半年狂赚500亿,长鑫科技从「碎钞机」到「印钞机」的逆袭

- 核心观点:中国DRAM芯片制造商长鑫科技凭AI驱动的存储芯片超级周期,在2026年上半年实现归母净利润500-570亿元,从连年巨亏的“碎钞机”逆袭为日赚近4亿的“印钞机”,正冲刺科创板IPO。

- 关键要素:

- 业绩爆发:2026年Q1营收508亿元(同比+719%),扣非净利润263.4亿元(同比+1993%);半年利润已追平国家能源集团全年水平。

- 亏损历史:截至2025年底累计亏损366.5亿元,2023-2024年分别亏损163.4亿和71.45亿元,十年投入填平芯片制造“无底洞”。

- 核心驱动力:AI大模型对DRAM需求达传统服务器8-10倍,叠加三星等巨头转产HBM,致通用DRAM供需极端错配,价格创2016年来新高。

- 产能与份额:北京、合肥3座12英寸晶圆厂,产能利用率达94.63%;全球DRAM市场份额从2025年Q2的3.97%升至Q4的7.67%,排名全球第四。

- 周期风险:DRAM强周期性为隐忧,但本轮由AI结构性需求驱动,预计供应缺口超20%且持续至2030年,可持续性高于传统消费电子周期。

- 估值争议:IPO拟募资295亿元(科创板历史最高),隐含估值约2950亿元;市场预期短期万亿、长期两万亿,并含国内稀缺性溢价。

Original Author: Xu Chao

Original Source: Wall Street News

With a net profit of 24.7 billion in a single quarter and nearly 57 billion in half a year, this chip company—once mired in years of massive losses and dubbed a "money incinerator" by the market—is staging the most astonishing earnings turnaround in China's tech history.

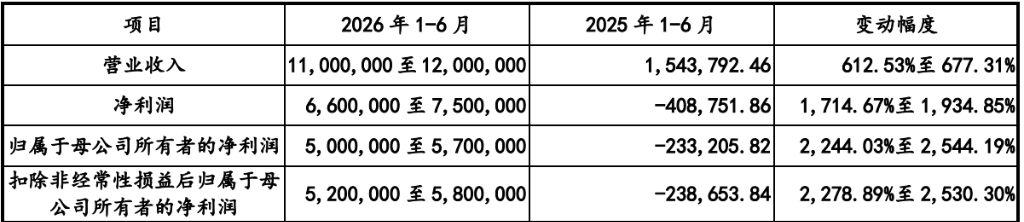

On May 17, ChangXin Memory Technologies (CXMT) updated its IPO prospectus for the STAR Market, revealing a set of figures that sent shockwaves through the capital market: In the first quarter of 2026, the company's revenue hit 50.8 billion yuan, a staggering 719% year-on-year increase; its net profit attributable to parent after deducting non-recurring gains and losses reached 26.34 billion yuan, up 1,993.41% year-on-year. The company expects H1 2026 revenue to be between 110 billion and 120 billion yuan, representing 612.53% to 677.31% growth, with net profit attributable to parent ranging from 50 billion to 57 billion yuan, a surge of 2,244% to 2,544%.

To grasp just how extraordinary this performance is, a horizontal comparison makes it clear.

Among non-financial A-share companies, only three—PetroChina, China Mobile, and CNOOC—recorded a full-year net profit exceeding 100 billion yuan in 2025. Kweichow Moutai was at 80 billion+, CATL at 70 billion+, and even China Energy Engineering Group, ranked sixth, stood at 52.9 billion. CXMT, with just half a year's net profit, has already matched China Energy Engineering Group's earnings level, thrusting itself into the top tier of these six non-financial A-share giants.

Even more staggering: if this data is linearly extrapolated, CXMT's net profit for the full year 2026 is expected to potentially surpass 100 billion yuan. Consequently, this chip company's annual profitability is chasing the profit scale of those former oil state-owned enterprises.

Yet, just over a year ago, this company was a veritable "money incinerator."

