MEXC Alpha Trader Investment Research Weekly Report | Rate Cut Expectations Fully Reversed, Crypto Legislation Breakthrough Meets Historic ETF Outflows

- Core Viewpoint: In the third week of May 2026, the U.S. Senate Banking Committee's passage of the CLARITY Act marked a milestone in the deregulation of the crypto industry. However, this positive development was offset by a complete reversal in the macro landscape. April's CPI and PPI significantly exceeded expectations, causing Federal Reserve rate cut expectations to vanish and the probability of a rate hike to surge to 28%. Bitcoin came under pressure, falling below $77,000. Institutional capital inflows, which had continued for six weeks, reversed to outflows of approximately $1 billion in a single week.

- Key Factors:

- The CLARITY Act passed the Senate Banking Committee with a bipartisan vote of 15:9. This marks the first time in U.S. history that a committee has voted on comprehensive crypto market structure legislation. It now requires a full vote by the Senate.

- April's PPI surged 6.0% year-over-year; Core PPI rose 5.2% YoY, its largest increase in over three years. CPI also jumped to 3.8% YoY. The CME FedWatch Tool implied probability of a December rate hike soared from 2% to 28%.

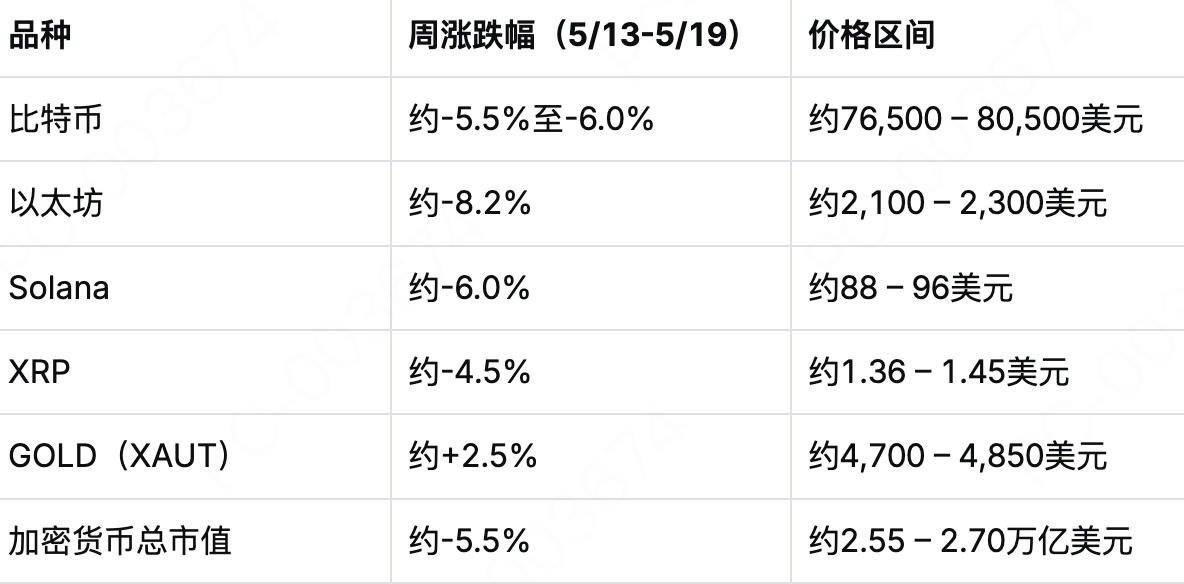

- Bitcoin fell continuously from $82,000 to approximately $76,700 on May 19, erasing most of its gains for the month. Ethereum dropped to around $2,100, a two-month low.

- Bitcoin spot ETFs saw net outflows of approximately $1 billion in a single week, ending a six-week trend of net inflows totaling around $3.4 billion. On May 13 alone, net outflows reached as high as $635 million.

- The stalemate in U.S.-Iran ceasefire talks pushed Brent crude oil above $110 per barrel. High energy prices reinforce inflationary pressures through transportation costs, further solidifying expectations of Fed tightening.

- The total stablecoin market capitalization surpassed $320 billion. USDC saw a one-time mint of 250 million tokens on Ethereum, indicating that on-chain liquidity pools are still expanding.

- The Nasdaq and S&P 500 ended a six-week winning streak. The 30-year U.S. Treasury yield returned to the 5% threshold, signaling a market shift from "earnings season-driven" to "inflation-pricing-driven".

