Nvidia Earnings Countdown: Beating Expectations Is Almost a Given, But Wall Street Cares Most About These Five Issues

- Core Thesis: BofA analysts believe that Nvidia's Q1 earnings "beating expectations" is essentially a certainty, shifting market focus to five key issues: shareholder returns, progress on the next-generation Vera Rubin chip, gross margin trends, and updated AI market size forecasts. Notably, significantly lower shareholder returns compared to peers are the core reason for its long-term valuation discount.

- Key Elements:

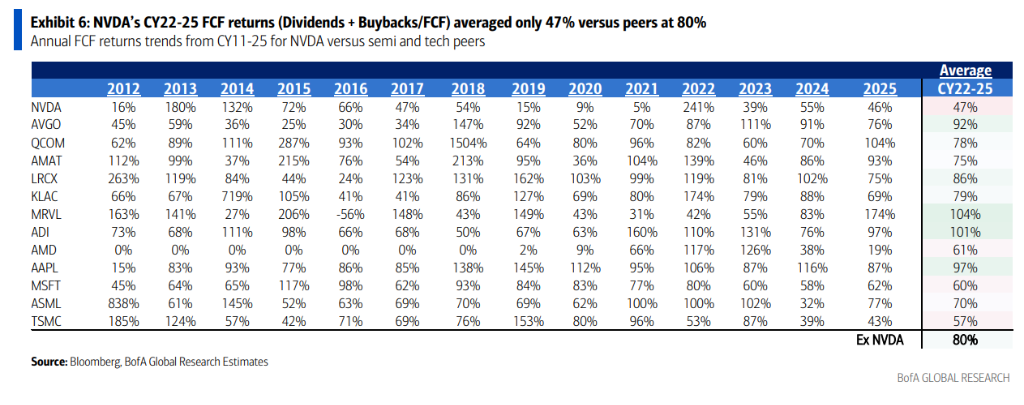

- Shareholder Returns: Nvidia's free cash flow return rate averaged only 47% from 2022-2025, far below the industry average of 80%. Its dividend yield is 0.02%, significantly lower than the peer average of 0.89%. This results in a nearly 50% valuation discount despite being the largest company in the S&P 500.

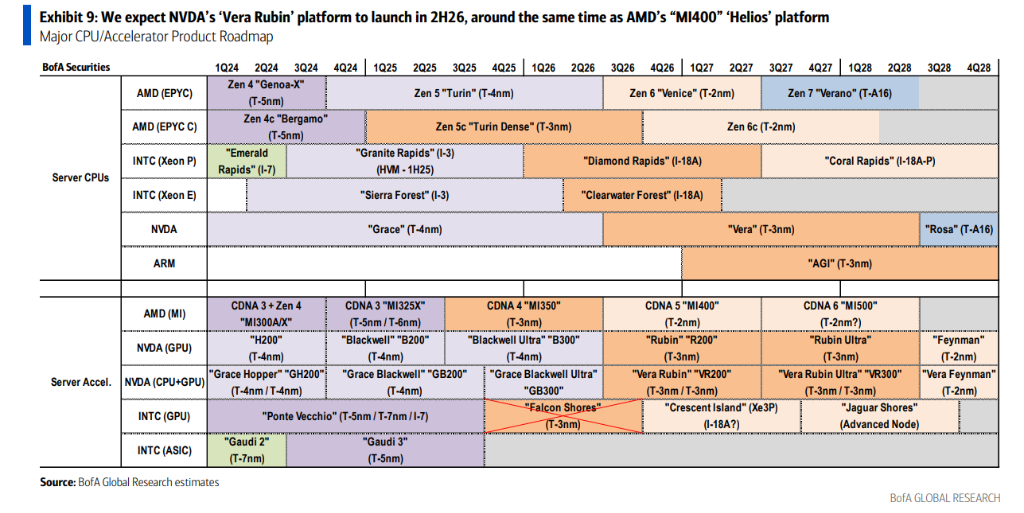

- Next-Gen Chip Vera Rubin: Expected to enter mass production in the second half of 2026, utilizing TSMC's 3nm process. The Vera Rubin Ultra is slated for the second half of 2027, featuring a new rack architecture.

