500 Dollars to Become a Silicon Valley 'Shareholder'? Unpacking Naval's New Fund, USVC

- Core Thesis: Renowned Silicon Valley angel investor Naval Ravikant has launched the USVC fund, opening up shares of top Silicon Valley companies like OpenAI and SpaceX to non-accredited investors with a minimum entry of $500. However, the fund is actually an FOF (Fund of Funds) with a complex fee structure, holding a relatively small underlying asset pool with liquidity constraints. This has led some critics to question whether it represents a "distribution of risk" rather than pure "financial democratization."

- Key Elements:

- By registering as a closed-end fund under the Investment Company Act of 1940, USVC bypasses the regulatory requirement limiting investments to "accredited investors," opening the door for the general public to invest with a low barrier of just $500.

- The fund structure is an evergreen closed-end fund with no fixed term. Shares are not traded on secondary markets; liquidity is primarily provided through quarterly repurchases (capped at 5% of net asset value), but these repurchases are at the Board's "sole discretion" and are not an obligation.

- The investment strategy follows three paths: acting as an LP in emerging fund managers on the AngelList platform (primarily for early-stage exposure), participating in growth-stage rounds, and buying secondary shares. Essentially, it operates as an Fund of Funds.

- The fee structure is complex: while it advertises a "1% management fee with no performance fee," the actual net expense ratio includes underlying fund fees. During a fee waiver period, this is approximately 2.50%, but upon expiration of the waivers, it rises to 3.61%.

