AI bull market countdown? Wall Street tech veteran: This year feels like 1997/98, next year could see a 30-50% drop

- Core Thesis: Analyst Dan Niles compares the current AI wave to the 1997-1998 internet era, believing the bull market isn't over, but predicting a 30%-50% correction in early 2027. He advises investors to hold significant cash reserves and remain vigilant.

- Key Factors:

- Agentic AI driving a leap in compute demand: Agentic AI increases token consumption by 10-100 times compared to conversational AI, causing hyperscale cloud providers' 2026 CapEx growth expectations to rise from 30% to 70%.

- Shifting hardware landscape: The orchestration nature of Agentic AI favors CPUs, with the GPU ratio potentially moving from 8:1 towards 1:1. Intel and AMD stand to benefit, while Nvidia faces marginal pressure. However, overall semiconductor overbought levels are the most severe since 2000.

- Two potential triggers for a 2027 correction: Agentic AI growth will naturally slow due to a high base; financial issues at companies like OpenAI or capital absorption from trillion-dollar IPOs could accelerate a market downturn.

- Macro warning signals: Record highs in the stock market, oil prices up roughly 60% year-to-date, and 10-year Treasury yields hitting elevated levels – one of these must be wrong. If oil prices remain high, inflation and consumer pressure will trigger a stock market correction.

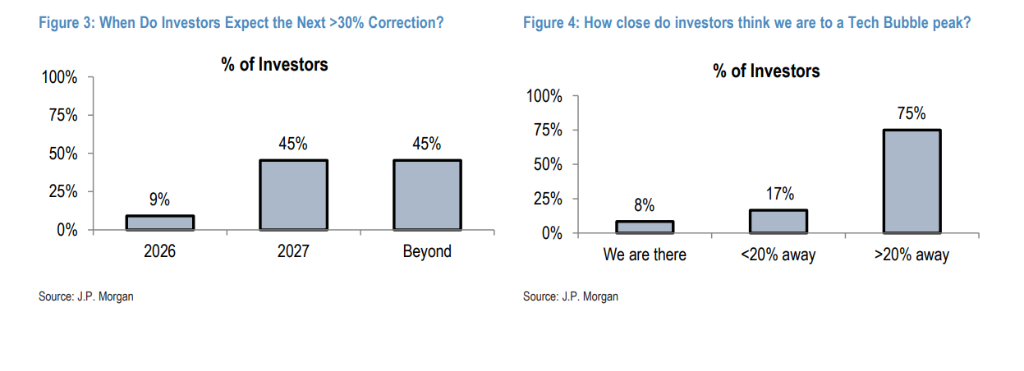

- Institutional consensus: A JPMorgan survey indicates that 54% of institutional investors expect a market correction of over 30% in 2026-2027, with 45% believing it will occur in 2027, highly consistent with Niles's assessment.

Original Author: Long Yue

Original Source: Wall Street News

The current market conditions are eerily reminiscent of 1997-1998 — Wall Street tech veterans are already counting down to the end of the AI bull run.

On May 11, Dan Niles, a renowned chip analyst from the dot-com bubble era and founder of Niles Investment Management, gave an in-depth interview on "The Master Investor Podcast," systematically outlining his assessment of the current AI market: the AI bull run isn't over yet, but he predicts a major correction could arrive in early 2027, and investors should start preparing now.

Meanwhile, a survey by JPMorgan Chase of 56 global investors found that 54% expect the U.S. stock market to experience a correction of over 30% this year or next, with 45% believing it will occur in 2027 — aligning closely with Dan Niles' forecast.

We're in 1997-1998, Not 1999, and Certainly Not 2000

Niles compares the current market to 1997-1998, rather than the peak of the bubble in 1999-2000 that many fear.

The logic is this: ChatGPT launched in late 2022, meaning AI infrastructure buildout is now entering its fourth year. In the internet era, the Netscape browser launched in 1994, and 1997-1998 was also the third and fourth year, respectively.

In 1997, the Thai currency crisis erupted, and the S&P 500 dropped 11% at one point during the year but finished up 31%. In 1998, Russia defaulted on its bonds and Long-Term Capital Management (LTCM) collapsed, sending the S&P 500 down 19% at its peak, yet it still ended the year up 27%.

Niles stated: "Back then, the backdrop of internet infrastructure buildout supported everything, so every macro shock was a buying opportunity. It's the same today."

He believes the oil price shock triggered by the Iran war is a "man-made event" and easier to resolve than the currency crisis or bond defaults of that era, leading him to judge this as a cyclical low point.

