深度拆解OpenAI Pre-IPO

- Core Thesis: OpenAI is building an "actively opened consumer portal" with 1.3 billion monthly active users. Its current $898B valuation only reflects visible revenue from subscriptions and API, and does not account for its advertising business (potentially reaching $25 billion by 2029), the revaluation of its consumer platform, or the re-rating effect from GPT-6. This suggests significant undervaluation.

- Key Factors:

- Consumer Portal Moat: ChatGPT has 900 million weekly active users. The behavioral pattern of users actively opening the application creates a high switching cost moat, analogous to trillion-dollar platforms like Google Search, iPhone, and WeChat.

- Technical Narrative Repair: The release of GPT-5.5 and Image2 has exceeded market expectations, repairing the narrative that its technological lead was being caught up. This could also drive a new wave of WAU growth and a return of enterprise budgets.

- New Advertising Revenue Stream: OpenAI projects advertising ARR of $1 billion in 2026 and $25 billion by 2029. Coupled with Shopify partnerships completing the shopping loop within six weeks, the implied value of its advertising inventory exceeds $300 billion.

- Massive Monetization Potential: Current ARPU per MAU is $1.5, only 1/10th of Netflix's. Each additional 1 million Pro users ($200/month) can generate an annualized ARR of $2.4 billion, demonstrating clear upside.

