Tiger Research: DeFi Is No Longer Chasing High Yields; Yield-Bearing Stablecoins Are the New Infrastructure

- Core Thesis: The yield-bearing stablecoin (YBS) market is undergoing a structural shift, with capital flowing from high-yield but volatile synthetic products (e.g., sUSDe) towards lower-yield but more predictable Treasury-backed products (e.g., USYC). The primary driver is moving from chasing APY to prioritizing asset predictability and institutional adoption.

- Key Elements:

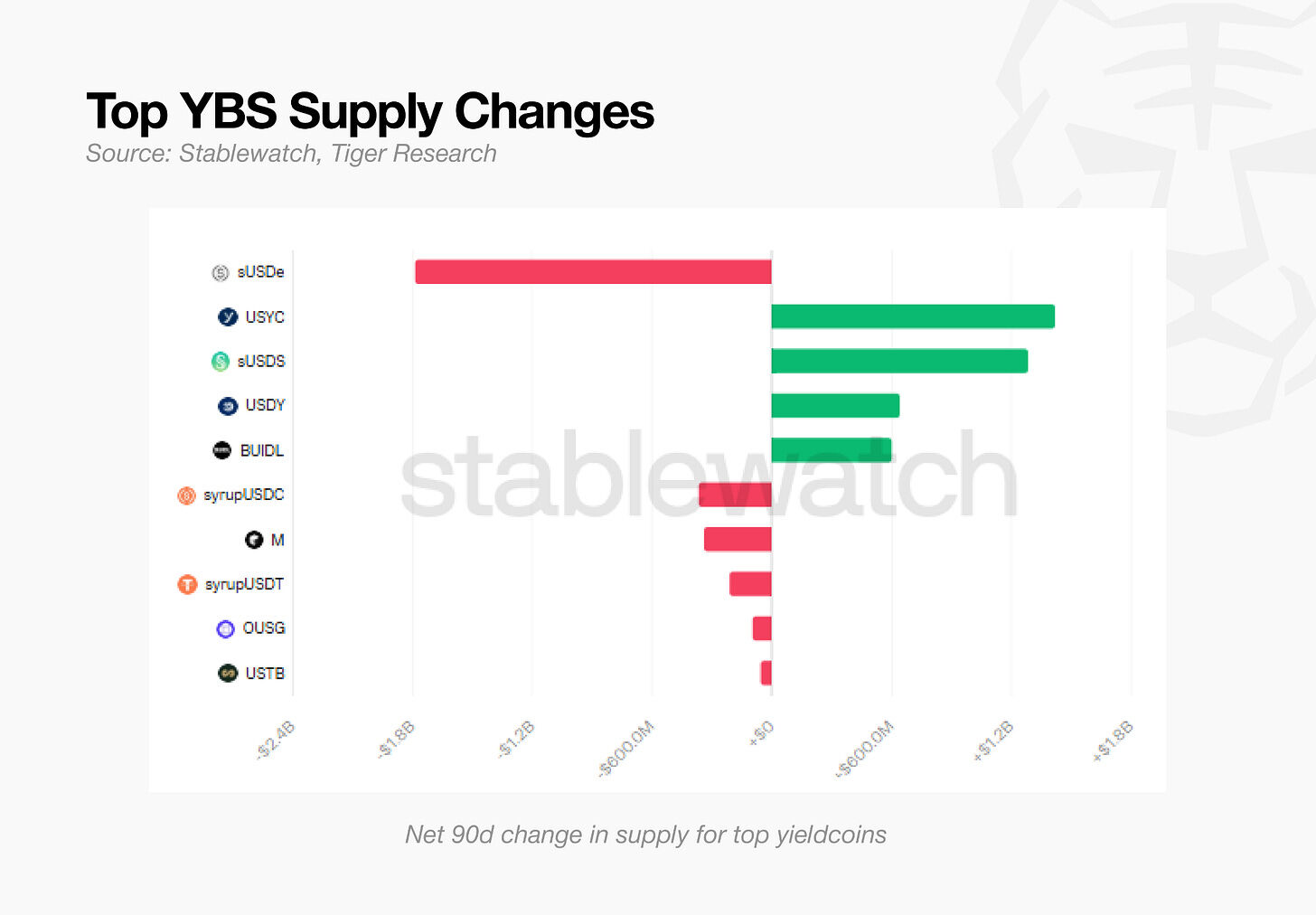

- Over the past 90 days, sUSDe supply has dropped by 49% (approximately $1.8 billion), but the total TVL in YBS has not declined. Capital has flowed into USYC ($1.4 billion) and sUSDS ($1.2 billion), indicating capital rotation within the sector rather than an exit.

