In-depth Analysis of Trade.xyz Data: Who is Trading US Stocks on-Chain?

- Core Insight: An in-depth analysis of Trade.xyz's four markets reveals that its trading volume is not driven by airdrop farmers, but rather by a small number of professional market makers, high-frequency trading bots, and retail traders primarily consisting of Polymarket users. Although airdrop farmers account for nearly half of the addresses, they contribute less than 1% of the trading volume.

- Key Elements:

- Address Distribution: Airdrop farmers make up 44% of total addresses (35,091), but contribute only 0.77% of the $52.65 billion trading volume; market makers account for less than 0.5% of addresses, yet contribute 63% ($32.75 billion) of the trading volume.

- Single Controller: 34,553 airdrop farmer addresses (99.9%) can be traced back to a single Polymarket user known as "Themino," who executed small transactions in a relay-style interaction to accumulate points.

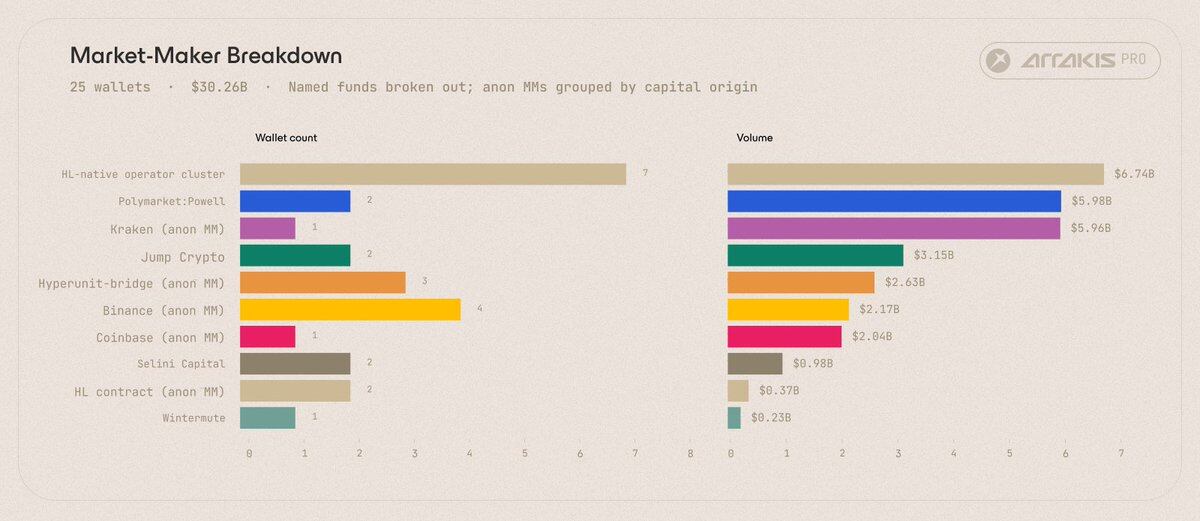

- Professional Market Makers: The top 5 market makers contributed 50% of the market-making trading volume, including well-known institutions such as Jump Crypto ($3.15 billion), Selini Capital ($1.03 billion), and Wintermute ($230 million).

- Retail Composition: Among high-volume retail traders, Polymarket users are the most identifiable group (22%), contributing $1.63 billion in trading volume, with fund sources linked to exchanges like Kraken.

- Data Authenticity: The analysis shows no evidence of large-scale wash trading; retail-level market-making bots provide genuine liquidity by placing orders, rather than actively taking orders to fabricate trading volume.

Source: Arrakis Finance

Compiled by Odaily Planet Daily (@OdailyChina); Translated by Azuma (@azuma_eth)

Earlier this month, we published an article titled "Who is trading on HIP-3". In that piece, we used a statistical inference methodology for attribution, classifying each address based on trading behavior over the past three months: addresses predominantly placing limit orders (makers) were categorized as Market Makers, addresses with high-frequency taker behavior were categorized as Arbitrageurs, and addresses with low fill rates and builder-tagged orders were considered Retail.

While this approach revealed some interesting patterns in the market structure, the classification was inherently probabilistic, and approximately 70% of addresses could not be effectively categorized.

In today's article, we will replace statistical inference with a mechanical classification approach. On HyperliquidX, every order contains a deterministic set of labels, signed and published by the exchange (e.g., time-in-force, builder code, fill flag, hold time). Based on this order metadata, we have divided all addresses into four main categories: Retail, Market Maker, Arbitrage Bot, or Airdrop Farmer.

The second step is to identify the specific entities behind these classifications. We extracted identity and trading behavior data from the Arkham and HyperTracker APIs. The top 450 addresses contributed 78% of total trading volume. Within this set, we identified multiple related entities, including addresses associated with Polymarket, Jump, Selini Capital, Wintermute, Abraxas Capital, and other institutions.

