Duan Yongping Builds a Position in Circle – What is He Betting On?

- Core Thesis: Duan Yongping’s family office has built a position in Circle (CRCL) for the first time, marking the formal acceptance of compliant stablecoin assets by traditional capital. Circle is attempting to transform from an "interest coupon" model highly dependent on interest rates into a payment infrastructure, leveraging the launch of its Layer-1 blockchain Arc and the AI agent toolkit Agent Stack. This move aims to address structural challenges such as a single revenue stream, the revenue-sharing agreement with Coinbase, and regulatory competition.

- Key Elements:

- H&H International, affiliated with Duan Yongping, established its first position in Circle, with a market value of $19.08 million, symbolizing the recognition of Web3 compliant assets by traditional value-investing capital.

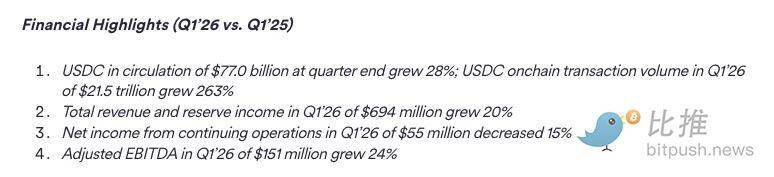

- Circle’s Q1 results show USDC in circulation reached $77 billion, with on-chain transaction volume hitting $21.5 trillion. However, 99% of its 2024 revenue came from reserve interest, making it highly dependent on the interest rate cycle.

- For its Layer-1 blockchain Arc, Circle raised $222 million through a token presale (with a $3 billion FDV), led by a16z, with participation from BlackRock and Apollo. This formally ushers tokenized assets into Wall Street.

- Arc is designed to help Circle break free from its profit-sharing agreement with Coinbase (which cost Circle $908 million out of its total revenue in 2024), by building a self-controlled on-chain infrastructure.

- Circle Agent Stack is aimed at AI agent development, supporting USDC micropayments, as it vies with Stripe (Bridge), Ramp, and others for the "banking for robots" market.

- The GENIUS Act allows banks to issue stablecoins, exerting regulatory competitive pressure on Circle. Arc serves as a defensive strategy to create network effects and switching costs.

- Analysis predicts that Circle’s non-reserve revenue will account for only 6% in 2026. Businesses like Arc are still in their early stages, and the current valuation likely reflects the option value of this transformation rather than actual performance.

Original source: Fintech Blueprint

Compiled and organized by: BitpushNews

Yesterday, the U.S. SEC disclosed the latest quarterly 13F holdings report. Duan Yongping, hailed as the "Chinese Warren Buffett," executed a major portfolio shift in his quietly managed family wealth and charitable fund account, H&H International Investment LLC (with assets exceeding $20 billion)—making an unprecedented initial purchase of compliant stablecoin giant Circle (Ticker: CRCL), with a holding value of $19.08 million.

As a staunch value investor, Duan Yongping has earned fame for heavy positions in Apple and Kweichow Moutai, adhering to the philosophy of "not investing in what you don't understand." This move into Circle not only signifies the formal acceptance of Web3 compliant assets by traditional legacy capital. This article delves into Circle's Q1 performance and latest product布局, examining whether this stablecoin giant can pivot its business model from "interest-driven" to "infrastructure-driven" through a fundamental restructuring of its underlying architecture.

Here is the main content:

Circle has had a busy week.

Alongside the release of its Q1 2026 results—total revenue and reserve interest income approaching $700 million (up 20% year-over-year), USDC circulation reaching $77 billion, and on-chain transaction volume hitting $21.5 trillion—the company also made two major product announcements and completed a $222 million token pre-sale.

Changing the "Interest Rate Voucher" Label

For a long time, Circle has been labeled as an "interest rate agency tool": 99% of its 2024 revenue came from interest earned on USDC reserve assets.

This makes the business extremely sensitive to the interest rate cycle and leaves equity investors with little valuation basis beyond net interest income and USDC circulation growth. Arc (its Layer-1 blockchain), the Circle Agent Stack (agent technology stack), and the Payments Network represent Circle's concentrated effort to change this status quo—aiming to diversify revenue and revalue the stock's valuation logic from "yield multiples" to "infrastructure multiples."

