Polymarket V2 Launches: Have Phantom Orders Been Fixed?

- Core Thesis: Polymarket's V2 upgrade removed the primary cause of "phantom orders" (the nonce mechanism) but hasn't completely eliminated the problem; as long as its off-chain matching, on-chain settlement model remains, order uncertainty cannot be fully resolved.

- Key Elements:

- "Phantom orders" refer to orders shown as filled off-chain that ultimately fail to settle on-chain, primarily due to the time lag between off-chain matching and on-chain settlement.

- In V1, attackers could exploit the incrementNonce mechanism at extremely low gas costs to invalidate already-matched orders on-chain, leading to unstable trading outcomes for users.

- V2 removed the global nonce mechanism, switching to single order hash cancellation, which significantly reduced the impact scope and profit potential for attackers attempting batch cancellations.

- While V2 patched the most obvious attack vector, the state discrepancies between off-chain and on-chain (balances, approvals, contract executions, etc.) still exist, meaning the underlying conditions for "phantom orders" remain unchanged.

- Other updates include the introduction of the collateralized stablecoin PUSD, a new CLOB-Client SDK, and 1271 signature support, aimed at improving system stability and institutional onboarding capabilities.

Original by Odaily (@OdailyChina)

Author: Asher (@Asher_0210)

Last night, Polymarket entered a maintenance window, paused trading, and cleared the order book, before officially launching CLOB V2.

According to details previously disclosed by the team, this upgrade includes new contracts, a new order book, a new collateral token called Polymarket USD, and a new CLOB-Client SDK. For users, changes like PUSD, the SDK, and the order structure may not be immediately noticeable. What truly deserves attention right away is the long-standing issue of Ghost Fills on Polymarket, commonly known in the community as "ghost orders."

V2 has indeed addressed this problem. The previously exploitable nonce mechanism has been removed, and the order structure along with the cancellation method have also changed. However, this does not mean ghost orders have been completely eliminated, because Polymarket's core trading model remains off-chain matching with on-chain settlement. As long as a time lag exists between these two stages, similar issues will be very difficult to eradicate entirely.

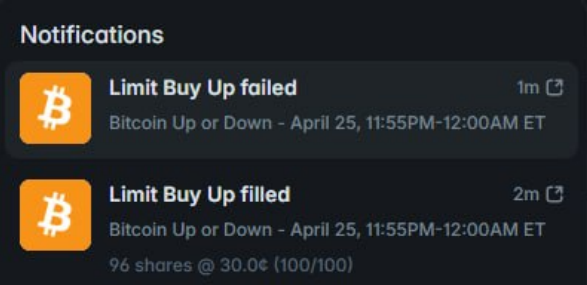

Orders Show as Filled, Why Do They Ultimately Fail?

Simply put, ghost orders refer to an order that appears to have been successfully matched off-chain but ultimately fails to settle on-chain.

Polymarket employs a model of off-chain order book matching followed by on-chain settlement. The advantage of this design is clear: faster transaction speeds, lower costs, and better suitability for short-cycle, high-frequency prediction markets like the 5-minute markets.

The problem lies precisely in this time gap. An order showing as matched on the off-chain order book doesn't guarantee successful on-chain settlement. In some short-cycle markets, users might see an order already marked as filled, believing they have purchased the corresponding position; but when the transaction is actually submitted on-chain, settlement fails. A trade that seemed completed a moment ago is later reversed by the system.

For users, the most frustrating aspect of this experience isn't simply the failure, but the uncertainty. Believing a buy or sell order has been executed, only to find it hasn't gone through by the time they check again. By the time they re-enter the order, the price may have changed, and the trading opportunity may have been missed.

Old Version's Problem: Cost of Cancellation Was Too Low

In V1, one of the most exploited paths for ghost orders came from incrementNonce. The nonce can be understood as a status identifier for an order. Originally designed to help the system manage orders, in the old version, attackers could call incrementNonce to invalidate orders associated with a specific address that carried old nonces during on-chain settlement.

