Six Titans in a Battle of Gods: A Panorama of 13F U.S. Stock Holdings – Top Institutions Starting to Take Opposite Sides?

- Core Thesis: The Q1 2026 13F filings of top-tier U.S. stock institutions reveal that Wall Street's consensus on AI investment has fractured, shifting from collective buying to intense internal divergence. Institutions are no longer investing in "AI" broadly but are instead pricing platform, application, and hardware layers separately based on different assumptions, forming a clear pattern of opposing bets.

- Key Elements:

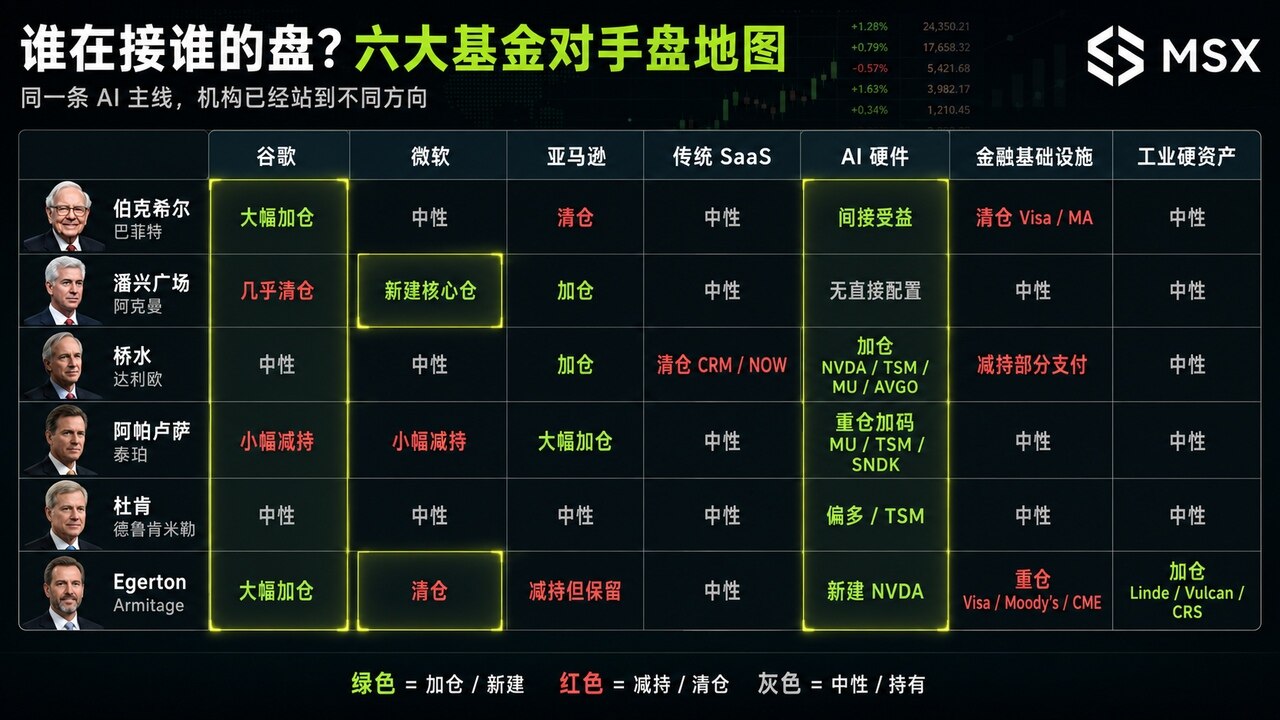

- Google (Alphabet) becomes the prime example of divergence: Berkshire Hathaway significantly increased its position, betting on cash flow and undervaluation recovery; Bill Ackman's Pershing Square nearly exited, fearing generative AI would disrupt the search business model.

- AI trading moves from "generalization" to "stratification": Institutional holdings diverge into three main tracks — the platform layer (Microsoft, Google), the application layer (Salesforce sold off), and the hardware & infrastructure layer (NVIDIA, TSMC heavily bought).

- Traditional SaaS (e.g., Salesforce) faced significant liquidation by Bridgewater Associates, while AI hardware (NVIDIA, TSMC) saw increased holdings, reflecting a structural shift from "software middlemen" to "AI hard assets."

- Microsoft also shows clear divergence: Ackman built a new position, betting on Azure and enterprise AI; Egerton Capital liquidated its Microsoft holdings, believing its AI premium has been exhausted.