Agentic AI: The New Fuel Driving This Bull Run

Niles boils down the core driver of this year's market to one term: Agentic AI.

Simply put, before, you would ask ChatGPT a question and it would give you an answer — that's "conversational AI."

Agentic AI is fundamentally different. Dan Niles explains: "You can tell it, 'This is Wilfred. Go get this data from the BBC website, get that data from Bloomberg, get this other content from CNBC, and compile it all into an Excel spreadsheet.'" This series of operations requires massive concurrent calls, consuming 10 to 100 times the compute tokens of conversational AI.

The data already proves this: In the two months before the launch of Open Claw on January 30, 2026, token growth was around 20%; in the two months after launch, token growth exceeded 120%.

This has directly driven up capital expenditure expectations for hyperscale cloud providers: at the start of the year, the market expected 2026 capex growth of around 30%, which rose to 60% after Q1 earnings, and then to 70% after the latest round of earnings.

Niles' conclusion: This isn't a minor change; it's a leap in magnitude, sufficient to support continued gains in AI-related stocks.

Hardware Landscape Shifts: CPU Rises, GPU Faces Pressure

The architectural characteristics of Agentic AI are quietly rewriting the competitive landscape of AI hardware.

Training large models involves repeating the same task, where GPUs excel; inference for conversational AI is also manageable. But Agentic AI requires simultaneously orchestrating multiple applications and coordinating multi-step tasks — essentially "orchestration," which is a CPU strength.

Dan Niles says: "Historically, it was about 8 GPUs to 1 CPU. With the shift to Agentic AI, this ratio will approach 1 to 1."

This means Intel and AMD benefit, while Nvidia is "marginalized in a way that will affect its stock price performance."

But Semiconductors Are Severely Overbought

Dan Niles quickly pivots: the short-term risk cannot be ignored. "In the short term, semiconductors are more overbought than at any time since before the 2000 or 1995 crash. That's for sure."

He specifically notes that semiconductor ETFs are up about 70% year-to-date and haven't even been knocked down by the Iran war shock.

However, he also emphasizes that short-term overboughtness doesn't mean the long-term thesis is broken — the demand for compute power from Agentic AI is real. He's willing to accept the risk of Intel potentially dropping 15-20% in the short term because he believes the stock will be higher by year-end.

Where Will the 30-50% Correction Come From in 2027?

Dan Niles is already modeling the next cycle.

The explosion of Agentic AI began on January 30, 2026. Based on this, by early 2027, growth will begin comparing against a high base, naturally leading to a significant slowdown. What will the market do then?

"I think these stocks could fall 30% to 50% from the highs they'll be at by then," he says.

The reference point is recent: in 2022, the "Magnificent 7" tech stocks fell an average of 46% — that was merely the aftermath of the pandemic-era tech buildout fading, a smaller scale than the current AI boom.

Another potential trigger is OpenAI. Dan Niles points out that OpenAI and Anthropic together account for roughly half the backlog orders of hyperscale cloud providers. The two companies have gone from a combined annualized revenue of about $70 billion in early 2025 to nearly $700 billion now (Anthropic ~$450B, OpenAI ~$240B) — an astonishing growth, but the money must come from somewhere else, squeezing budgets of other companies.

"When OpenAI had annual revenue of just $20 billion, it publicly claimed it would commit $1.4 trillion in capital expenditure over eight years. Where is the money coming from? If OpenAI runs into trouble, it would greatly accelerate this process."

He also highlights a structural liquidity pressure: IPOs from companies like OpenAI, SpaceX, and Anthropic are coming soon, each potentially valued at over a trillion dollars. "This money has to flow from somewhere else. Fund managers don't have piles of idle cash sitting around; they have to sell other things."

Three Signals Flashing Simultaneously: Stocks, Oil, Bonds, One Must Be Wrong

The first thing Dan Niles does every morning is check oil prices, bond yields, and the stock market simultaneously.

The current combination makes him uneasy: stocks are at all-time highs, oil is up about 60% year-to-date, and U.S. 10-year and 30-year Treasury yields are at their highest levels of the year.

Historically, 10 out of the last 12 recessions were preceded by sustained increases in oil prices. If oil stays near $90 for a quarter or two, inflation will rise, consumer purchasing power will erode, and a significant stock market correction will become inevitable. McDonald's recent earnings mentioned pressure on lower-end consumers with same-store sales missing expectations — signs like this are starting to appear, and you have to be concerned.

