Has the Starting Gun for SpaceX's IPO Fired Yet? Smart Money in the "Space Sector" Already Jumping the Gun?

- Core View: The anticipation of SpaceX's IPO has ignited the commercial aerospace sector rally, but the deeper logic lies in the industry's shift from a long-term narrative to a "pricable sector" with clear industry chain stratification and verifiable business models. Its value revaluation is supported by multiple factors, including declining launch costs, integration with mainstream themes like AI/defense, and market perception differentiation.

- Key Elements:

- SpaceX's Anchoring Effect: Its potential $75 billion IPO and $1.75 trillion valuation expectation provide a powerful valuation anchor and confidence boost for the entire commercial aerospace sector.

- Industry Chain Coverage and Fundamental Support: The rally shows sector-wide resonance. Related companies like MNTS (on-orbit services), SIDU (defense contracts), PL (remote sensing data) represent substantial progress in core industry chain segments such as in-orbit transportation, defense orders, and data services.

- Cost and Business Model Inflection Point: Reusable rocket technology has significantly reduced launch costs, enabling businesses like satellite constellation deployment and data commercialization to move from experimentation to scale, making profit pathways clear.

- Integration with Mainstream Narratives: Commercial aerospace is deeply integrated with era-defining themes like AI computing power (e.g., NVIDIA's involvement), defense needs, and communication networks, enhancing its strategic value and attracting capital attention.

- Market Pricing Becoming More Rational: Differentiation is emerging within the sector. Investors are beginning to price companies in layers based on their specific business models (e.g., satellite platforms, data services, defense qualifications) rather than speculative hype.

- Key Variables to Watch Going Forward: The sustainability of the rally depends on substantial progress in SpaceX's IPO, the flow of specific contracts under the US defense space budget, and the cash reserves and financing actions of individual companies.

