MSTR STRC Deep Dive: The BTC Funding Flywheel Behind the 11.5% Yield

- Core Thesis: STRC is a sophisticated financing tool that converts fixed-income demand into Bitcoin buying pressure, offering an 11.5% floating yield in a bull market. However, its risk profile is essentially a "sold put option" on Bitcoin's asset coverage. Its fragility lies in the mNAV dropping below 1.0x, potentially triggering a downward spiral, with a probability of approximately 70% in the second half of 2026.

- Key Elements:

- STRC has a notional size of $5B and has provided Strategy with over $3.5B in BTC purchasing capital since its launch. Its stability relies on investor confidence and consecutive dividend auctions, not collateral support.

- The risk trigger path has three stages: A BTC decline breaking the $100 anchor, the dividend hike trap (currently raised from 9% to 11.5%), and the flywheel breaking when mNAV falls below 1x, forcing Strategy to choose between adding positions or abandoning its stable narrative.

- The simultaneous occurrence in April 2026 of the first pause in dividend increases (a bullish signal) and the reduction of MSTR ATM issuance to zero indicates that mNAV had compressed to near 1.0x, partially disabling the flywheel.

- STRC's liquidation priority is lower than that of the $8.2B convertible bonds and STR F preferred shares. If BTC drops by more than 50%, its asset buffer would significantly thin.

- NYDIG describes its risk as "shorting a put option on Bitcoin asset coverage," while the core disagreement among analysts is: bulls view it as a safe yield instrument, while bears see it as mispriced credit risk.

Original Author: Benji

Original Source: IOSG Ventures

Core Thesis: STRC is an ingeniously designed financing tool that converts fixed-income demand into buying pressure for Bitcoin. In a bull market, it offers 11.5% floating yield with relatively low price volatility. However, its risk structure is essentially equivalent to "selling a put option" on Bitcoin's asset coverage ratio. Therefore, when BTC declines, it cannot substitute for genuine fixed-income products.

STRC's true vulnerability is not the BTC price itself, but mNAV. Once MSTR's mNAV breaks below 1.0x for more than four consecutive weeks, the flywheel enters a passive-mode downward spiral within three months. We estimate a ~70% probability of this trigger occurring in the second half of 2026, at which point STRC would present a buyable entry point of $85 – $90. If the trigger is not activated, it would mean that Saylor has successfully created a brand-new category of BTC-native credit instruments.

