposit tokens, enabling institutional CBDC and private digital assets to operate on the same network and migrating traditional finance security standards and processes entirely onto the blockchain.

Additionally, the company has undertaken the development of STO platforms for KOSCOM and Mirae Asset Securities. Its business布局 focuses on three main directions: building token issuance and circulation platforms for banks, providing software services for credit card companies and payment processors, and creating digital asset payment platforms for securities firms. Once regulations are in place, LG CNS is well-positioned to be a key winner in the local infrastructure market.

DSRV

DSRV is a leading blockchain infrastructure service provider. Its operations cover over 70 public chains, with over 4 trillion Korean won (approximately $2.9 billion) in assets under its custody. It ranks first in Korea and among the top ten globally for Ethereum staking volume.

The company has evolved from a pure node operator into a comprehensive one-stop institutional on-chain infrastructure service provider. Its DSRV portal allows financial institutions to access wallet, payment, asset tokenization, custody, and staking functions via APIs and data dashboards. Financial institutions can quickly launch retail wallets, institutional wallets, auto-payments, token issuance/burning/transfer/locking, asset custody, and staking services without needing to build their own nodes and security systems.

DSRV has obtained VASP, Information Security Management System (ISMS), and SOC 1 Type 1 certifications, directly addressing financial institutions' core requirements for compliance, security, and risk control. It handles aspects that financial institutions are reluctant to manage themselves, such as wallet security, internal controls, and operational risks.

Its partnership strategy focuses on cross-border and on-chain payment rails: collaborating with SBI Ripple Asia to develop compliant cross-border remittance infrastructure between Korea and Japan; partnering with Circle to build an institutional-grade USDC issuance, redemption, and settlement system independent of exchanges; and working with BC Card to bridge traditional credit card networks and stablecoin payment channels. The company recently completed a ₩30 billion (approximately $21.7 million) Series B funding round to accelerate technological iterations.