- Berkshire Hathaway liquidated its positions in Amazon and Visa while adding to Google, reflecting a trend of streamlining portfolios and adhering strictly to valuation discipline in a high-market environment, rather than holding the same assets long-term.

In Q1 2026, the results of the top six fund managers' portfolio adjustments are out.

As is well known, mid-May each year is one of the most noteworthy time windows for the global US stock market. At this point, major institutions must submit their 13F filings to the U.S. Securities and Exchange Commission (SEC), disclosing their holdings at the end of the previous quarter. Although 13F filings themselves have a lag, typically submitted within 45 days after the quarter ends, making them unsuitable for "real-time copy trading," they are extremely valuable for observing how institutional money reassessed the market's main narrative in the previous quarter.

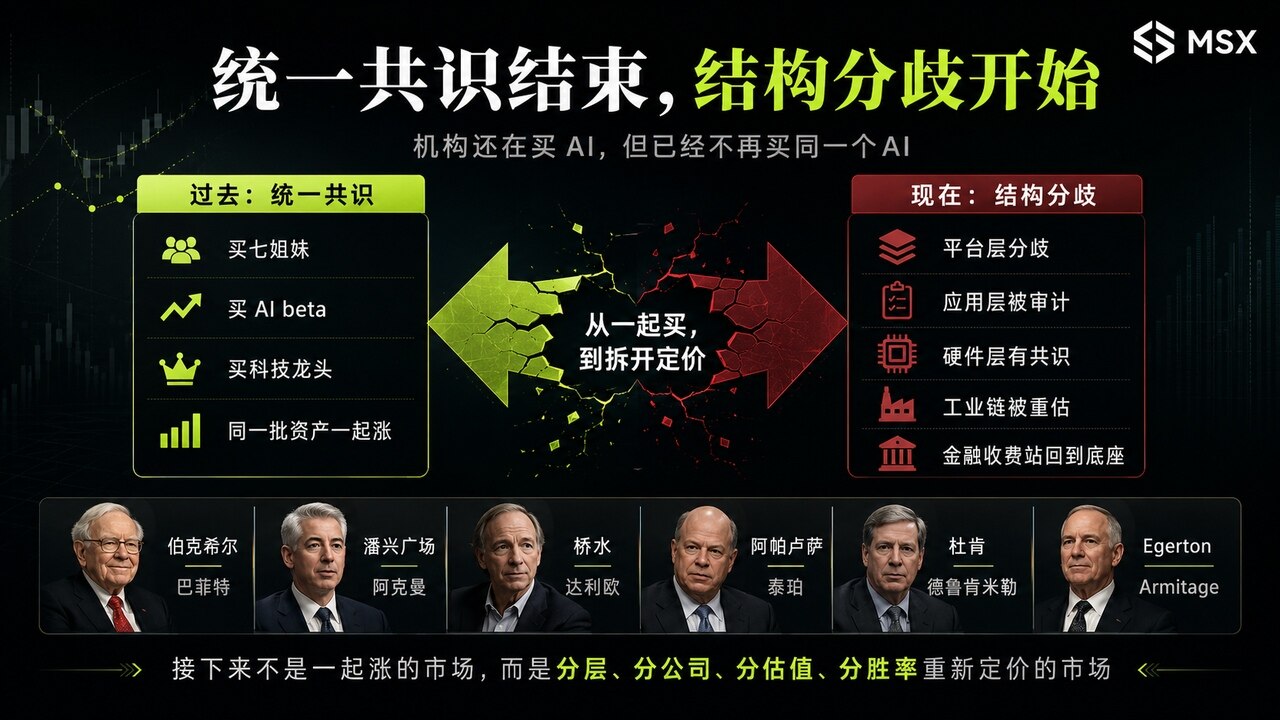

And for the Q1 2026 13F filings, the most significant change isn't which stock was bought by whom, nor which big-name investor liquidated something. Instead, it's that the consensus among Wall Street's top capital is beginning to fracture.

In the past few years, the US stock market had a very clear, shared narrative: buy the Magnificent Seven, buy AI, buy platform leaders, buy high-quality tech. Although capital flow had a sequence, it was largely moving in the same direction. But this time is different – with Google, some are crazily adding to their positions while others are nearly liquidating; with Amazon, some have completely sold out while others continue to hold heavy positions; with Microsoft, some have established new core positions while others have directly cleared them out. Traditional SaaS was massively liquidated by Bridgewater, but AI hardware and computing infrastructure were heavily bought by another group of funds.

