Arkstream Capital: How Ordinary People Can Properly Participate in Tokenized Pre-IPOs

- Core Thesis: The tokenization of traditional assets is the main narrative for the next 5-10 years in crypto. The latest development is leading exchanges launching Pre-IPO token products, such as those linked to SpaceX. This breaks down high-threshold old-stock trading, originally only available to institutions, into fractional shares accessible to retail investors, marking a new phase for the RWA wave.

- Key Elements:

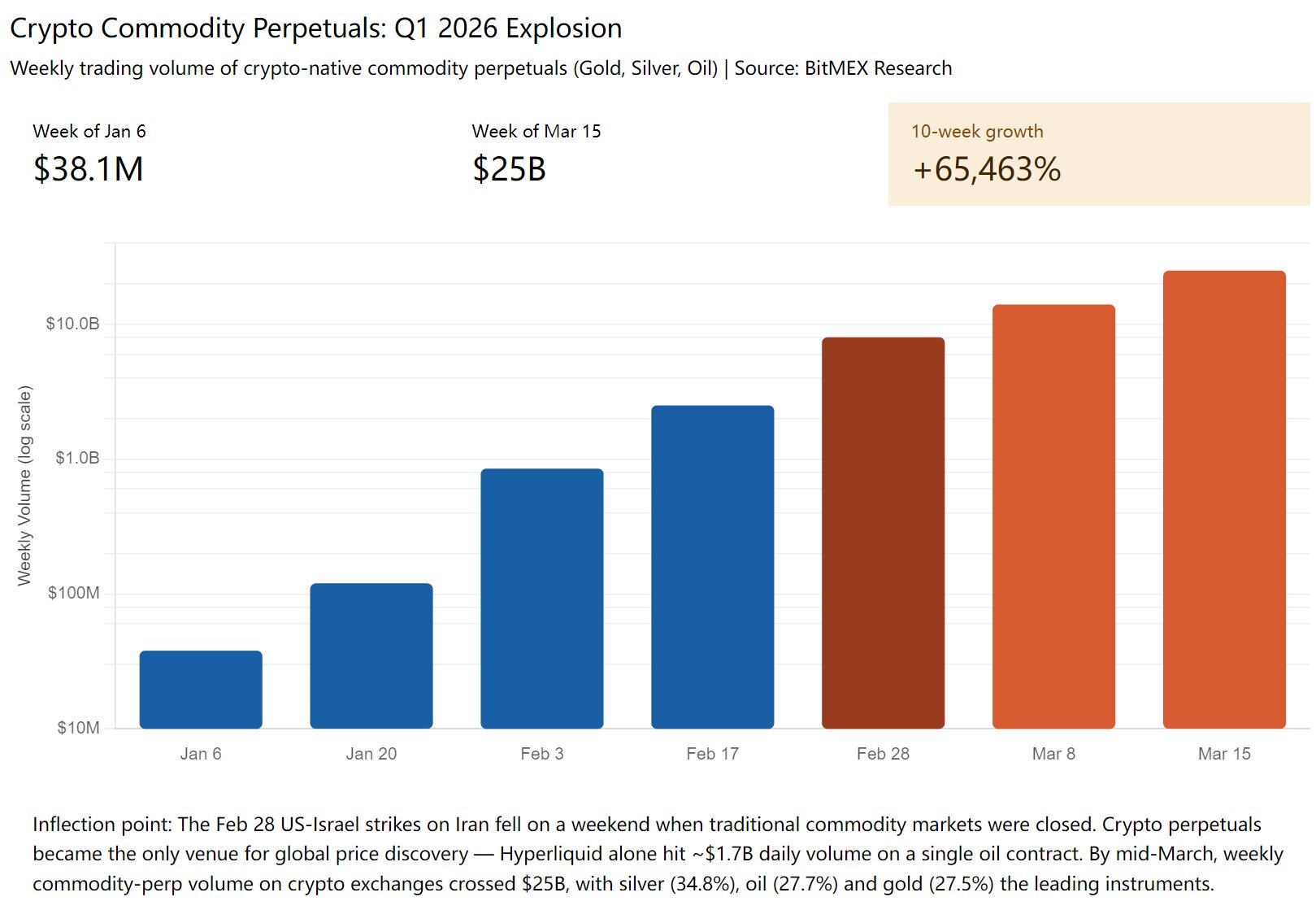

- In Q1 2026, weekly trading volume for commodity perpetual swaps on crypto exchanges surged from $38.1M to $25B, a growth of 65,463%. Notably, Binance's TradFi Perpetual segment recorded cumulative trading volume exceeding $153B over three months, with its Silver contract's global market share soaring from 0.2% to 4.9%.

- Traditional assets (US stocks, precious metals, crude oil, forex) are being tokenized, offering 7×24 global liquidity. For example, during the Iran conflict, while traditional markets were closed, Hyperliquid's crude oil perpetual instantly spiked 5%, and Tether's gold token XAUT saw a single-day trading volume surpassing $300 million.