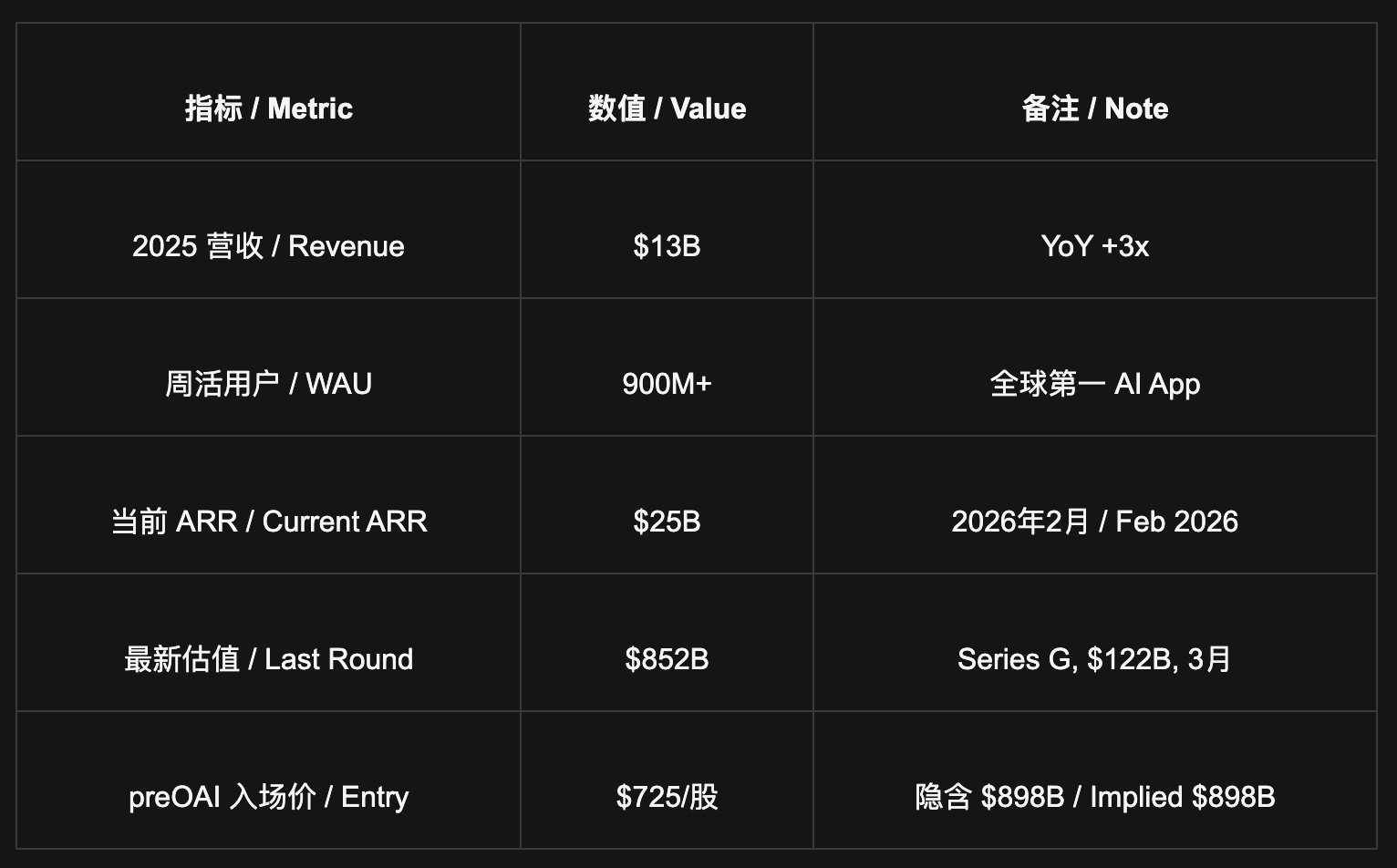

- Valuation & Entry Price: Institutional round equivalent share price is $687.7 ($852B valuation). Latest market valuation is $898B ($725/share). Bitget preOAI is the only tradable channel without qualification requirements. Base case scenario suggests 12-month upside of +11% to +28%.

- Competition is Not Zero-Sum: OpenAI (consumer platform), Anthropic (developer OS), and Google (ecosystem suite) target user pools that largely do not overlap. OpenAI's consumer platform premium has yet to be fully priced in by the market.

- OpenAI's 1.3 billion MAUs are creating the most valuable consumer gateway in human history—users actively open it daily, it's deeply embedded in their workflows, and switching costs are extremely high. The current $898B valuation only reflects an extrapolation of "visible revenue" from subscriptions and API. New revenue streams like advertising (projected $25B by 2029), consumer-side platform repricing, and the GPT-6 re-rating effect have not been fully priced in. Bitget preOAI, entering at $725/share, is currently the only channel available in the retail market without requiring accredited investor status, directly linked to the public market price post-IPO.