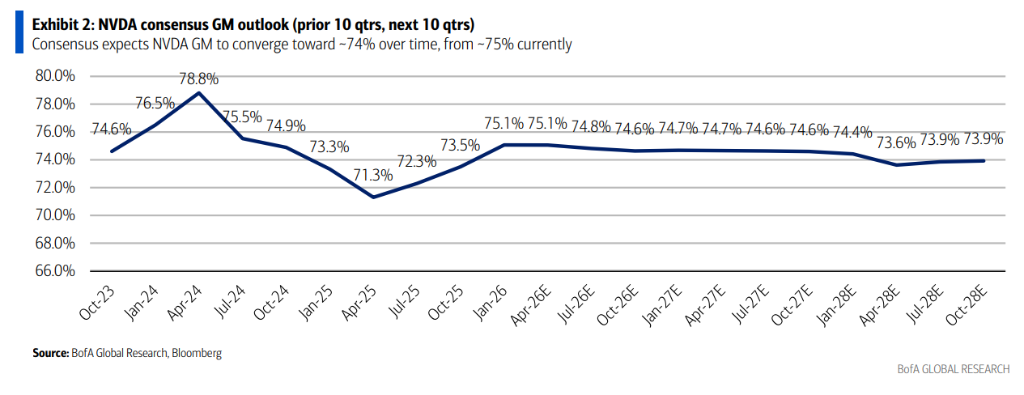

- Gross Margin Support: Market consensus expects gross margins to fluctuate in the 74%-75% range. In the short term, margins remain relatively stable due to a smooth product transition period. However, medium to long-term pressures arise from rising High Bandwidth Memory (HBM) costs.

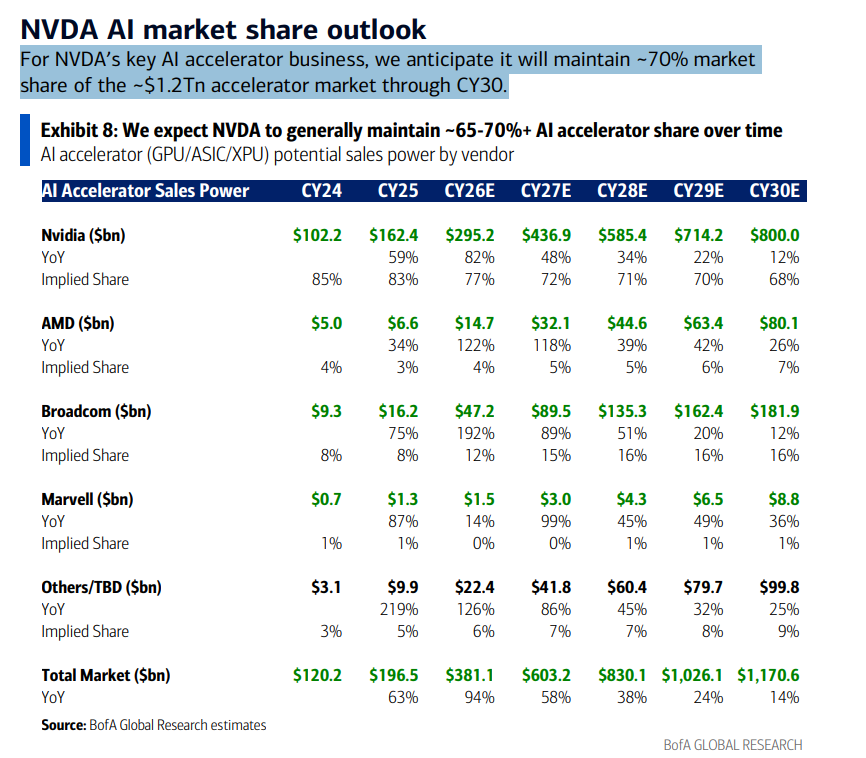

- AI Market Forecast: BofA projects the AI accelerator market size to reach approximately $1.17 trillion by 2030, with Nvidia maintaining a 68%-70% market share. Revenue is expected to grow from $102.2 billion in 2024 to $800 billion in 2030.

- Competitive Threat Assessment: Recent claims that CPUs are becoming more important than GPUs have been overstated. The actual deployment CPU to GPU ratio is 1:2. Furthermore, Nvidia will announce new progress on its in-house Vera CPU, making its AI dominance difficult to challenge in the near term.

Original author: Long Yue

Original source: Wall Street News

For NVIDIA's earnings season, the numbers themselves are no longer the most important thing.

On May 18th, a team of analysts led by BofA Securities analyst Vivek Arya released a preview report on NVIDIA's Q1 earnings, which is scheduled to be announced after the market closes on Wednesday, May 20th, Eastern Time.

According to NVIDIA's historical pattern over the past ten quarters, actual revenue has exceeded management's guidance by an average of 7% to 8%. Management previously provided F1Q27 revenue guidance of $78 billion. Based on this, actual revenue is likely to fall between $83 billion and $84 billion, while the current market consensus is only $78.7 billion.

In other words, "beating expectations" is almost a certainty. However, analysts believe that what will truly drive market sentiment after the earnings release are the following five questions.