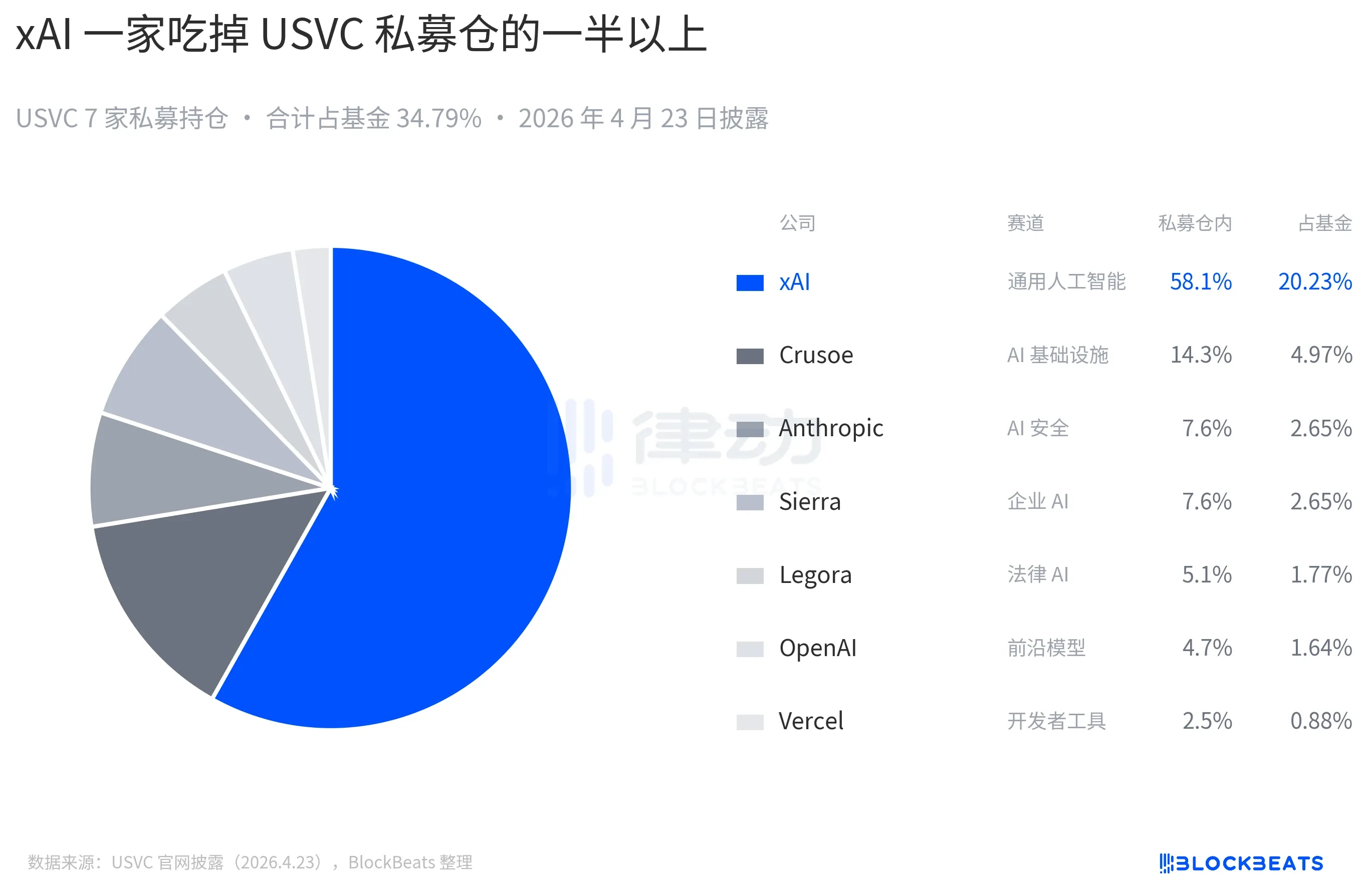

- As of December 31, 2025, USVC's total fund size was only $8.3 million, of which 56% (approximately $4.65 million) was invested in a government money market fund yielding 3.66%, creating a stark contrast with the advertised portfolio of star holdings.

- Market commentary suggests that the launch of USVC comes at a time when the valuations of several private companies (such as OpenAI, xAI) have already appreciated significantly. Furthermore, cases like Figma and Klarna indicate that private market valuations may be inflated. This suggests the fund may be "distributing" positions that have already seen their primary gains rather than providing early-stage entry opportunities.

Naval, the most famous angel investor in Silicon Valley, has just launched a new fund. Unlike the over 400 companies he has personally invested in before (including Uber, Twitter, and Notion), this time, you can invest too.

You don't need to be a millionaire. You don't need connections. You don't need "accredited investor" certification as defined by U.S. securities law. Starting with $500, you can simultaneously buy shares in OpenAI, Anthropic, xAI, and SpaceX.

The fund is named USVC (United States Venture Capital), built by AngelList, with Naval himself serving as Chairman of the Investment Committee. Last night, after its launch, AngelList's announcement tweet garnered 2.75 million views, and Naval's long thread received 2.25 million views. They gave the fund a grand tagline: "The Endowment Fund for the American People."

It sounds like a complete democratization of finance. But beneath the surface of this basket, the contents are far more complex than the marketing slogans suggest.

Buying into a Top-Tier Silicon Valley Portfolio for $500

The long thread announcing the launch was penned by Naval himself, in his classic style: short sentences, aphorisms, historical analogies. He started with the Age of Exploration in the 1500s, then presented a comparison: the median age of U.S. companies going public in 1980 (6 years old) versus today (13 years old). This implied that the growth retail investors used to capture in public markets is now largely locked away in private markets.

The entire thread culminated in a somewhat fatalistic aphorism: "In the future, you either tell the computer what to do, or the computer tells you what to do. You don't want to be on the wrong side of that trade." The narrative is beautifully crafted, like one of the last serious prospectus advertisements ever written in Silicon Valley.

For decades, a hard rule in the U.S. private market has been the "accredited investor" standard, effectively barring the vast majority of ordinary people from venture capital investments.

USVC bypasses this barrier by registering itself as a closed-end fund under the Investment Company Act of 1940. This is the same law governing U.S. mutual funds and ETFs. By registering, the fund must adhere to standardized audits and regular financial reporting. In return, it can open its doors to everyone, bypassing accredited investor checks, and issues 1099 tax forms annually, which are far friendlier for individual investors than the K-1 forms common in private equity.

A number appears repeatedly in USVC's promotional materials: $125 billion. This is the cumulative assets currently held on the AngelList platform. Co-founded by Naval in 2010, AngelList has become a foundational infrastructure for U.S. private investment, hosting over 4,500 fund managers, operating more than 25,000 funds, and supporting over 13,000 active startups.

USVC's GP, Ankur Nagpal, framed this in his announcement thread as "our unfair advantage." In other words, USVC's stock-picking ability doesn't come solely from the judgment of Naval or Ankur, but from using AngelList's data flow and manager network as a screening tool.

Ankur Nagpal handles USVC's day-to-day management. He is the founder of the online education platform Teachable, currently USVC's GP, and also the founding GP of Vibe Capital, an emerging fund within AngelList. Naval's role at USVC is Chairman of the Investment Committee, responsible for shaping investment strategy but not day-to-day decisions.