What is OpenAI: A Three-Tier Revenue, Actively Opened Consumer Empire

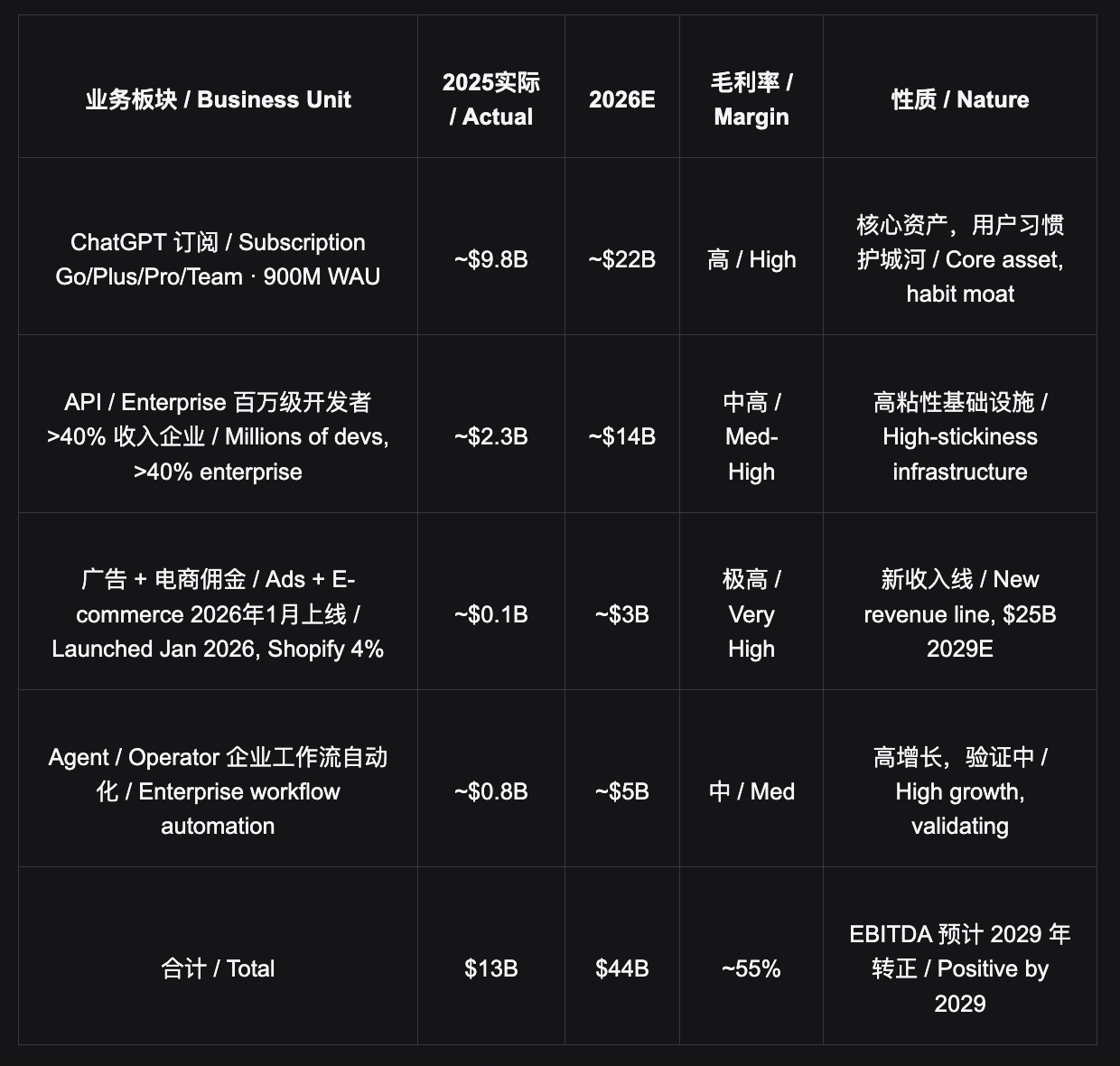

OpenAI's business cannot be understood using a single "AI company" framework. It is simultaneously a consumer subscription platform (ChatGPT, 900 million WAU), a developer infrastructure (API, relied upon by millions of developers), an enterprise software company (Enterprise, contributing over 40% of revenue), and a rising advertising and e-commerce platform—four identities forming a vertical closed loop centered on the consumer gateway.

ChatGPT is an app users actively open, not a feature embedded in another product. This is fundamentally different from Google Gemini (distributed via Search/Suite) and Anthropic (pure API). The behavior of its 1.3 billion MAUs actively opening the app daily constitutes the most difficult-to-replicate distribution moat in the AI field so far.

Switching costs aren't just about changing an app; they involve cognitive restructuring. The cost of reshaping the behavioral pattern of a user who "actively seeks answers" from ChatGPT daily is far higher than switching streaming platforms. This habit moat historically belongs only to a few platforms: Google Search, iPhone, WeChat—all of which eventually entered the trillion-dollar valuation club.

Why OpenAI is Worth Over $1T Short-Term and Approaching $2T Long-Term

Short-Term Catalysts

The current frontier AI benchmark landscape remains fragmented: different models have advantages in dimensions like knowledge work, scientific reasoning, coding, and multimodal generation. The market's core concern over the past period has been: Is OpenAI losing its "absolute technological lead" narrative premium?

However, this narrative is being rewritten. OpenAI has released GPT-5.5, officially positioned as its "smartest model yet," further enhancing capabilities for complex tasks like coding, research, and data analysis. More critically, the performance of Image2 / ChatGPT Images 2.0 has significantly exceeded market expectations, creating strong user-side perceptual differentiation in image generation, editing, text rendering, multilingual support, and practical creative scenarios.

GPT-5.5 + Image2 are sufficient to constitute a new product cycle: on one hand, repairing the market narrative that "OpenAI's tech lead has been caught up"; on the other hand, driving consumer-side activity, enterprise budget reallocation, and high-tier subscription conversion through stronger multimodal capabilities.

1. GPT-5.5 Released: Tech Lead Narrative Begins to Repair

The significance of GPT-5.5 is not just a routine model upgrade, but a direct response to the narrative over the past year that OpenAI's lead was being eroded by Gemini and Claude. The official emphasis on GPT-5.5's improved performance in complex tasks, research, coding, and data analysis indicates OpenAI still maintains a strong position in core knowledge work scenarios.

Image2 Exceeds Expectations: Improvements in image generation and editing capabilities are more easily perceived by ordinary users than pure text benchmarks and are more easily spread on social platforms. Image2 could be the core trigger for accelerating ChatGPT's WAU growth again.