Through this two-step classification method, we observed several key findings, which are detailed below.

Address Distribution

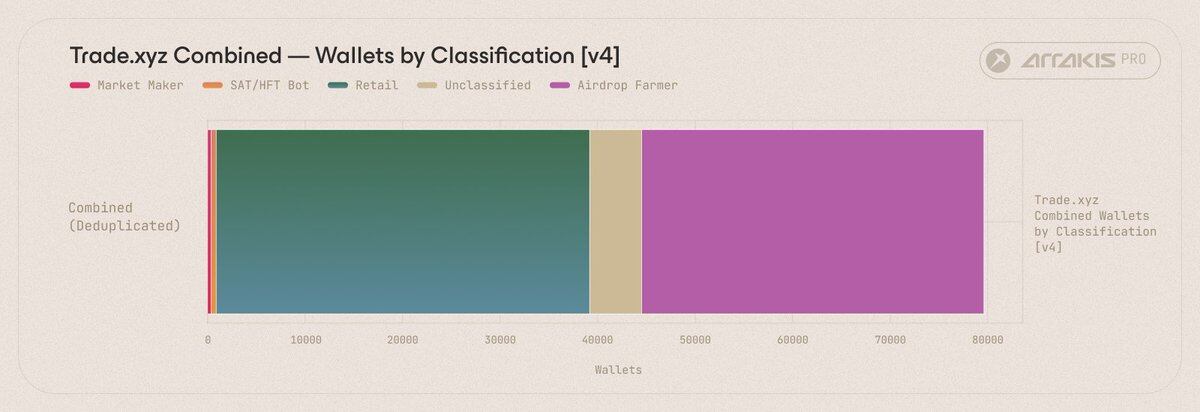

Our observation period was from March 10, 2026, to March 31, 2026, a total of 21 days. During this period, we monitored four Trade.xyz markets: CL (Crude Oil), SILVER (Silver), TSLA (Tesla), and XYZ100 (Index), recording a total of 79,622 unique participating wallets and $51.95 billion in total trading volume.

Of these 79,622 addresses that traded over the 21 days, a breakdown by volume shows that while market makers constitute less than 0.5% of total addresses, they contributed 63% of the trading volume.

When classified by wallet count rather than trading volume, the Airdrop Farmer category alone contained 35,091 addresses, nearly half of the total identified addresses.

Airdrop farmers constitute one of the largest categories by address count but the smallest by trading volume contribution. These 35,091 addresses, representing 44.07% of the total, generated only $400 million in trading volume during the observation period, which is 0.77% of the platform's total $51.95 billion volume. In other words, nearly half of the active addresses on Trade.xyz contributed less than 1% of the total market volume.

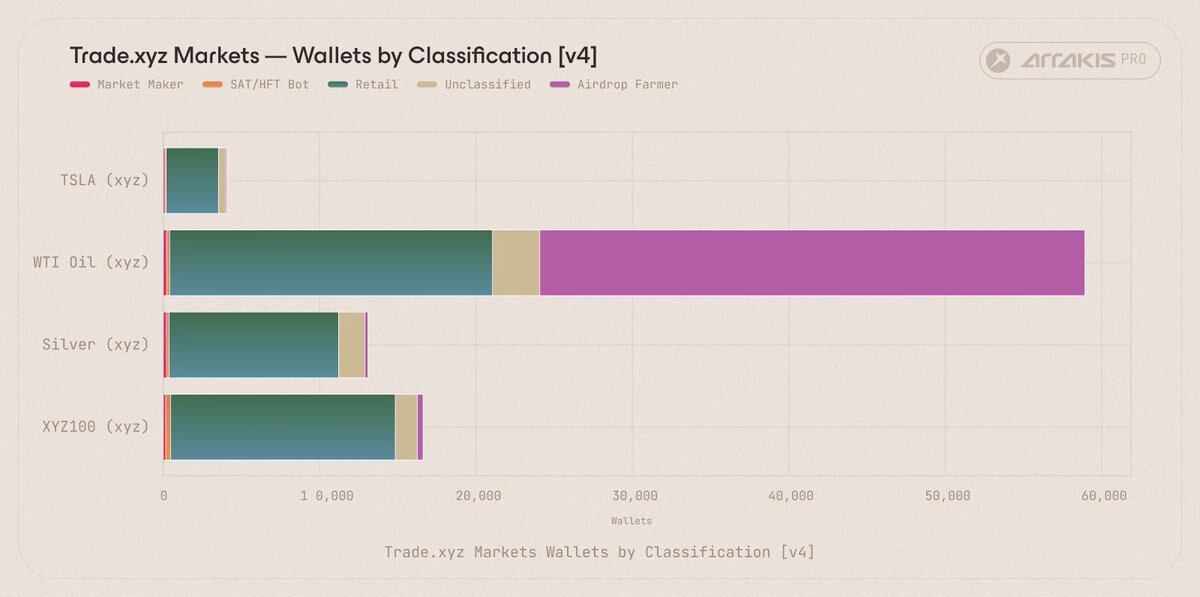

Breaking down by the specific market they participated in reveals another significant pattern.

