Tiger Research: On-Chain Risk Managers – A Vast Gulf Between a $147 Trillion and a $70 Billion Market

- Core Thesis: The decentralized finance (DeFi) lending space is shifting from being protocol-led to being driven by professional risk management teams, with the core of the industry now revolving around competition in risk assessment capabilities. Traditional asset management institutions, leveraging their mature risk control experience, are at the best entry window. However, the track's scale is still small, making first-mover advantage crucial.

- Key Elements:

- The DeFi lending sector has given rise to the professional asset management role of the "risk manager," responsible for strategy formulation and risk control, replacing the earlier model dominated entirely by protocols and communities.

- As of May 2026, the global risk management track manages approximately $70 billion in assets. The top three teams (Steakhouse, Sentora, Gauntlet) hold a 70% market share, with capital concentrating among the leaders.

- There are three pathways for entering the industry: channel distribution (outsourcing risk control), asset supply (onboarding high-quality on-chain assets), and independent operation (building an in-house risk team). These pathways determine the distribution of influence, capability, and risk.

- The underlying DeFi architecture has replicated the division of labor found in traditional finance: top-level capital raising (exchanges), mid-level strategy and risk control (risk managers), and bottom-level products and custody (lending protocols).

- The optimal entry point for traditional asset management institutions is the strategy management layer. Their core advantage lies in professional risk assessment capabilities, not technology or traffic. For instance, Bitwise has already deepened its involvement through an independent operation model.

- The current DeFi market size (approximately $80 billion) stands in stark contrast to the global traditional asset management scale ($147 trillion), indicating immense growth potential. However, early risk management teams benefit from setting the rules of the game.

This report is written by Tiger Research. Within decentralized finance lending, the power to influence is shifting from protocol projects to professional entities that hold risk control decision-making power. The essence of entering this industry boils down to one choice: leveraging external risk assessment capabilities, providing your own, or building that capability in-house.

Key Takeaways

- The decentralized finance landscape is giving rise to new asset management roles, signaling the end of an era dominated entirely by protocols and community governance.

- The sector is still nascent, but capital flows and channel resources are rapidly concentrating among top-tier risk management teams, whose track records are becoming the core benchmark for institutional entry.

- Three primary entry paths exist: distribution channels (leveraging risk teams for backend support), asset supply (tokenizing off-chain assets), and independent operation (building an in-house risk management team).

- The chosen path directly dictates an entity's influence, required core competencies, and potential risks.

- The core decision for the industry is not whether to enter DeFi, but how to allocate responsibilities: which risk control decisions to delegate externally, and which core powers to retain in-house.

I. Risk Managers: Professional On-Chain Asset Managers

Traditional finance has long separated decision-making and execution. As the crypto market matures, specialized operational entities have emerged for its distinct functions.

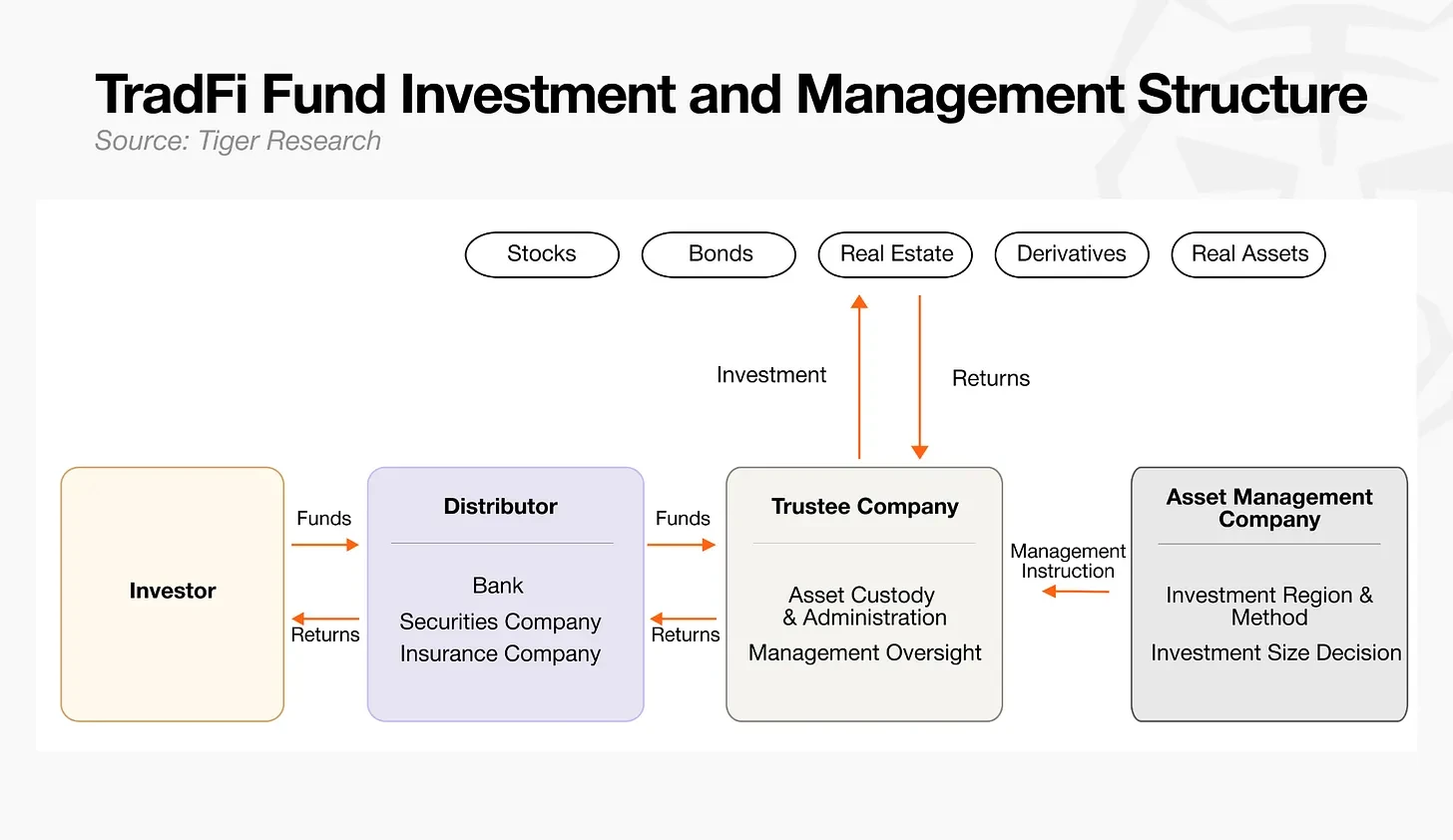

Functional Division in Traditional Finance

- Asset Managers: The core decision-making hub for capital allocation, formulating overall investment strategies and issuing execution instructions to custodians.