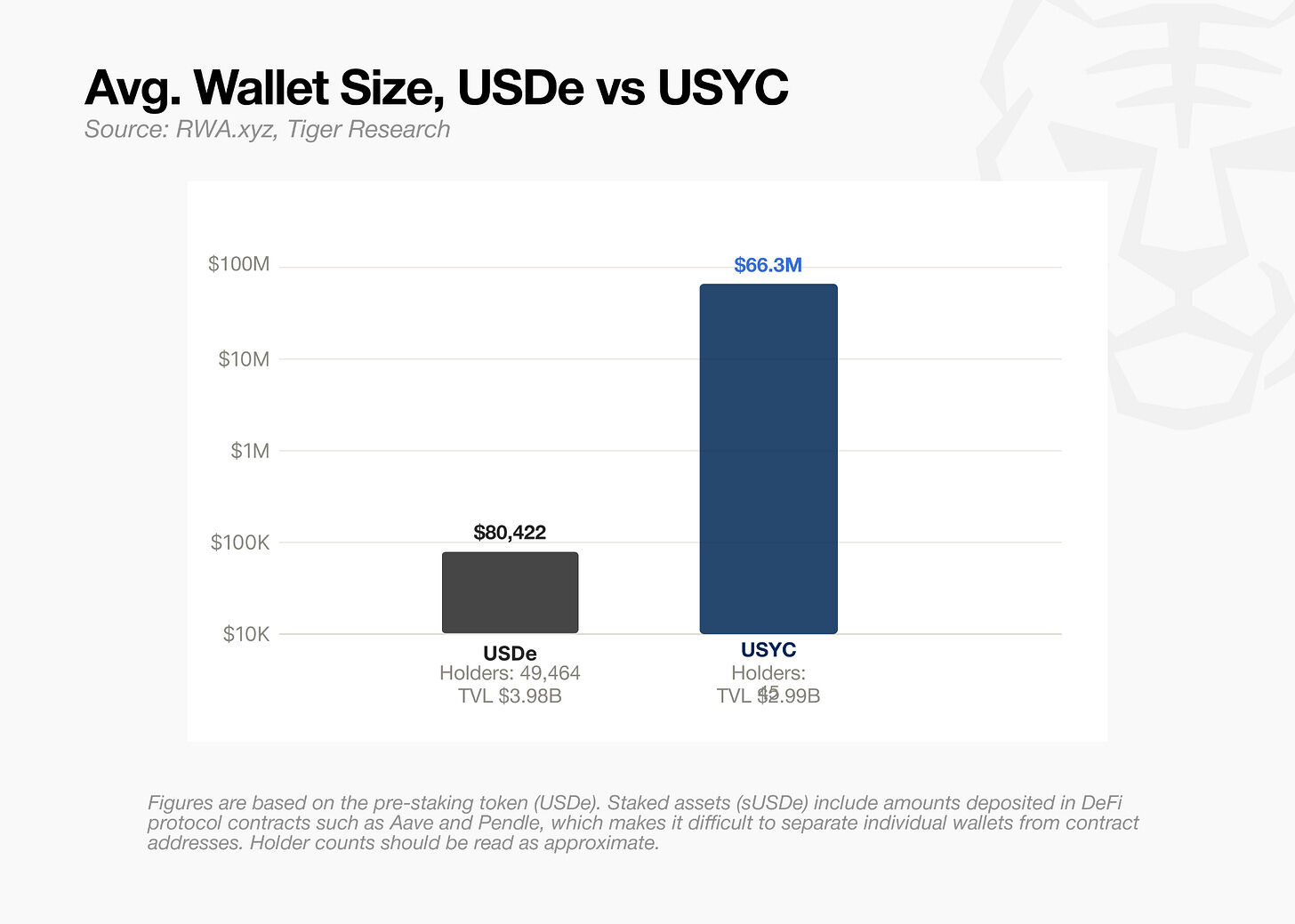

- The holder bases of USYC and sUSDe are significantly different: the average holding per wallet for USYC is 800 times that of sUSDe. Designed with institutions in mind, USYC has been adopted by Binance as collateral for derivatives, driving demand.