Background

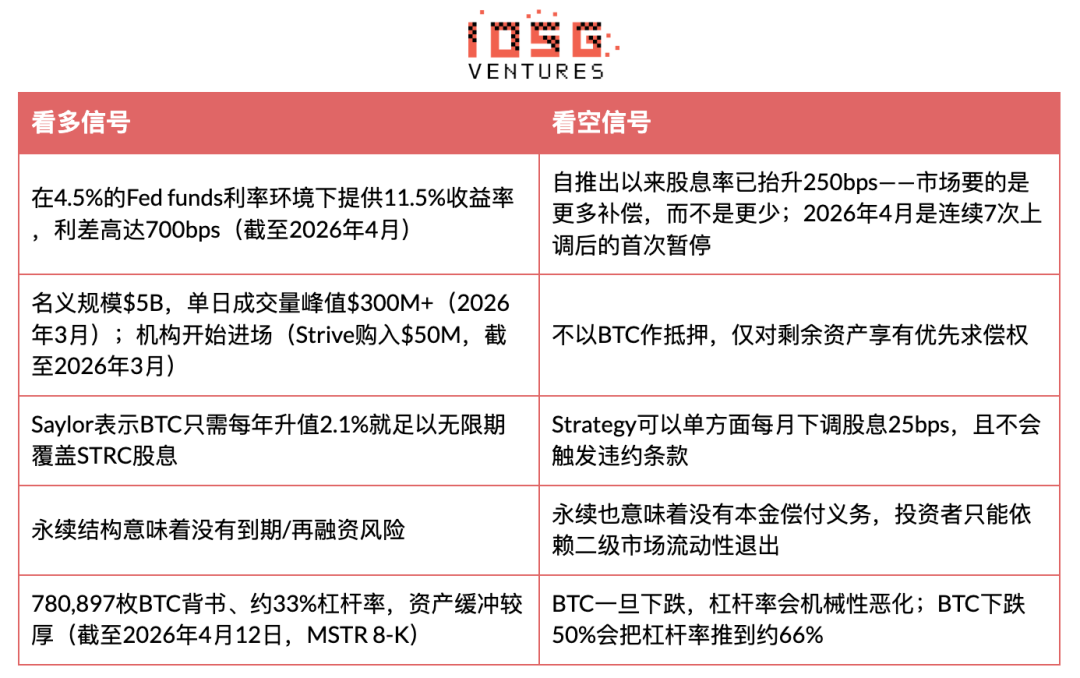

Strategy (formerly MicroStrategy) launched STRC ("Stretch"), a perpetual preferred stock with a target par value of $100, stabilized by monthly floating dividends. As of March 31, 2026, STRC had a nominal size of $5B, with peak daily trading volume exceeding $300M (as of March 2026 data). Since inception, it has provided Strategy with over $3.5B in BTC purchasing capital, making it the company's most important current funding vehicle. As of April 12, 2026, Strategy's balance sheet held 780,897 BTC, with a leverage ratio of 33%, and approximately $21.6B remaining issuance capacity under the STRC ATM program.

This instrument occupies a novel category: it resembles a money market fund (stable price, high yield) but carries credit risk derived entirely from a single company's BTC holdings.

Before elaborating on our argument, let's clarify "where we could be wrong."