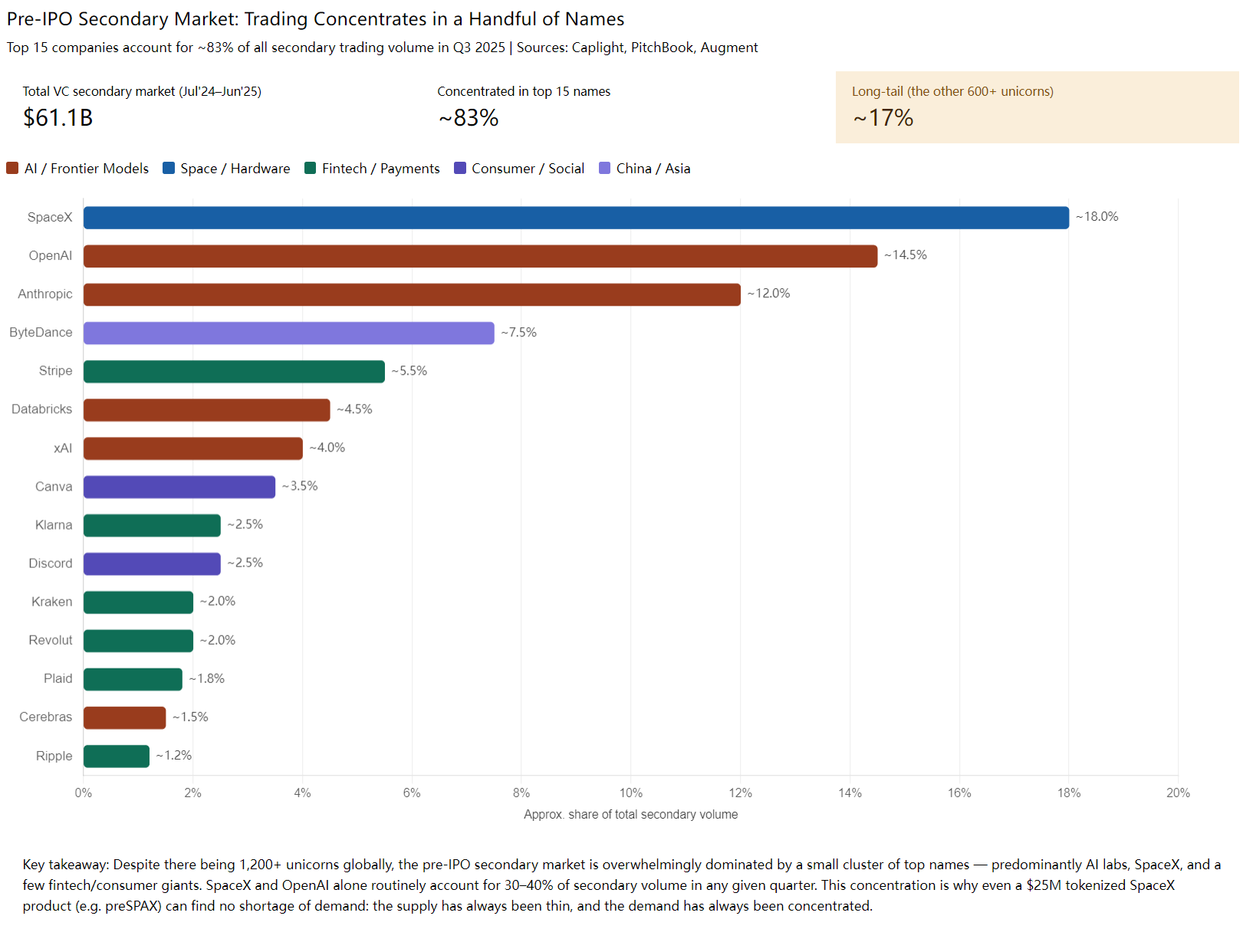

- The global trading volume of the Pre-IPO secondary market reached $160B in 2024, but the minimum transaction ticket size is typically over $10M, effectively excluding retail investors. The top 15 targets, like SpaceX and OpenAI, account for approximately 83% of the trading volume, making supply scarce.