- The stability of the yield source is the core difference. sUSDe's delta-neutral structure generates returns linked to crypto market funding rates, which are highly volatile (ranging from 47% down to 3%). USYC's yield comes from Treasuries, linked to real-world interest rates and is more predictable.

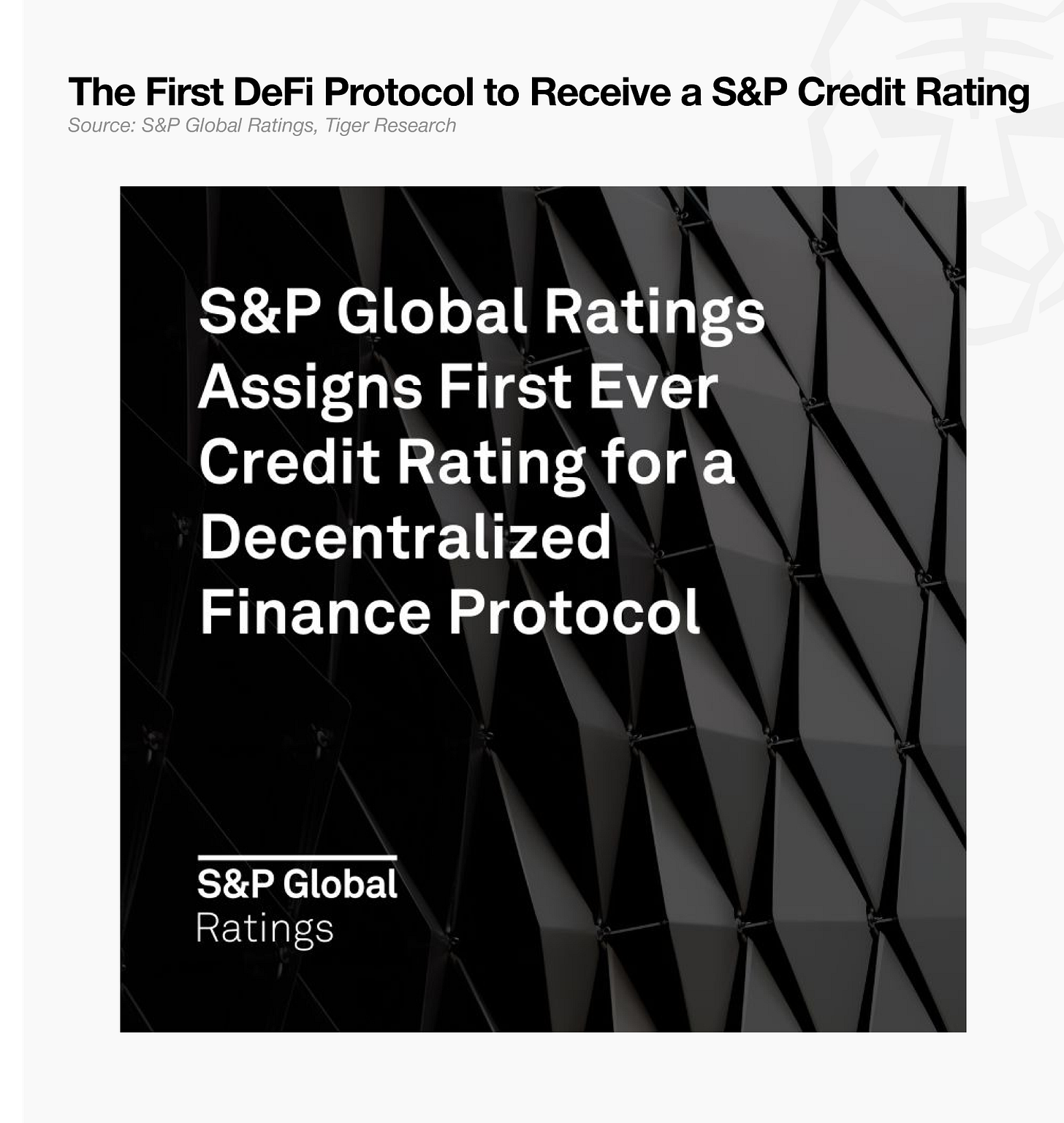

- S&P Global has granted its first credit rating (B-) to a DeFi protocol (Sky Protocol/USDS), while also assigning USDe a 1250% risk weight (based on Basel III). This highlights the institutional focus on predictability.