- Custodians: Responsible for the safekeeping of assets, executing investment operations strictly per the manager's instructions, and overseeing asset security.

- Distributors: Market fund products to investors, handling capital raising and aggregation.

The crypto industry has evolved a corresponding functional system. Early DeFi relied entirely on smart contracts, but market experience has proven that code alone cannot fully prevent all types of on-chain risks. To ensure the stable operation of on-chain lending, a cohort of professionals specializing in complex risk assessment and coordination—Risk Managers—emerged, formally assuming the asset management function within the on-chain ecosystem.

II. Early DeFi Lacked Specialized Risk Control Roles

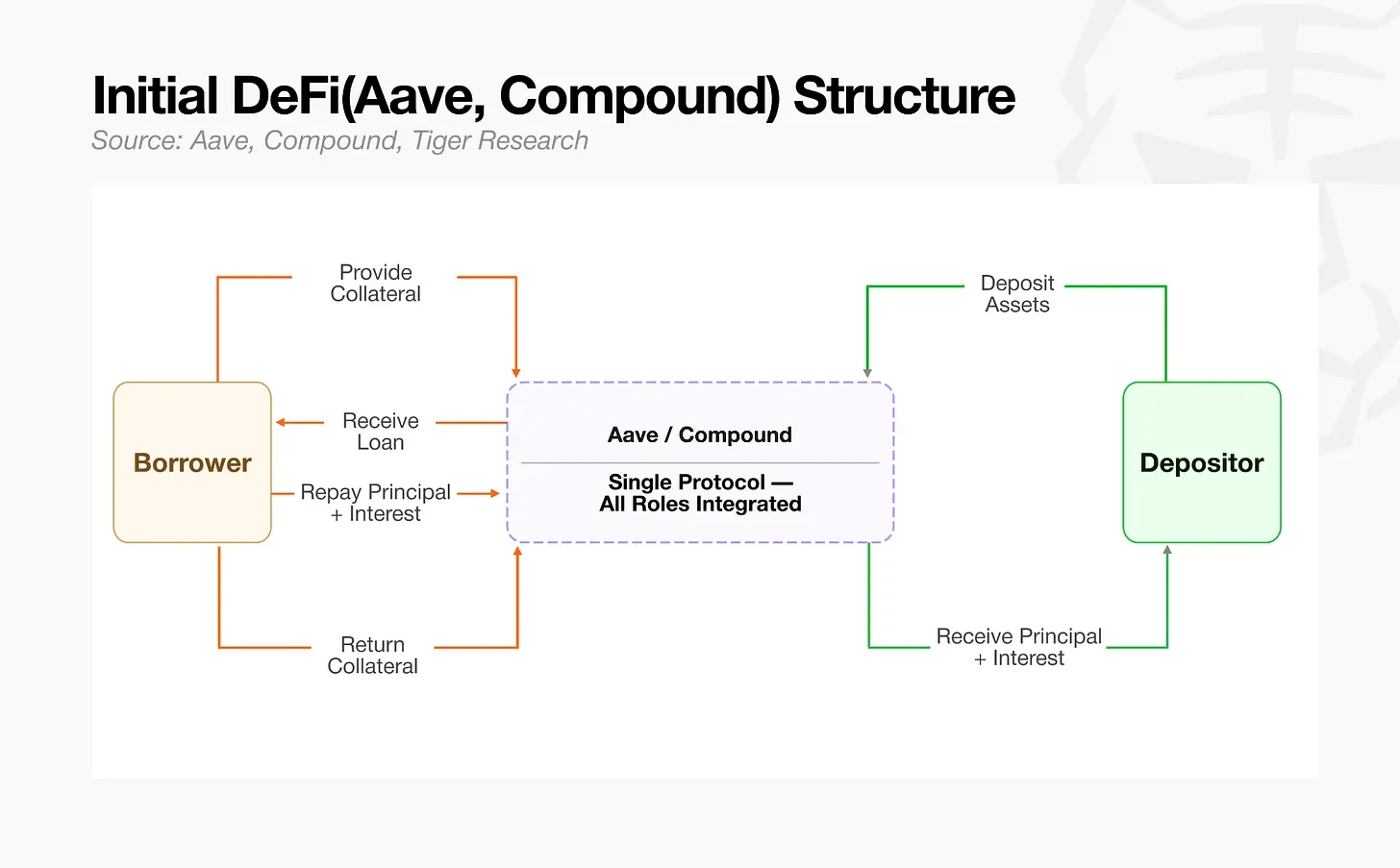

Early lending protocols like Aave and Compound deeply integrated lending infrastructure with risk control standards into a single architecture. While risk-related practitioners existed, all network assets were pooled into one pool. Practitioners could only act as global protocol risk managers, making minor adjustments to overall risk parameters. When high-volatility assets entered the pool, this structure easily propagated risk; a loss from a single poor-quality asset could rapidly spread throughout the entire ecosystem, creating an urgent need for specialized chain risk management.

