Nvidia's Wednesday Earnings Night: The Battle That Could Determine the Fate of the AI Bull Market Begins

- Core Thesis: Nvidia's May 20 earnings report represents a critical stress test for the AI bull market. The current market is technically overbought to an extreme degree, and options positioning is overwhelmingly bullish, significantly amplifying the risk of two-way volatility. The earnings results and forward guidance will determine the subsequent trajectory of the AI compute super-cycle.

- Key Factors:

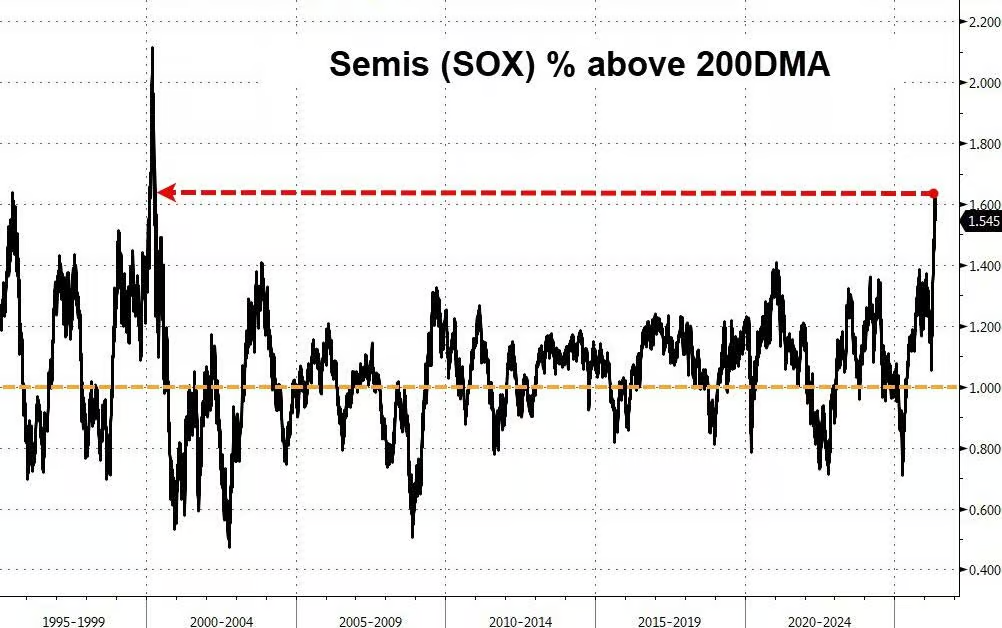

- Goldman Sachs data shows the Philadelphia Semiconductor Index (SOX) is trading approximately 60% above its 200-day moving average, the largest deviation since the 1999/2000 dot-com bubble, indicating historically extreme overbought technical conditions.

- An unusual "concurrent rise in stock price and volatility" signal has emerged. Nvidia's earnings-implied volatility swing has reached 6%, suggesting traders are simultaneously chasing price increases and paying a premium for downside protection.

- Goldman Sachs estimates Nvidia's quarterly revenue will exceed market consensus by approximately $20 billion. However, the market's primary focus is on the guidance for the upcoming quarter, around $86 billion. Forward guidance is more critical than the current quarter's performance.

- Options positioning is extremely bullish. Last Friday, the nominal notional value of S&P 500 call options traded hit a record high of $2.6 trillion. Concurrently, hedging via deep out-of-the-money put options for downside protection is also increasing.

- Warning signs of market breadth have emerged. Only about 52% of S&P 500 components have recorded positive returns year-to-date. Gains are concentrated in a handful of large-cap AI stocks, revealing a structural divergence in the market.

Original Author: Zhang Yaqi

Original Source: Wall Street CN

Nvidia is set to report its quarterly earnings after the market close on Wednesday, May 20th (Eastern Time), marking a critical stress test for the current AI bull cycle. The semiconductor sector faces severe technical overbought conditions, options positions are heavily skewed towards calls, and a rare signal of "stock price and implied volatility rising in tandem" suggests significantly amplified two-way risk around this earnings window compared to the past.

Goldman Sachs TMT lead specialist Peter Callahan published a briefing titled "Yellow Light" on Monday, noting that the Nasdaq 100 (NDX) and the Philadelphia Semiconductor Index (SOX) recorded their first down week of the quarter last week; the 10-year US Treasury yield rose to approximately 4.60%, its largest single-week increase in over a year; oil prices rebounded to around $109 per barrel; and the VIX also moved higher. He pointed out that the core contradiction currently facing the AI and semiconductor theme is that fundamentals remain strong while technical pressures continue to accumulate.