- In response to structural limitations, Ethena will reform USDe's collateral structure in April 2026, shifting from a purely synthetic model to a hybrid model. This will significantly reduce the proportion of perpetual swaps and increase categories like stablecoin reserves, RWAs, and credit.

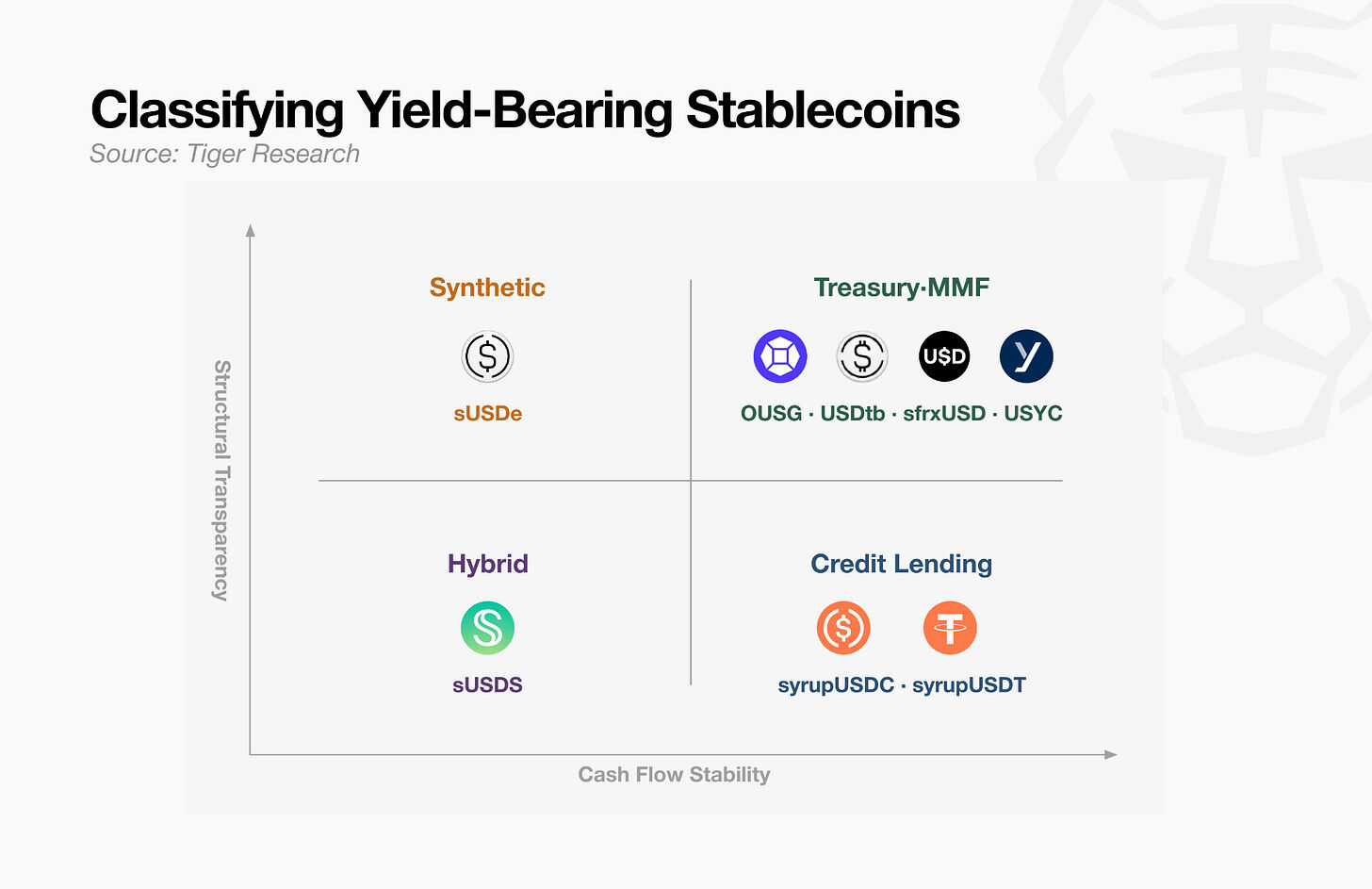

- The YBS market can be categorized along two axes: "yield stability" and "verifiability of yield source." Treasury-backed products are the easiest to quantify, synthetic products are volatile, and credit-based products are hard to verify. Capital is moving towards the more predictable Treasury-backed category.

- YBS is transitioning from native crypto yield production to "importing" traditional finance yields (e.g., Treasuries). While this may seem contradictory to decentralization principles, a stable infrastructure layer will support innovation on top, much like the internet supports blockchain.

This report is prepared by Tiger Research. DeFi is shifting from a market that produces yield to one that imports and distributes yield from traditional finance. The stronger the foundation, the more robust the upper layers can be.

Key Takeaways

- While sUSDe supply halved, capital flowed into lower-yielding USYC and sUSDS. This isn't capital flight, but a change in selection criteria.

- APY is no longer the dividing line for assets. What matters more is adoption as collateral, a savings product, or a reserve.

- S&P issued the first-ever credit rating for a DeFi protocol to USDS, while assigning USDe a 1250% risk weight.

- Ethena will completely overhaul its collateral structure in April 2026, transitioning from a synthetic model to a hybrid one. A single source of yield is no longer sufficient to survive in the YBS market.

- DeFi is shifting from a market that produces yield to one that imports and distributes yield from traditional finance. The stronger the foundation, the more robust the upper layers can be.

What Happened Behind the sUSDe Decline

Yield-bearing stablecoins (YBS) are tokens pegged to the US dollar that generate yield while held. USDC and USDT are like cash; YBS are like deposits, their value rising with interest rates.