Shareholder Returns: Can NVIDIA's "Stinginess" Change?

This is the most extensively discussed topic in the report and is considered the core reason for NVIDIA's long-standing valuation discount.

NVIDIA is currently the most valuable company in the S&P 500 index, accounting for 8.3% of the index weight, surpassing the historical peaks of Apple (7.9%) and Microsoft (7.2%). However, the issue is that NVIDIA's intensity of shareholder returns severely mismatches its massive size.

The data is straightforward: from 2022 to 2025, NVIDIA's free cash flow return rate (dividends + buybacks) averaged only 47%, compared to an average of 80% for comparable companies in the same industry during the same period. Even NVIDIA's own average over the earlier decade was 80%.

Meanwhile, NVIDIA's current dividend yield is only 0.02%, while the industry average is 0.89%. Among equity income funds, only 16% hold NVIDIA, whereas 57% hold Microsoft and 32% hold Apple.

Where has the money gone? The analysts point out that NVIDIA has invested heavily in its ecosystem – OpenAI, Anthropic, and technology partners. These investments are viewed controversially by some, with voices suggesting it is "circular financing," where NVIDIA lends money to customers who then use it to buy NVIDIA's chips.

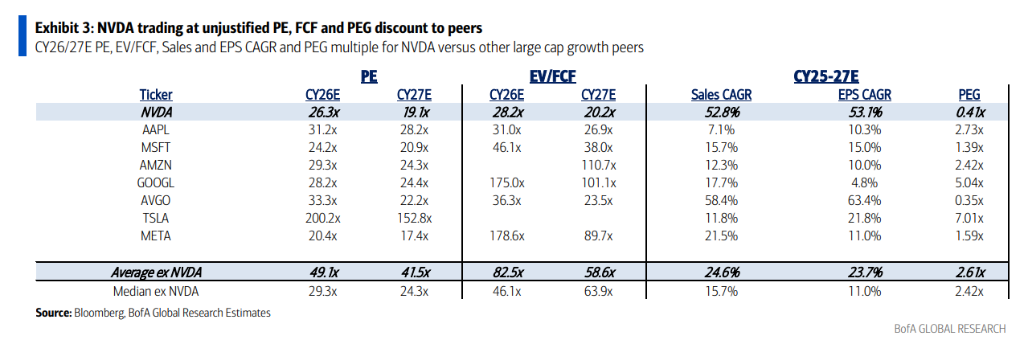

How significant is the valuation discount? Data shows NVIDIA's 2026/2027 forward P/E ratios are 26x/19x, while the average for the other members of the "Magnificent Seven" is 49x/42x, a discount of nearly 50%.

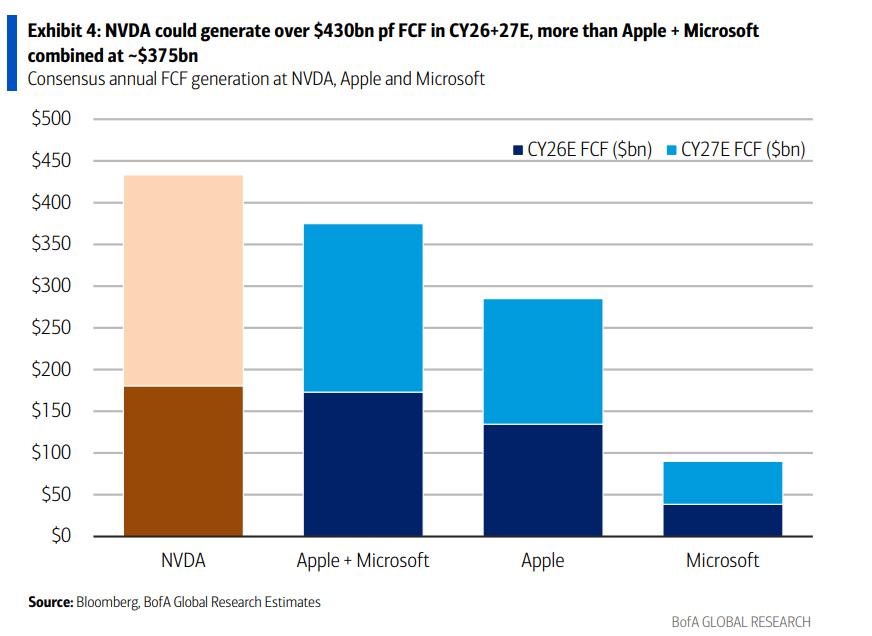

A more specific comparison: Analysts predict that NVIDIA's combined free cash flow for 2026 and 2027 will exceed $430 billion, higher than the combined total of approximately $375 billion for Apple and Microsoft. However, NVIDIA's market cap is around $5.46 trillion, about 28% lower than the combined $7.5 trillion of Apple and Microsoft.