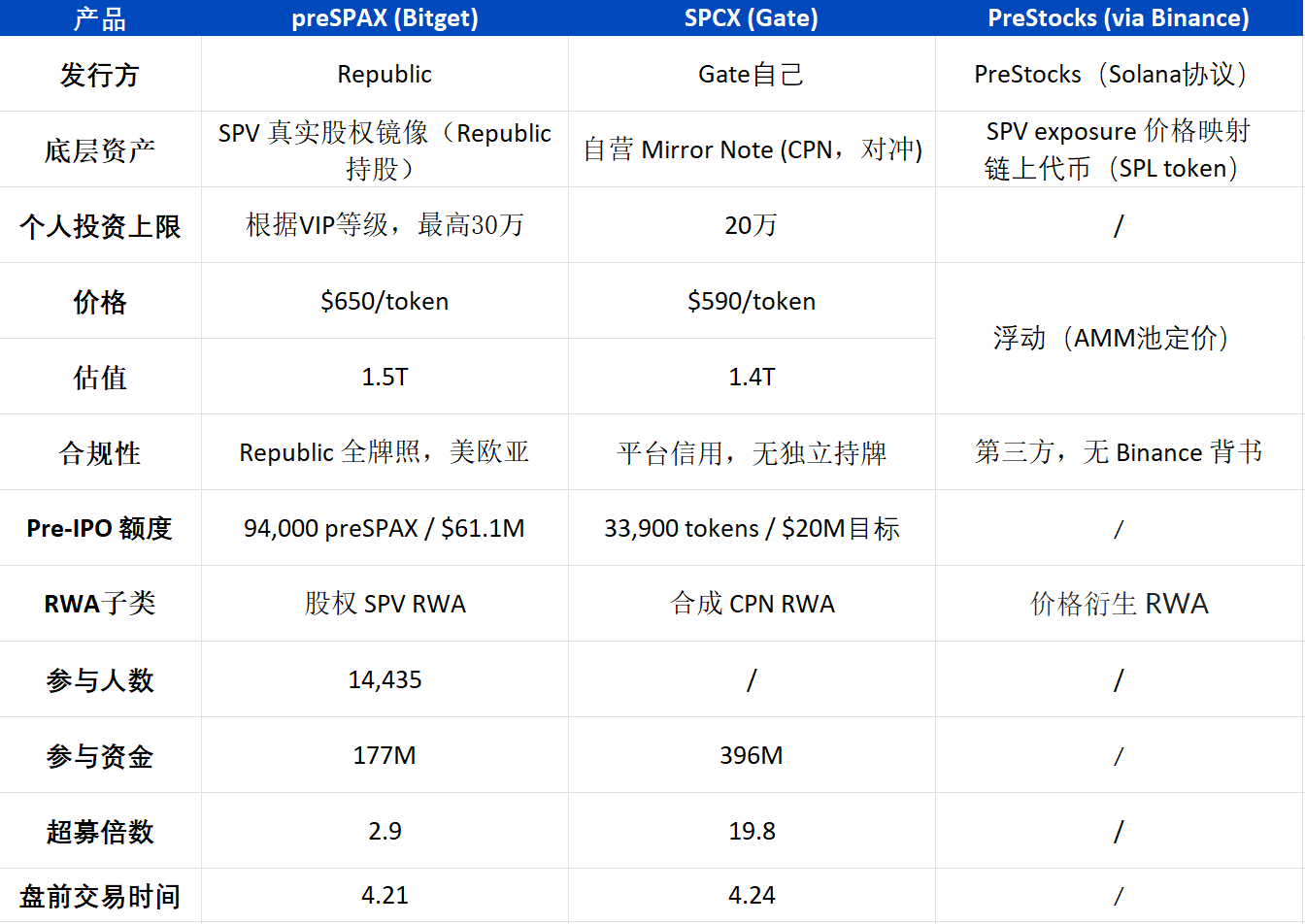

- Pre-IPO token products launched by exchanges (e.g., SpaceX-related tokens on Bitget, Gate, Binance) essentially involve the platform purchasing old shares in the traditional market, splitting them for retail via a token wrapper, and providing a 6-month settlement period to correspond with the post-IPO lock-up.

- Participating in Pre-IPOs requires differentiating them from short-term crypto IDO speculation. One should be long-term bullish on the valuation growth potential of the target (e.g., SpaceX, OpenAI), and pay close attention to the product's security and the issuer's ability to absorb losses. Historically, entities like Stripe and WeWork have experienced significant valuation declines or even bankruptcy.

Original author: @Chandler_btc | Arkstream Capital

TL;DR

- In Q1 2026, the weekly trading volume of commodity perpetual contracts (gold, silver, crude oil) on crypto exchanges surged from $38.1M to $25B, a growth of 65,463%. The tokenization of traditional assets will be the main narrative for Crypto over the next 5-10 years. Pre-IPO tokenization is just the latest category to enter this arena.

- In April, three major exchanges – Bitget, Gate, and Binance (PreStocks) – almost simultaneously listed SpaceX-related tokenized products. Their compliance methods differ, but the essence is the same: breaking down the pre-IPO market share, previously reserved for ultra-high-net-worth clients, into small pieces for retail investors.