The advisory board also includes several familiar faces from Silicon Valley: Cyan Banister (former partner at Founders Fund), Arielle Zuckerberg (formerly invested at hedge fund Coatue and Kleiner Perkins), and Jeff Fagnan (founder of Accomplice, an early investor in Carbon Black, PillPack, and Whoop). This list itself is a signal from USVC to retail investors: We are not a hastily assembled retail product; behind us is an entire mature venture capital circle.

Lifting the Lid: What's Inside USVC?

Structurally, USVC is different from common ETFs or mutual funds. It is an evergreen closed-end fund with no fixed term, and its shares are not traded on secondary markets. Compared to traditional VC funds, it lacks a 10 to 15-year lock-up period. Compared to ETFs, its shares are not listed on any exchange, and its price doesn't fluctuate with secondary market sentiment but tracks the fair value of underlying companies.

This structure can yield a "sounds reasonable" return profile. It won't be tossed around by daily secondary market sentiment like a publicly traded ETF, nor will it lock your money away for a decade like an old-school VC fund.

According to official disclosures, USVC's investment strategy after fundraising follows three paths:

First, investing in other fund managers. USVC acts as an LP, allocating capital to emerging fund managers it favors on the AngelList platform. This is USVC's primary route to gaining early-stage exposure.

Second, participating in growth rounds. When a company in the portfolio starts to succeed, USVC attempts to increase its position in subsequent rounds to avoid dilution of its stake as the company continues to raise capital.

Third, acquiring secondary shares. USVC uses the AngelList network to buy shares of private companies with existing traction directly from current shareholders.

These three paths have a hidden implication: USVC is essentially more like a fund of funds (FOF) than a direct investment fund. Most of its money doesn't go directly onto the shareholder registries of OpenAI or Anthropic; instead, it first goes to other fund managers, who then make the investments.