Week 3 of May 2026

Statistical Period: May 13, 2026 – May 19, 2026

Data Cutoff: May 19, 2026

Core Narrative

The past week has been a critical window for the complete restructuring of macro logic in the crypto market since 2026. On May 14, the U.S. Senate Banking Committee voted 15-9 in a bipartisan decision to formally pass the CLARITY Act. This marks the first time in U.S. congressional history that a committee-level vote has been held on comprehensive crypto market structure legislation, signaling the end of nearly a decade of regulatory "grey area" for the crypto industry. However, this legislative breakthrough was unable to offset the deeper macro reversal.

A landmark inflection point has emerged on the macro front. Following the April CPI report on May 12 showing a year-over-year surge to 3.8% (the highest since autumn 2023), the U.S. Bureau of Labor Statistics reported on May 13 that April's PPI skyrocketed to 6.0% year-over-year, far exceeding all economist expectations and marking the largest monthly increase since 2022. Core PPI at 5.2% was the biggest gain in over three years. This stronger-than-expected inflation, alongside rising energy costs fueled by geopolitical conflicts, has fundamentally shifted the Fed's monetary policy path. The CME's implied probability of a Fed rate hike in December 2026 has surged from about 2% a month ago to approximately 28%. The 30-year Treasury yield has returned to the 5% threshold, and mainstream market expectations have directly switched from "rate cuts within the year" to "the possibility of a rate hike."

Bitcoin experienced a significant pullback during this week. From above $82,000 in early May, Bitcoin slid throughout the week, dipping below $77,000 during Asian trading hours on May 19 and briefly approaching the $76,500 mark, erasing most of its gains from the month. Ethereum weakened in tandem, falling to around $2,100, its lowest level since April 7. Against the backdrop of a definitive macro reversal, the crypto market entered a phase of risk repricing in mid-May, shifting from pricing in "regulatory optimism + easing expectations" to a complex narrative of "regulatory thaw + liquidity tightening."

Geopolitical factors continue to provide imported volatility. US-Iran ceasefire negotiations failed to make substantial progress. During Asian hours on May 18, Brent crude oil stood above $110 per barrel, and WTI crude broke through $107 per barrel, reaching its highest level since May. Rising oil prices are feeding through to core inflation via transportation costs, further reinforcing expectations of Fed policy tightening.

In the US stock market, although the Nasdaq and S&P 500 had hit all-time highs for six consecutive weeks, US stock futures fell across the board starting May 13, with the semiconductor sector leading the decline. The market is transitioning from being driven by earnings season to pricing in inflation. Nvidia's earnings report and the Fed meeting minutes are set to be the two major focal points for the market in the coming week.

I. Key Crypto Market Dynamics

1. Institutional Flows: Six-Week Inflow Streak Ends with ~$1 Billion Weekly Outflow

The strong six-week net inflow trend for spot Bitcoin ETFs officially reversed this week. According to data from multiple sources, over the five trading days ending May 15, 2026, U.S. spot Bitcoin ETFs saw total net outflows of approximately $996 million to $1 billion, ending a streak of six consecutive weeks totaling about $3.4 billion in net inflows.

May 13 saw the peak of this week's selling pressure. According to reports from BingX, CoinDesk, and others, spot Bitcoin ETFs recorded net outflows of up to $635 million that day (some reports cite $630.4 million), making it one of the largest single-day net outflows of 2026. Driven by the triple shock of ETF selling, inflation data, and long liquidations in the derivatives market, Bitcoin's price accelerated its decline from near $82,000 to around $78,000. Ethereum spot ETFs also mostly recorded net outflows during the week. Combined net outflows for BlackRock's Bitcoin and Ethereum ETFs totaled approximately $653.9 million for the week, reflecting institutions taking a phased defensive de-risking stance after the macro risk repricing.

Flows took a brief breather on May 14. Bitcoin ETFs recorded $131 million in net inflows, with total trading volume reaching $2.76 billion, higher than the previous day's $1.99 billion. However, this rebound was short-lived—another net outflow of approximately $290 million occurred on May 15, creating a weak weekly flow pattern of "precipitous outflow → modest replenishment → renewed outflow."

Notably, despite the ~$1 billion weekly net outflow, the total cumulative net inflow for Bitcoin ETFs remains above approximately $59 billion, and the existing holdings haven't been severely eroded. As of press time on May 19, Bitcoin was trading around $76,769. Total market-wide derivatives liquidations for the day were about $180 million. The Crypto Fear & Greed Index fell to 31, returning to the "Fear" zone.