The Abyss of Past Losses: 36.6 Billion Yuan Burned in Three Years

Looking at CXMT's historical public financial data: it lost 16.34 billion yuan in 2023, 7.145 billion yuan in 2024, and as of December 31, 2025, its accumulated losses totaled a staggering 36.65 billion yuan. For nearly a decade, CXMT poured almost every yuan it raised into the bottomless pit of chip manufacturing.

So, how did this "money incinerator" transform into a "money printer," earning nearly 400 million yuan a day, in less than half a year?

The answer lies in two keywords: AI and chip shortage.

An Epic Super Cycle: AI is "Devouring" Memory

The world is experiencing an epic memory chip cycle.

The root of this super boom cycle is AI large language models' "brute-force consumption" of memory.

Each model inference fundamentally involves massive data retrieval between GPUs and memory. A single AI server's demand for DRAM is 8 to 10 times that of a traditional server. As global cloud providers and AI computing infrastructure investments continue to accelerate, DRAM demand is experiencing a structural explosion.

Meanwhile, the three major camps—Samsung, SK Hynix, and Micron—are shifting significant advanced production capacity towards the higher-profit HBM (High Bandwidth Memory), severely squeezing the production line resources for general-purpose chips like DDR4 and DDR5.

This extreme mismatch between supply and demand has driven historical peaks in DRAM prices.

TrendForce data shows that in Q1 2026, DRAM contract prices surged by 93% to 98% quarter-over-quarter; Q2 maintained an expected increase of 58% to 63%. Data from the National Development and Reform Commission's Price Monitoring Center indicates that as of January 2026, mainstream DRAM product prices have hit their highest historical records since 2016. All of Samsung, SK Hynix, and Micron's production capacity for 2026 has already been announced as sold.

Industry institutions predict this memory boom could last until 2030, with a supply gap exceeding 20%.

Optimal Volume and Price: CXMT Hits the Sweet Spot

In this epic memory super cycle, CXMT hasn't just caught the wave; its years of strategic positioning have allowed it to maximize the benefits of the industry boom.

Founded in 2016, CXMT is currently the only company in mainland China that has truly achieved large-scale DRAM mass production as an IDM (Integrated Device Manufacturer)—covering the entire chain from design and manufacturing to packaging and testing independently. The company owns three 12-inch fabs in Beijing and Hefei, with capacity utilization climbing to 94.63% in 2025.

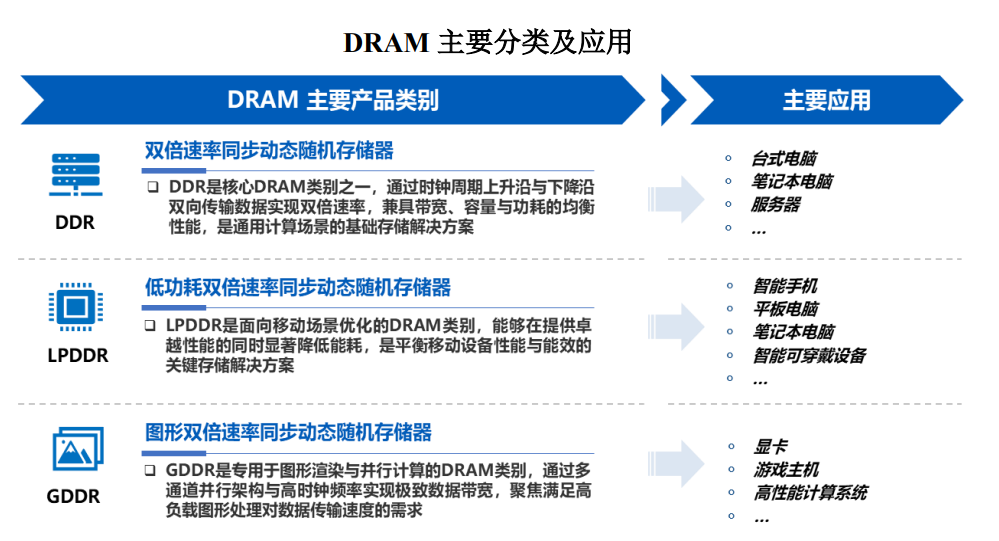

On the product front, CXMT has completed a comprehensive upgrade from DDR4 to DDR5 and from LPDDR4X to LPDDR5/5X. The continuous push for high-end products has directly amplified the profit elasticity brought by price increases.