Options analytics firm SpotGamma noted in a recent report that the market is exhibiting a rare pattern where "stock prices are rising while volatility is climbing simultaneously" — typically, the two should have an inverse relationship. This signal indicates that traders are both chasing the rally and paying a premium for protection against large swings. The implied move for Nvidia's earnings has already reached 6%, with market attention highly concentrated on this event.

The earnings results and forward guidance will directly test the market's assessment of the AI computing power supercycle. Given Nvidia's high correlation with the semiconductor and broader tech sectors, its earnings performance, whether positive or negative, is expected to trigger widespread ripple effects across the market.

Technical Indicators Flash Most Extreme Warning Since 1999/2000

The magnitude and speed of the current semiconductor rally have pushed technical indicators to historically overbought levels.

According to Goldman Sachs data, the SOX index has rallied approximately 70% since its late March low, adding over $5 trillion in market capitalization along the way. Drivers include a phased easing of geopolitical tensions, better-than-expected corporate earnings — such as AMAT raising its full-year guidance by more than anticipated and CSCO achieving 35% year-over-year product order growth — as well as increased investor confidence in AI computing demand. Semiconductor industry earnings expectations have been revised up by over 25% since the start of the year.

However, Peter Callahan specifically highlighted that the SOX index is currently trading about 60% above its 200-day moving average, a deviation not seen since the peak of the internet bubble in 1999/2000. He also noted that Goldman Sachs' high momentum factor basket has experienced 12 trading days with single-day moves of ±5% or more this year, accounting for nearly 15% of all trading days. The rapid expansion of leveraged ETFs and options products has further amplified this two-way elasticity.

"It is worth keeping these tactical dynamics in mind before this week's earnings season (Nvidia on May 20th) concludes and we head into summer trade," Callahan wrote. Overall, Goldman Sachs' trading desk maintains a medium-term constructive stance on AI and semiconductors but advises investors at a tactical level to remain cautious regarding technical challenges.

Nvidia Earnings: Forward Guidance May Be More Crucial Than Quarterly Results

Market optimism regarding Nvidia's fundamental outlook remains high, but recent price action has already partially priced in some expectations.

According to Goldman Sachs' Nvidia earnings preview report, analysts generally expect Nvidia's quarterly revenue to exceed market consensus by approximately $20 billion — the company's historical surprise range is typically between 2% and 3%. Greater attention is focused on the forward guidance for the next quarter, where the current analyst consensus stands at roughly $86 billion, implying a sequential increase of about 9%. Other key areas of focus include: whether there is further upside potential in Nvidia's cumulative ~$1 trillion data center revenue guidance, and the narrative of accelerating Agentic AI inference demand — particularly its pure CPU rack products expected to begin shipping in the second half of 2026.