Perhaps most unusual is this: Circle, a publicly traded company with a traditional equity structure, raised $222 million through a token pre-sale for its new stablecoin-focused Layer-1 blockchain, achieving a fully diluted valuation (FDV) of $30 billion.

In finance, some instruments go on a standard Cap Table, while others are protocol-specific tokens. Notably, Coinbase's Ethereum L2 network, Base, has not yet issued a token. A multi-billion dollar publicly listed company completing such a token raise signifies that tokenized assets have officially arrived on Wall Street.

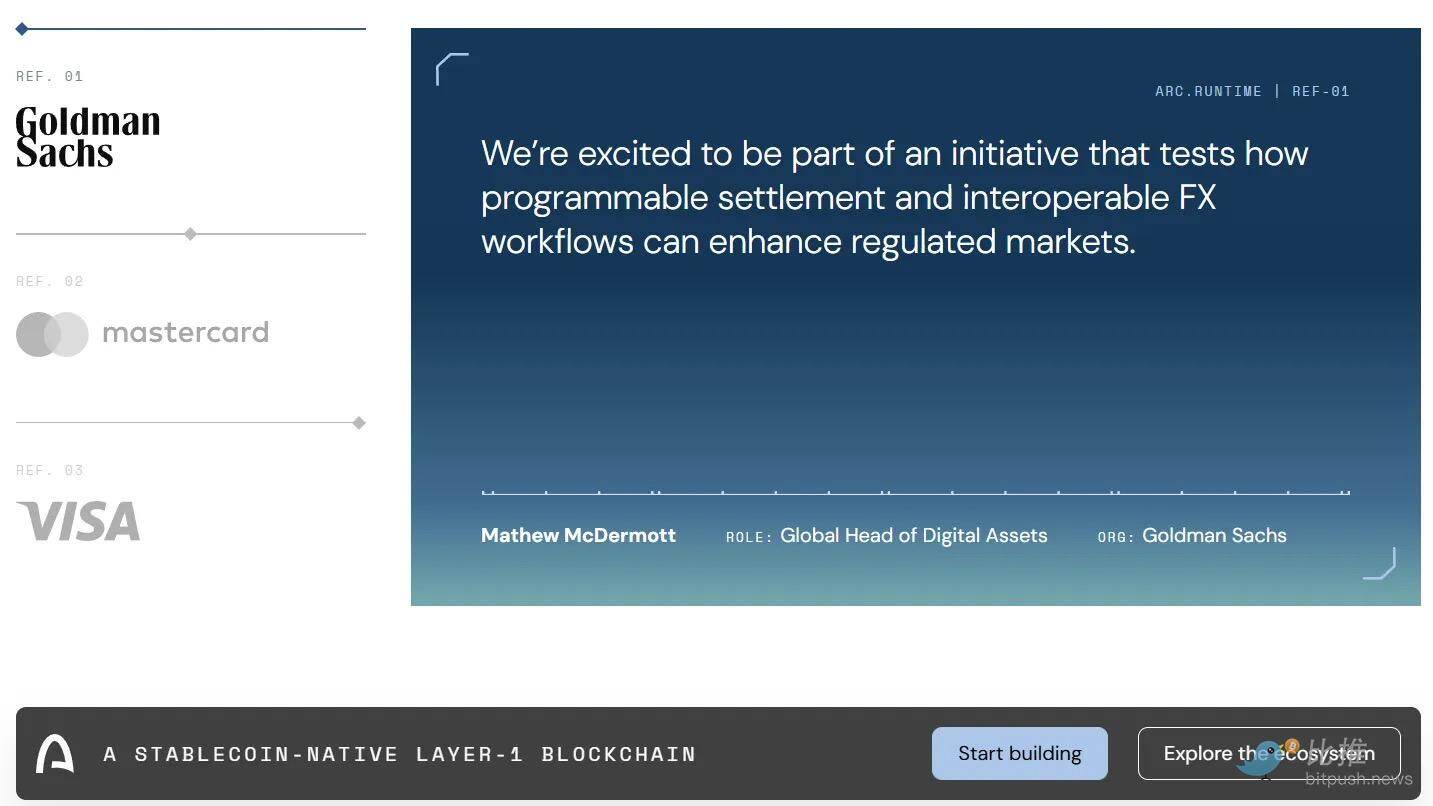

This round was led by Andreessen Horowitz (a16z), committing $75 million, with participation from BlackRock and Apollo. The pre-sale involves multi-year lock-up periods; investors also have repayment rights if Arc network fails to meet key milestones.