This article aims to clarify two main points: first, what traditional Pre-IPO actually is, and second, how retail investors can participate.

Tokenization of Traditional Assets Will Be the Main Narrative for Crypto in the Next 5-10 Years

According to statistics, in Q1 2026, the weekly trading volume of commodity perpetual contracts (gold, silver, crude oil) on crypto exchanges soared from $38.1M to $25B, a growth of 65,463%. After Binance launched the TradFi Perpetual segment in January, cumulative trading volume exceeded $153B in three months, with over 114 million trades executed. Its XAG (Silver) contract achieved an average daily trading volume of $1.31B, and its global market share surged from 0.2% to 4.9% (a 23.5x increase).

The most notable event was the Iran crisis at the end of February. When the US and Israel launched strikes against Iran over the weekend, traditional futures, stocks, and forex markets were all closed. Only the crypto market remained active globally. At that time, Hyperliquid's crude oil perpetual instantly surged 5%, Tether Gold (XAUT) saw a single-day trading volume exceeding $300 million, and Bitwise's CIO called it "the weekend that changed finance."

US stocks, precious metals, crude oil, and forex – assets traditionally traded only from 9 to 4 on weekdays – are now being tokenized, placed on-chain, and provided with 7×24 global liquidity. Pre-IPO tokenization is simply the latest category to join this wave.

Source: BitMEX Research

What Exactly is Pre-IPO?