2. Price Action: Bitcoin Drops Below $77k, Ethereum Hits Two-Month Low

Bitcoin's price trajectory this week was characterized by a sustained one-sided decline. The fundamental backdrop can be summarized in three phases:

- Phase 1 (May 13-14): Inflation data shock, breakdown below $80k. Following the dual surprise of April's CPI at 3.8% YoY and PPI at 6.0% YoY, Bitcoin rapidly declined from above $81,000, breaking below the $80,000 mark and briefly touching areas under $79,000. On May 13, Bitcoin fell below $80,000 intraday, down over 2% from its daily high.

- Phase 2 (May 15-17): Regulatory boost provides temporary lift, but rebound is limited. News of the Senate Banking Committee passing the CLARITY Act on May 15 provided some emotional support, stabilizing prices in the $78,000-$79,000 range temporarily. However, persistent ETF outflows capped the upside.

- Phase 3 (May 18-19): Macro pressure mounts, breakdown below $77k. In the latter half of the week, concerns over multiple macro pressures such as rising oil prices from the US-Iran standoff and growing expectations of a Fed rate hike continued to build. Bitcoin dipped below $77,000 on May 18 and by May 19 had fallen further to around $76,500-$76,800, erasing most of its gains from the month.

The Crypto Fear & Greed Index (FGI) dropped to 31 on May 19, entering the "Fear" zone.

Data Sources: CoinGecko, MEXC

Technically, after breaking below the 100-hour moving average and the $80,000 psychological level, Bitcoin's short-term trend has weakened. The $76,000 level is a critical support zone since February—it corresponds to previous lows tested multiple times. A decisive break below this level could open the door to a deeper decline. On Polymarket, the probability of traders betting on Bitcoin falling below $75,000 before the end of May has risen to 74%.