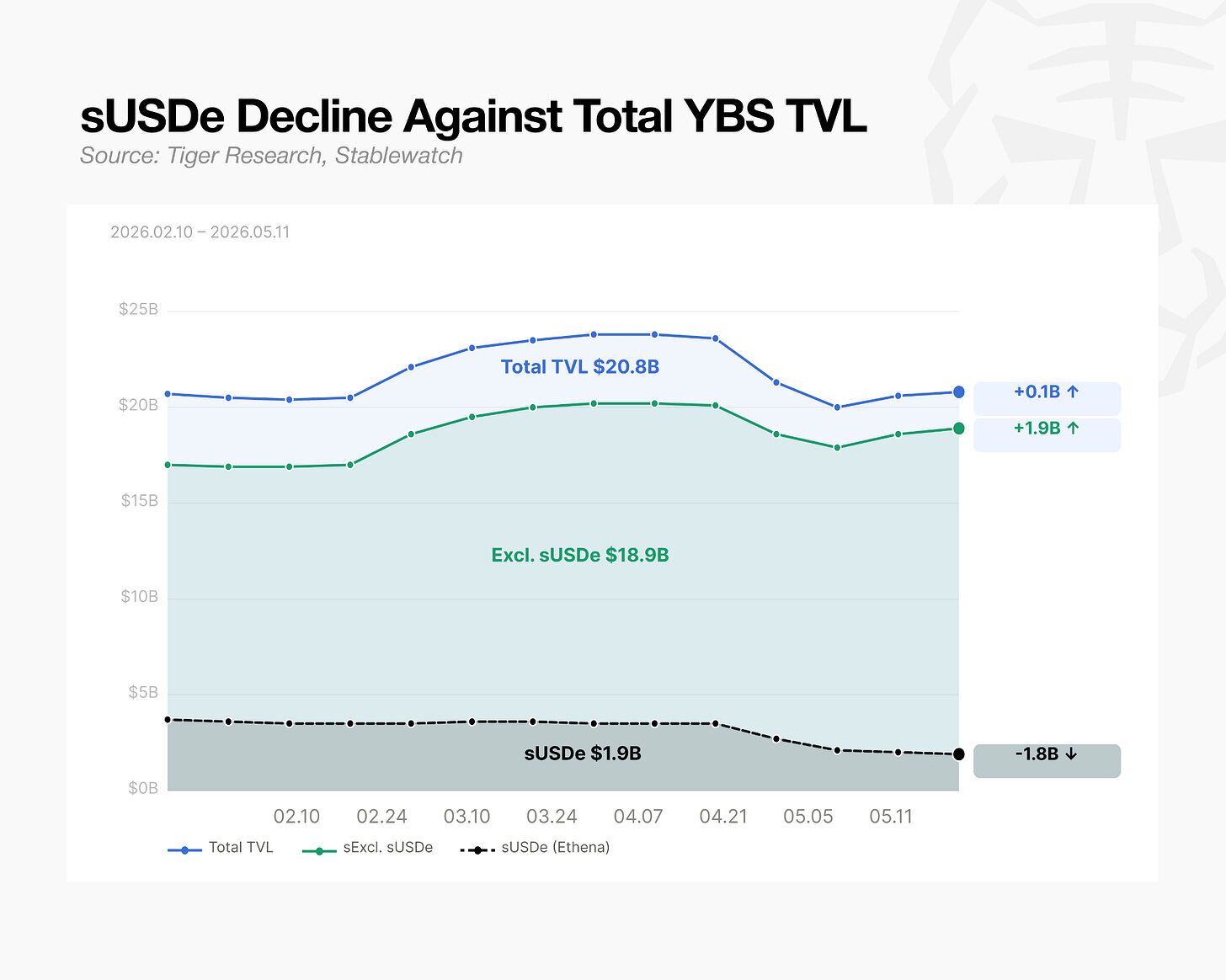

An unusual shift is occurring in this market. Ethena's flagship product, sUSDe, which once held over 30% of the YBS market share, has seen its supply drop by approximately $1.8 billion over the past 90 days, a 49% decline from its peak. There was no hack, no protocol failure.

But the market itself hasn't shrunk. The total TVL in YBS actually increased over the same period. Within 90 days, USYC (Circle's treasury-backed stablecoin) saw inflows of $1.4 billion, and sUSDS (Sky's hybrid stablecoin) saw inflows of $1.2 billion. These two inflows combined exceed sUSDe's decline.

Simply looking at capital flows tells a different story. Capital isn't exiting; it's rotating within the same market.

More Important Than APY: Holder Base and Underlying Assets

Looking purely at APY, there's no reason for capital to shift. On a 30-day basis, USYC yields ~3%, sUSDS ~3.6%, and sUSDe is actually higher at ~4%. If yield were the driving force, capital should concentrate in sUSDe. The rotation seems driven not by yield, but by two other factors: (1) holder base, and (2) underlying assets.

Retail vs. Institutional

Calculated by average holdings per wallet, USDe holders are approximately 1/800th the size of USYC holders. Excluding large block purchases, the gap widens further. USYC was designed from the start to attract only large capital, while USDe heavily relies on retail.

USDe and USYC diverge in their holder bases.

For USDe, the investment thesis for both retail and institutional holders revolves around yield. They come for the APY and leave when it declines. USYC takes a different path: no retail, institution-centric application.

USYC is only open to qualified investors with a minimum purchase of $100,000. In July 2025, Binance adopted it as institutional derivative collateral. Once traders can collateralize yield-bearing assets on the largest exchange, demand follows. BNB Chain alone issued $2.54 billion.

Delta Neutral vs. RWA

The difference between USDe and USDS comes from their reserve assets. Institutions want predictability – how yield is generated and how it fluctuates must be predictable.

USDe operates a delta-neutral structure: crypto collateral on one side, perpetual short positions on the other, offsetting price volatility. Yield is tied to perpetual funding rates. During the 2024 bull market, sUSDe APY exceeded 47%. After the market turned sideways, it dropped to the 3% range. Volatility exceeded tenfold in months. Yield fluctuates in sync with market conditions.

USDS is backed by short-term US Treasuries and money market funds. Yield is linked to real-world interest rates. At the end of 2024, APY was in the 9% range and took over a year to drop to the 3% range.