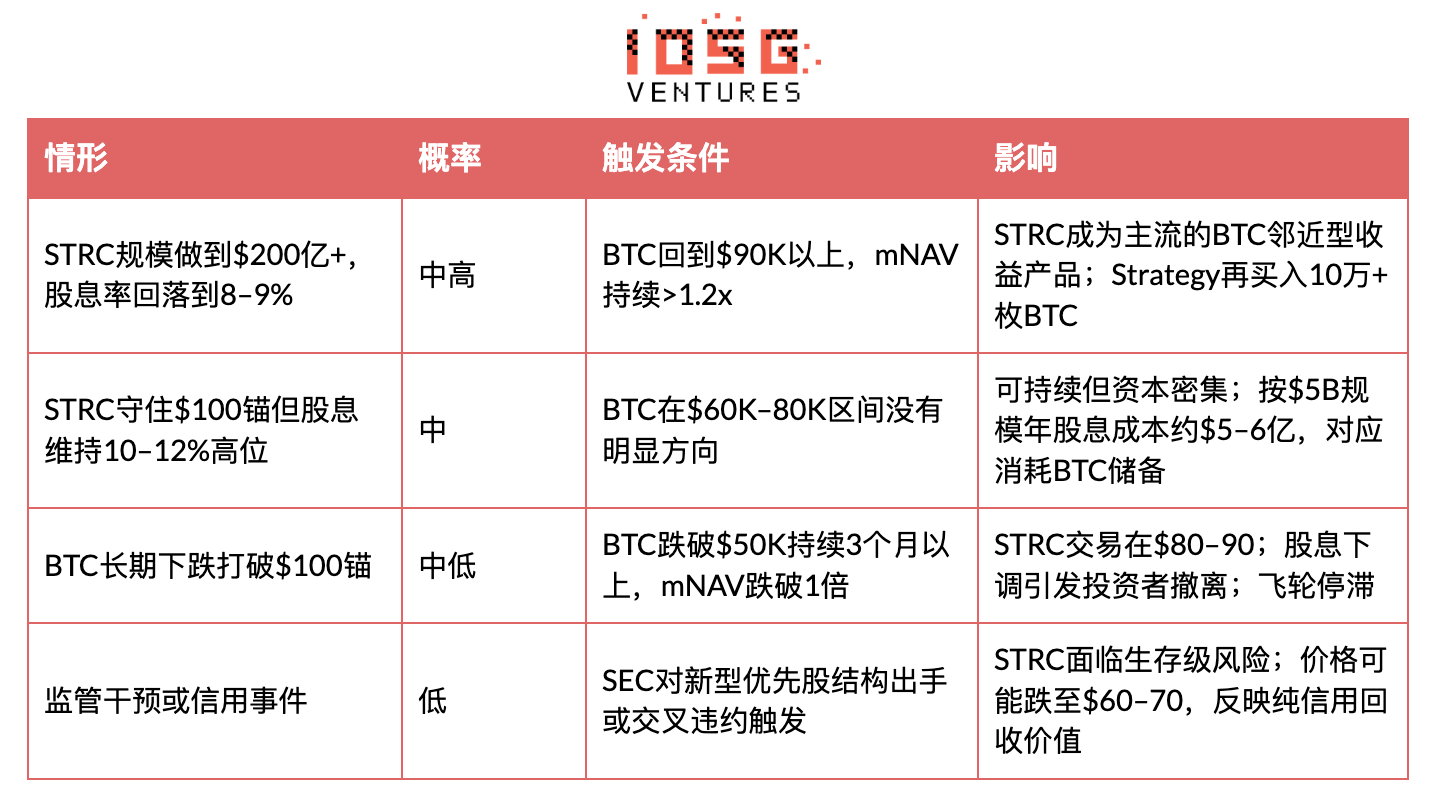

If our analysis is wrong, it would be because: traditional fixed-income allocators are genuinely willing to accept reflexive risk for a 700bps spread; STRC scales to $50B within 3 years, becoming the de facto BTC yield curve; Saylor successfully securitizes BTC into an interest-bearing collateral asset acceptable within institutional portfolios. This outcome would represent the largest integration of crypto into traditional finance to date—a $50B+ asset class that simply did not exist before 2025.

In this optimistic scenario, the dividend pause in April 2026 is not a warning signal but a feature: a maturing instrument stabilizing yields after initial price discovery, similar to how early high-yield bond ETFs gradually repriced downward with institutional adoption.

Thesis Deconstruction

STRC's core innovation: it converts yield-seeking capital into buying pressure for BTC. When STRC trades near $100, Saylor uses ATM issuance (approximately 40% of daily volume) to purchase BTC with the proceeds, then issues MSTR common stock at a premium to NAV (mNAV>1x) to deleverage. The net result is that $100M in STRC daily volume can catalyze approximately $120M in BTC purchases.

However, the fragility of this mechanism lies in its inherent circularity: STRC stabilizes at $100 because investors believe it can stabilize; Saylor maintains this belief by continuously raising dividends. This anchor is not backed by collateral, but by confidence, sustained through a continuous dividend auction with no formal upper limit. Once this confidence breaks, the auction becomes increasingly expensive.

Evidence and Comparison: STRC vs. Other Bitcoin Exposure Vehicles

Key Insight: For Strategy, STRC converts fixed-income demand into fuel for BTC accumulation. For investors, it offers Sharpe-optimized returns in a benign environment but conceals a BTC "put sale." NYDIG's description is precise: "It is akin to shorting a put option on Bitcoin's asset coverage ratio — earning yield in exchange for assuming the downside risk of BTC declines eroding the asset buffer."