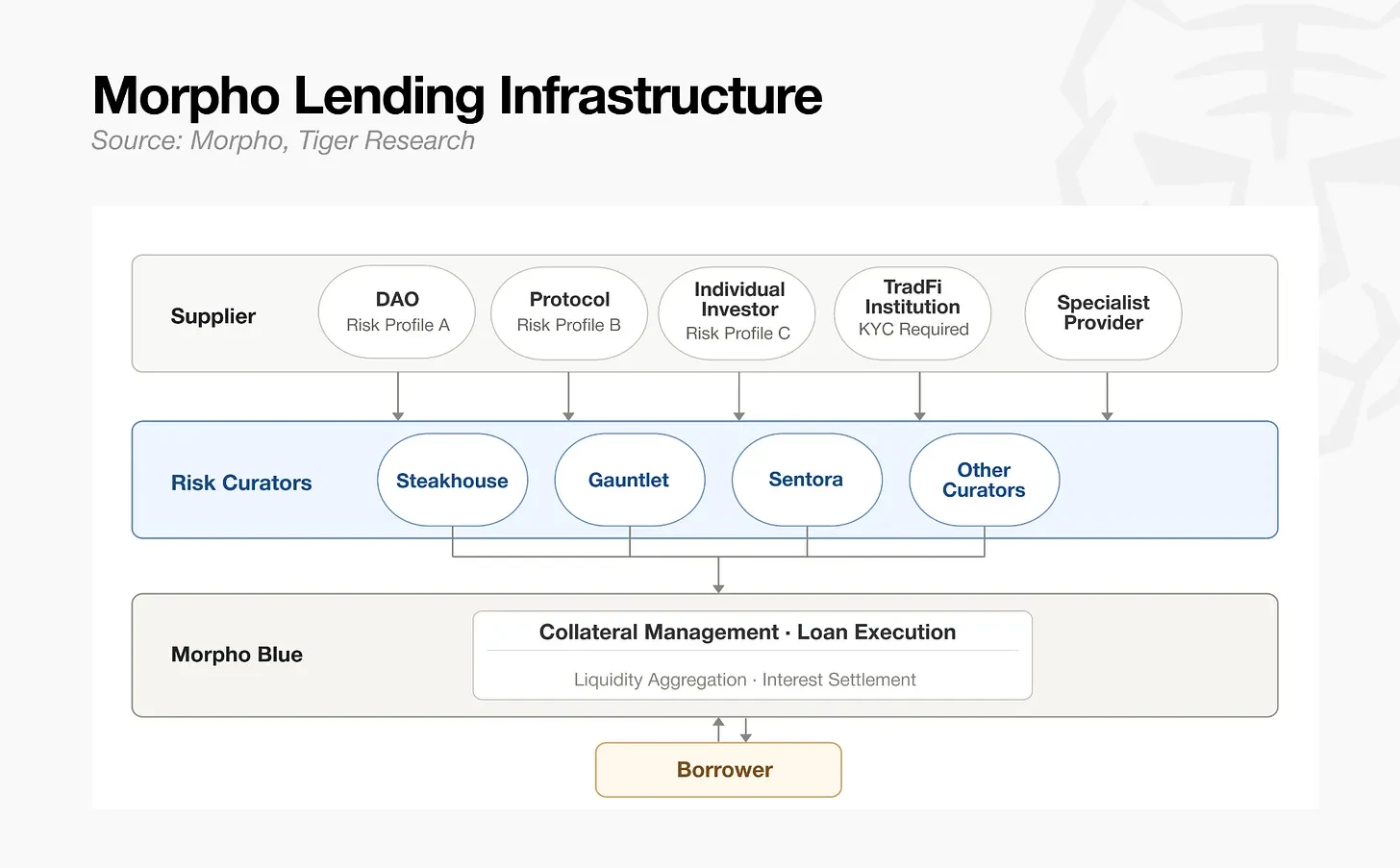

The industry landscape changed completely with the arrival of Morpho. Morpho separated collateral asset types and lending terms into independent trading markets, replacing the traditional single pool with a modular multi-vault architecture. This fundamentally restructured asset operations, leading to a complete transformation of the risk manager's role. Practitioners were no longer limited to passive risk control within a fixed protocol framework. External professional teams could now set their own risk control rules and independently build and operate their own lending vaults. With the complete separation of underlying infrastructure and risk assessment authority, risk managers transitioned from global protocol risk controllers to professional on-chain asset operators, independently managing multiple vaults.

III. Current Landscape of the Top Tier

As of May 2026, the global risk management sector manages approximately $70 billion in assets, with the top three teams commanding a 70% market share. The sector only truly took off in 2025, and capital is rapidly consolidating around competent teams, with significant preference shown for operators possessing a proven track record.

The three leading teams entered the space through different paths:

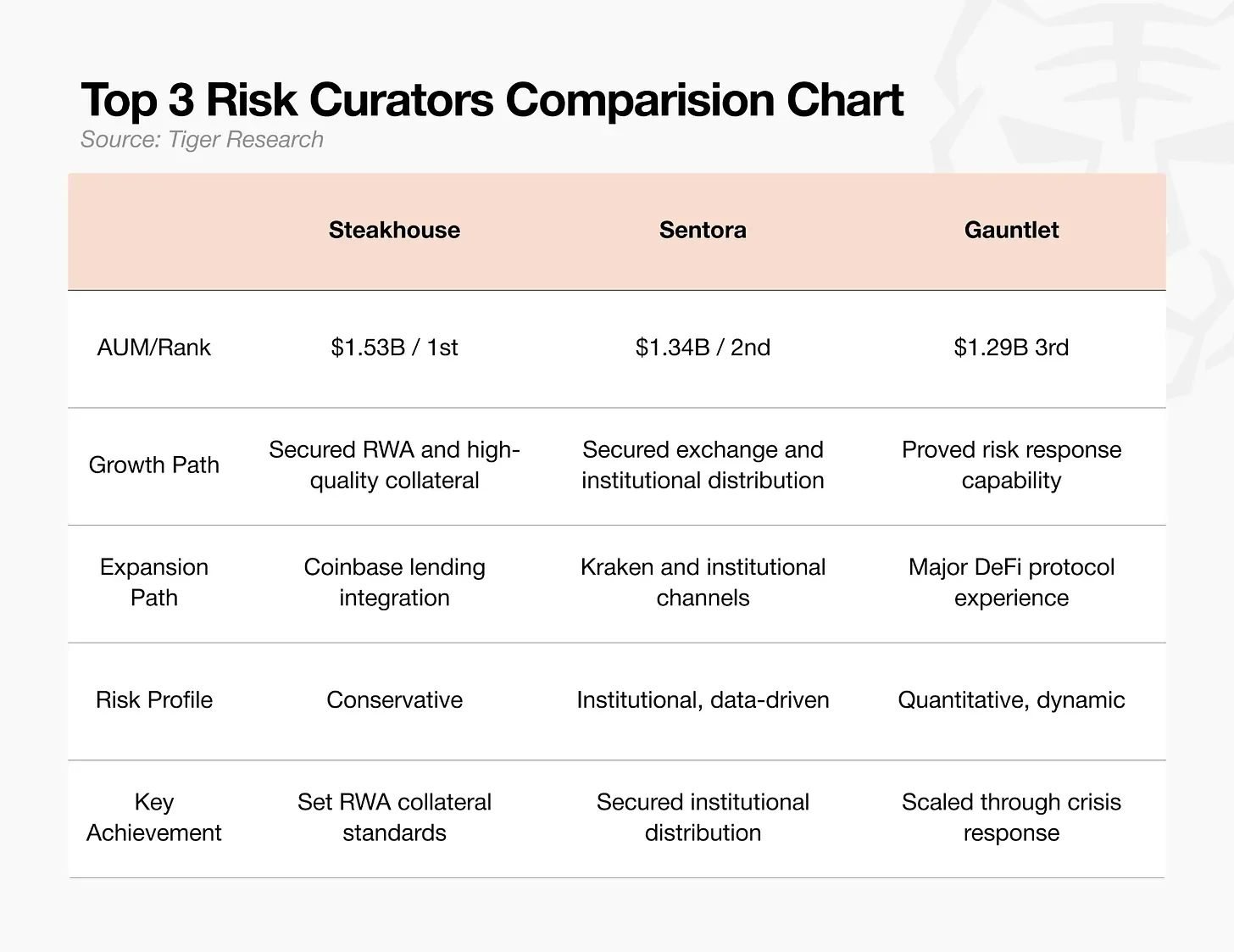

- Steakhouse: A conservative risk management institution, pioneering the compliant on-chain tokenization of high-quality real-world assets (RWAs) like US Treasuries for collateral. As Coinbase's exclusive backend risk management partner for its lending business, it holds access to a premier distribution channel. With AUM of $15.3 billion as of February 2026, it ranks first and largely sets the standards for acceptable RWA collateral within the DeFi ecosystem.

- Sentora: Built on AI-driven risk models and institutional-grade data systems, deeply integrated with Kraken exchange as its backend service provider, securing institutional capital flows. With $13.4 billion in AUM, it ranks second, focusing on facilitating capital flow between exchanges and institutional clients.

- Gauntlet: A veteran on-chain quantitative risk modeling firm specializing in simulating various market risk parameters. In October 2025, it managed the onboarding of $775 million in capital, rectifying yield anomalies within just 10 days. Its strong track record in managing large capital inflows and crisis response is industry-recognized. With $12.9 billion in AUM, it is considered the benchmark for risk management stability during large capital deployments.

Competition in the sector has moved beyond simple AUM comparison. The core battleground now revolves around three major barriers: collateral admission standards, capital distribution channels, and emergency risk response capabilities.