Address distribution by market shows that the CL market absorbed 99.3% of airdrop farmers, likely due to its best execution efficiency.

Among the 35,091 airdrop farmer addresses, 34,859 (99.3%) traded CL during the observation period, with the remaining 232 wallets distributed across SILVER, TSLA, and XYZ100. This pattern aligns with typical airdrop farming behavior – each wallet accumulates volume through small, bidirectional consecutive trades without taking on price risk. This strategy relies on low execution costs and benefits from minimal slippage. CL, having the best depth among the four Trade.xyz markets, naturally became the venue for this activity.

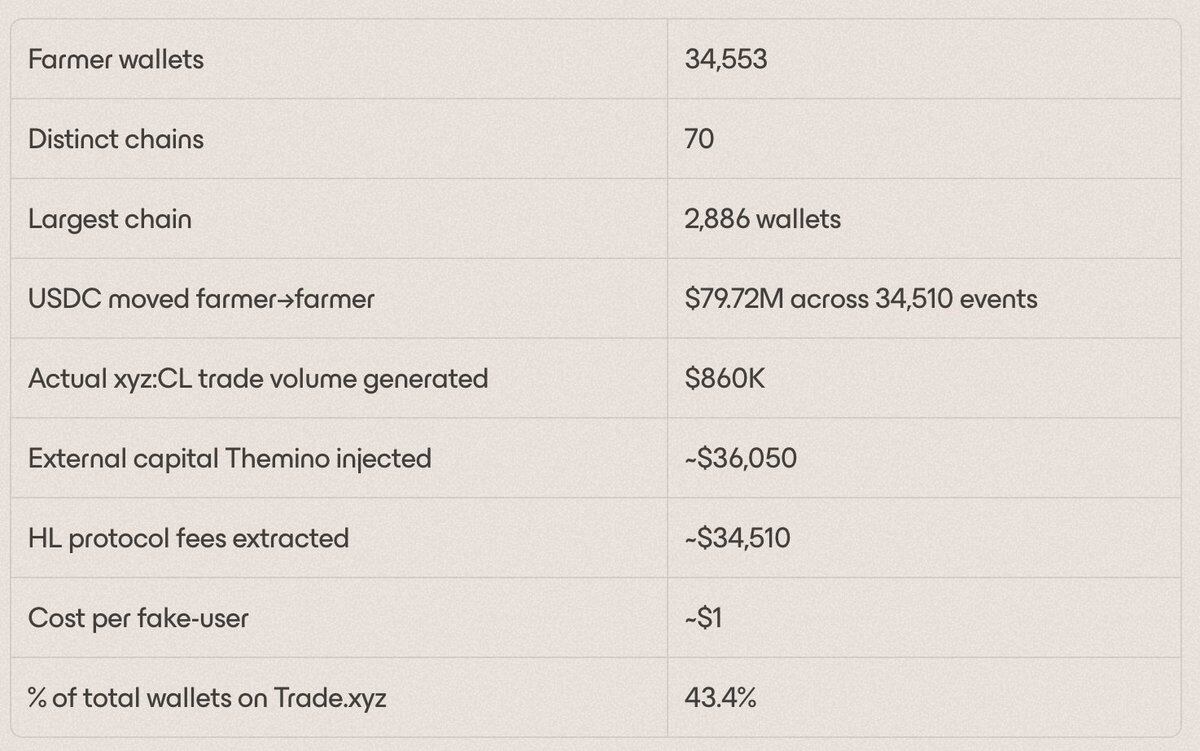

Another interesting observation is the entity behind these addresses. On-chain tracking, detailed later in this article, links 34,553 of these farmer addresses to a single Polymarket operator, which alone accounted for 43.4% of all participating addresses on Trade.xyz during the observation period.

At the other extreme of this classification are the market makers. 363 wallets (0.46% of active addresses) executed $32.75 billion in trading volume during the observation period, representing 63% of Trade.xyz's total volume. The remaining three categories lie in between – 522 SAT/HFT bots contributed $3.5 billion (6.7%), 38,307 addresses classified as Retail contributed $8.7 billion (16.7%), and 5,339 unclassified addresses contributed $6.61 billion (12.7%).

This unclassified volume, accounting for 12.7%, cannot be definitively assigned to a clear strategy based solely on metadata. A reasonable assumption is that a significant portion comes from retail users placing limit orders via the Hyperliquid frontend, or users submitting market and limit orders via the Trade.xyz frontend. Since orders from these two channels lack a dedicated builder code or specific TIF tag, these trades are invisible in our metadata-based classification.