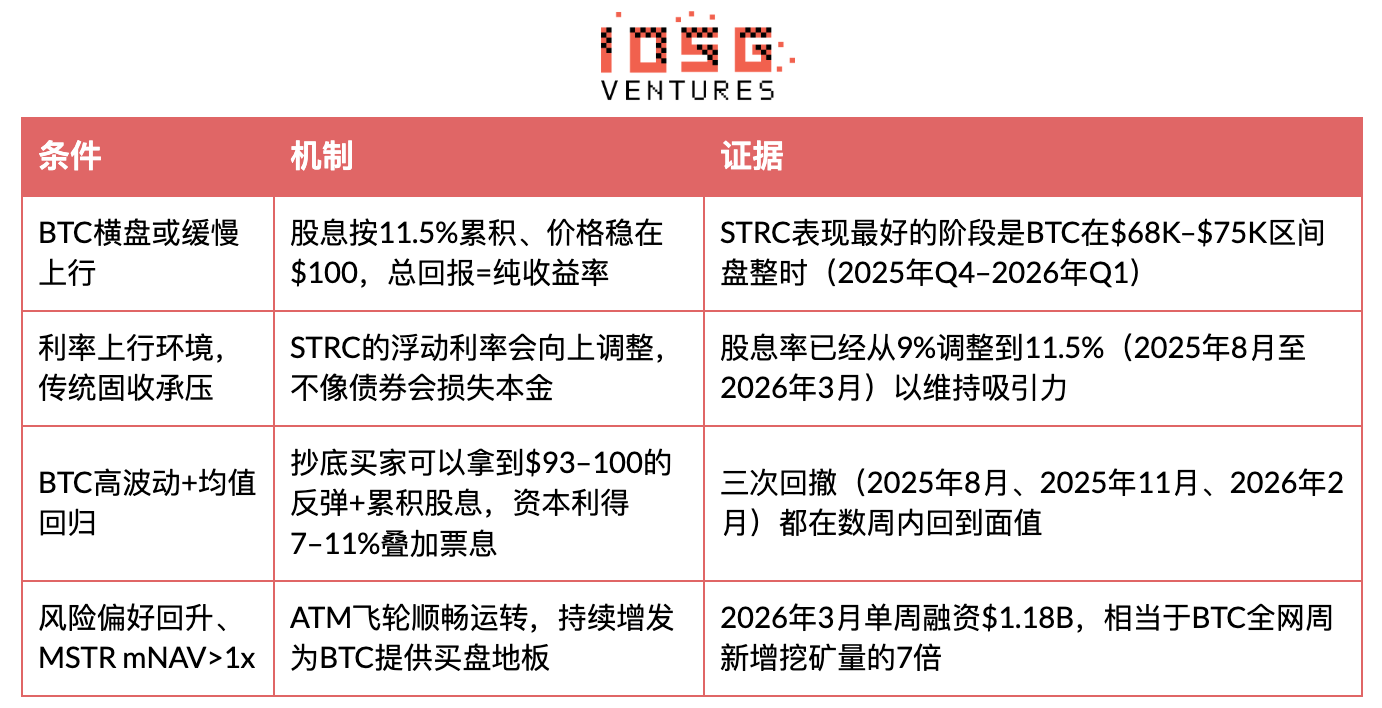

When STRC Performs Well

When STRC Performs Poorly

When STRC Could Collapse: The Death Spiral Scenario

The key question: Can STRC enter a self-reinforcing downward cycle? The answer is yes, but under specific conditions. The mechanism involves three interconnected failure paths.