The Pre-IPO secondary market (trading of existing shares) has existed for over a decade, with global trading volume reaching $160B in 2024. The direct secondary market in the US alone accounted for $61.1B. Buyers are primarily family offices, sovereign wealth funds, institutional investors, and high-net-worth individuals, with single transactions typically starting at $10M+, effectively shutting out retail investors.

The vast majority of transactions are conducted through SPVs (Special Purpose Vehicles): the original shareholder places shares into a newly established shell company, which then sells its own shares to new buyers. The buyer receives an interest in the SPV, indirectly holding shares in the underlying company. This is because secondary share transactions rarely allow strangers directly onto the cap table (company shareholder registry), as this could trigger other shareholders' ROFR (Right of First Refusal), a cumbersome process that could be blocked by the original shareholders. Therefore, the end buyer ultimately acquires and holds LP interests or Units in the SPV, equivalent to indirect ownership of the existing shares.

As secondary market trading is highly concentrated in a few top assets, US AI/aerospace giants like SpaceX, OpenAI, and Anthropic consistently account for 30-40% of trading volume. Coupled with leading unicorns like ByteDance, Stripe, Databricks, and xAI, the top 15 companies capture approximately 83% of the total market volume. (This concentration explains why even when Bitget/Gate only issue a single SpaceX token, they can easily be oversubscribed by hundreds of millions – supply for top-tier Pre-IPO shares is scarce, while demand is highly concentrated.)

The vast majority of these assets are US-based, making CFIUS (Committee on Foreign Investment in the United States) the biggest regulatory hurdle. It restricts foreign capital from investing in sensitive US industries (AI, semiconductors, defense). Funds from certain countries face strict scrutiny when buying into SpaceX/Anthropic. Consequently, sellers typically stipulate that purchases by UBOS from certain countries are prohibited – the GP will look through the SPV to check if the buyer's ultimate controller holds a restricted nationality (e.g., Chinese, Russian, Iranian). The deeper the structure, the harder to check, but it's not foolproof. We've seen a deal fall through because a Chinese UBO was discovered within a two-tier SPV structure.

Sources:Caplight PitchBook, Augment

After a US company's IPO, there is a standard Lock-up Period: SEC Rule 144 combined with underwriter agreements stipulate that early shareholders and employees cannot sell their shares on the public market until 6 months after the IPO. This rule applies to almost all US companies (Facebook, Coinbase, Reddit, Cerebras all had 6-month lock-ups). This is why Bitget/Gate's Pre-IPO tokens require a "6-month wait for delivery," but it doesn't affect pre-market trading.

Insights into Real Pre-IPO Transaction Details

High Ticket Size Threshold

Traditional Pre-IPO ticket sizes generally start at $10M. Sub-$1M tickets are mostly ignored – not due to lack of interest, but because the fixed costs per transaction (legal fees, KYC, SPV setup, placement fees) make them unviable. Therefore, this move by exchanges is a disruptive attempt to break down class barriers. Previously, retail investors (who also needed to be sophisticated players with conditions like US stock accounts) could only participate after an IPO. Now, although exchanges might charge a premium, it at least offers ordinary people a chance to participate.

Broker/FA Chaos

A cross-border Pre-IPO deal typically passes through multiple layers:

Underlying GP - Rep (Seller Representative) - Tier 1 Broker - Tier 2 Broker - … - FA - Client

Each layer adds 1-5% in fees. A deal with a $500B underlying valuation could reach an end buyer priced at over $600B.

Take SpaceX as an example. The real market price might be an ~$1.25T valuation plus a 3-11% access fee (varying by channel and tier), meaning a final price of around $1.375T. This doesn't even include the compliance costs for Tokenization. All things considered, the prices offered by the exchanges seem reasonable, likely a strategy for customer acquisition.

Furthermore, most block supply in the market is fictitious – the same block of shares is listed by multiple brokers. Less than 10% is genuinely executable. For instance, for SpaceX, platforms might list shares at a $1.2T valuation, but upon deeper inquiry, these often turn out to be phantom listings, a common issue even on large platforms and intermediaries.