2. Media Cycle Explosion → WAU Continues Upward

ChatGPT's DAU surged tenfold within a week of GPT-4's launch. GPT-5.5 improves high-tier user retention, while Image2 pulls in returning ordinary users. The combination is expected to drive ChatGPT's active users higher.

3. Enterprise Budgets Re-Centralize on OpenAI

GPT-5.5 covers professional workflows like research, code, and data analysis; Image2 covers marketing, design, e-commerce, and content production scenarios. OpenAI's platform attributes are further strengthened, giving enterprises more reason to re-centralize their fragmented AI budgets onto OpenAI.

4. Free/Plus → Pro ($200/month) Upgrade Acceleration

Jump in model capability is the strongest driver for users to upgrade their paid plans. Every additional 1 million Pro users = $2.4 billion in annualized ARR. If GPT-6 is released in the coming months with full-dimensional leadership, it will further strengthen OpenAI's "number one" narrative before the IPO.

5. IPO Roadshow Valuation Upgrade → $1T Target for Q4 2026

OpenAI's capital market story is upgraded from "waiting for GPT-6 to regain the lead" to "GPT-5.5 / Image2 has already proven the product cycle restart, GPT-6 is additional upside." This is more robust than simply betting on a future model release and more likely to support a higher valuation range.

Long-Term Bullish · Consumer Super-Platform

OpenAI is not just an AI company; it is becoming the "default interface for humans to interact with information and tasks." This position has historically only been reached by a few products: Google Search, iPhone, WeChat—all of which eventually entered the trillion-dollar valuation club.

- ARPU Comparison: Full Monetization Space. OpenAI's current blended ARPU is approximately $1.5/month ($25B ARR / 1.3B MAU); Netflix $15/month; Microsoft 365 $10-25/month; Spotify $10/month; Instagram advertising global average $3.3/month. ChatGPT's usage depth and frequency are not lower than any subscription product, but its monetization is only 1/10 of Netflix's. This gap is not a ceiling, but an opportunity.

Advertising Business: An Overlooked New Revenue Stream. Ad testing launched in January 2026, with full rollout to US users in February. Internal forecasts predict $1B in ad ARR for 2026, reaching $25B by 2029. The Shopify partnership has proven the closed loop: in-chat shopping surpassed $100M ARR within six weeks, taking a 4% commission. The advertising inventory from 900 million WAU, valued at Facebook's global average, implies over $300B in value. This revenue stream was almost entirely unpriced in the $898B valuation.