This created a window of opportunity for attackers to exploit the time lag. An attacker could first have an order matched off-chain, making the system display that a "trade has occurred." Then, before the settlement was actually broadcast on-chain, they could update the nonce, causing the execution of these orders to fail. The result is that a seemingly completed transaction never actually materializes on-chain.

The core issue is that this operation had an extremely low cost but could affect a batch of orders. An attacker only needed to pay a very low gas fee to cause orders that should have been filled to fail during the settlement stage. What the front-end shows is an order that was first filled and then failed, but the actual impact is unstable trade outcomes, potentially causing users to miss the original fill price and trading opportunities.

The ghost order problem is not just a simple front-end display error or an occasional on-chain failure; it directly undermines user trust in trade results.

V2 Provides a Fix, But Not a Complete Eradication

The most critical change in V2 is the removal of the original global nonce design. This means the past method of using incrementNonce to affect a batch of old orders at once has been closed off. Concurrently, V2 simplifies the order structure, moving order cancellations to a more granular, single order hash basis. Compared to the old version, the scope of impact for cancellations has been significantly reduced, making it much harder for attackers to disrupt a large number of pending orders with a single low-cost action.

This is a substantial fix for the ghost order problem. The previous issue was the combination of low attack cost, wide impact range, and low barrier to replication. With V2, the most easily exploited path has been removed. Attackers will need to pay a higher cost and rely more on specific system responses to continue creating similar issues. Furthermore, the introduction of delays in mechanisms like pauseUser also reduces the potential for certain state changes to be instantly abused during the matching and settlement window.

Overall, the direction of V2 is clear: first address the links most vulnerable to attackers, and then reduce the profit margin for similar attacks.

However, this is not equivalent to completely solving the ghost order problem. The reason is that Polymarket has not changed its fundamental model of off-chain matching and on-chain settlement. As long as orders are not matched and settled within the same environment, a state discrepancy will always exist between the off-chain and on-chain systems. Changes in balance, authorization issues, order status updates, cancellation actions, or contract execution failures can all prevent an order that has been matched off-chain from ultimately settling on-chain.

In other words, V2 solves the most obvious and exploitable attack path from the old version, but not the underlying conditions that give rise to ghost orders.

Other Updates: More About Bolstering the Trading System's Foundation

Beyond ghost orders, V2 also introduces updates like PUSD, the SDK, and 1271 signature support:

- PUSD is the new collateral stablecoin. Polymarket is migrating from USDC.e to Polymarket USD, which is 1:1 backed by USDC. This is largely transparent to regular users, but the underlying asset processing will be more unified.

- The new CLOB-Client SDK is mainly targeted at market makers, bots, and system integrators. After V2, these users need to upgrade their client and re-sign orders using the new order structure.

- 1271 signature support allows smart contract wallets, multi-sig accounts, institutional accounts, and more complex bot wallets to connect to Polymarket more smoothly.

In summary, Polymarket isn't just fixing a single vulnerability; it's transforming itself from a prediction market application into a trading infrastructure closer to that of an exchange. As the number of market makers, API users, and automated traders grows, the stability of order execution, settlement, and payout becomes more critical than "how fun the market is."

V2 is Not the End, But the Beginning of Continuous Repair

With the launch of V2, Polymarket has at least closed off the most obvious attack vector for ghost orders. The past method of low-cost cancellation impacting a batch of orders is now very difficult to replicate in the same way. For a rapidly expanding trading platform, this was a necessary step.

However, the root cause of ghost orders will not completely disappear with just one version upgrade. As long as Polymarket continues to use the off-chain matching, on-chain settlement model, the system must constantly manage the discrepancies between off-chain states and on-chain results. V2 is more like a first step – first address the most obvious and exploitable problems, then continue to bolster matching, settlement, monitoring, and risk control capabilities through subsequent updates.

Prediction markets inherently trade in uncertainty. If the orders themselves are also filled with uncertainty, users are no longer just facing market risk, but systemic risk.

Related Content

Polymarket Stalled: The Real Test After the Traffic Boom Has Arrived