This indicates that their judgments on "which layer AI money will ultimately flow to," "which company's moat will be reassessed by AI," and "which valuation has already overextended its future" are beginning to diverge significantly.

Therefore, this 13F filing season isn't just a simple list of holdings; it's more like a map of Wall Street's opposing trades.

1. The Core Change: Consensus Shifted from 'What to Buy' to 'Who is Dumping on Whom'

The most noteworthy trend in this 13F season is that institutions have begun to act as counterparties to each other within AI stocks themselves.

In the past, institutional trading in US stocks was more like a large river, with everyone heading in a similar direction, just differing in position size and timing. Now, it's more like a fork in the road. Everyone knows AI is the main theme, but no one is willing to pay the same valuation for the same story anymore:

- Some buy Google because it's cheap, has strong cash flow, and YouTube and Search still have moats; others sell Google because AI search might directly puncture its core business model.

- Some buy Microsoft because Azure and the enterprise AI entry point have higher certainty; others clear out Microsoft because the market has already given it an excessive AI premium.

- Some buy Amazon because AWS remains the core platform for AI cloud capital expenditure; others sell Amazon because their portfolio no longer needs to bear the risk of such highly-valued platforms.

- Some flee from Salesforce and ServiceNow because the intermediary value of traditional SaaS is being compressed by AI; others buy NVIDIA, TSMC, Micron, and SanDisk because, no matter which AI application wins, the underlying hardware must be purchased first.

So, the core of this 13F season is not "buying AI."

Rather, it's that AI as a unified concept is disintegrating. Institutions are starting to break it down into platform layers, application layers, hardware layers, industrial capex layers, and financial tollbooth layers, and repricing them.

Let's break down each one in detail.

1. Berkshire Hathaway: Redrawing the Lines in the Post-Buffett Era

Objectively speaking, Q1 2026 is the first complete observation window for Berkshire Hathaway entering the post-Buffett era.

The most interesting part of this 13F is that it did two seemingly contradictory things simultaneously: drastically streamlined the portfolio while heavily increasing its stake in Google.

According to public reports, Berkshire significantly increased its Alphabet position in Q1, while establishing new positions in Delta Air Lines and Macy's, and liquidating holdings in Amazon, Visa, Mastercard, UnitedHealth, and others:

- Liquidating Amazon, Visa, and Mastercard indicates it doesn't want to continue holding all previously seemingly high-quality business models.

- Increasing its stake in Google represents that it hasn't moved away from technology, but is searching within tech for assets closer to Berkshire's traditional aesthetic: strong cash flow, not expensive valuations, enough controversy, but whose underlying business hasn't been completely invalidated.

This is why Google became the biggest point of divergence in this 13F season. Berkshire isn't buying an "AI story"; it's buying a cash flow giant that the market is re-questioning, betting that "Google's moat still has value."

2. Pershing Square: Ackman Takes the Opposite Side of Buffett

If Berkshire was one of the largest buyers of Google this quarter, then Ackman is the quintessential counterparty.

Pershing Square's most stunning move in Q1 was nearly liquidating its Alphabet position and establishing a new position in Microsoft. Ackman explained publicly that Microsoft's valuation became more attractive after its share price pullback, and the long-term growth potential of Azure, Microsoft 365, and enterprise AI remains strong. In other words, he switched his tech exposure from Google to Microsoft.

This forms a stark contrast with Berkshire. Ultimately, Berkshire sees the resilience of Google Search, YouTube, Cloud, and advertising cash flows, while Ackman sees the disruptive risk that generative AI poses to the search entry point.

One thinks Google is undervalued; the other thinks Google's moat is being repriced. To put it bluntly, Ackman hasn't given up on AI; he just believes Google isn't the highest probability bet in this AI trade.

3. Bridgewater Associates: Dalio Sells Software, Buys Hardware

Bridgewater's 13F is always complex, as it's not about judging individual companies but making macro allocations.

But this time, Bridgewater's direction is very clear: sell traditional software, buy AI hardware.

Public 13F tracking shows Bridgewater exited Salesforce in Q1 and clearly rotated towards AI hardware and infrastructure names like NVIDIA, TSMC, and Amazon. Some market reports also mention TSMC as one of Bridgewater's important new positions this quarter, while Salesforce was a primary exit. This line is very important.