This difference is also reflected in S&P's assessment. In August 2025, S&P Global assigned a B- credit rating to Sky Protocol, the first credit rating ever given to a DeFi protocol. The rating itself isn't high; the significant point is that a DeFi protocol received a credit rating.

In the same report, USDe was assigned a 1250% risk weight. The rationale cited is its "complex maintenance mechanism." Under Basel III (the bank capital adequacy framework set by the Bank for International Settlements BIS), USDe falls into the highest-risk crypto asset category. Independent of any incident, sUSDe sits outside the approval range of institutional risk committees.

For institutions, predictability is as important as yield. Ethena can offer higher returns depending on market conditions, but it may be harder for institutional trading desks to underwrite.

The Direction of the YBS Market

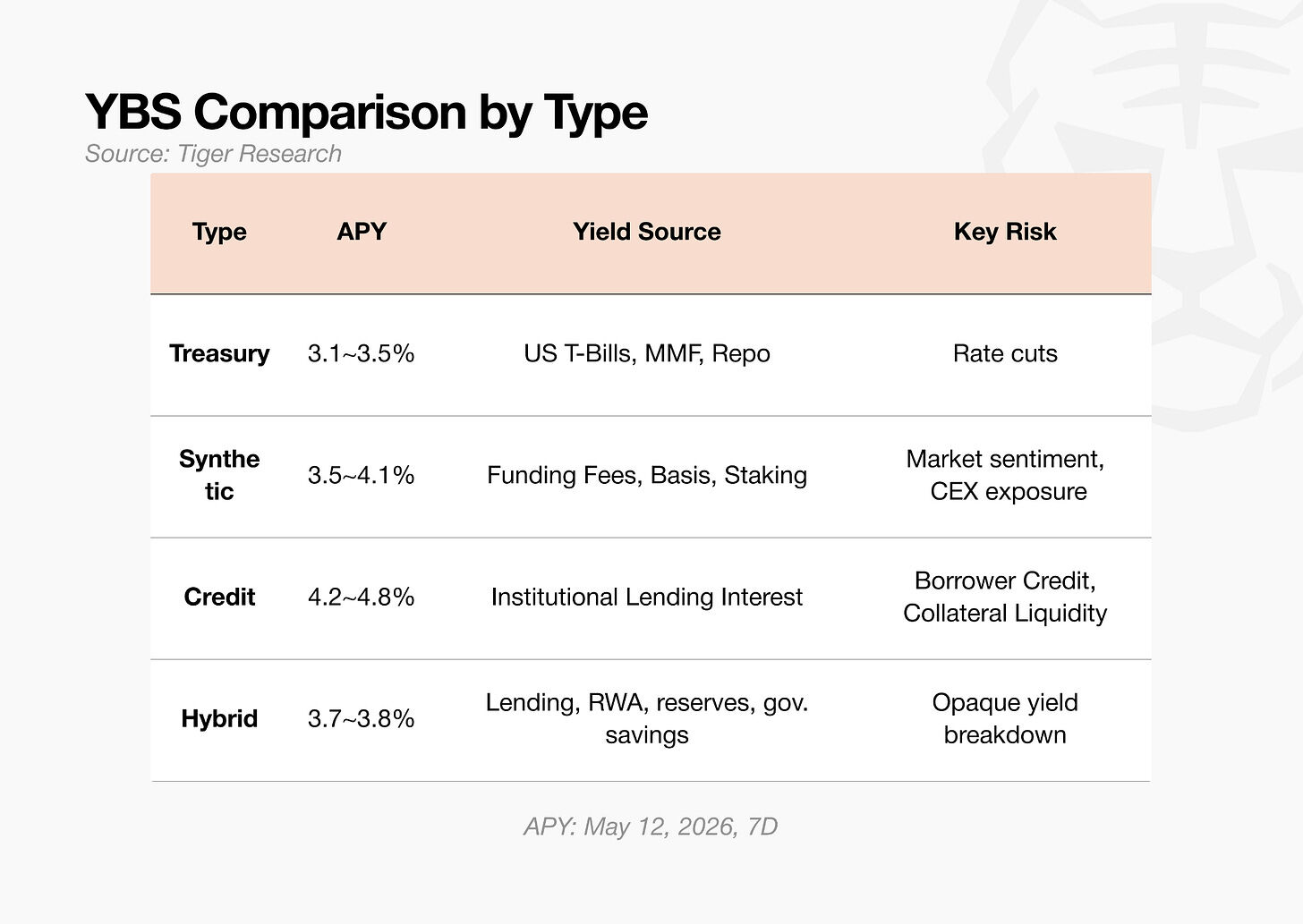

YBS assets can be categorized along two axes: "how stable is the yield" and "can the yield source be verified." A 4% APY is not always the same 4%. The type of risk depends on who is paying the interest. The majority of capital is moving towards the more predictable side.

Treasury-backed YBS (OUSG, sfrxUSD, USYC) are the easiest to describe.

Short-term Treasury yields flow from the issuer to the holder through the operational layer. As of May 2026, average APY ranges from 3.1% to 3.5%. The constraint is that yield is tied to Treasury rates.

Synthetic YBS (sUSDe) offers transparent yield sources but is sensitive to market conditions.

Perpetual swap funding rates are the primary income source. Yield is verifiable on-chain but fluctuates dramatically with market conditions. APY exceeded 15% in September 2025, and on a 7-day basis as of May 12, 2026, it was in the 4% range.

Credit-based YBS (syrupUSDC, syrupUSDT) offer high yield stability but low verifiability.

Via Maple Finance, interest paid by hedge funds and trading firms flows back to holders. The fixed-rate structure in the 4% range maintains low volatility. Borrower credit and collateral value are difficult to inspect externally.

Hybrid YBS (sUSDS) sits between the two ends.

Yield is a mix of Spark lending fees, RWA returns, reserve management, and governance-set savings rates. The 7-day rate is 3.6%, lower than sUSDe. On the risk side, the lack of a single point of failure helps. The trade-off is that decomposing the yield structure externally is difficult.

This classification points towards a single pattern: except for Ethena's synthetic model, every category is bringing traditional finance yield sources onto the chain.