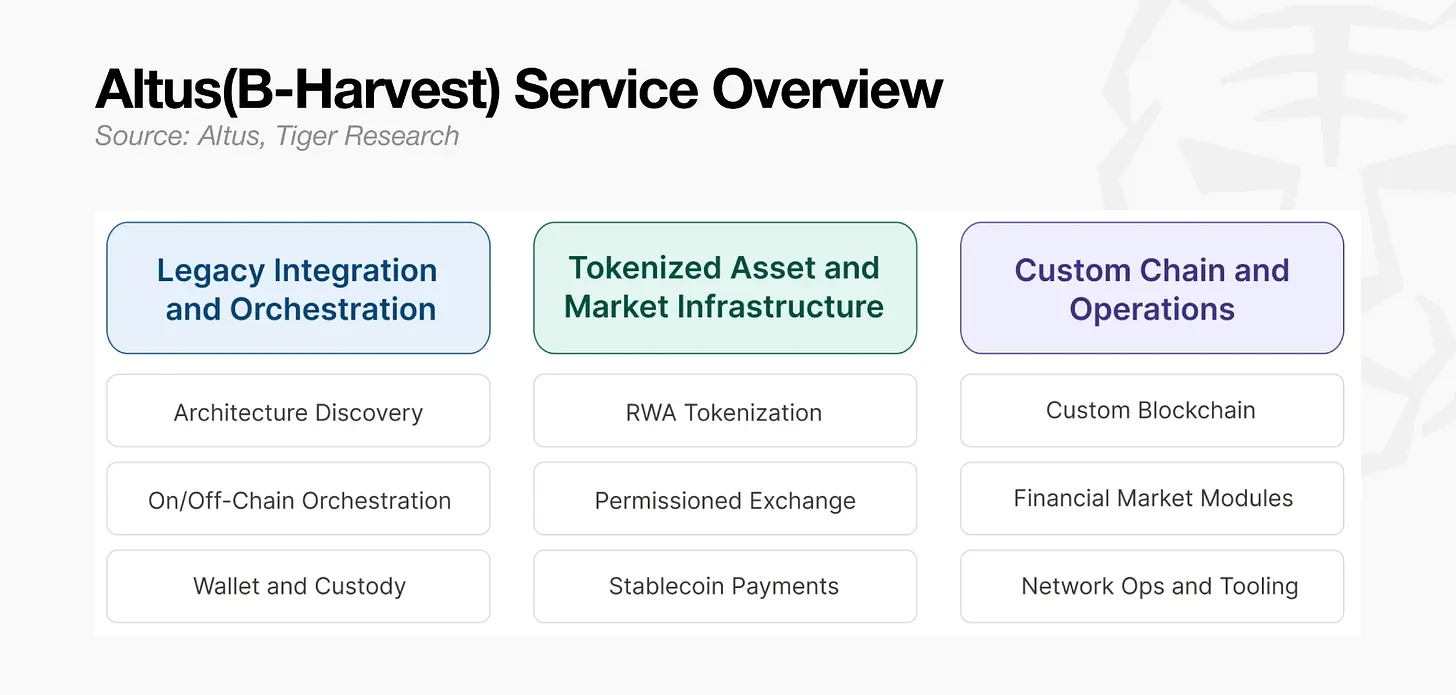

Altus (formerly B-Harvest)

Altus specializes in the integration layer between legacy traditional finance systems and blockchain. Founded in 2018, the team comprises over 40 engineers and researchers and has been deeply involved in developing EVM-compatible public chains based on the Cosmos SDK, leading the development of multiple commercial public chains such as Canto, Crescent, Stable, and Ault.

The company provides protocol development and underlying architecture design for Ault, an institutional-grade public chain focused on real-world assets, trading, and payments. It also completed EVM adaptation, performance optimization, and security audits for the Bitcoin staking project Babylon, ensuring its successful mainnet launch.

For financial institutions, Altus builds solutions tailored to their needs from the ground up, including cross-chain orchestration layers connecting legacy systems and blockchains, real-world asset tokenization frameworks, permissioned exchanges, stablecoin payment and settlement systems, and institutional wallet and custody infrastructure.

Currently, two major R&D projects are progressing in parallel: the Canton network architecture supporting selective data disclosure between institutions, and the Commonware Stack, a modular blockchain framework targeting a throughput of 1 million transactions per second.

Each of these three companies has its strengths. LG CNS leverages its reputation in traditional financial IT, DSRV relies on its node and staking infrastructure, and Altus specializes in customizing underlying protocols. However, their goal is highly consistent — to secure control over core underlying systems before large-scale institutional capital enters the market. The ultimate outcome will depend on the commercial implementation experience each accumulates before the market fully opens.

Retail Exit, Institutions Take the Lead

The recent flurry of partnership signings is not merely business development; it is a strategic positioning move by institutions ahead of regulatory clarity, even an attempt to influence the final regulatory framework. The current signing contest is less about capturing market share and more about shaping the regulatory landscape.

In just six months, Korea's crypto market landscape has been completely reshaped: custody camps have formed, STO alliances have emerged, and major financial holding companies have acquired exchange equity. Concurrently, retail trading enthusiasm has cooled significantly, with total trading volumes across Korea's top five mainstream exchanges declining by approximately 48% year-on-year. The market's center of gravity is rapidly shifting from retail to institutions.

This market transformation has also rewritten the localization strategies of overseas Web3 public chain foundations. Shinhan Card's choice of Solana and Mirae Asset Securities' partnership with Avalanche are just two examples of a growing trend. Overseas institutions are no longer relying on offline community events to attract retail investors. Instead, they are shifting their focus to connecting with local financial giants and large corporations. The traditional model of community management is no longer effective.

Korea Blockchain Week (KBW 2026), scheduled for September in Seoul, may vividly demonstrate the results of this industry transformation. Judging from the announced guest list, traditional finance figures have become