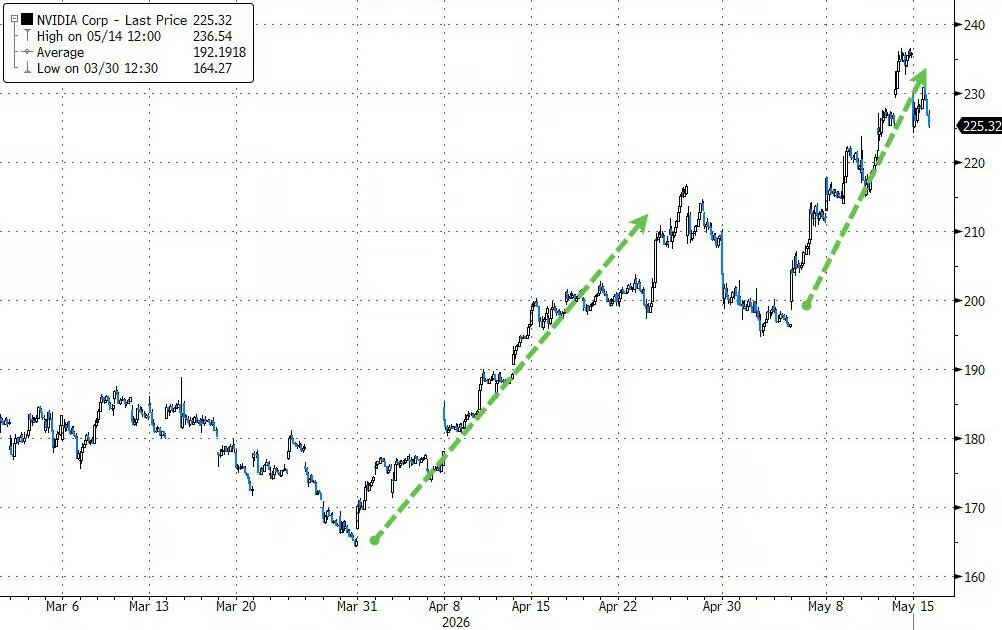

Looking at recent price action, Nvidia has risen for seven consecutive trading days, posting a 20% gain — its longest winning streak in nearly two years. Since its late March low, it has added approximately $1.7 trillion in market capitalization. However, Goldman Sachs data also shows that Nvidia's stock has declined on the first trading day after earnings (T+1) in four out of the last five reports, and substantial single-day upside moves triggered by earnings have actually not occurred since May 2022.

Options Market: Extreme Bullish Bets and Tail Hedging Coexist

The options positioning structure presents a set of internally contradictory signals.

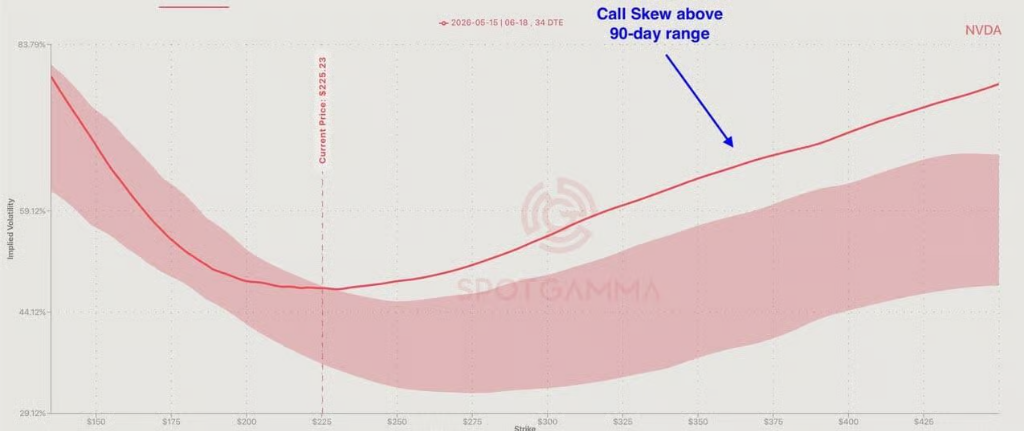

According to SpotGamma data, overall positioning remains heavily skewed towards bullish bets, with traders continuously rolling Nvidia call options to higher strike prices. Call skew remains at the high end of its 90-day historical range, while demand for downside protection is extremely limited. Citing data from 22V Research, notional trading volume for S&P 500 call options hit a record high of $2.6 trillion last Friday, with call options accounting for 60% of total options volume. The RSI for the Philadelphia Semiconductor Index also climbed to levels not seen since March 2000.

Simultaneously, hedging layouts against downside risk are quietly underway. SpotGamma noted a significant increase in large put option structures and buying activity around the S&P 500 (SPY), Semiconductor ETF (SMH), and DRAM-related assets, concentrated in deep out-of-the-money strikes. This suggests their function is closer to tail risk hedging rather than outright directional bets. "Market participants are not bearish on Nvidia, but preparedness for downside scenarios is not trivial," SpotGamma wrote in its report. "Any directional shift will almost quickly spill over into the broader market."

SpotGamma added that Nvidia has surged over 35% since its March low. The sheer size of current call option positions means that if earnings disappoint or trigger widespread profit-taking, it could lead to a significant directional reversal.

Market Breadth Concerns: Rally Propped Up by a Handful of Stocks

Beneath the strong performance of semiconductors and large-cap tech stocks, a lack of broad participation in the US stock market is forming a structural concern.

In his report, Peter Callahan noted that while the S&P 500 is up roughly 8% year-to-date, only about 52% of its constituents have posted positive returns. Areas that have notably lagged this year include residential real estate, medical equipment, engineering and construction without government business exposure, federal IT services, software and services, independent power producers, restaurant chains, commercial real estate brokerage, and insurance brokerage sectors.

Callahan admitted that looking at the charts of these sectors makes him question whether the current market performance truly reflects "health" or is merely the effect of investors being forced to concentrate capital into a few large-cap AI stocks, a "funding source" effect. Oppenheimer's equity derivatives team also pointed out that only about one-fifth of S&P 500 components have outperformed the index over the past month, with dispersion rising to its highest level in over a year, while implied correlation is near its year-to-date low. Goldman Sachs' Prime Brokerage (PB) data also shows a notable "risk reduction" in the tech sector recently.