The world is grappling with a new wave of inflation as a "long-term bond storm" sweeps across the globe

- Core Thesis: Conflict in the Middle East has pushed up oil prices and inflation expectations, causing long-term U.S. Treasury yields to surge to their highest levels since 2007 and triggering a global bond sell-off. Markets now expect the Federal Reserve to raise interest rates rather than cut them, potentially marking the beginning of a new era of sustained high interest rates.

- Key Elements:

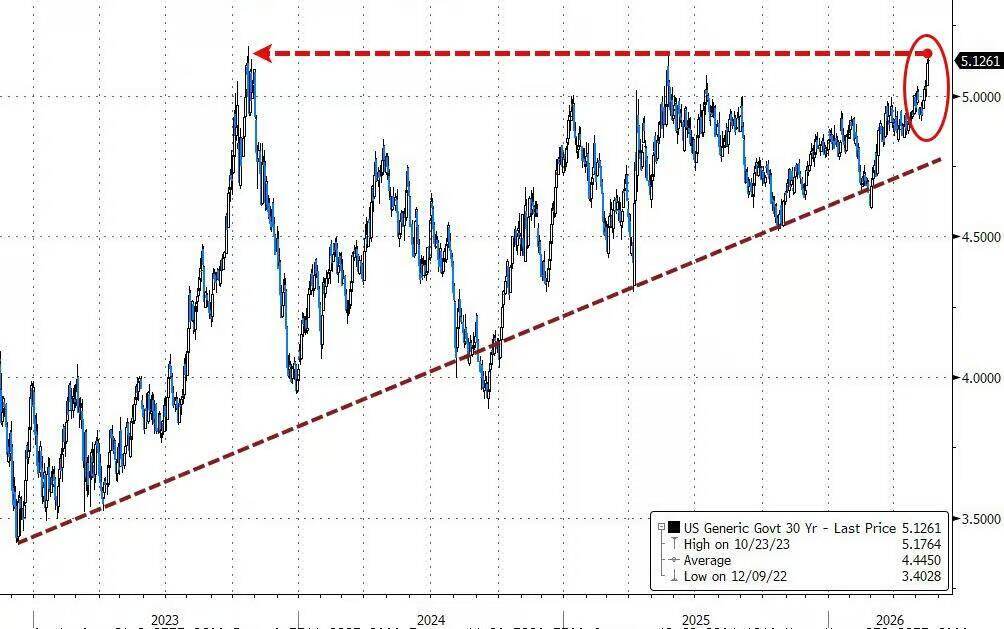

- The U.S. 30-year Treasury yield has broken through 5%, hitting a 16-year high. Demand at the 30-year auction was tepid, indicating a lack of buying appetite from investors even at these elevated levels.

- Traders now view a rate hike next March as a high-probability event, a fundamental reversal from late February when the market had priced in rate cuts by 2026. The inflation narrative now dominates market pricing.

- The blockade of the Strait of Hormuz continues to drive up oil prices and inflation expectations, becoming the core driver of bond market turmoil. Unless this situation changes, pressure on the bond market is unlikely to dissipate.

- Markets fear the next CPI report could show annual inflation at 4%, the highest level since 2023. The expanding U.S. fiscal deficit further reinforces the demand for term premium compensation.

- JPMorgan's survey of U.S. Treasury investors shows short positions at their highest in 13 weeks, indicating increased bets on further declines in the bond market. Some investors have chosen to remain on the sidelines.

Original author: Zhao Ying

Original source: Wall Street Sights

The global bond market is at a historic inflection point. Surging oil prices triggered by the conflict in the Middle East and rising inflation expectations are pushing U.S. Treasury yields to two-decade highs, triggering a cascade of sell-offs in major markets such as the UK and Japan. A new era of persistently high interest rates may have quietly begun.

The yield on the 30-year U.S. Treasury bond has breached the 5% threshold, reaching its highest level since 2007. Despite such elevated levels, demand was lackluster in last week's 30-year bond auction, failing to ignite buying enthusiasm. Meanwhile, market expectations for the Federal Reserve's policy path have undergone a fundamental reversal. Traders now see a rate hike next March as a high-probability event, with about a three-in-four chance by December. This contrasts sharply with expectations from late February this year, when the market anticipated two rate cuts by 2026.

This bond market turmoil has weighed on equities and drawn high-level attention from G7 finance ministers, who will specifically discuss this round of bond selling at their meeting this week. Priya Misra, a portfolio manager at J.P. Morgan Asset Management, warned, "The synchronized rise in long-end yields globally tends to reinforce itself, and expectations of a Fed rate hike are now entering the market narrative."

Iran Conflict Flips Bond Market Narrative

The blockade of the Strait of Hormuz is the core driver of this bond market turmoil. Disruption to this critical global oil shipping route continues to push up oil prices and reignite inflation expectations.

Investors broadly believe that as long as the standoff in the Middle East remains unresolved, pressure on the bond market will be difficult to dissipate. Priya Misra stated bluntly, "Unless the strait reopens, the entire interest rate range has shifted higher."

Data shows that U.S. Treasury yields are currently about 50 basis points or more above their levels from late February. The 2-year yield briefly rose to 4.09%, its highest since February 2025; the 10-year yield stood at 4.58%, a near one-year high. Year-to-date, U.S. Treasuries have posted negative returns overall, compared to gains of nearly 2% earlier in the year by the end of February.

Inflation Narrative Dominates Market Pricing

The market's core concern is the re-anchoring of inflation expectations. Karen Manna, fixed-income strategist and portfolio manager at Federated Hermes, stated, "We are witnessing a world that is genuinely dealing with a new wave of inflation."

Kevin Flanagan, Head of Fixed Income Strategy at WisdomTree, expects the next Consumer Price Index report to show an annual inflation rate of 4%, the highest level since 2023 – April CPI already came in at 3.8%. He noted, "The inflation narrative is dominating the market. The bond market demands higher premium compensation for holding newly issued Treasuries."

Concerns over the persistent expansion of the U.S. fiscal deficit, coupled with signs of economic resilience despite wartime headwinds, further strengthen the logic for investors demanding higher term premiums. Last week's Treasury auctions confirmed this: the 30-year bond auction rate hit 5%, the first time since 2007, but demand was tepid; investor demand for the 3-year and 10-year auctions was also lackluster.

Rate Hike Expectations Reshape Fed Outlook

This inflation storm also puts immense pressure on incoming Fed Chair Kevin Warsh, dashing market bets on rapid rate cuts after he takes office.

Austan Goolsbee, President of the Chicago Fed, said last week that broad price pressures could even signal an overheating economy; Fed Governor Michael Barr called inflation an "overwhelming" risk to the economy. The Fed's April meeting minutes are due Wednesday, and the market will closely watch how much support the dissenting committee members garnered among officials.

In the latest J.P. Morgan U.S. Treasury Investor Survey, bearish positions on Treasuries reached their highest level in 13 weeks, indicating a clear increase in market bets on further bond market declines.

Investors on Sidelines, Awaiting More Signals

Faced with persistent selling pressure, some investors are choosing to stay put. Kevin Flanagan said he is currently sticking with floating rate notes and maintaining lower interest rate exposure, preferring to "buy late rather than too early." He considers the 4.5% level on the 10-year yield "more of a psychological threshold," adding that if the Middle East situation escalates further, pushing oil prices higher, yields could retest last year's high of 4.62%.

Hank Smith, Head of Investment Strategy at Haverford Trust, adopts a more cautious stance. He stated that whether the rise in consumer and producer prices is temporary "or will extend into 2027" remains an open question, requiring more data to judge the direction of the bond market.