Phase 1: BTC Decline Breaks the $100 Anchor

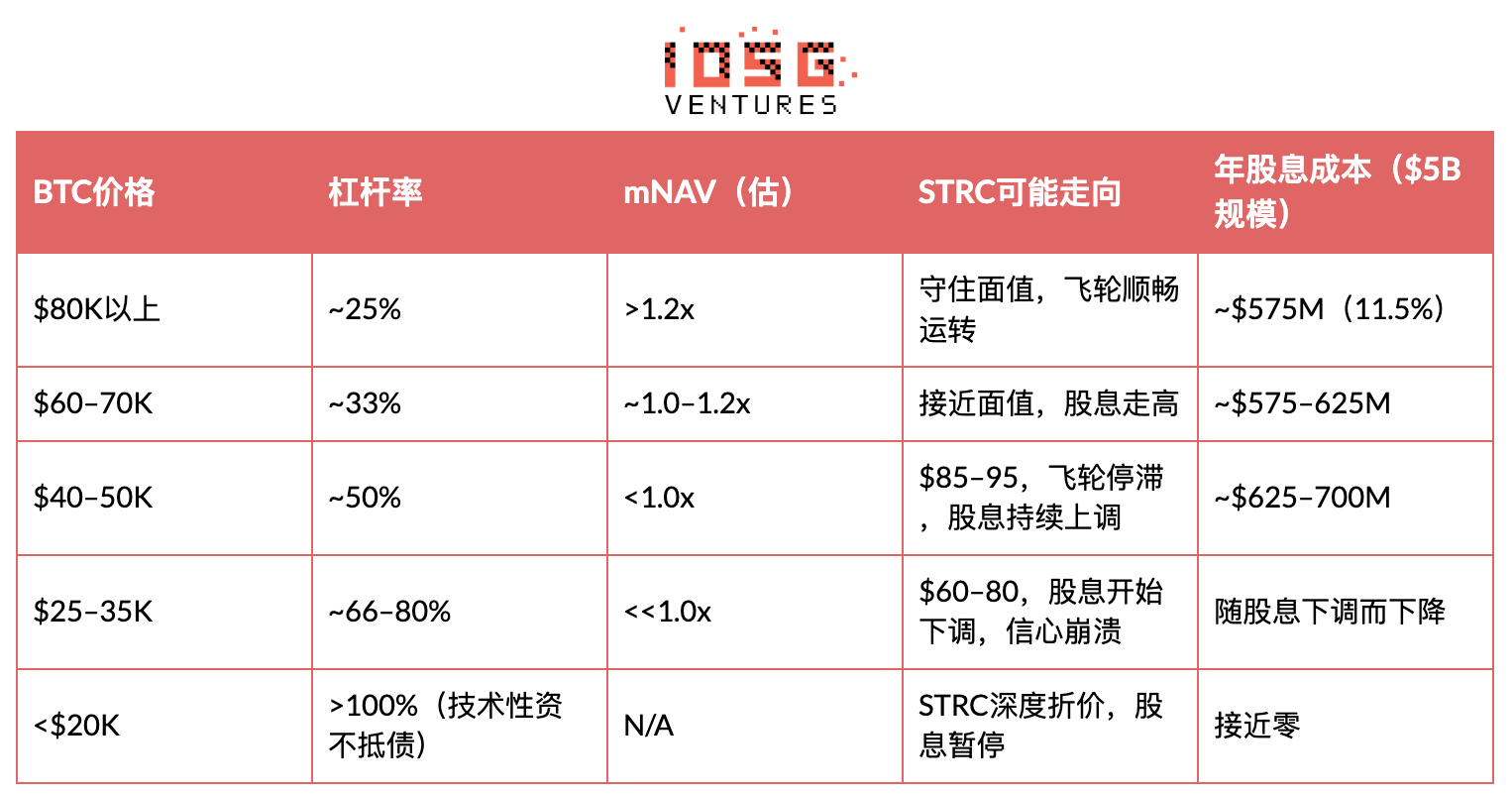

During a sharp BTC decline (e.g., the ~45% retracement from all-time highs in late 2025), Strategy's leverage ratio mechanically increases. Based on 780,897 BTC and 33% leverage (as of April 12, 2026, MSTR 8-K), a further 50% drop in BTC would push the leverage ratio to approximately 66%. At this point, STRC's credit quality deteriorates as its priority claim on remaining assets thins. The price breaks below $100. This scenario has occurred three times (August 2025: ~$92, November 2025: intraday low, February 2026: ~$93), but each time BTC rebounded quickly, pulling the anchor back.