He also mentions that incoming Fed Chair Kevin Warsh favors rate cuts and views AI as a deflationary force, "which is a positive factor driving markets higher in the short term." But he warns that if 10-year or 30-year yields continue to climb, market valuations will face real pressure. His conclusion:

Among stocks, oil, and bonds, one must be wrong. When one reprices, it could cause a lot of market turmoil.

His advice is simple: "You should be holding a lot of cash right now. — At the end of March, I thought it was a good time to be actively buying. But now, I think you should hold a lot of cash and be highly vigilant about how this eventually resolves."

JPMorgan: 54% of Institutional Investors Expect a Major Correction in 2027

Dan Niles' warning is not an isolated case.

A roadshow feedback report from JPMorgan Chase's Global Market Strategy team, released on May 12, 2026, showed that analyst Eduardo Lecubarri and his team visited five cities in Latin America and spoke with 56 institutional investors.

Key data from the report:

- 92% of surveyed investors believe equity market returns will be positive for the full year 2026, but none expect gains to exceed 20%;

- 54% of surveyed investors expect the stock market to experience a correction of more than 30% sometime between 2026 and 2027 (9% expect it in 2026, 45% in 2027);

- 75% of surveyed investors believe there is still more than 20% upside from here to the peak of the tech bubble;

- Regarding regional allocation, investors show a strong consensus on Europe: 100% underweight Europe, 100% overweight the U.S.;

- Investors' most favored sectors are Technology, Utilities, and Industrials.

This aligns perfectly with Dan Niles' "1998 logic": the bull market is far from over, but the timeline for a major correction is quietly forming in market consensus.

Quantum Computing: Huge Potential, But Don't Rush

At the end of the interview, Dan Niles also touched on quantum computing. He is a firm long-term believer. "I'm a big believer in quantum. I think we'll get there eventually" — but he quotes Bill Gates: technology tends to be overestimated in the short term and underestimated in the long term.

"The earliest AI papers were written over 50 years ago. When did ChatGPT appear? End of 2022. Quantum computing is probably on a similar path. The arrival of quantum computing IPOs will bring market attention back, but truly disruptive applications will take longer than most people think."

Big Tech Divergence: Google Leads the Pack

The past few weeks of Big Tech earnings gave Dan Niles even more clarity.

Google Cloud: Q4 year-over-year growth was 48%, accelerating to 63% in the latest quarter — a jump of 15 percentage points.

AWS: Accelerated from 24% to 28%, an increase of 4 percentage points — quite good for the largest cloud provider.

Microsoft Azure: Accelerated from 38% to 39%, essentially flat.

"These numbers tell you who is actually executing and gaining market share," Dan Niles says.

He gives a direct verdict: "Over the next 3 to 5 years, who is the best position among Big Tech? Clearly, Google. They have the full technology stack. You should bet on them. Unless something drastic changes, they will continue to be winners because they have everything and immense cash flow to support it."

Google's advantages include: its in-house large language model Gemini, its own AI chips (over a decade old, the longest track record among the three major cloud providers), strong cash flow supported by its advertising business, and the Android ecosystem covering over 75% of global smartphones. Microsoft relies on OpenAI and lacks its own large model; Amazon's AI products have limited brand recognition.

Meta's situation is more concerning. Dan Niles points out that Meta lacks a public cloud, so it cannot sell excess compute power to external enterprises; its progress on custom ASIC chips is also lagging. More importantly, Meta saw its first sequential decline in Family of Apps users this quarter — for an advertising monetization model driven by two growth engines (user numbers and user monetization), a turning point has appeared for the former. "That's something to worry about."

Regarding Apple, Dan Niles believes the launch of an AI-powered Siri and a foldable iPhone will drive a replacement cycle — he cites the iPhone 6 as an example: the screen size increased from 4 inches to 5.5 inches, propelling Apple's revenue growth rate from 7% to 28%.

Stay Nimble, Don't Be Greedy

Dan Niles sums up his market philosophy in one sentence: "Be Nimble. Hold strong convictions, but hold them loosely."

His analytical framework: short-term momentum is upward, driven by Agentic AI and expectations of loose monetary policy as two engines. But by early 2027, these growth figures will start comparing against a high base. The explosive growth from Agentic AI will enter a phase of comparative weakness. Coupled with the potential risk of OpenAI and the liquidity shock from mega-IPOs, "stock prices could fall 30% to 50% from the highs they reach by then."

What to do now? Hold plenty of cash. Keep a close eye on those three key coordinates every morning — oil prices, Treasury yields, and the stock market — and be ready to adjust at any time.