Analysts believe that if NVIDIA increases its dividends and buybacks, it could attract more yield-seeking long-term capital, narrow the valuation discount, and also alleviate concerns about "circular financing." They list this change as a "potential catalyst for the second half of the year."

Vera Rubin: When Will the Next-Gen Chip Arrive?

NVIDIA's current flagship product is the Blackwell series. The market is concerned with: When will the next-generation Vera Rubin platform officially ramp up production?

The bank's judgment is the second half of 2026. Vera Rubin (codenamed R200) uses TSMC's 3nm process and shares the "Oberon" rack architecture with Blackwell Ultra, making the product transition relatively smooth and the expected impact on gross margin limited.

Looking further ahead, Vera Rubin Ultra (codenamed VR300) is expected to launch in the second half of 2027, adopting a new "Kyber" rack architecture, while the cost share of High Bandwidth Memory (HBM) is also expected to increase further.

The market also wants to hear NVIDIA's latest stance on the "trillion-dollar revenue forecast" during the earnings call. Previously, NVIDIA provided an outlook of $1 trillion in cumulative revenue for 2025-2027, but this did not include contributions from LPU (Language Processing Unit) racks, CPUs, and Vera Rubin Ultra. Will this be updated this time?

Gross Margin: Can the 75% Defense Line Hold?

Gross margin is one of the core pillars supporting NVIDIA's valuation.

Analysts' judgment: In the short term, since Vera Rubin uses Blackwell's rack architecture, the gross margin during the product transition period is relatively stable. However, medium to long term, the rising cost share of HBM memory is a persistent source of pressure.

Market consensus shows NVIDIA's gross margin fluctuating within the 74% to 75% range. The bank has no objection to this but emphasizes that any gross margin performance exceeding expectations would be a positive catalyst.

How Will the AI Accelerator Market Size Forecast Be Updated?

BofA previously provided a "trillion-dollar" forecast framework for the AI market covering NVIDIA from 2025 to 2027. This earnings season, the market is watching whether NVIDIA will update this forecast, especially by incorporating three previously unaccounted growth drivers:

- LPU (Language Processing Unit) Racks

- Vera CPU (NVIDIA's self-developed server CPU)

- Vera Rubin Ultra

The bank expects that by 2030, the overall AI accelerator market size will reach approximately $1.17 trillion, with NVIDIA maintaining a market share of about 68% to 70%.

Specifically, NVIDIA's AI accelerator revenue is expected to grow from $102.2 billion in 2024 to $800 billion by 2030, while AMD's grows from $5 billion to $80.1 billion, and Broadcom's from $9.3 billion to $181.9 billion over the same period.

Are the Competitive Threats from Google TPUs and CPUs Exaggerated?

Recently, a narrative has circulated in the market suggesting that as AI enters the "Agentic AI" era, the importance of CPUs will surpass that of GPUs, thus threatening NVIDIA's moat.

The bank explicitly disagrees with this view, providing two reasons:

First, NVIDIA's self-developed "Vera CPU" will have new developments disclosed at the upcoming Computex conference, and its competitiveness in the standalone CPU market should not be underestimated.

Second, in the currently large-scale deployed Blackwell and TPU clusters, the ratio of CPUs to GPUs is already 1:2, which does not align with the narrative that "Agentic AI requires more CPUs."

The conclusion: Although the CPU market is large, it is highly competitive (with strong rivals in both x86 and ARM architectures). NVIDIA's dominant position in the GPU/AI accelerator field is unlikely to be shaken in the short term. It is estimated that by 2030, NVIDIA will maintain approximately 70% of revenue share in the total AI addressable market of over $1.7 trillion.

Valuation: The "Top Tech Stock" at a 50% Discount

Finally, back to valuation. The report uses a set of data to directly highlight NVIDIA's current valuation paradox.

Based on CY26/27 forward P/E ratios, NVIDIA stands at 26x/19x, while the average for the "Magnificent Seven" (Mag-7) is 49x/42x – a nearly 50% discount for NVIDIA.

Based on EV/FCF (Enterprise Value to Free Cash Flow), NVIDIA is at 28x/20x, while the Mag-7 average is 83x/59x – a discount of over 66%.

Based on PEG (Price/Earnings to Growth) ratio, NVIDIA is at 0.41x, the Mag-7 average is 2.61x, and the S&P 500 overall is above 1.3x.

BofA maintains a "Buy" rating and a price target of $320, based on a CY27 forward P/E ratio of 28x (excluding cash), which is in the mid-to-low range of NVIDIA's historical valuation band of 25x to 56x.