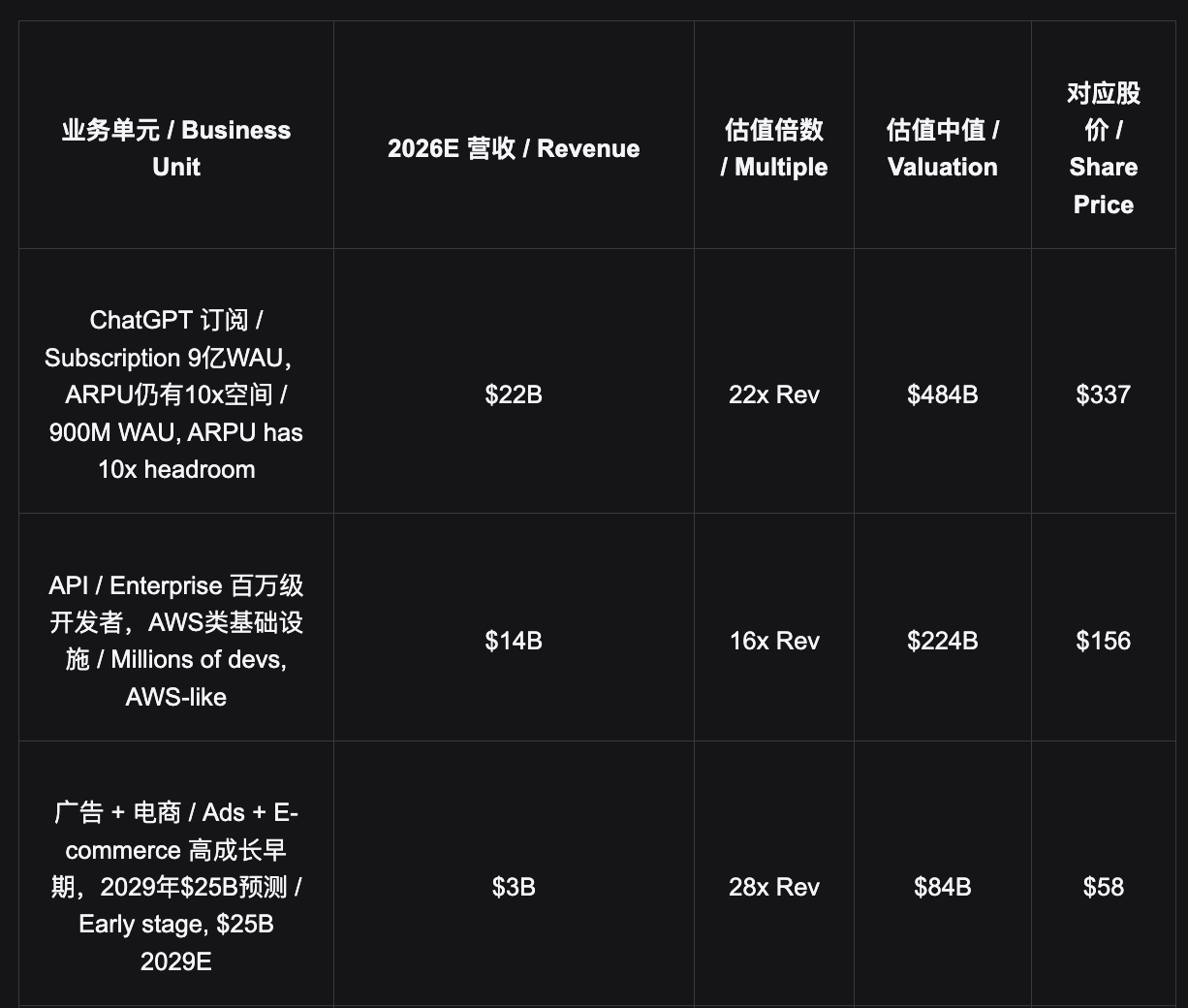

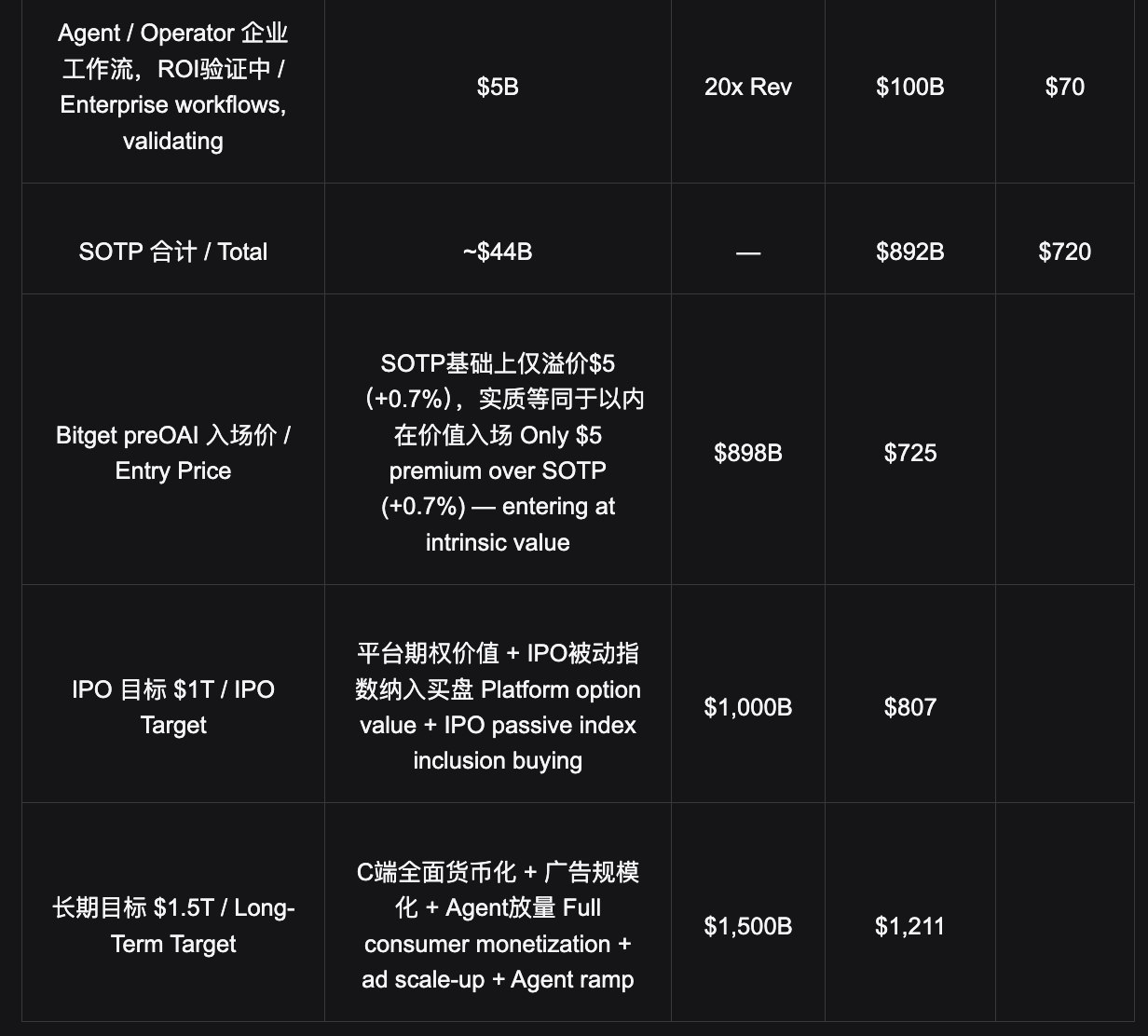

Sum-of-the-Parts Valuation: $898B is Already Below Intrinsic Value

Using forward-looking valuation based on expected 2026 financial data, the goal is to assess whether Bitget preOAI's entry price of $725 is reasonable and identify the sources of upside.

- Core Pricing Conclusion: The $725 entry price is almost flat with the SOTP median of $720—meaning you are entering at a price close to "visible business only," while the $300B+ option value from the ad business, AGI option value, and upside from repricing consumer platform premiums are not yet factored in. $898B is not an overvaluation; it undervalues the new revenue curve.

Pre-IPO Entry: Channel Comparison and Pricing Analysis

OpenAI is a private company; ordinary investors cannot directly purchase its equity through any public market. Key fact: The Series G institutional round equivalent price was $687.7 ($852B valuation), with a minimum subscription threshold of $100 million—a scale unattainable for individual investors regardless of asset size. Bitget preOAI at $725/share, corresponding to the current latest market valuation of $898B, is the only retail channel offering accessibility with secondary market liquidity.

Access Channel Comparison

Series G · $687.7

Institutional Round · Closed

Implied $852B · Closed · Min $100M

To IPO Low End +17.3%

To LT Target $1.5T +76.1%