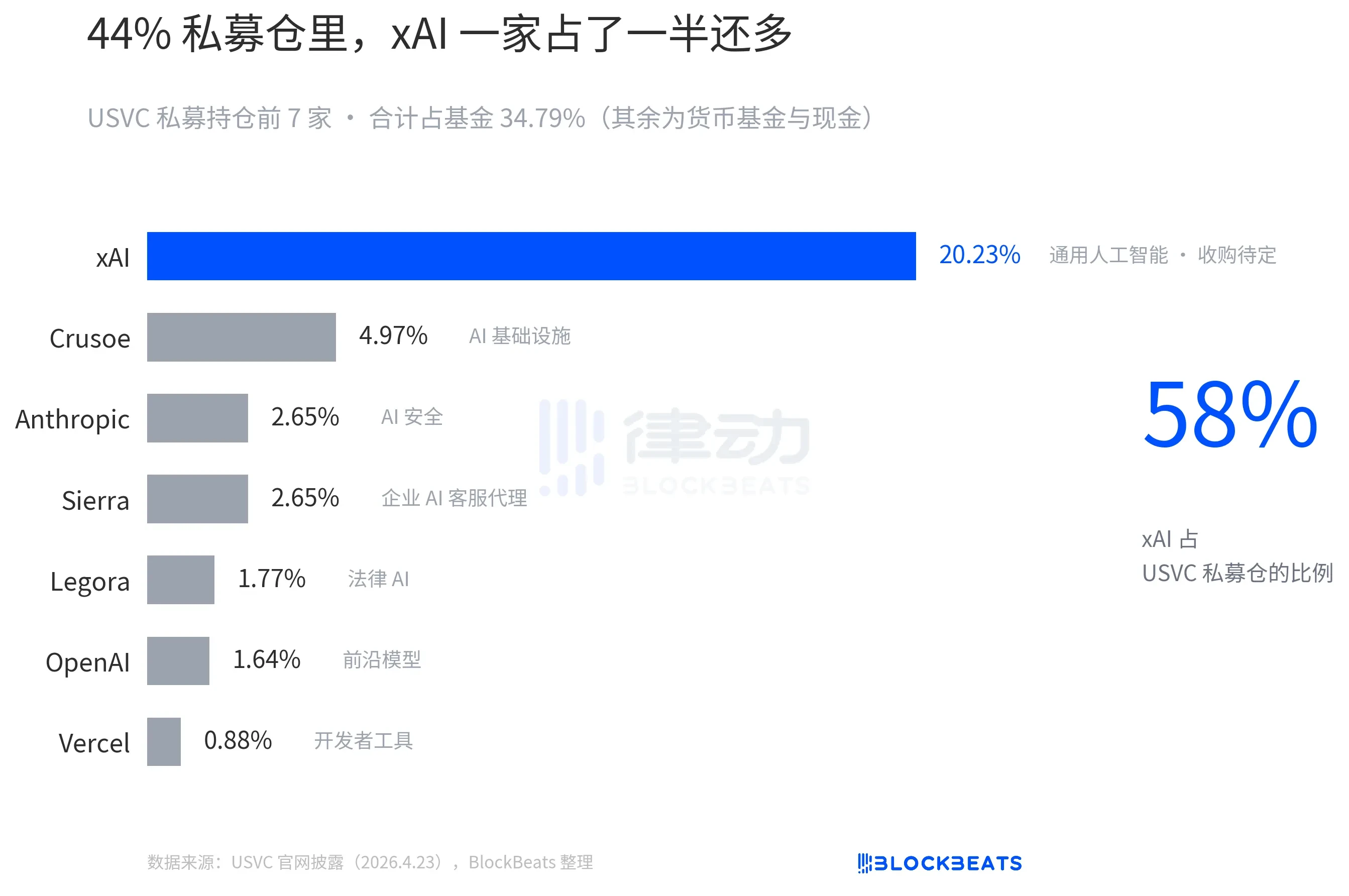

USVC's website currently discloses its holdings, including OpenAI and Anthropic, but the largest allocation is to xAI:

Since USVC shares aren't listed on any national securities exchange, you might ask: How do investors get their money back? The answer is a quarterly repurchase offer. The fund has the discretion to initiate a repurchase each quarter, up to 5% of the fund's net asset value. However, this is a board "discretionary power," not a contractual obligation. This is a middle ground—worse than an ETF but better than traditional VC. For the reader, this means if you urgently need cash someday, USVC shares are essentially illiquid.