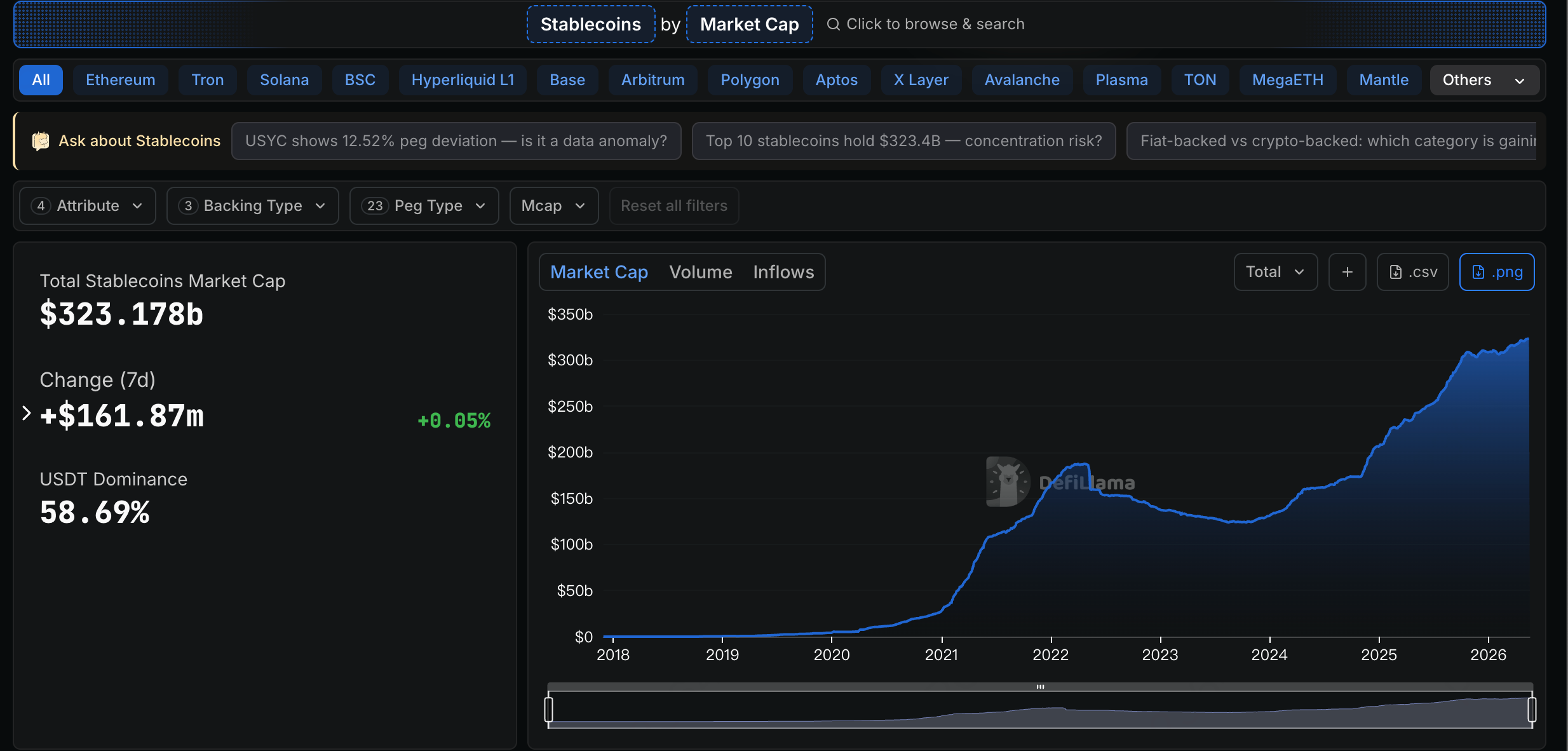

3. Stablecoins: Total Market Cap Surpasses $320 Billion, USDC Supply Continues to Grow

The stablecoin market continued its moderate expansion trend. As of mid-May, the total global stablecoin market cap officially broke through the $320 billion mark. USDT's market cap is approximately $189.6 billion, accounting for about 60% of the total stablecoin market cap. USDC's market cap is roughly $77-78 billion, representing about 24-25%. Together, they command nearly 90% of the market share.

Newly issued USDC continues to enter circulation. On May 19, according to Whale Alert's on-chain monitoring, the USDC Treasury executed a large-scale minting transaction on the Ethereum network, issuing 250 million new USDC tokens in one go. Yield-bearing stablecoins are becoming the fastest-growing sub-sector, adding approximately $4.3 billion in market cap in Q1 2026. The sUSDS token alone absorbed over $2.5 billion in new capital. The latest movements of USDT and USDC suggest that the on-chain "dry powder" pool is still expanding in an orderly manner.

II. Global Asset Performance

1. Equity Markets: Inflation Data Weighs on US Stocks, Six-Week Winning Streak Ends for Nasdaq and S&P 500

The US stock market transitioned from being "earnings season-driven" to "inflation pricing-driven" this week. With April's CPI (3.8% YoY) and PPI (6.0% YoY) both significantly exceeding expectations, the CME's implied probability of a Fed rate hike in December 2026 jumped from about 2% a month ago to 28%. The 30-year Treasury yield returned to the 5% level.

The Fed's April FOMC meeting held the federal funds rate steady in the 3.50%-3.75% range with a vote of 8-4, the most divided since 1992. Following the inflation data release, institutions like CICC adjusted their forecasts from "possible rate cuts within the year" to "difficulty in further easing this year." Under the baseline scenario, US PCE inflation is expected to stay above 3.5% for the year, with core PCE above 3%, both significantly higher than the Fed's 2% target.

On May 13, futures for the three major US stock indices fell across the board, with chip stocks generally declining and the semiconductor sector leading the losses. After six consecutive weeks of record highs, both the Nasdaq and S&P 500 are under pressure at elevated levels. The repricing of the Fed's policy path is driving capital outflows from growth sectors.

Key earnings and events this week: Cisco (CSCO) reported on May 13; Home Depot (HD) reported on May 19; Nvidia is expected to report in late May, seen as a litmus test for market sentiment.

2. Commodities: Oil Volatile at Highs, Precious Metals Under Pressure

Over the past week, international commodity markets showed a clear pattern of "strong oil, weak gold." On May 18, Brent crude broke through the $110/barrel level, and WTI crude stood above $107/barrel. Key drivers of this rally included: irreconcilable core differences in US-Iran ceasefire talks; the continued closure of the Strait of Hormuz reducing global oil supply by over ten million barrels per day; the expiration of Russian oil sanctions waivers in mid-May; and drone attacks on Gulf energy facilities over the weekend.

For the week ending May 12, London gold was priced at $4,528.00/oz, down $213.40/oz from May 8, a weekly decline of 4.50%; London silver was priced at $78.74/oz,