Circle holds 25% of the initial 10 billion token supply, with 60% allocated to network participants and 15% reserved as a long-term reserve. The Arc mainnet is expected to launch in the summer of 2026, and as of early May, its testnet had processed 244 million transactions.

Currently, the utility of the ARC token is still in the exploratory phase. This means you can still raise over $200 million today without a fully designed tokenomics. And, upon closer inspection, building a Layer-1 blockchain doesn't actually require $200 million either.

Alongside Arc, Circle also unveiled the Circle Agent Stack—a toolkit for developers to build "AI agents that transact using USDC," including wallets, a marketplace, and a nanopayments layer supporting transfers as low as $0.000001.

With this, Circle joins Stripe, Coinbase, Visa, Mastercard, Shopify, Fiserv, and Brex in the race to "provide banking services for bots."

Arc is a Defensive Play

Today, USDC operates across dozens of public chains and wallets like Ethereum and Solana. Circle earns interest income from all these reserve assets. The problem is how much of that income it can actually retain.

According to the 2023 Cooperation Agreement signed with Coinbase (created when the Centre Consortium dissolved, giving Coinbase, as Circle's largest distribution channel, significant bargaining power), the distribution of reserve interest income follows a three-step process:

- Circle first takes a small issuer fee at the top.

- Then, both parties receive their respective share of reserve interest income based on the proportion of USDC held in their respective custody products.

- As for the remaining profit—Coinbase takes 50% directly.

The result is that Coinbase extracts a portion of reserve interest income even from USDC not held in its custody.

In 2024, out of Circle's total revenue of $1.68 billion, a significant $908 million was ceded to Coinbase. This agreement auto-renews every three years, and Circle has no unilateral right to exit. Therefore, Arc represents Circle's effort to build its own fully controlled underlying infrastructure, directly earning fees from it.

To reiterate: Coinbase enjoys a 50% "net clipping right" over virtually all of Circle's revenue, and Circle has no escape route other than finding a clever "back door."