It shows Bridgewater isn't simply bullish on tech, but is performing a supply chain rotation *within* tech. For the past decade, traditional SaaS was one of the most comfortable business models: subscription revenue, customer stickiness, high margins, beautiful cash flow. But with the advent of AI, the valuation logic for traditional SaaS is being reassessed.

If large language models can automatically generate code, automate processes, and replace some enterprise software functions, then the intermediary value of traditional SaaS is compressed. So, Bridgewater isn't retreating from tech stocks this time; it's more like moving from "software middlemen" to "AI hard currency."

Assets like NVIDIA, TSMC, Micron, Broadcom, Oracle, and Amazon represent computing power, wafer foundry, memory, networking, cloud, and infrastructure. Their commonality is that, no matter which AI application ultimately wins, the underlying capital expenditure will likely have to pass through these links first.

To sum it up in one sentence: Bridgewater isn't buying the AI concept; it's buying the money that *must* be spent on AI.

4. Appaloosa Management: Tepper Bets on Hardware That 'No One Can Bypass'

David Tepper's Appaloosa Management also gave a very strong direction in Q1.

Public reports show Appaloosa significantly increased its positions in Amazon and Uber in Q1, exited airline stocks, added a new position in SanDisk, and continued to increase exposure to semiconductor and AI hardware chain assets like Micron and TSMC.

Tepper's logic is similar to Bridgewater's, and also very direct: Who wins in AI in the end doesn't matter; first, buy what all winners must procure:

- Micron represents HBM and memory;

- TSMC represents advanced process and foundry capacity;

- SanDisk represents the storage chain;

- Amazon represents AWS cloud infrastructure;

These aren't pure AI application stories; they are the hardware, cloud, and infrastructure in the AI arms race. Of course, while this overlaps with Bridgewater's thinking, Tepper is more concentrated and more aggressive.

In other words, Bridgewater is a macro-configuration-style "increase hardware, decrease software" play, while Tepper seems more like a direct bet that the AI compute cycle isn't over yet, and the ones who will truly capture orders and cash flow are the hardware and infrastructure chain.

To sum it up in one sentence: Tepper is buying the shovel sellers, and specifically the group of shovel sellers closest to the computing bottleneck.

5. Duquesne Family Office: Druckenmiller's Signal is 'Don't Chase the Hottest Spots'

Drückenmiller's Duquesne Family Office is a bit different from the previous firms.

It wasn't the biggest buyer of AI hardware this quarter, but its significance lies in representing another institutional mindset: not staying too long in the most crowded trades.

In fact, Druckenmiller has already reduced or exited popular AI concepts like NVIDIA and Palantir in the past, while continuously focusing on more upstream parts of the supply chain like TSMC. Public reports also show that Duquesne, as a macro-trading oriented fund, is characterized by rapid adjustments rather than long-term adherence to a single story.

This is highly consistent with the main theme of this 13F season: When the market hypes the AI application layer into a consensus, truly sensitive macro capital has already begun moving towards more upstream, more foundational, and cheaper links.

To sum it up in one sentence: he doesn't stand where the crowd is thickest but goes early to places the market hasn't fully priced yet.

6. Egerton Capital: Clears Microsoft, Adds Google, NVIDIA, and Industrial Hard Assets

Egerton Capital didn't just buy AI; it also bought financial infrastructure and industrial hard assets. More importantly, it liquidated Microsoft, taking the opposite side of Ackman.

Public 13F tracking shows Egerton Capital's Q1 13F portfolio was approximately $9 billion, with its top five holdings including Visa, Alphabet, Moody's, Linde, and Carpenter Technology. It also established or increased positions in NVIDIA, Linde, Devon Energy, Canadian Natural Resources, and others.

This portfolio composition is very interesting. It's not simply buying the Magnificent Seven, but dividing the portfolio into several lines:

- Line 1: Financial Infrastructure – Visa, Moody's, CME, Interactive Brokers, Mastercard;

- Line 2: AI Platforms and Computing – Alphabet, NVIDIA;

- Line 3: Industrial Hard Assets and Capex – Linde, Vulcan Materials, Carpenter Technology, Amphenol;

- Line 4: Energy and Resources – Devon Energy, Canadian Natural Resources;

This suggests Egerton isn't buying a single AI story but is buying the intersection of the AI cycle, industrial capital expenditure, and financial tollbooths.

Most importantly, it liquidated Microsoft, creating a very clear counterparty trade with Ackman.

Ackman believes Microsoft has a higher probability of winning in enterprise AI entry points and Azure, so he initiated a new position in Microsoft; Egerton chose to clear out Microsoft, putting more tech exposure into Google and NVIDIA.