Led by SoftBank with $122B, minimum $100 million, accessible only to large institutions. Institutional cost basis $687.7 ($852B), current preOAI at $725 corresponds to the latest $898B valuation—the market has repriced OpenAI, yielding a 5.4% paper profit for institutional entrants.

Hiive · $608

Real Equity · Accredited Only

Implied $873B · Secondary Transfer

To IPO Low End +32.7%

To LT Target $1.5T +99.2%

Must meet accredited investor criteria (net worth ≥ $1 million) with a minimum subscription of $25,000. Private equity transfer, no secondary market, settlement takes weeks—cannot react to catalyst events in real-time.

preOAI · $725

Bitget IPO Prime · Tokenized · Only Tradeable

$898B · Latest Market Price · No Accreditation

To IPO Low End +11.3%

To LT Target $1.5T +67.0%

The only channel with a secondary market. Tokenized structure, no accredited investor requirement, no minimum amount limit. Can be bought and sold anytime—catalyst events like GPT-6 release, IPO announcements can be traded in real-time. Post-IPO settlement is directly linked to OpenAI's public market price.

- Liquidity is the core differentiator: preOAI is a tokenized product with a secondary market that allows buying and selling anytime—directly trading on price catalysts within weeks of a GPT-6 release, capturing windows of opportunity. Hiive involves private equity transfers without a secondary market, unable to respond to catalysts; institutional rounds also lack exit paths. preOAI's $725 is approximately 5.4% above the institutional round's $687.7, corresponding to the latest market valuation of $898B—the entry price reflects the current market consensus on OpenAI's value.