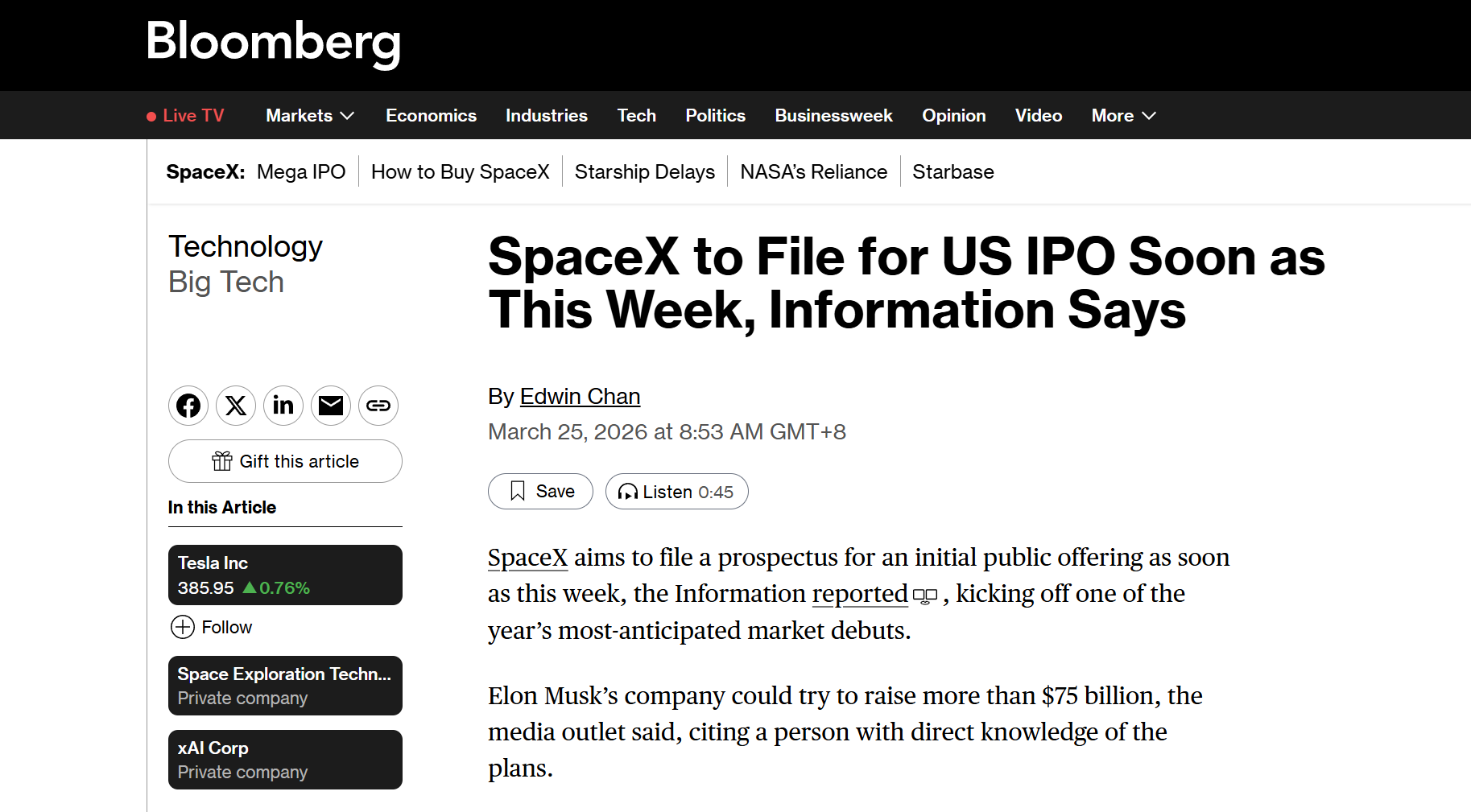

The most anticipated unicorn IPO in the U.S. stock market this year seems to be just one step away.