The same AI, the same quality growth, but different institutions arrived at completely opposite answers.

2. Cross-Comparison: Who Exactly is the Counterparty for Whom?

1. Google: The Ultimate Divergence Sample of This 13F Season

It can be said that Google is the single most noteworthy asset in this 13F season: Berkshire significantly increased its position, Egerton also added to Alphabet, but Ackman nearly liquidated it.

This shows that Google has transformed from a consensus tech leader into a divergent asset. The bullish side believes Google Search, YouTube, Cloud, and advertising cash flows remain strong; the valuation is relatively less expensive; and the AI impact is exaggerated by the market. The bearish side believes generative AI may change the search entry point; the advertising business model faces reassessment; Google Cloud and Gemini need to prove their commercialization efficiency; and capital expenditure may suppress profit margins.

So, Google isn't a simple case of "institutions are all buying" or "institutions are all selling." It's more like a moat stress test.

Whoever buys Google is buying cash flow and low-valuation recovery; whoever sells Google is selling the risk that AI search disrupts the old entry point.

2. Microsoft: Seen as Enterprise AI Entry Point by Some, Already Overpriced by Others

Microsoft is also a stock with significant divergence this time.

Ackman initiated a new position in Microsoft because he sees long-term certainty in Azure, Microsoft 365, and enterprise AI. However, Egerton cleared its Microsoft position, indicating that another class of institution is unwilling to continue paying an excessively high AI platform premium for Microsoft.

This divergence is crucial. Microsoft hasn't been abandoned by the market, but it is no longer a consensus asset without controversy.

Its problem is a classic one for high-priced tech stocks: has the good company's price already been over-extrapolated? The business can continue to perform well, but the stock price may have already priced in several years of future growth.

3. Amazon: Sold by Berkshire, Bought by Ackman and Tepper

Amazon is also not a unanimous consensus.

Berkshire liquidated Amazon, but Ackman and Tepper still value it highly, Bridgewater also keeps it in a significant position, and Egerton maintained a position even after reducing it.

The divergence behind this is: Is Amazon a high-valuation platform risk, or is it core infrastructure in the AI cloud capex cycle?

Bulls see AWS, the e-commerce base, advertising business, and AI cloud demand. Bears see portfolio simplification, valuation discipline, and the rebalancing of platform assets.

So, Amazon isn't like Google with its "moat controversy." It's more of a "portfolio position controversy," where institutions question whether such a large Amazon exposure is necessary at the current price and portfolio structure.

4. Traditional SaaS: From Safe Haven to Audited Asset

Bridgewater's liquidation of Salesforce and ServiceNow is one of the most structurally significant moves this 13F season.

It's not simply selling two stocks; it represents the market starting to reassess the traditional SaaS business model. In the past, SaaS was a high-quality asset, earning money through subscriptions, stickiness, data, and process management. But with the generalization of AI LLMs, the intermediary value of enterprise software is being challenged.

If many processes can be automated by AI, much code can be generated by AI, and many software functions can be invoked directly by LLMs, then the high valuations of traditional SaaS need to be re-explained.

This is why traditional software and AI hardware formed such a clear counterparty relationship in this 13F season: selling the software middle layer, buying computing power, memory, foundry, cloud, and hardware infrastructure.

5. Financial Infrastructure: Sold by Berkshire, Bought by Egerton

Visa and Mastercard also showed interesting divergence.

Berkshire liquidated Visa and Mastercard, but Egerton's top holding is Visa, alongside holdings in Moody's, CME, and Interactive Brokers. This shows that financial tollbooths haven't lost their value.

It's just that different institutions have diverging views on their role in a portfolio. Berkshire might be performing portfolio cleaning and trimming old positions, while Egerton views assets like Visa and Moody's as long-term cash flow foundations.

So, this isn't a simple case of "payment stocks are failing," but rather that financial infrastructure is no longer a thoughtless consensus, though it remains a high-quality core holding in the eyes of some institutions.

3. How Should We Understand This 13F Season?

Many might say: This 13F season still looks like everyone is buying AI. How can you say the consensus is gone?

The key point is that the consensus on the AI *direction* remains, but the consensus on AI *beta* is gone.

As is well known, in the past, buying AI, buying the Magnificent Seven, buying tech leaders, and buying semiconductor ETFs would likely allow you to track the main trend. But it's different now.

AI has been disaggregated – into platform layers, application layers, hardware