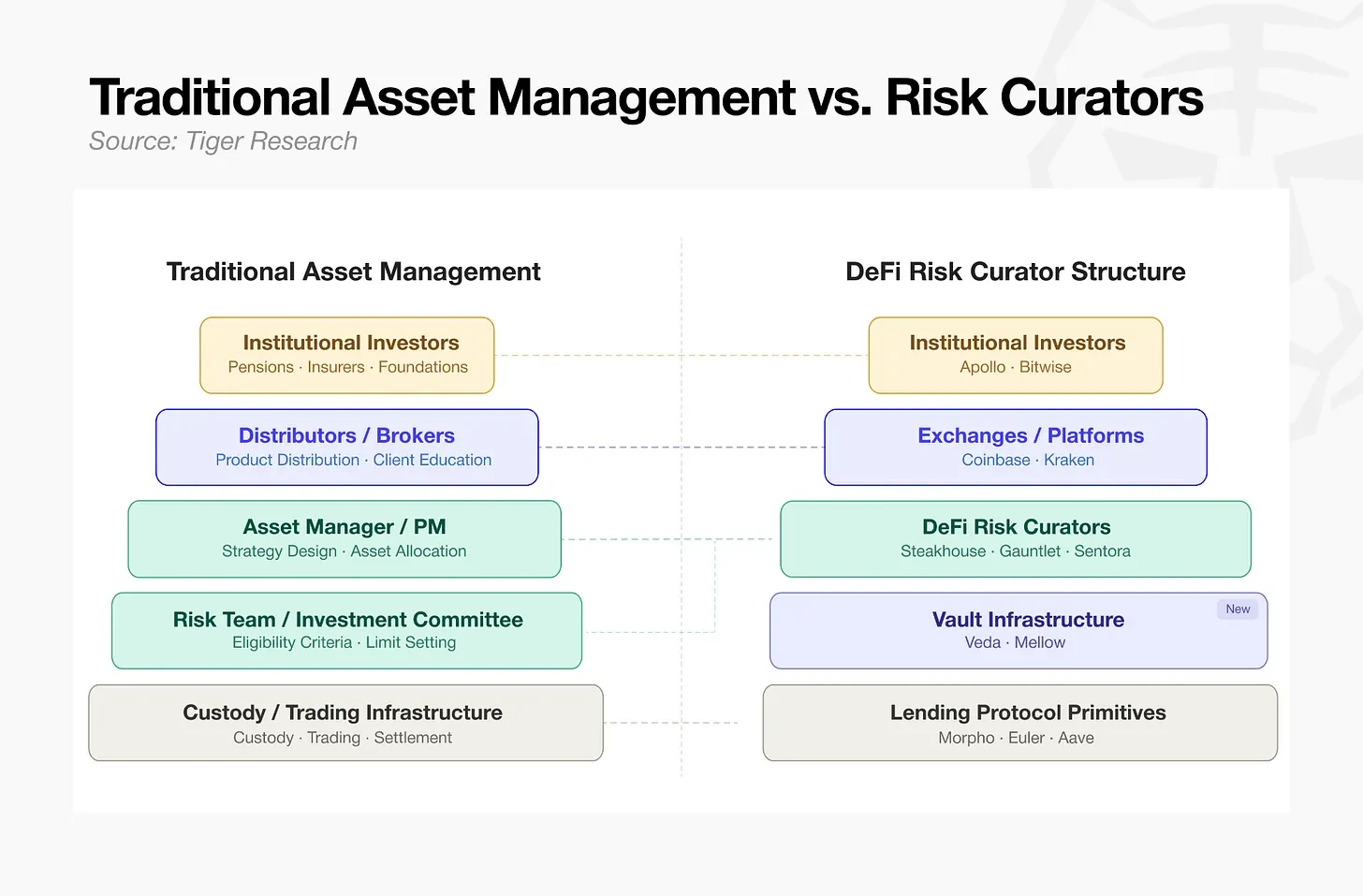

IV. Traditional Asset Management Model vs. DeFi Risk Management System

With Morpho's market modularization, different types of collateral assets require dedicated professional teams for independent assessment and control. Professional risk teams like Steakhouse entered the fray, becoming DeFi-specific risk managers, gradually aligning DeFi operational models with mature traditional asset management processes.

From top to bottom, it's clear that the current DeFi architecture has fully replicated the division of labor from traditional finance:

- Top Layer: Fundraising & Distribution: Institutional investors are the primary source of capital, flowing into the on-chain ecosystem via major centralized exchanges and integrated platforms, analogous to traditional financial brokerages and distribution channels.

- Middle Layer: Strategy & Risk Management: DeFi risk managers oversee the capital deployment strategy, akin to traditional portfolio managers and risk committees, setting asset admission criteria, position limits, and overall capital allocation strategies.

- Bottom Layer: Product & Custody: Using vaults as vehicles, strategies are translated into investable on-chain financial products. The underlying lending protocols handle asset storage and on-chain settlement, mirroring the functions of traditional asset custody and clearing infrastructure.

From capital raising and strategy execution to asset custody and settlement, the entire operational framework now mirrors mature traditional financial systems. For traditional financial institutions, on-chain lending is no longer a foreign new frontier but a standardized market with clear logic and a complete system, significantly lowering the barrier to entry.

V. Benchmarking Traditional Asset Management: Opportunities Within the Sector

Following the asset-management-style functional division of on-chain lending, the door is now open for various institutions. However, the entry barriers differ significantly across different layers of the sector:

- Distribution Layer: Faces the end-user market. Top crypto institutions have achieved market monopoly, making direct competition for traditional financial institutions a low-value proposition cost-wise.

- Strategy Management Layer: Competition revolves around core financial analysis capabilities and talent reserves. Asset risk assessment, management, and product packaging are core businesses for traditional asset managers. By leveraging mature modular infrastructure to deploy their own risk control systems without needing to develop complex underlying technology from scratch, they can quickly build stable, profitable business models. This is the optimal entry point.

- Custody & Infrastructure Layer: Focuses on blockchain technology development and implementation. It is a technology-intensive field with high demands for underlying Layer 1 development capabilities, making it extremely difficult for traditional financial institutions to enter by building their own systems.

Compared to other paths reliant on traffic resources or underlying technology, the strategy management and risk control layer offers the lowest barrier to entry. Traditional financial institutions can leverage their own mature, time-tested risk control systems to quickly seize a dominant position in the industry.