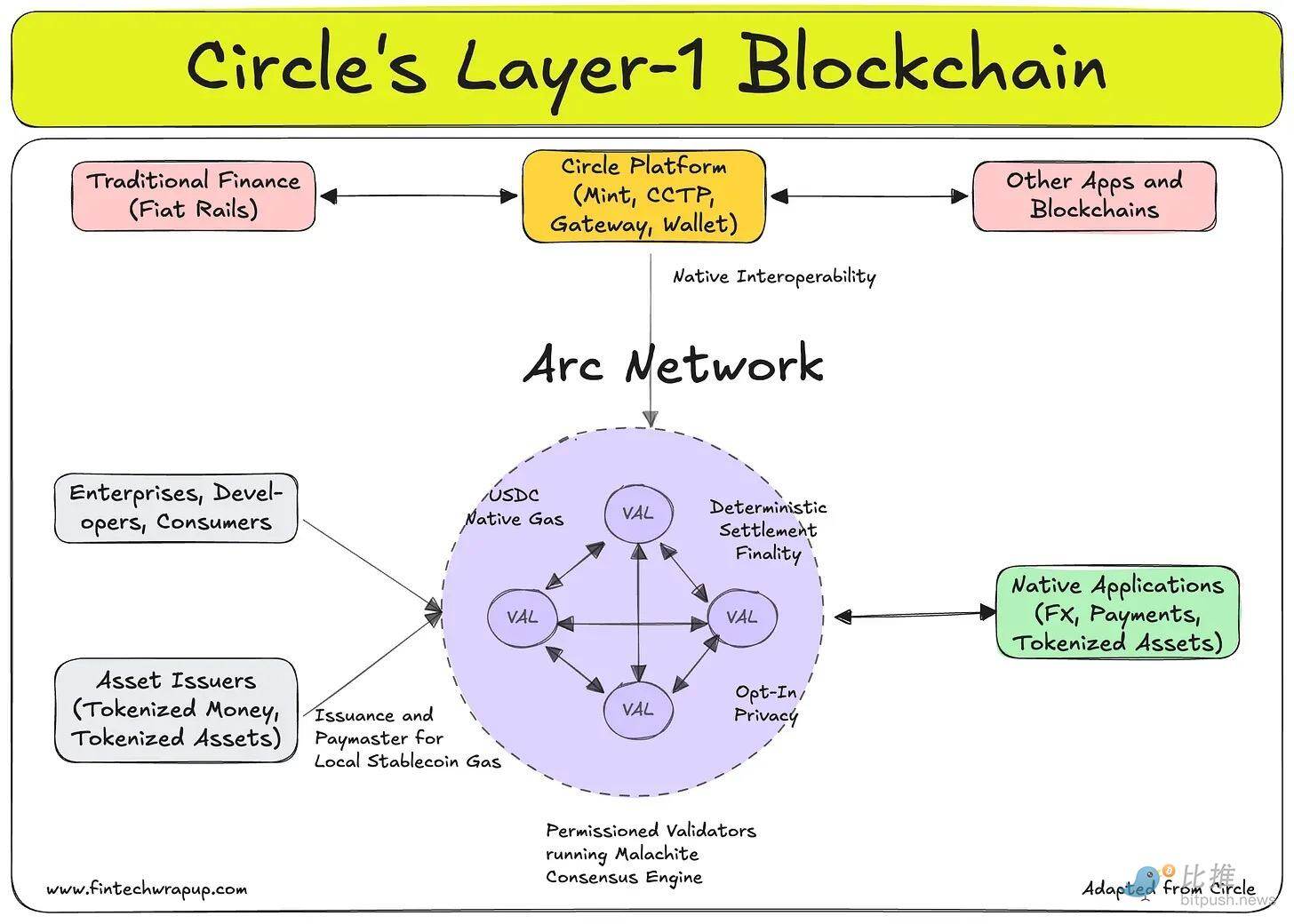

Arc's value proposition for user acquisition is straightforward: a Layer-1 blockchain purpose-built for stablecoin-native finance. It uses USDC as the gas token, features sub-second transaction finality, optional privacy, EVM compatibility, and quantum-resistant architecture. For institutions whose core business involves fund transfers, it represents a new generation of settlement infrastructure and an alternative to ACH, SWIFT, and correspondent banking.

Launched as a testnet in October 2025, it has already attracted over 100 institutional participants including BlackRock, Goldman Sachs, Visa, and State Street, processing 244 million transactions.

To be fair, similar institutions have previously joined Tempo and various AI payment and agent protocols we've covered. This shows the industry is diversifying in restructuring payment rails.

In contrast, the $30 billion FDV associated with the pre-sale seems harder to justify. The functionality of the ARC token is still being explored. Investors are essentially betting on the option value of Circle owning the "stablecoin settlement mother chain"—thereby closing the vertical ecosystem loop and plugging the current value leakage to third parties. Whether this option is worth $30 billion depends on future transaction volumes. Specifically, it hinges on Circle's ability to migrate a sufficient share of its current $77 billion circulation onto Arc, generating enough service fees to support that valuation.

Simultaneously, the regulatory backdrop intensifies this urgency.

The GENIUS Act, signed into law in July 2025, explicitly paves the way for banks to issue their own payment stablecoins through subsidiaries, under the supervision of their existing federal regulators. JPMorgan and Bank of New York are already running tokenized deposit pilots. Once regulated bank-issued dollar tokens reach scale, market demand for third-party stablecoin issuers like Circle could narrow.

Arc doesn't directly solve this, but owning proprietary on-chain infrastructure can create network effects and switching costs. It's a defensive line against the risk of everyone from Canton to Ripple to JPMorgan's Kinexys potentially capturing profit or vertically integrating.

Circle Agent Stack is an Offensive Play

The Agent Stack is a developer toolkit for building AI agents that can transact using USDC. It comprises wallets, a marketplace, and a nanopayments layer enabling transfers as low as $0.000001. The core logic: as AI agents autonomously handle more operational and financial tasks, the transaction sizes and granularity they require will be unsupported by existing payment rails (like card networks, ACH, SWIFT) due to high fixed costs (making fractional cent transactions economically unfeasible). A programmable, micro-payment capable USDC-native chain has no such cost floor. For an AI agent needing to pay per API call, per second of compute, or per data query, there is currently no perfect solution in the market.