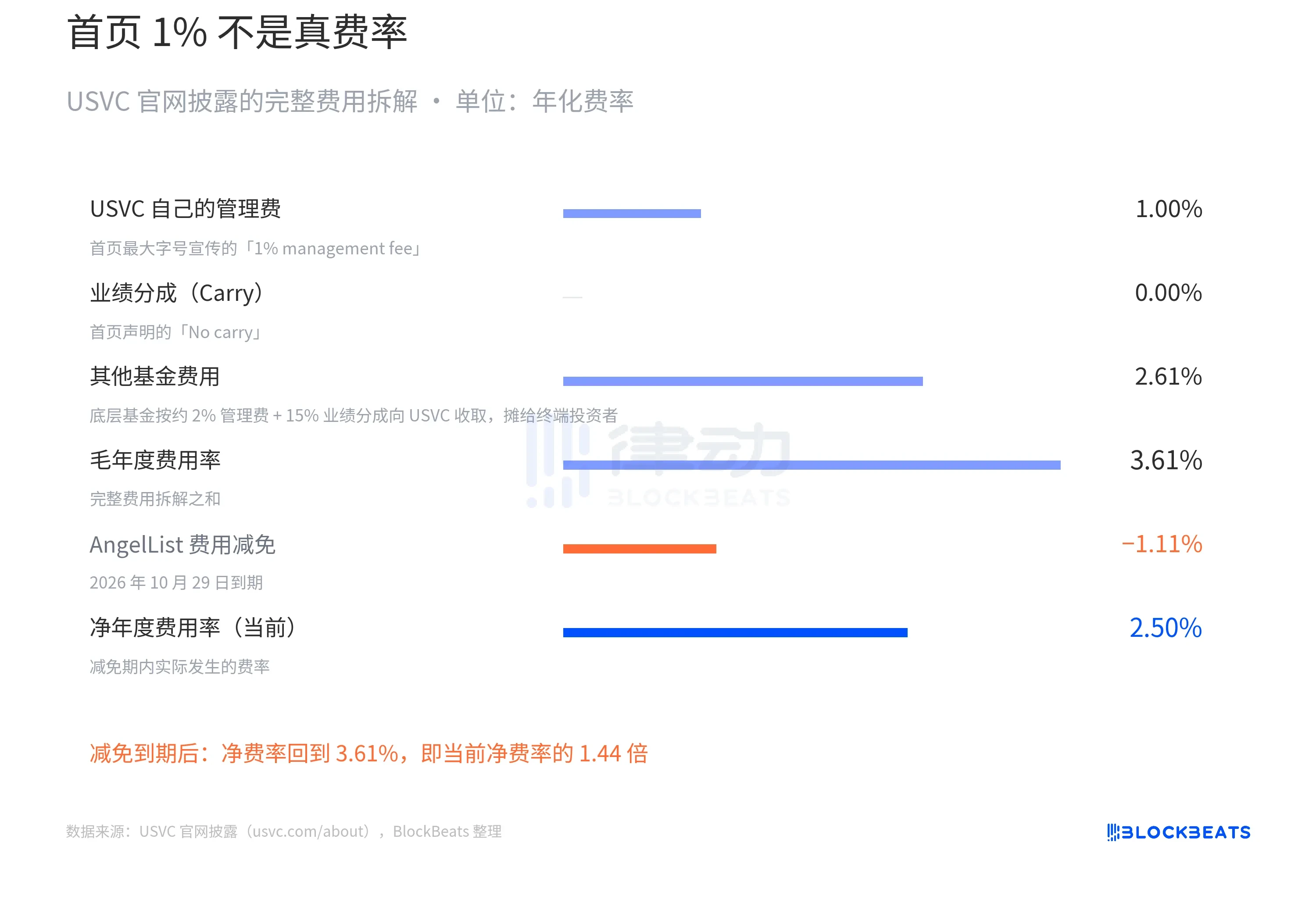

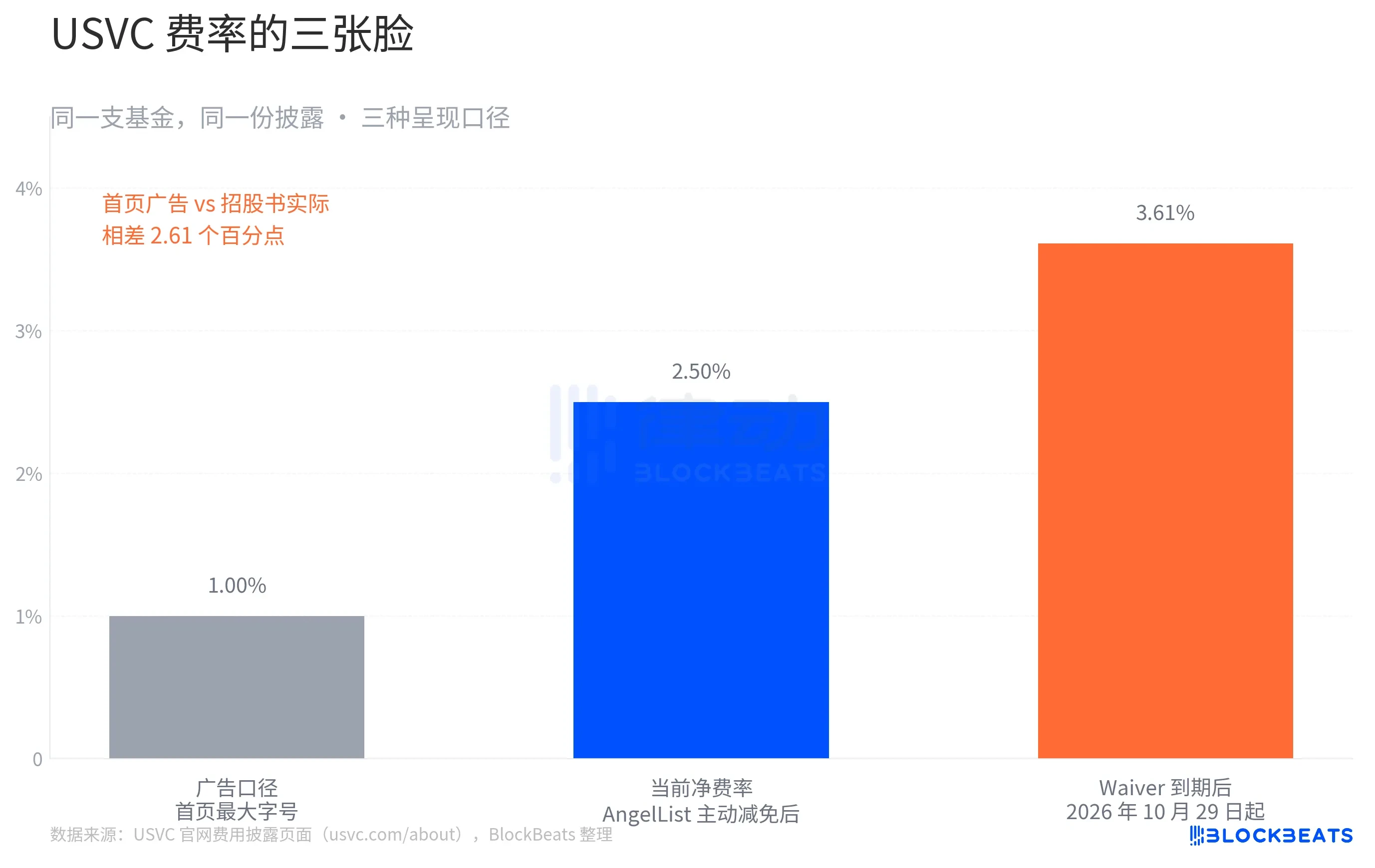

The most detail-worthy aspect of the entire USVC story is its fee structure. At the top of the homepage, USVC states in the largest font: "1% management fee, no performance fee," conveniently using the traditional VC's 2% management fee as a comparison.

This is USVC's public face. Scroll to the fee schedule at the bottom of the same page, and the story changes. USVC's full fee breakdown is as follows:

What is "Other Fund Fees 2.61%"? This relates to the first of USVC's three investment paths – investing money in other emerging fund managers. Those managers themselves charge USVC a 2% management fee and a 20% performance fee. USVC bears these costs as an LP, which are ultimately passed on to the end investor.

Thus, USVC's net expense ratio is actually around 2.50%. And this isn't the final state. The website also includes a crucial limitation: AngelList has agreed to waive some fees and cover certain operating expenses, with the waiver period lasting at least until October 29, 2026. However, once the waiver expires, the fee jumps to 3.61%.

Let's assume the underlying portfolio generates a 12% annual gross return, aligning with the median level of top-tier VC funds over the past decade. During the waiver period, with a net fee of 2.50%, the investor's net return is approximately 9.5%. After the waiver expires, with the net fee returning to 3.61%, the investor's net return drops to approximately 8.4%.

Compounded over 10 years, an initial $10,000 investment would grow to roughly $24,800 and $22,400, respectively. The difference is $2,400, or 24% of the initial principal.

This isn't a fabricated story. All the numbers are explicitly stated on USVC's website compliance disclosure page. However, for a fund promoting "financial democratization," this disparity is worth highlighting.

Beyond the Narrative: Is This Truly 'Democratized Investing'?

Aakash Gupta, a well-known analyst in the Silicon Valley product circle, directly examined USVC's SEC filings. He found that as of December 31, 2025, USVC's total fund size was only $8.3 million. Furthermore, within that $8.3 million, 56% (approximately $4.65 million) was sitting in a government money market fund yielding 3.66%.