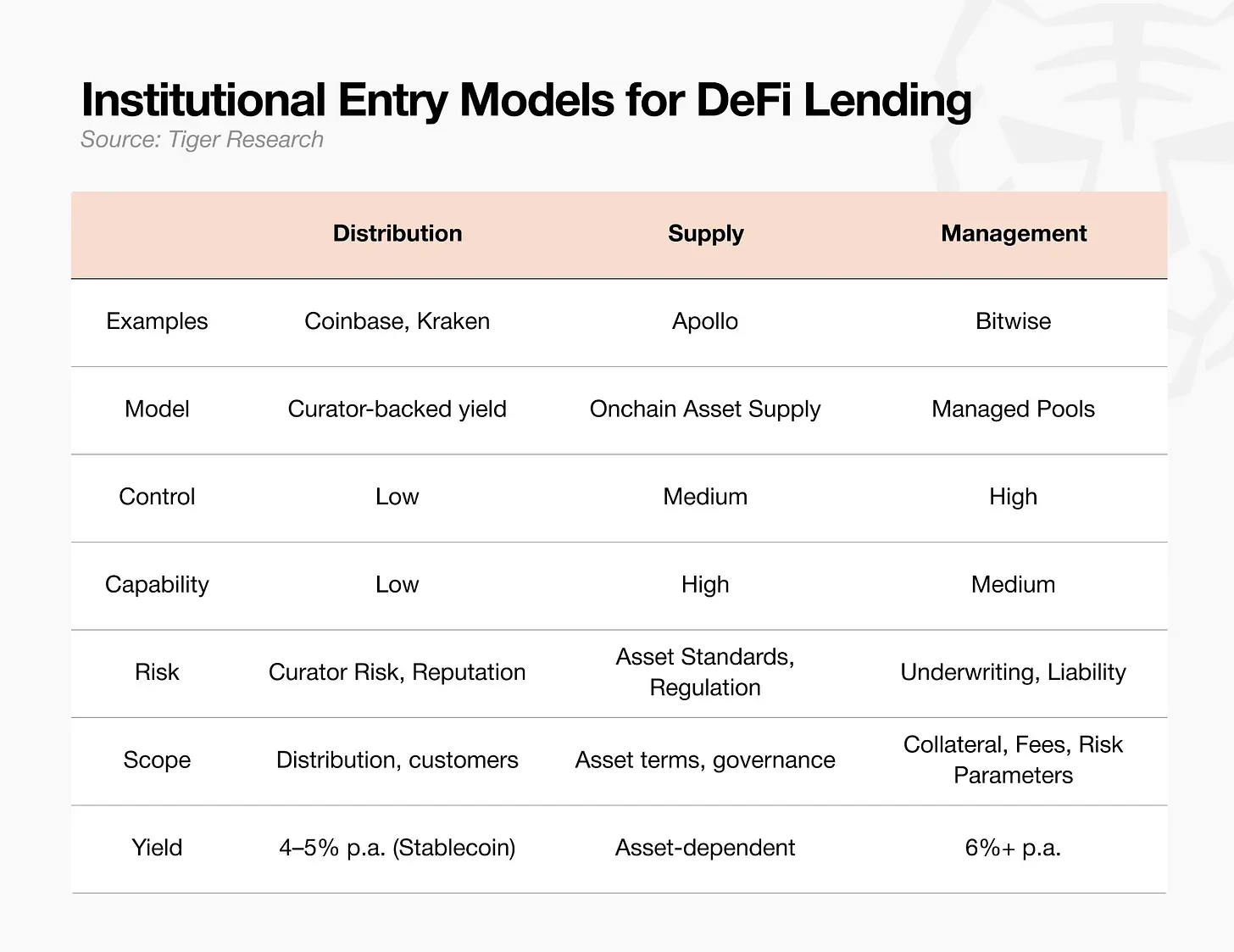

Currently, there are three mainstream models for institutional entry into DeFi. Regardless of the path chosen, the core competitive advantage always lies in the professional risk assessment capabilities of the risk management team.

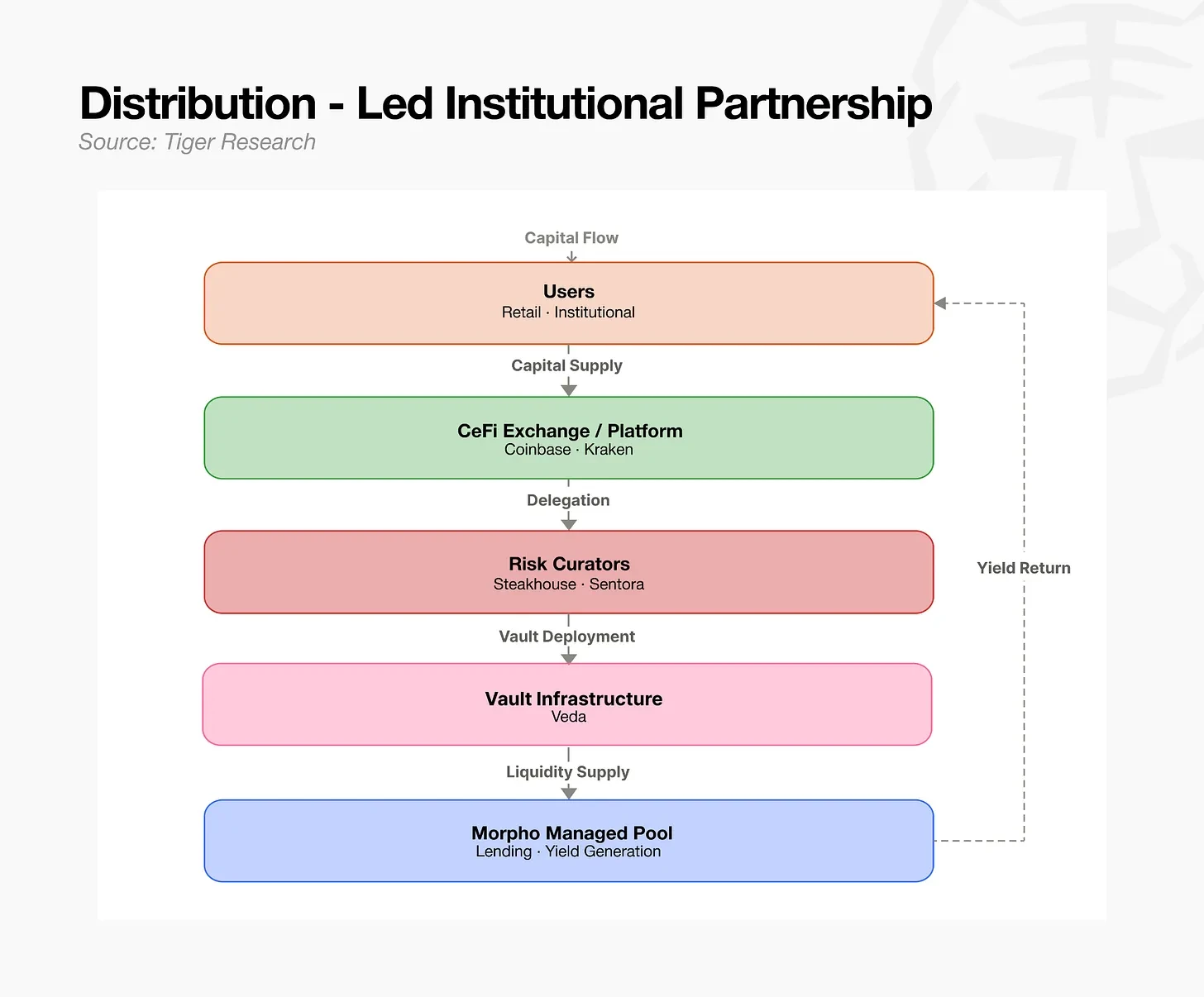

5.1 The Distribution Model: Leveraging Professional Teams for Backend

By leveraging mature external risk management teams as backend services, entities can quickly capture market share. This is suitable for exchanges and fintech platforms with vast user traffic but lacking independent on-chain risk control capabilities. Investment strategies are fully outsourced, but the entity still bears the reputational and operational liability risks associated with the partner team. Centralized exchanges with end-user traffic, but unwilling to deeply develop complex on-chain lending risk control, typically adopt this model: integrating with an authoritative, compliant external risk management team as the business backend to launch lending financial services. The platform leverages its own traffic for large-scale capital acquisition, while collateral vetting and full process risk control are entirely handled by the partner risk management team.