Sources: A secondary trading platform

Sources: A secondary trading platform

If a transaction involves an LP Interest Swap, you need GP Consent – the consent right of the underlying SPV's GP regarding the transfer of LP interests. The GP has the right to refuse. The industry reality is that GPs dislike such transfers due to the hassle of vetting new LPs, compliance, and onboarding strangers. So, in many cases, you need to pay the GP to facilitate the process, adding another layer of cost.

Illiquidity is the biggest pain point of Pre-IPO secondary shares

Selling mid-way is very difficult. You either wait for the company's IPO (usually 3-7 years), often followed by a 6-month lock-up period, or find another buyer and repeat the structural process – taking 2-3 weeks (at best) plus FA fees.

Each transfer is an independent OTC transaction, requiring new legal documents, KYC/AML/UBO checks, and GP approval. This is why Pre-IPO shares are consistently priced as "illiquid assets."

How Ordinary People Can Participate in This Round of Pre-IPO

One can predict that the market will see a series of secondary share tokenization products. Their essence is the same: the platform buys real existing shares in the traditional Pre-IPO market, then packages them into a tokenized wrapper and sells fractionalized pieces to retail investors.

For ordinary people, it offers an opportunity to enter before a company's IPO, benefiting from the natural valuation increases in subsequent funding rounds.