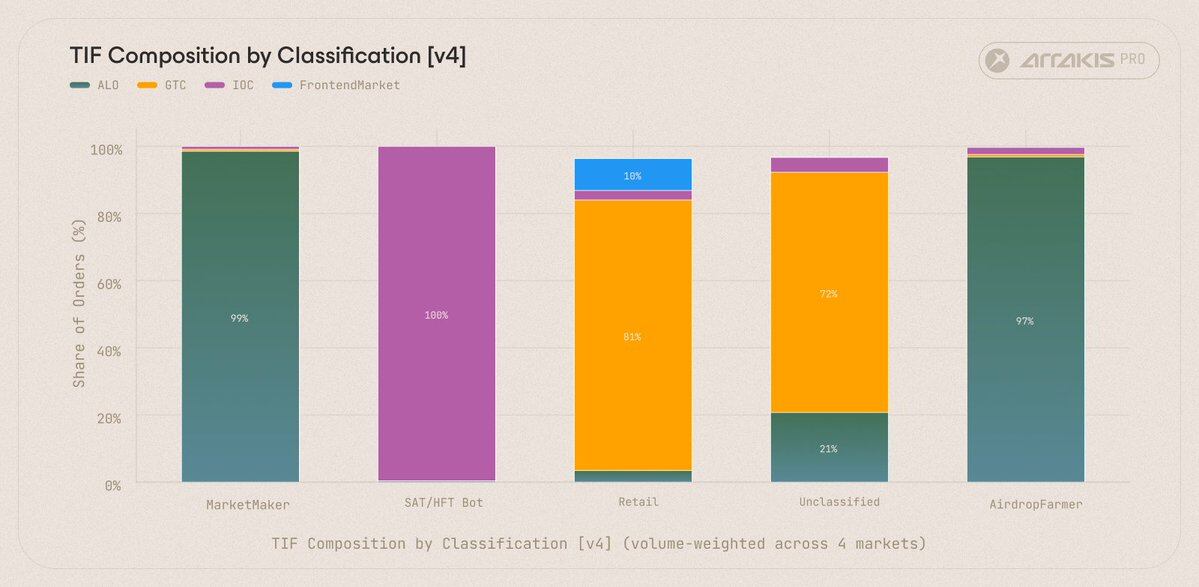

The time-in-force (TIF) distribution weighted by order count shows that 98.5% of market maker orders are ALO orders, while arbitrage bots use 100% IOC orders; the unclassified category has 71.5% GTC orders, a typical characteristic of manual limit orders placed by frontend users.

The TIF structure further supports this assumption. Within the aggregated orders of the unclassified category, 71.5% carry a GTC (Good Till Cancel) time-in-force label, typically used for persistent limit orders placed by frontend users.

Introducing the True High-Volume Player, Themino

In recent weeks, a growing controversy has surrounded Trade.xyz – whether its apparent user numbers reflect genuine human participation or are artificially inflated by airdrop farming activities in anticipation of the platform's imminent TGE. While we cannot comment comprehensively on the interaction status across the entire trading platform, our analysis of tick-by-tick trade data for the four Trade.xyz markets in March uncovered a noteworthy clue.