This set of numbers presents a stark contrast to the lineup of seven star companies on the fund's homepage. You see OpenAI, Anthropic, xAI, SpaceX, and you might think your $500 will be proportionally allocated to these companies. However, the reality is that the entire fund's SEC-reportable total size is under $10 million, with over half parked in short-term treasuries.

There are, of course, reasonable explanations. The fund is newly established, and deploying cash takes time. Ankur later mentioned in a tweet that "there is also a pipeline of promising new projects."

Some in the community have criticized USVC as a new "liquidity exit art" by Naval, arguing that USVC isn't about access but a distribution mechanism for distributing positions that have already appreciated. Over the past decade, private market valuations have already captured most of the gains. OpenAI's valuation surged from $86 billion to $500 billion in three years; xAI went from $24 billion to over $200 billion in 18 months. Public markets also offer precedents suggesting private valuations can be excessive: Figma's IPO price was 50% below its private valuation; Klarna's valuation crashed from $46 billion in private markets to $6.7 billion at its IPO. Against this backdrop, packaging these stakes and selling them to retail investors does indeed look more like "distribution."

The 5% quarterly repurchase cap seems friendly in normal market conditions. However, imagine a major market correction in 2027, causing the valuations of USVC's underlying private companies to fall and secondary market trading to dry up. In such a scenario, the board's rational choice would be to skip the quarter's repurchase rather than selling underlying assets at a loss to meet redemption requests.

Kenn Ejima, a Silicon Valley developer and investor, directly commented, suggesting that USVC be seen as a fund with a limited opportunity window, the duration of which depends on how long Naval remains Chairman of the Investment Committee.

The term "democratization" has appeared several times in the financial history of the past century. A repeatedly asked question has been, "What is being democratized – opportunity or risk?". This time, however, the question might need to be: "Are you buying a fund, or a slice of Naval's attention for those few years?"