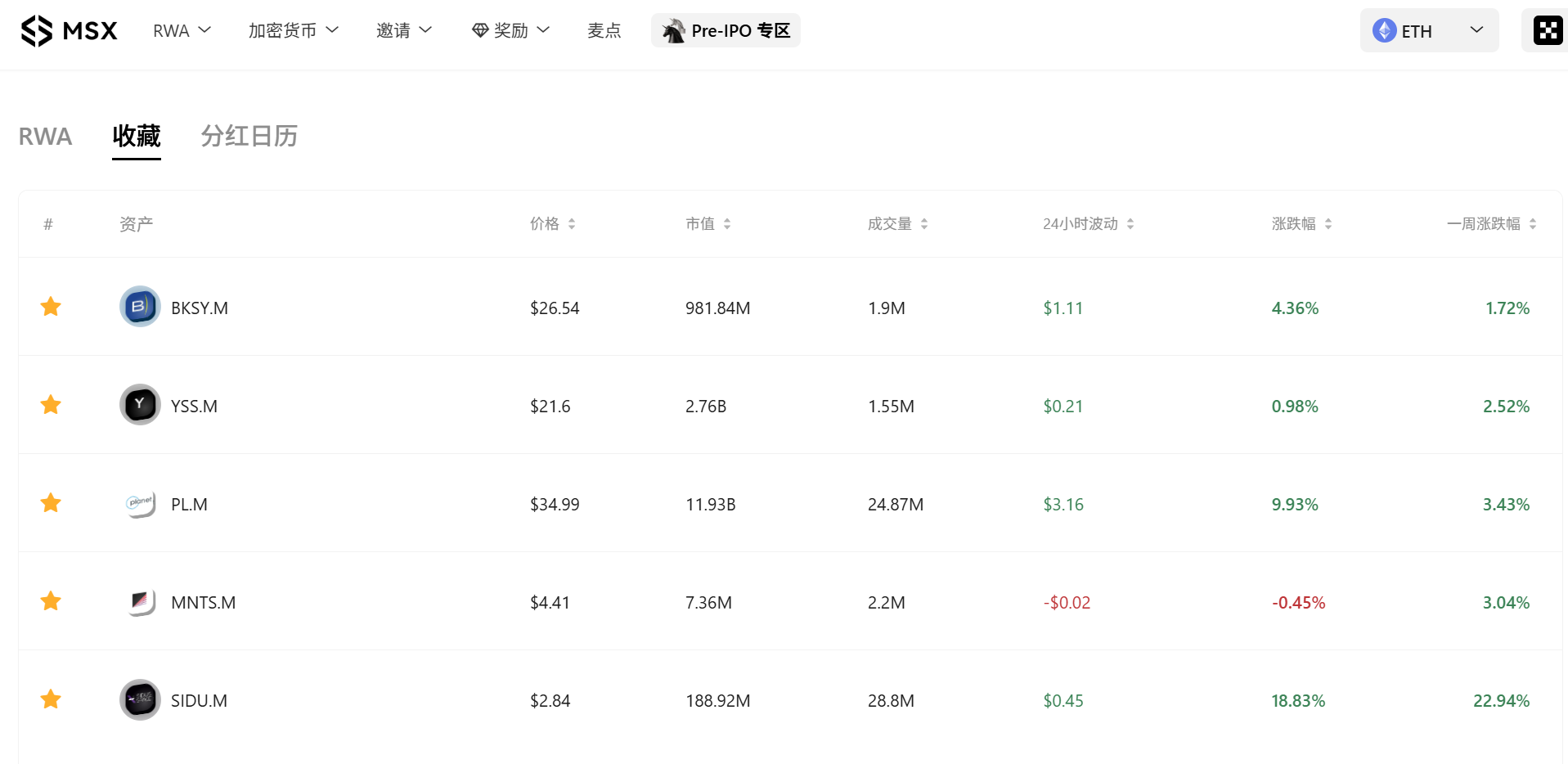

Sources reveal that SpaceX plans to confidentially file its IPO prospectus as early as this week or next, aiming to list in June. The commercial aerospace and space concept sectors reacted accordingly. It was precisely before this wave of market movement started that MSX listed five commercial aerospace U.S. stock tokens on March 23rd: MNTS.M, SIDU.M, PL.M, BKSY.M, and YSS.M. These tokens generally recorded double-digit gains, with some individual stocks surging nearly 30% intraday, providing investors with a relatively ample entry window.

Notably, SpaceX's fundraising scale could exceed $75 billion. If realized, this would not only be significantly higher than the previously rumored target of around $50 billion but would also far surpass Saudi Aramco's $29.4 billion fundraising record from 2019, making it the largest IPO in history, bar none.

This leads to the core question this article aims to discuss: beyond the emotional catalyst of the SpaceX rumor itself, what deeper logic underpins this rally in the commercial aerospace sector? And does this wave of revaluation have a foundation for further diffusion?

1. SpaceX IPO: The Starting Gun for the Commercial Aerospace Sector?

Although SpaceX has not yet gone public, its influence on the secondary market has never been absent.

To understand this, one must first grasp SpaceX's position within the entire commercial aerospace ecosystem. It is no longer just a rocket company but a provider of infrastructure supporting the operation of the entire commercial aerospace industrial chain, serving as the strongest "valuation anchor" in global commercial aerospace—from launch capacity to Starlink communications, from orbital transport to crewed flights, every technological breakthrough by SpaceX reduces costs and increases efficiency for the commercial pathways of a host of downstream small and medium-sized aerospace companies.

Precisely because of this, the current strength in space stocks is naturally first driven by the news catalyst of SpaceX's potential IPO launch. The $75 billion fundraising target and the potential $1.75 trillion valuation are figures that essentially serve as a shot in the arm for the entire commercial aerospace sector.

Consequently, we are not seeing strength in a single company but a synchronous warming across the entire space concept, forming a relatively clear sector-wide resonance.