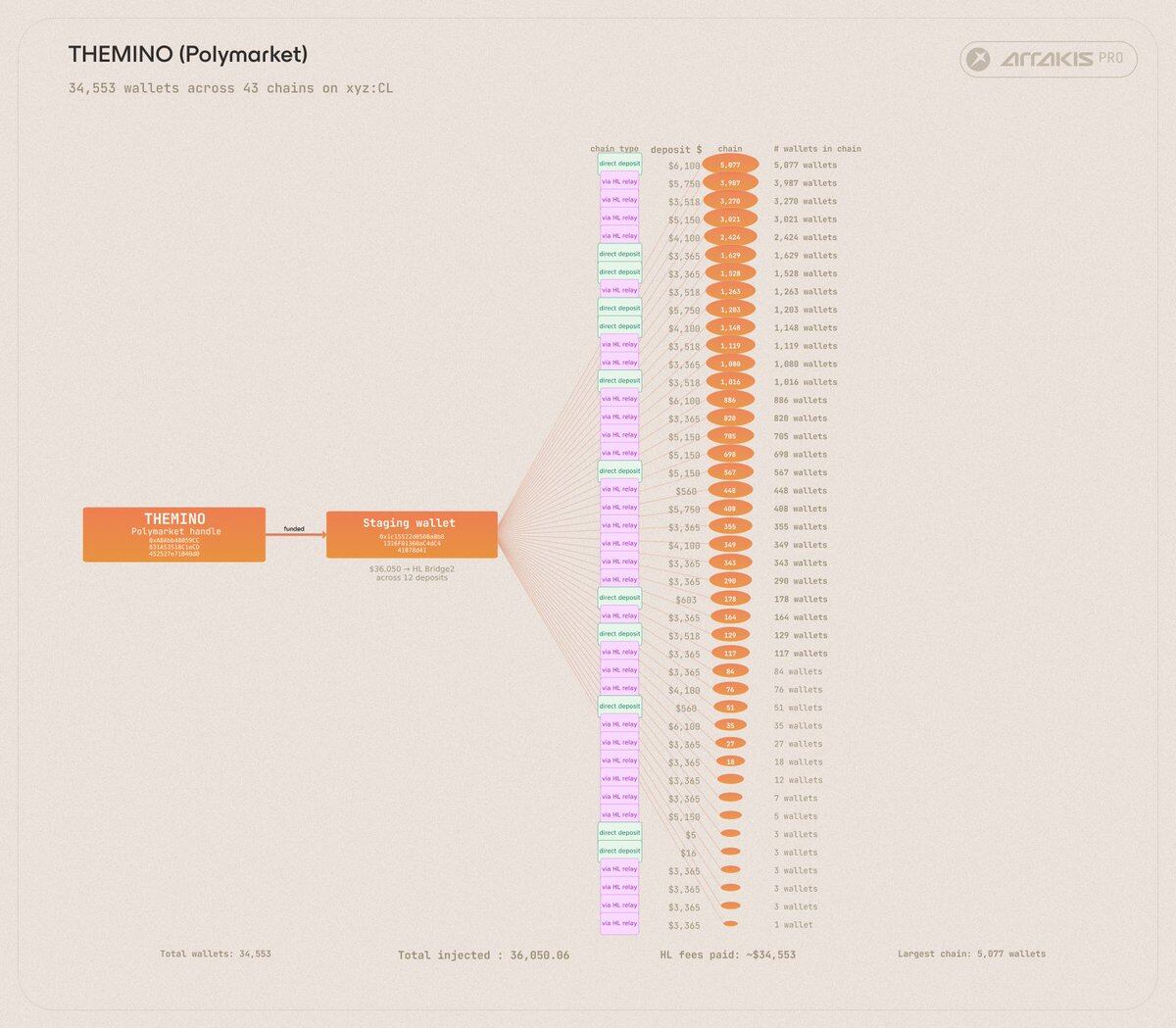

Out of the 34,602 addresses classified as airdrop farmers, 34,553 (99.9%) can be traced back to a single Polymarket user named Themino.

The Themino Cluster: A single Polymarket user identity spawned 70 independent linear chains, covering 34,553 airdrop farmer addresses.

Here is how Themino operates. Hyperliquid's Layer 1 provides an `internalTransfer` primitive that allows transferring USDC between addresses for a fixed fee of $1, regardless of the amount. The operator of Themino used this mechanism to "pass" an initial amount of funds sequentially through tens of thousands of new addresses. Each address executes the same five-step process in approximately 26 seconds:

- Receives funds from the previous address via `internalTransfer` (paying the $1 transfer fee upon the incoming transfer);

- Transfers $14 to a sub-account labeled `xyz`;

- Executes two IOC orders on the CL market (one buy, one sell), generating two fills and recording a certain volume;

- Transfers approximately $13.99 back to the main account (the few-cent difference results from execution slippage and trading fees);

- Transfers the remaining funds to the next address via `internalTransfer` (again paying the $1 fee);

- Repeats the process...

Throughout Themino's entire operation, 34,510 internal-transfer events occurred. Consequently, Themino accumulated $34,510 in protocol fees, a behavior pattern consistent with its trading history on Polymarket.