Phase 2: The Dividend Hike Trap

According to Strategy's SEC guidance: if the monthly VWAP is between $95–$99, the dividend rate increases by 25bps per month; if it falls below $95, the increase is 50bps per month. From 9% to 11.5%, the dividend rate has cumulatively risen 250bps over approximately 8 months (August 2025 to April 2026), averaging ~31bps per month—a pace faster than any comparable company's preferred stock repricing in stable market conditions. April 2026 marked the first pause after seven consecutive increases. Two interpretations: (a) demand stabilizes—bullish; (b) Strategy has hit the yield sensitivity ceiling of traditional fixed-income buyers—bearish. This is the single most important signal to track over the next 1–2 months.

If BTC remains depressed, dividends must continue rising to attract buyers back near par value. At a $5B scale, every 100bps increase represents approximately $50M in additional annual cash expenditure; if STRC expands to $20B (authorized ATM capacity), the cost per 100bps becomes $200M annually. A bear market persisting for over six months at the current rate of increase would push STRC's yield towards 13–15%; at this level, the annual dividend expense for a $20B scale would exceed $2.6–3 billion, consuming a significant portion of Strategy's BTC reserve potential, forcing a choice between "continue raising" and "abandon the stable narrative."

There is no formal upper limit on dividend increases. This "no cap" dynamic is precisely what bears focus on.

Phase 3: Flywheel Breaks as mNAV Drops Below 1x

This is the true breaking point. Strategy relies on issuing MSTR common stock at a premium to NAV (mNAV>1x) to purchase BTC and deleverage. If BTC falls deeply enough and mNAV drops below 1x, issuing common stock would dilute existing shareholder value, preventing Saylor from deleveraging through issuance. At this point, Strategy faces a trilemma: (a) continue issuing STRC at higher dividend rates, accepting higher leverage; (b) unilaterally cut dividends (25bps per month) per SEC filing terms, allowing STRC price to fall; (c) sell BTC into a declining market.

Saylor has repeatedly stated he will never sell BTC. BitMEX Research concludes (b) is most likely: "Strategy won't sell Bitcoin; it will simply abandon STRC's pursuit of stability." All pressure would transfer to STRC holders.

An early warning signal has already flashed: during the week of April 6–12, 2026, MSTR's ATM mechanism issued $0—all funding was completed via STRC ($1.00B, 10.028 million shares; MSTR 8-K). mNAV is already too tight for Saylor to risk diluting common stock. The preconditions for Phase 3 are partially triggered—the flywheel is already running on one leg.

Quantifying the Crash Scenario

Why this is different from UST/Terra: UST relied on an algorithmic mint-burn mechanism, with the only support being an endogenous token (LUNA). STRC is backed by real BTC, and Strategy has the discretion to choose dividend cuts over forced liquidation. STRC's floor is not zero—it's its priority claim on residual assets in bankruptcy liquidation. However, if BTC falls over 60% and stays low, this floor could be far below $100.

The key variable is time. Every previous STRC drawdown was repaired within weeks because BTC rebounded. A genuine crash requires a sustained bear market (over 3 months below $50K), allowing the dividend hike mechanism to run long enough to erode confidence. The longer STRC stays below par with continuously rising dividends, the more it resembles a company rolling over increasingly fragile debt at higher and higher rates—a pattern with a well-defined outcome in credit markets.

Capital Structure Priority: Liquidation order is: Convertible Bonds (~$8.2B) → STRF → STRC → STRK → STRD → MSTR Common Stock. STRC sits behind $8.2B of unsecured debt and STR F preferred stock.