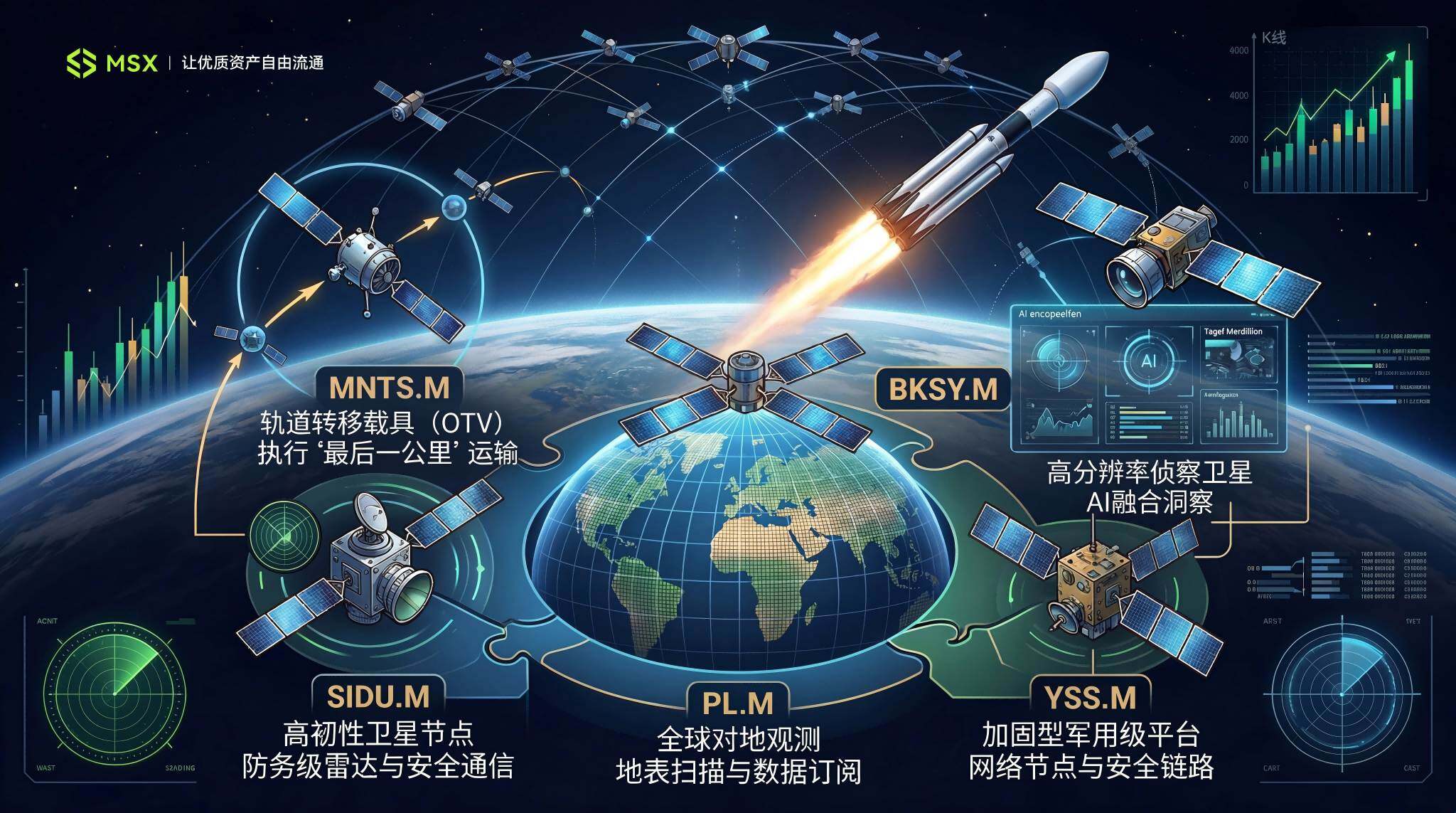

The most evident manifestation is the "Five Dragons" of commercial aerospace newly listed by MSX—MNTS.M, SIDU.M, PL.M, BKSY.M, YSS.M—each supported by solid fundamentals, collectively representing a concentrated coverage of several core directions within the commercial aerospace industrial chain:

MNTS.M (Momentus) is positioned for "last-mile" orbital transfer services in Low Earth Orbit (LEO). Its Vigoride vehicle is scheduled to ride on a SpaceX Falcon 9 for its next mission. Therefore, this is not merely a simple launch but more akin to a commercial validation, signifying that as global satellite constellation deployment accelerates, orbital transfer demand is shifting from an "option" to a "necessity."