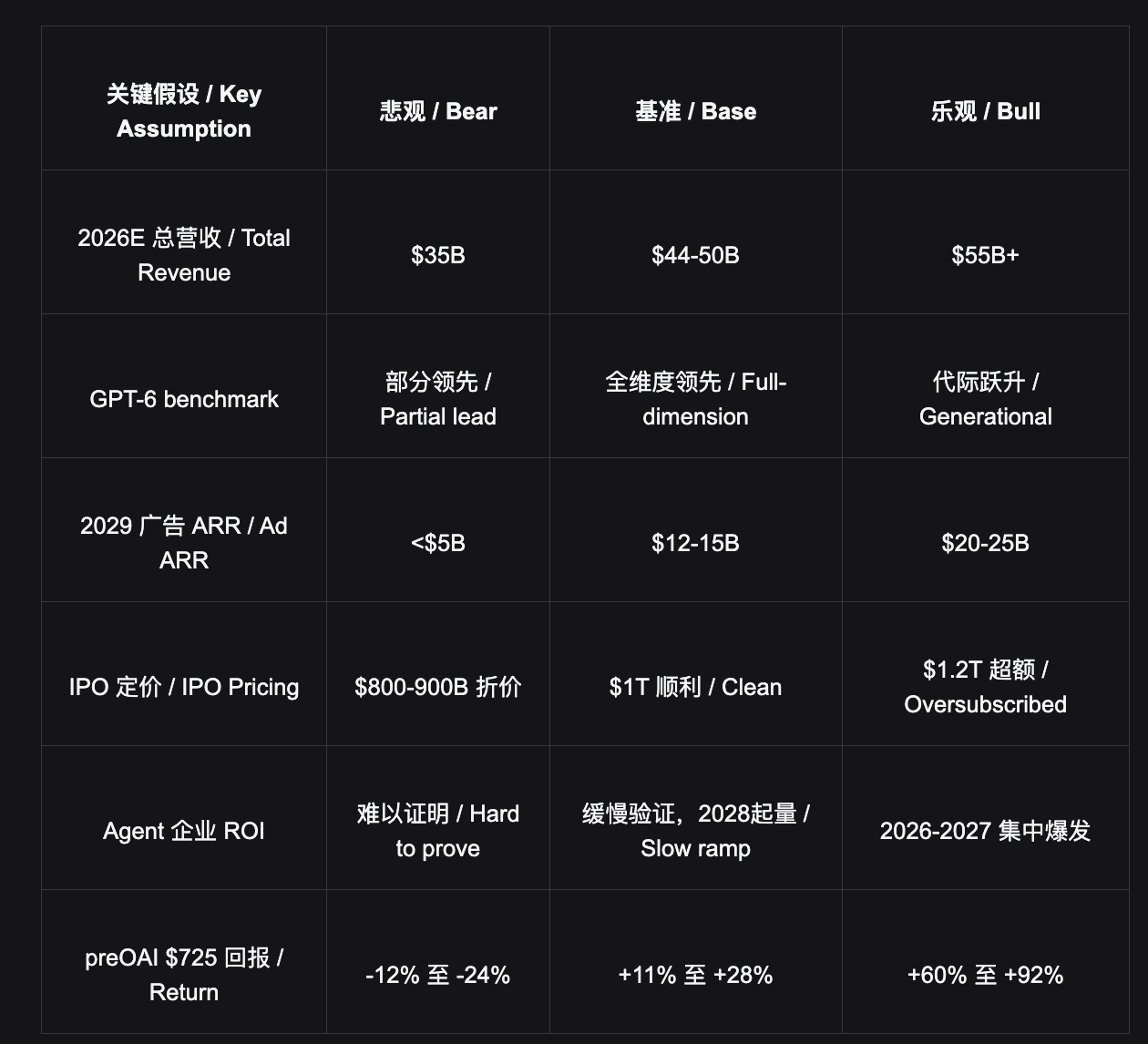

Scenario Analysis and Key Assumptions

Scenario Analysis

Bear Case $475—$550 $682B — $790B

GPT-6 disappoints; Gemini significantly erodes market share; advertising monetization harms user trust; IPO priced at a discount. Calculated from preOAI $725: Downside approximately -12% to -24%. ChatGPT's 1.3 billion MAUs provide a floor.