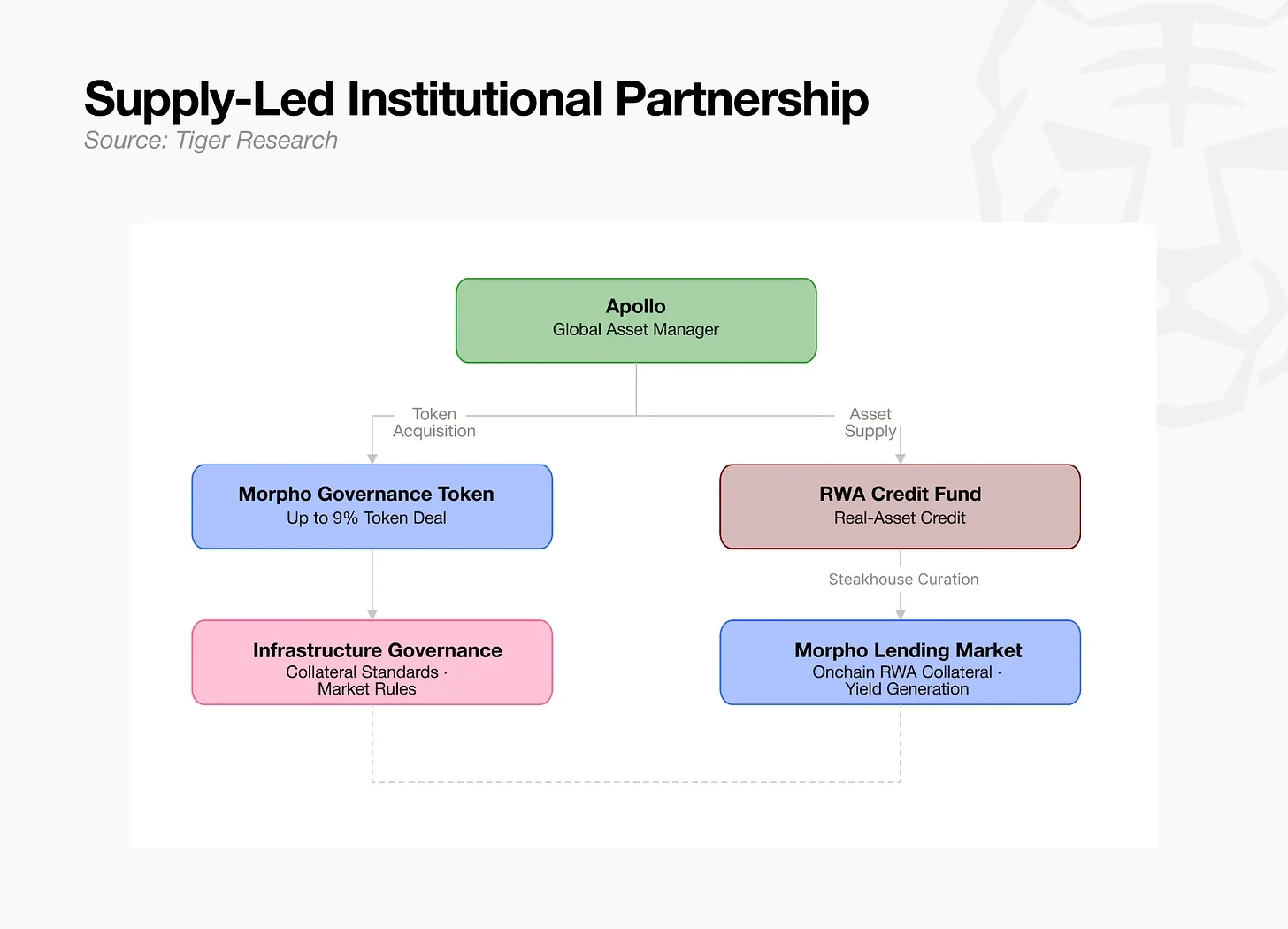

5.2 The Asset Supply Model: Compliant Tokenization of Off-Chain Assets

Asset managers holding high-quality underlying assets like RWAs or credit assets directly supply their existing assets to the on-chain market. Using Apollo as an example, while supplying assets on-chain, the institution also acquires governance tokens of lending protocols to participate deeply in setting industry collateral admission rules favorable to its assets. The core challenge of this model lies in standardizing assets for compliance and building a supporting regulatory framework. Large private equity firms and holders of physical assets can directly connect their high-quality assets to on-chain financial channels. Apollo goes beyond simple asset supply, accumulating governance tokens of leading lending protocols to participate in rule-making, actively pushing for its off-chain assets to become officially recognized, high-priority compliant collateral within the market. However, suppliers cannot arbitrarily include any asset as collateral. The market requires objective third-party verification of asset safety and confirmation of quick, sufficient liquidation capabilities on-chain. This process is inseparable from the rigorous vetting and credit endorsement of risk management teams. Ultimately, the long-term viability of this model still relies on the institution's own professional risk assessment capabilities.