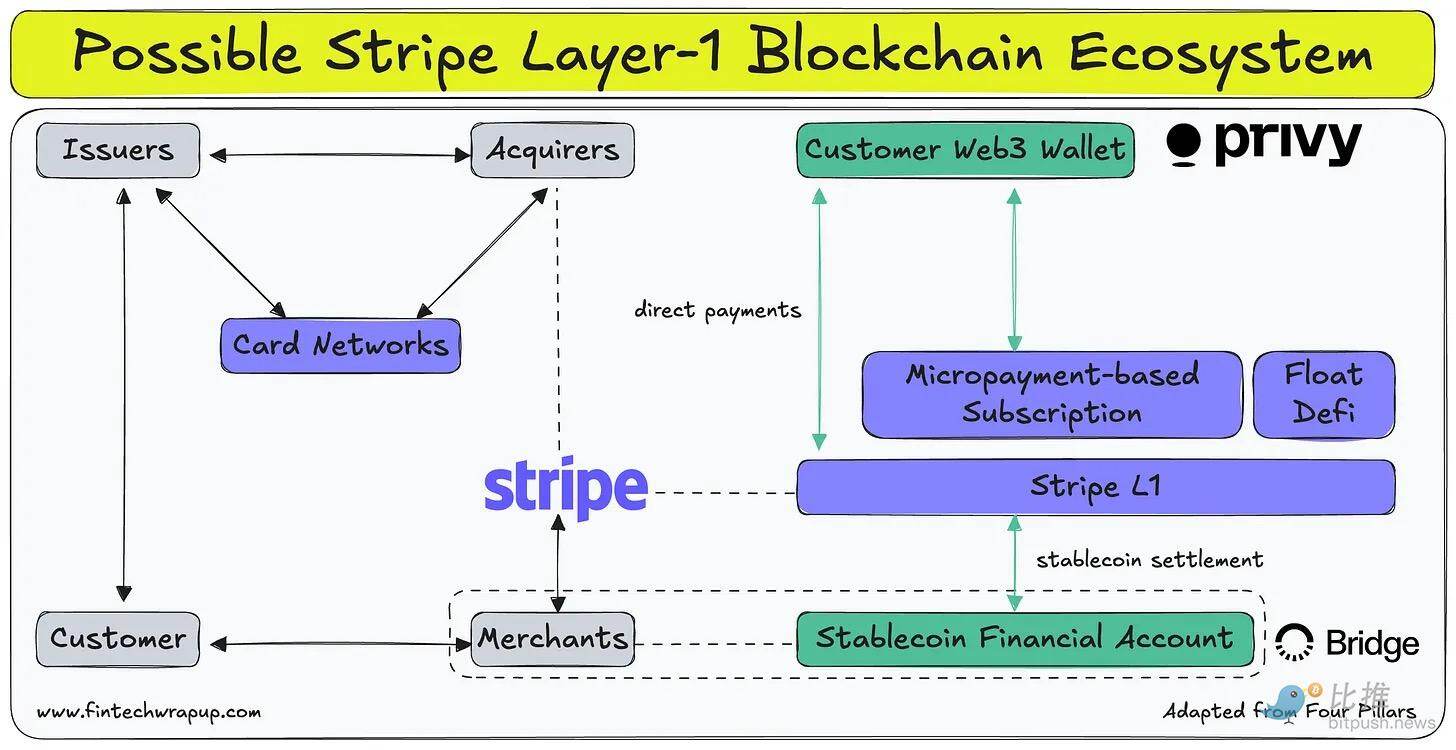

Ramp launched Agent Cards in March 2026. Simply put, it allows businesses to issue virtual cards for autonomous agent spending. Stripe, after acquiring Bridge in late 2024, also has its own answer: issuing agent-specific cards via Bridge, providing wallet infrastructure via Privy, and supporting stablecoin payment acceptance in 32 markets.

- Ramp's Agent Cards: Built for enterprise expense control.

- Circle's Agent Stack: Focused on USDC-native micropayments on the Arc chain.

- Stripe: Positions itself as a full-stack layer (offering fiat, stablecoin, and wallet infrastructure under one API).