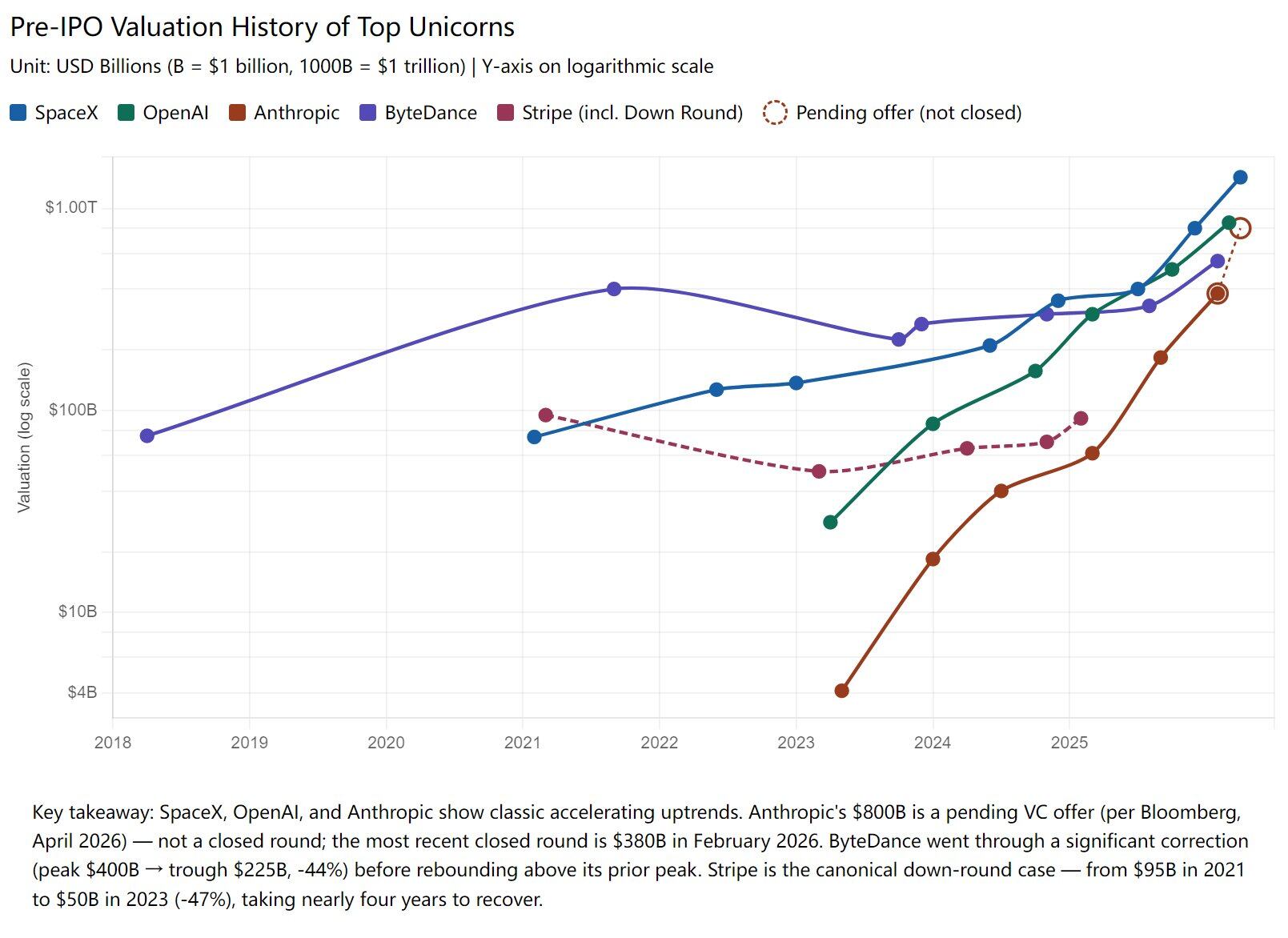

Valuations of top-tier targets typically rise monotonically from round to round. SpaceX grew from a $74B valuation in 2021 to over $1.4T+ today, OpenAI from $29B to $852B+, Anthropic from $4B to $800B+, and ByteDance from $75B to $600B+. Each new funding round pushes the valuation higher, benefiting existing shareholders.

However, it's crucial to understand this is not a guaranteed profit. Historically, Stripe saw its valuation halve from $95B to $50B in a down round. TrueLayer dropped 30%, Cybereason fell 90%, and WeWork went from a $49B valuation to bankruptcy. In 2023, 128 unicorns globally saw their valuations decline, with 42 falling out of the unicorn club entirely.

So, the key to participating in Pre-IPO is selecting the right asset, not timing the market. Profit comes from long-term gains alongside the company's natural valuation appreciation – not from rushing in at launch hoping for short-term sentiment-driven pumps. Many crypto users treat Pre-IPO like a crypto IDO, but these are two fundamentally different logics.

Here's a summary of the participation logic:

First, are you bullish on this asset for the long term? Does SpaceX/OpenAI/Anthropic justify their post-IPO valuation levels? Are you willing to hold until the next funding round or after the IPO?

Second, is the chosen product safe? Who is the issuer? Where is the guarantee/recourse? Who do you claim against if something goes wrong?

RWA Landscape in the Next 3 Years

The RWA-ification of Pre-IPO is still in its very early stages. Supply of top-tier assets is scarce, demand is highly concentrated, and valuations are trending upward long-term. In the coming months, tokenized products for leading names like OpenAI, Anthropic, xAI, Stripe, ByteDance, and Kimi will emerge one after another.

This is just a small branch of the broader Tokenization trend. We can now clearly foresee a four-layer structure for the main narrative:

- Stablecoin Issuers: Providing the on-ramp for on-chain dollars and settlement.

- Public Chain Networks: Hosting the issuance and transfer of assets.

- Trading & Distribution Platforms: CEXs and DEXs. We also see strong potential in LaunchPad / IDO platforms (like Buidlpad, etc.). They already possess the full suite of capabilities for new asset KYC, issuance, subscription, and distribution. Previously used for crypto tokens, today they can be readily used for Pre-IPO tokens.

- Asset Issuance Service Providers: Companies specializing in bringing various types of assets onto the blockchain.

It is foreseeable that the Tokenization narrative will not just create a handful of unicorns but has the potential to nurture new trillion-dollar infrastructure and a group of hundred-billion-dollar platform-level players.

This is just the beginning.