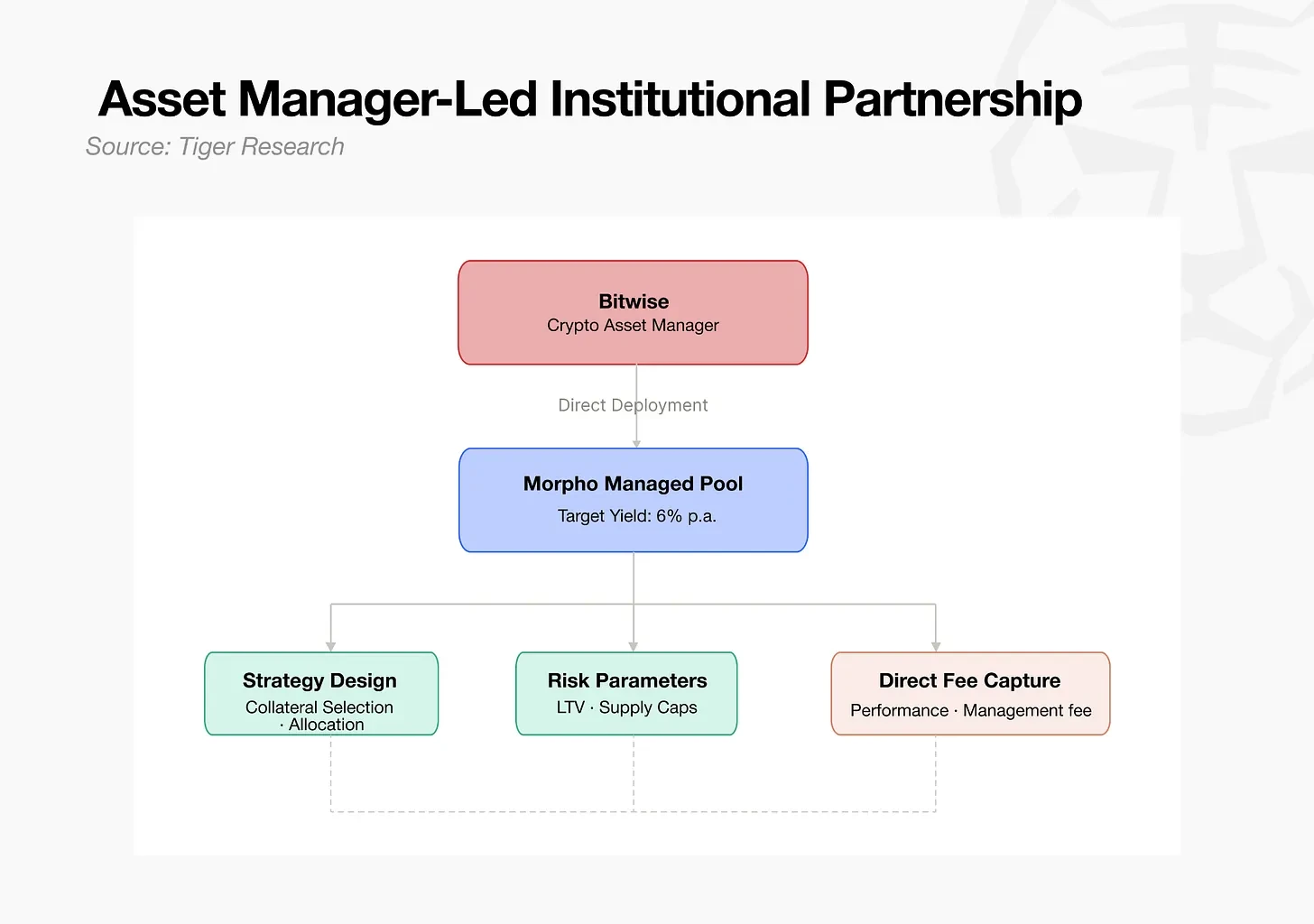

5.3 The Independent Operation Model: Building an In-House Risk Management Team (Representative: Bitwise)

Asset managers develop their own investment strategies and independently build and operate their own on-chain vaults. Bitwise has pioneered defining on-chain vaults as the version 2.0 of exchange-traded products (ETFs), formally committing deeply to the space. This model offers the highest autonomy over fee pricing and collateral admission standards, but the entity bears full responsibility for all operational risks and losses. It is suitable for large asset managers with established in-house risk teams. This model involves a traditional asset manager transforming directly into an independent risk manager without reliance on external platforms. Bitwise, leveraging its mature portfolio construction systems and risk controls, autonomously designs and fully controls its on-chain vault operations, capturing stable management fees directly on-chain.

VI. Industry Landscape Ahead of Massive Traditional Capital Inflows

Looking at industry trends, as the on-chain lending ecosystem continues to mature, traditional large-scale asset managers possess the strongest advantages for entry. With the DeFi ecosystem completing its modular functional split, market demand has shifted: the industry no longer lacks smart contract development talent but is desperate for the professional financial skills honed over decades by traditional finance, such as collateral due diligence and risk limit setting. The practical risk management experience accumulated by traditional asset managers over decades can be seamlessly adapted and migrated to on-chain financial scenarios.

However, the current total market size of DeFi is still unable to absorb direct large-scale entry from the world's top-tier giant asset managers. The global traditional asset management industry totals a staggering $147 trillion in AUM. BlackRock alone manages approximately $14 trillion. In contrast, the entire DeFi sector is only $80 billion, with the risk management niche comprising just $7 billion—less than 1/2000th of BlackRock's AUM.

This massive disparity underscores the sector's immense potential for growth. Institutional capital is inherently risk-averse and will only enter mature markets with sound risk control systems. Once risk management teams establish safe and stable on-chain capital flow systems, alongside a maturing regulatory framework, the industry will undergo a qualitative transformation. Even a tiny fraction of the $147 trillion traditional market flowing in could rapidly trigger explosive growth in the $80 billion DeFi market.

Many of these industry dividends exist only during this early stage. Currently, there are a handful of high-quality top-tier risk management teams globally. Large-scale institutional entry requires well-developed industry operating rules. Teams that build the foundational industry infrastructure first will firmly grasp the power to set the rules. Later entrants, while enjoying a more mature and better-regulated market environment, will have to compete within the established set of rules, missing the core influence and first-mover advantages of the early stage.