Ethena Knew It All Along

The first sign that Ethena recognized its structural limitations was the launch of USDtb. USDtb is a treasury-backed dollar with short-term US Treasuries as reserves. It was designed as a buffer for USDe when funding rates turn negative.

In April 2026, Ethena went further, directly overhauling USDe's collateral structure. Ethena cut the perpetual swap share to 11% of total collateral and added new categories: stablecoin reserves, DeFi lending, CLOs, investment-grade corporate bond funds, and short-term credit.

Ethena is also researching plans to incorporate a gold-perpetual-based delta-neutral strategy into USDe collateral. The same methodology used for BTC and ETH would be applied to gold (PAXG, XAUT). The risk committee has completed a formal review.

This is the biggest structural change since its launch. In effect, Ethena acknowledges that a delta-neutral strategy built solely on crypto assets is no longer viable.

USDe and sUSDe started as synthetic and are evolving into a hybrid. This shift confirms that a single source of yield is no longer sufficient to remain competitive in the YBS market.

Foundation First

DeFi importing yield from traditional finance rather than generating it natively might seem contrary to the ethos of decentralized finance. But it doesn't mean DeFi is finished.

Blockchain originally aimed to build a decentralized internet, yet ultimately runs on top of the internet itself. Without the internet, there is no blockchain. Stablecoins sought to replace the US dollar, yet ultimately run on top of it. They subsequently fueled the rise of DeFi. The traditional foundation has never prevented innovation in the layers above it.

YBS can follow the same path. BUIDL is already collateral for USDtb. USDtb becomes a reserve for USDm (MegaETH's native stablecoin). New money legos are already stacking on top of treasury-backed YBS.

As treasury-backed YBS settles into infrastructure, yields will compress, and the range of underlying assets will narrow. The alpha available from any single asset will continue to shrink. Just as the internet became infrastructure with access costs approaching zero, YBS will follow the same path. Stability and composability will matter more than yield.

Once the infrastructure matures, experiments built upon it can operate on a stronger foundation. Early synthetic dollars were unsustainable because their underlying assets were unstable.

Early DeFi yield structures were built on sand. They relied on altcoin prices, token incentives, and leverage demand. Now, proven yield sources are forming a base upon which on-chain financial structures are being built.