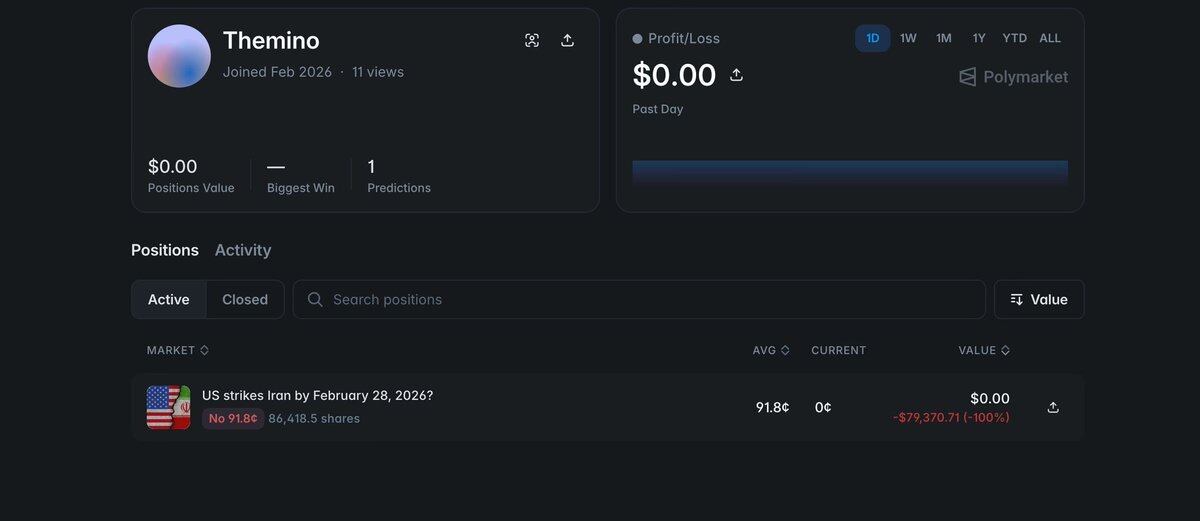

Furthermore, Themino once bet "No" on Polymarket for the event "Will the US strike Iran before Feb 28, 2026?", eventually losing about $80,000 – and the airstrike indeed occurred on February 28.

Different Groups Behind the Builders Tag

Hyperliquid appends an identifier to orders routed through third-party frontends to facilitate the collection of custom frontend fees. This identifier is the Builder Code, and it is the most direct basis for determining which interface (if any) an address uses to trade. The addresses that traded in these four markets can be grouped into three categories based on their Builder tags.

Algorithmic Builders: These products are primarily used by retail users to maximize trading volume on DEXs to accumulate points for potential airdrops. Before the end of 2025, interacting with a Perp DEX typically meant executing wash trading or non-directional taker-taker orders via algorithms. This was not only costly for participants but also a net negative for the exchange. Retail market making bots like tread.fi, Planemo Trading, and Origami Tech replaced wash trading with "valuable market making." Orders submitted through these products are post-only, meaning the wallet adds liquidity to the order book rather than consuming it.

As David Jeong (CEO of tread.fi) stated: "Before retail market making solutions, farming on a Perp DEX meant wash trading, artificially inflating volume by paying execution costs, taking on slippage, and even risking bans. We solved this by building a new interaction scheme where bots only post maker orders on both the bid and ask sides. Users interact at a lower cost, often capturing spread, and the byproduct is real liquidity at the best bid and offer – exactly what the HIP-3 equity-style perpetual contracts need during the nights and weekends when traditional market makers do not quote. It is a better way to interact and is why HIP-3 markets now have good execution quality."

The contribution of these market making bots to the market is particularly evident during periods when traditional market makers do not quote. CME WTI crude oil futures close on Friday afternoon and reopen on Sunday evening; equity-style perpetuals face similar overnight and weekend gaps. During these time windows, retail market making bots fill the top-of-book liquidity for markets like CL and TSLA.

It is important to note that although we classify addresses routed through these algorithmic products as "airdrop" in this analysis, their trading behavior and market impact are structurally different from sybil farming.

Wallet-integrated Builders: These are perpetual trading interfaces embedded directly within user wallets. Since early 2026, this type of integration has become one of the largest sources of retail order flow on HIP-3. This category includes Phantom, MetaMask, Rabby, Rainbow, and OneKey. The median trading volume per wallet ranges from $1,000 to $3,000, consistent with convenience-focused retail users who prioritize ease of access over small differences in builder fees.