Industry Perspectives

"STRC's risk is significantly higher than short-duration Treasuries... When the music stops, investors might feel somewhat offended." – BitMEX Research, *A Bit of a Stretch* (November 2025)

"The appropriate way to assess STRC risk is from the perspective of governance and subordination, not just payment risk." – Greg Cipolaro, Head of Global Research, NYDIG (March 2026)

"It is akin to shorting a put option on Bitcoin's asset coverage ratio — earning yield in exchange for assuming the downside risk of BTC declines eroding the asset buffer." – NYDIG Research Report (March 2026)

The core disagreement among analysts lies here: Bulls view STRC as the safest way to earn 11.5% in the current market; Bears view it as mispriced credit risk packaged as a money market product. The bears' core concern directly maps to the dividend hike mechanism described above: STRC won't suddenly default, but slowly reprice—the longer BTC stays weak, the more it slides from a quasi-money market instrument into a distressed yield product. This gradual erosion is the real risk, not an overnight crash.

Inferences and Predictions

Bottom Line: STRC is a genuinely novel financial instrument that performs beautifully in the environment for which it was designed—BTC steadily rising, open capital markets, mNAV>1x. In this state, it offers an attractive 11.5% yield with manageable volatility. However, its downside structure is asymmetric: earn coupons in good times, bear concentrated, single-name BTC credit risk in bad times. It is not a substitute for Treasuries or diversified high-yield bonds, but a leveraged bet on the continued operation of Strategy's BTC accumulation flywheel—packaged to look like fixed income.

Three New Signals (As of April 2026)

Signal 1: First Pause in Dividend Hikes in April (As of April 1, 2026, CoinDesk).

After seven consecutive increases from August 2025 to March 2026 (from 9% to 11.5%), Saylor kept the dividend rate unchanged in April. Two interpretations: (a) demand stabilizes at this yield level—bullish; (b) Strategy hits the yield sensitivity ceiling of traditional fixed-income buyers—bearish. This is the single most important signal to track in May-June and the inflection point around which the mNAV trigger framework revolves.

Signal 2: MSTR ATM Issuance was $0 in the Week of April 6-12, All Funding via STRC ($1.00B; MSTR 8-K, April 2026).

At current BTC price levels, mNAV is already too tight for Saylor to risk diluting common stock by issuing MSTR. The preconditions for Phase 3 of the death spiral are partially triggered—the flywheel is running on one leg.

Signal 3: Last Week's Average BTC Purchase Price was $71,902/coin, Below Strategy's Historical Cost of $75,577/coin (As of April 12, 2026, MSTR 8-K)

Strategy is DCA buying into a weak market. The flywheel is still turning, but each marginal purchase is thinning the asset buffer rather than thickening it—the opposite dynamic of the 2024-2025 accumulation cycle.

Investment Advice

HOLD, wait for a better entry point and BTC upside.

Current Status: HOLD existing positions; do not add without better signals. MSTR's mNAV has compressed to near 1.0x. STRC still holds at the $100 par value and pays 11.5%, indicating the dividend mechanism is functioning as designed. But the margin of safety is very thin.

Conditions for Re-entry: BTC establishes above $70-75K, and MSTR mNAV confirms above 1.1x for two consecutive weeks. At that point, STRC returning to near its $100 par value enters the conditional buying zone. Historically, buying below $95 combined with a subsequent BTC rebound has delivered 7-11% capital gains plus accumulated dividends—but this only occurs in environments where BTC rebounds within weeks (August 2025, November 2025, February 2026). Whether the current drawdown continues this pattern or foreshadows a more persistent bear market is the true unknown.

Exit Signals: Initiate sell evaluation upon any of the following: (a) MSTR mNAV breaks below 1.0x and remains there for over two weeks; (b) STRC VWAP remains below $95 for four consecutive weeks; (c) BTC breaks below $55K on volume.

Appendix

Timeline

Concentration of Holdings—Who Could Forcefully Break the Price?

Strive's $50M purchase was mentioned, but there is no discussion of whether STRC has a few large institutional holders—if they were to rotate out simultaneously, could they overwhelm the average daily volume of $258M and push STRC below par value in a self-fulfilling manner? This is the "run" risk.