In terms of market share, according to Omdia data for Q4 2025 DRAM sales revenue, CXMT's global market share has increased to 7.67%, ranking fourth globally and first in China. From 3.97% in Q2 2025 to 7.67% in Q4, the company's market contribution nearly doubled in just six months.

The result: surging volume and prices, leading to an explosion in profits.

Zhu Yiming's Decade-Long Bet: No Salary Until Profitability

CXMT's journey to this point is inseparable from one key figure: Chairman Zhu Yiming.

As the founder of GigaDevice, Zhu Yiming made an industry-puzzling decision in 2016: abandoning the stable path of a chip design company to go all-in on Hefei, establishing CXMT, and betting heavily on domestic DRAM.

How difficult was this path? DRAM is the most brutally competitive segment globally. Samsung, SK Hynix, and Micron collectively control over 90% of the global market share, leaving almost no room for new entrants. Compounding this, DRAM manufacturing is extremely capital-intensive; a single 12-inch fab requires billions of dollars in investment. For a very long time, CXMT was essentially throwing money into a pit.

Zhu Yiming famously made a pledge that year: He would take no salary and no bonuses until CXMT became profitable.

This promise has been more than fulfilled.

Valuation Debate: One Trillion or Two Trillion?

With such explosive performance, what is CXMT actually worth?

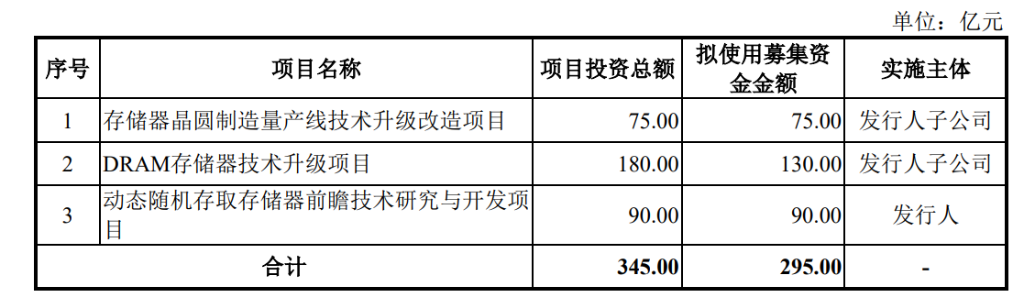

According to the current IPO plan, CXMT intends to raise 29.5 billion yuan on the STAR Market, with total share capital post-IPO no less than 10%, implying a valuation of approximately 295 billion yuan. The proposed IPO raising of 29.5 billion yuan is also the highest in the STAR Market's history (SMIC aimed to raise 20.7 billion yuan in 2020 but oversubscribed to 53.2 billion yuan).

Current market expectations for CXMT's valuation are roughly 1 trillion yuan in the short term and 2 trillion yuan in the long term. Based on an estimated net profit of 100 billion yuan attributable to the parent by the end of 2026, a market cap exceeding one trillion yuan is well-supported by relative valuation calculations.

Of course, there are also controversies.

The cyclical nature of DRAM is an inescapable historical law—CXMT was still deeply in the red last year, but booming this year. Once the super cycle ends and prices fall, performance could shrink sharply at any time.

However, some argue that the core logic of this cycle has shifted from "short-term consumer electronics peak season" to "structural AI demand," making it far more sustainable than previous ones. Furthermore, CXMT's scarcity premium as the sole domestic DRAM player is another factor that cannot be ignored in pricing.

A Textbook Financial Comeback

From accumulated losses of 36.6 billion to earning 50 billion in half a year, CXMT has executed a textbook financial comeback in less than six months.

But behind this comeback lies a decade of unwavering capital commitment, technological accumulation, and strategic perseverance. What Zhu Yiming and the CXMT team bet on was not just an industry cycle, but a national industry proposition: securing a place for China on the global DRAM map.

The report card of earning nearly 400 million yuan a day is a gift from the prevailing trend, but also the reward for ten years of hard work.

On the day CXMT ultimately rings the bell for its IPO, the answer it gives the capital market may be more convincing than any research report.