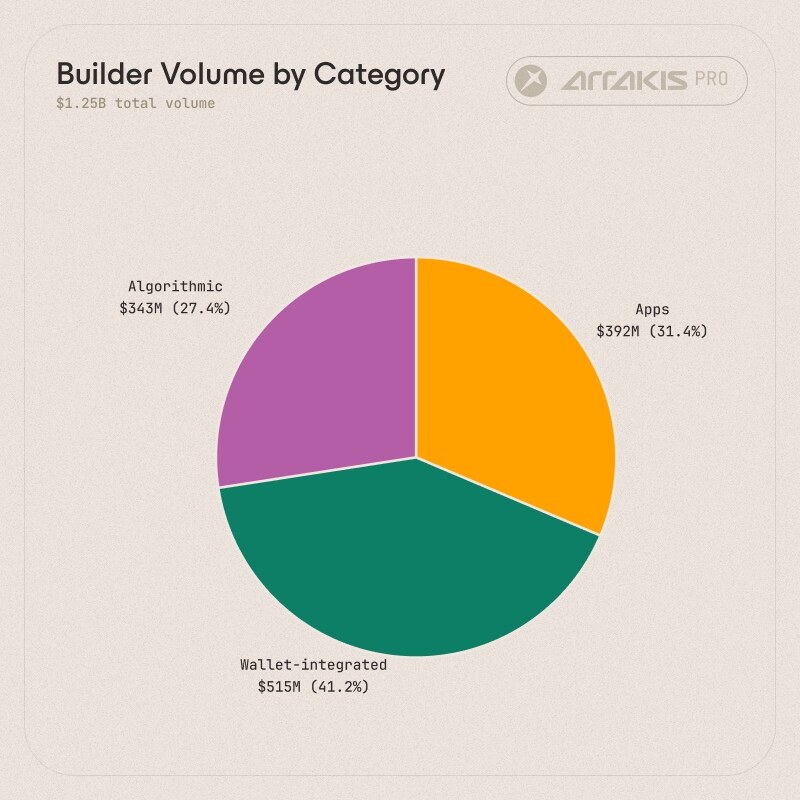

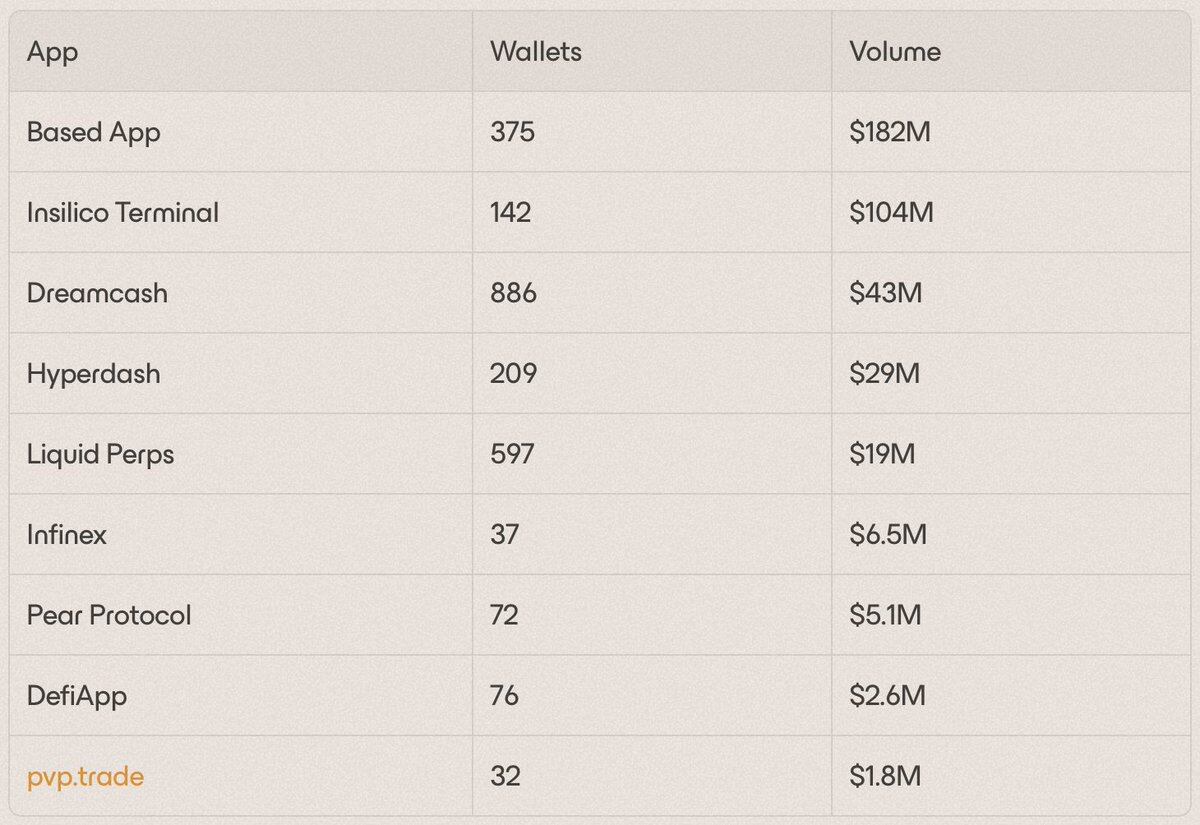

Apps Builders: These are standalone perpetual trading frontends and integrated products – tools for traders that offer a more complete workflow than wallet plugins, including better order placement experience, charts, position management, and execution tools. This category has fewer addresses than wallet-integrated channels but higher volume per address, characteristic of a heavy user base that values functional depth over out-of-the-box convenience. Relevant products include Insilico Terminal, Liquid, Hyperdash, Based, Dreamcash, Infinex, Pear Protocol, Defi App, and pvp.trade.

VKTR (Growth Lead at Insilico Terminal) summarized: "At Insilico, we view HIP-3 markets as the next step in running real-world asset exposure natively on crypto rails. Traders don't just want another frontend; they need fast execution, clear market access, and the ability to switch seamlessly between crypto and macro assets without leaving their existing workflow. Trade.xyz is one of the clearest manifestations of this demand. The order flow routed through Insilico shows that when a trading venue has sufficient depth, a practical product, and an experience designed for professional participants, there is indeed a genuine, sophisticated user base for on-chain perpetuals."