The Circle vs. Stripe Showdown

Circle's structural advantage lies in the asset itself.

USDC is the dominant compliant stablecoin, serving as the unit of account for a large portion of on-chain activity. Stripe's Bridge, on the other hand, enables issuing its own stablecoins via "Open Issuance." USDH, one of Bridge's flagship issuances, was shut down this week after failing to compete with $5 billion in USDC on Hyperliquid, leading Coinbase to step in as the official USDC treasury deployer. Building agent infrastructure on top of USDC means agents inherit existing liquidity and network depth from day one. This asset advantage has proven much harder to replicate than it might seem.

As mentioned, Stripe also incubated Tempo—a Layer-1 blockchain specifically tailored for payments. However, Tempo is positioned as a general-purpose payment settlement layer supporting any stablecoin, whereas Arc is built entirely around USDC. Both companies are betting that the future of payments will be settled on customized proprietary chains, rather than general-purpose chains like Ethereum.

Differences in capital structure are also noteworthy. Circle raised $222 million for Arc via a pre-sale ($30 billion FDV). Stripe is privately held, consistently profitable, and valued at $70 billion—it can easily use its own balance sheet cash to fund Tempo and Bridge's expansion without diluting equity via tokens.

The ways these two companies can deploy ammunition to absorb and subsidize the cost of bootstrapping a new chain ecosystem are fundamentally different.

Ultimately, the capabilities and inclinations of a "payment processor (like Stripe)" versus a "cash-equivalent financial instrument issuer (like Circle)" are vastly different. The former excels in distribution, sitting amidst countless merchants and customers. The latter has its asset embedded in every exchange and crypto wallet. We believe blindly pursuing vertical integration and entering an expensive arms race would be a mistake.

The Arithmetic of the Income Statement

Circle's business model today is simple: $77 billion USDC in circulation earns approximately 4.1% return on reserve assets, a significant portion of which flows to Coinbase according to distribution agreements. Its full-year 2025 revenue was $2.75 billion.

Analysts forecast 2026 revenue around $3.2 billion, implying about 15% growth. This is quite modest compared to last year's 64% growth rate, reflecting two real headwinds:

- Falling interest rates compressing reserve asset yields;

- The GENIUS Act imposing limits on how reserve income is shared with distribution partners, putting the Coinbase agreement under regulatory scrutiny.

New products must be understood in this context. Circle estimates non-reserve income for 2026 at $150 to $170 million, higher than 2025's $110 million, but still less than 6% of total revenue. Arc transaction fees, Agent Stack developer revenue, and CPN (Circle Payments Network) fees are all at very early stages. To achieve the valuation re-rating from "interest rate agency tool" to "infrastructure platform," these business lines not only need to grow in absolute terms but also need a substantial increase in their revenue share. Based on the current trajectory, Circle's narrative is running ahead of its financial numbers.

The stock's movement reflects this tug-of-war. CRCL was IPO'd at $31 in June 2025, briefly surged to near $300, then retreated to stabilize around $114. After the Q1 results, JPMorgan raised its price target to $155, Needham to $150, while Deutsche Bank gave $101. Consensus market expectations hover between $125 and $130, implying very cautious upside from current levels.

Bull vs. Bear Case

The bull case requires three conditions to materialize simultaneously:

- USDC circulation grows fast enough to offset the impact of declining reserve yields;

- Arc generates meaningful fee income, partially replacing or circumventing the Coinbase cooperation agreement;

- The Agent Stack establishes an early lead as the underlying infrastructure for agent payments before Stripe overwhelms it with scale.

If all three are met, Circle will have successfully transformed into a payment infrastructure company, with its valuation multiple driven by transaction volumes and network effects, rather than being hostage to the Fed's interest rate cycle.

The bear case is much simpler:

Interest rates fall faster than circulation grows; restructuring the Coinbase agreement reduces distribution channels without effectively compensating with volume; Arc fails to migrate enough USDC onto its own chain; Stripe or Ramp launch superior agent infrastructure at lower cost, encircling Circle.

Circle's announcements are strategically the right moves. But for now, they remain chips and bets, not yet transformed into real business. Circle is asking investors to pay for the option value of these three things happening simultaneously, while its core business model faces genuine structural headwinds. This demand isn't unreasonable—it just seems expensive at current valuation levels.