Base Case (Primary) $807—$928 $1T — $1.15T

GPT-6 re-establishes leadership; IPO in Q4 2026 priced at $1T; advertising scales gradually; 2026E revenue of $44-50B materializes as expected. Calculated from preOAI $725: Upside approximately +11% to +28%, realizable within 12 months.

Bull Case $1,000—$1,200 $1.44T — $1.72T

GPT-6 establishes generational leadership; Agent enterprise ROI proven and accelerates rollout; IPO oversubscribed; advertising reaches $25B ahead of schedule by 2029. Calculated from preOAI $725: Upside approximately +60% to +92%.

※ Key Downside Risks: ① Google Gemini achieves a large-scale comeback leveraging its product suite distribution (20% probability); ② Advertising monetization damages user trust, leading to WAU contraction (10%); ③ Continued delays in Agent delivery affect Enterprise renewals (15%); ④ Governance controversies (10%). The impact of these risks occurring independently is limited. Floor support: the user habit moat of ChatGPT's 1.3 billion MAUs will not collapse.

LLM Competitive Landscape: Strategic Divergence and Long-Term Coexistence of the Top Three

Competition in the large model layer is not a zero-sum game, but a coexistence of multiple oligopolies—the core user pools each company targets hardly overlap. OpenAI's 1.3 billion active users, Anthropic's 1-2 million high-paying developers, and Google's 3 billion ecosystem users represent three distinct infrastructure models for the AI era.

Competitive Landscape

OpenAI

$852B (Institutional Round)

▸ Strengths

1.3 billion MAU consumer gateway, actively opened, habit moat; only entity capable of raising capital at "national scale"; bottom-up culture allows for generational leaps by talent.

▸ Challenges

Coding dominance challenged by Anthropic; 300+ internal projects leading to execution dispersion; large consumer traffic creates pretraining burden.

▸ LT Ceiling

$1.5T+ (Consumer Platform Grade)

Anthropic

Secondary shares imply ~$800B, next round expected $800-850B

▸ Strengths

Abandons consumer space to go all-in on Coding; organizational execution is its moat; 1-2 million core developers generate more revenue than OpenAI's 50 million consumer subscriptions; transitioning API towards Agent OS.

▸ Challenges

No consumer platform; ceiling is "best developer tool" rather than "largest consumer platform."

▸ LT Ceiling

$1.5T+ (Developer OS Grade)

Google / Gemini

Alphabet $2T (AI upside not separately priced)

▸ Strengths

Ample compute, most data, unparalleled distribution capability (3 billion+ ecosystem users); robust advertising infrastructure.

▸ Challenges

Benchmark performance potentially inflated; coding lags by 3-4 months; complex internal politics, lacking PM culture; perpetually chasing, perpetually half a step behind.

▸ End-Game

Everyone finds their place: Google strong in distribution, OpenAI strong in the active gateway.

- Core Judgement: OpenAI and Anthropic are both $1.5 trillion+ companies long-term. Different paths, similar destination—OpenAI follows the consumer platform path (Apple/Google-like), Anthropic follows the developer OS path (AWS-like). The core user pools they target hardly overlap. This is not a zero-sum game but the parallel evolution of two dominant infrastructure models in the AI era. However, OpenAI's consumer platform premium has not been fully priced by the market—this is the core thesis for entering at $725 and the structural mispricing compared to Anthropic.

Disclaimer

This report is for internal research reference only and does not constitute investment advice. Tokenized products (preOAI) do not confer shareholder rights, voting rights, or dividend rights; economic returns are linked to a reference index, and settlement mechanism relies on platform credit. Private equity (Hiive) is limited to qualified/accredited investors with 3-5% fees; lock-up periods depend on shareholding structure. OpenAI's S-1 is in preparation; IPO valuation, timing, and issuance structure are all subject to change. Financial projections are analyst estimates, not official disclosures from OpenAI.

OpenAI — $122B Funding Announcement · CNBC — Series G $852B · Sacra — OpenAI Equity Research 2026 · Business of Apps — ChatGPT Statistics 2026 · Hiive — OpenAI $608.06 (April 2026) · Polymarket — GPT-6 Release Odds · IndexBox — OpenAI IPO $1T Target 2026 · ALM Corp — ChatGPT Ads $25B 2029 Projection