Market Maker Address Analysis

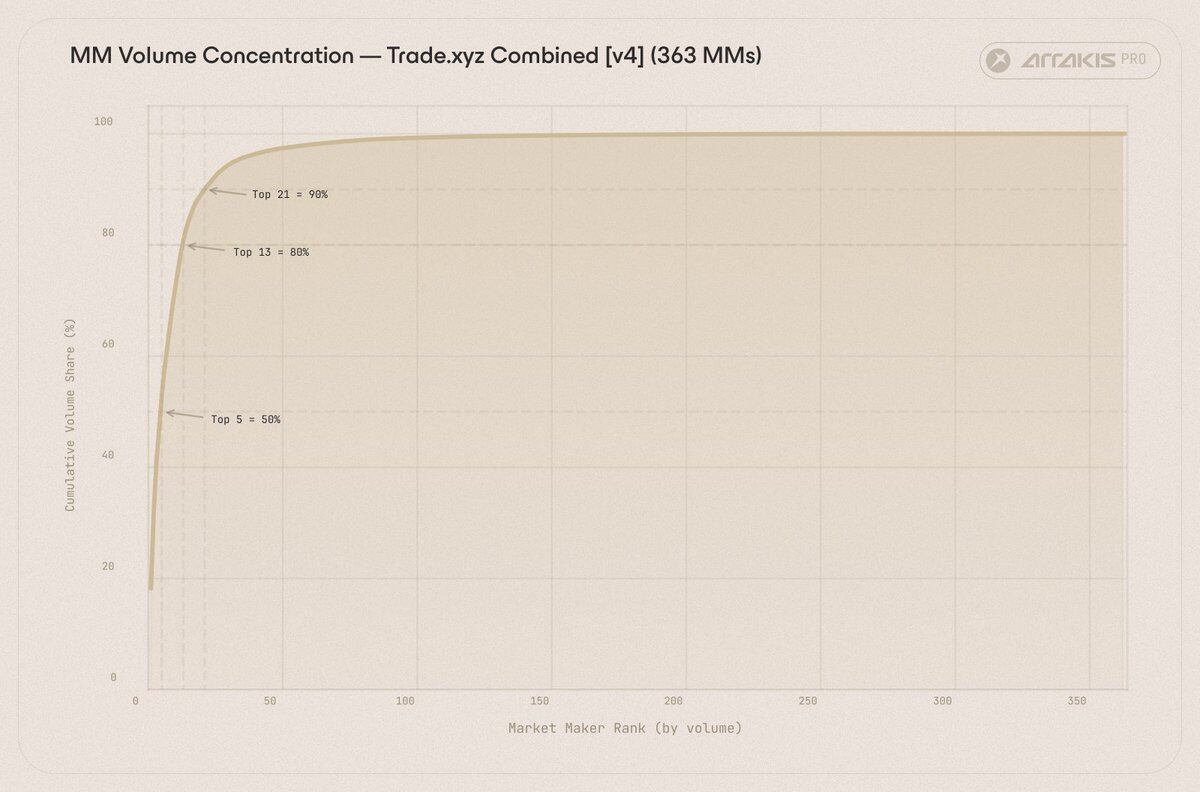

The market making landscape on Trade.xyz is highly concentrated. The top 5 market makers contributed 50% of market making volume, the top 13 accounted for 80%, and the top 21 for 90%. In other words, the vast majority of the market making order book is dominated by a small number of trading desks.

The cumulative share of market making volume by address rank shows that the top 5 desks contributed 50% of all market making flow, the top 13 reached 80%, and the top 21 reached 90%.

The second largest market making address is one of the most interesting in the entire sample. 0xc926ddba…98d3 executed $4.39 billion in volume with a 0.52% fill rate, a classic market making behavior pattern. Arkham tags this address as Powell from Polymarket. That is to say, one of the largest market makers on Trade.xyz is, in fact, a Polymarket user who provides two-sided quotes across multiple HIP-3 markets.

Other notable market making desks include:

- Jump Crypto operated two addresses, with a combined volume of $3.15 billion, funded from 0xf584…d621 (identified by Arkham as a Jump funding wallet), which holds over $160 million in a diversified portfolio including LINK, LIT, EIGEN, BNB, ETH, USDC, and USDT.

- Selini Capital operated three addresses, two executing pure market making quotes (0x44a3e1…35dd, 0x76987c…4480) and one executing pure aggressive takers (0x427be6…d1d9), all running via API, with a total trade size of $1.03 billion. Hyperliquid's order flow tagging mechanism allows Selini's market making wallets to be distinguished from its HFT wallets, showing the same desk operating on both sides of the order book.

- Wintermute ran one market making address, with a volume of $229.6 million (0xecb63caa…2b00), smaller than Jump and Selini, with funds sourced from OKX.