SIDU.M (Sidus Space) acts as a "door opener" within the defense system, having secured qualification for multiple project office contracts from the U.S. Missile Defense Agency (MDA), thus holding a ticket for continuous bidding within the defense procurement system. For early-stage aerospace companies, government contract qualification is the most direct trigger for valuation reassessment and the most stable revenue anchor beyond commercial orders.

PL.M (Planet Labs) is the remote sensing leader with the most solid fundamentals in this rally and also the token with the highest total market capitalization among the five U.S. stock tokens newly listed by MSX. It possesses a global satellite constellation, daily revisit capability, and a commercially viable data subscription model.

This makes it one of the few space companies that can be discussed in terms of ARR and gross margin. Its backlog grew 79% year-over-year, approaching $900 million, and it achieved profitability for the first time—the significance of this inflection point extends far beyond a single quarterly report number.

BKSY.M (BlackSky) is pushing its transformation from a "satellite company" to an "intelligence service provider." Its core competitiveness stems from the closed-loop capability of high-frequency revisit + AI analysis. For instance, its third-generation (Gen-3) satellite constellation can provide commercial high-definition imagery with 35-centimeter (0.35-meter) resolution. Coupled with intelligence demand driven by geopolitical situations, shifting from selling data to selling decision support undoubtedly offers a much higher premium space than being a mere remote sensing data provider.

YSS.M (York Space Systems) is a core supplier for the U.S. Army's Proliferated Warfighter Space Architecture (PWSA) project, backed by the military. Military contracts provide a predictable cash flow foundation. As a recent IPO candidate, the institutional accumulation cycle is not yet complete, the shareholding structure is relatively clean, and it possesses high upward elasticity.

Ultimately, the five tokens MSX proactively listed this time are precisely intended to cover the core directions within the commercial aerospace industrial chain: some lean towards in-orbit transportation and mission execution, some towards satellites and defense orders, some towards Earth observation and remote sensing data, and some towards newly listed, high-elasticity satellite platform companies.

The significance of such a portfolio is not merely betting on a single event but attempting to make preemptive layouts around different beneficiary directions along the main theme of "Commercial Aerospace Revaluation," which is also the core factor behind MSX's successful early call on this broad-based rally.

2. Revaluation: From "Science Fiction" to "Hard Asset"

Of course, if this wave of gains is simplistically understood as "news-driven stimulus," it actually underestimates its historical context.

Reviewing the logic behind the stock selection that captured this surge, MSX was not blindly gambling on sentiment but captured two core signals:

- On one hand, at the recently concluded NVIDIA GTC conference, Jensen Huang announced a strategic-level layout in the space industry, from dedicated space-grade computing chips to cosmic digital twins for the orbital environment, all indicating that AI is no longer just a terrestrial productivity tool; it is becoming the underlying architecture for satellite autonomous navigation and real-time LEO data processing.

- On the other hand, on March 23rd, SpaceX, Tesla, and xAI jointly announced the launch of the "TERAFAB" project, aiming to leverage AI and highly automated manufacturing capabilities to produce one terawatt of AI computing chips annually, primarily for space deployment. This essentially paints an enormous picture of scaled multiplication for the secondary market.

Based on an in-depth analysis of these two major signals, the MSX research team decisively completed the listing coverage of the commercial aerospace "Five Dragons" on the 23rd.

As is well known, for a long time, the commercial aerospace sector was viewed as a "chicken rib" (unappealing yet not entirely discardable) in the secondary market, primarily because it was a "cash-burning" game: rockets, satellites, moon landings, deep space, Starlink—each term is sexy enough, but in the capital markets, many companies long faced high R&D investment, long project cycles, slow profit realization, and significant cash flow pressure.

But this time, something is starting to change.

Starting from 2025, commercial aerospace is no longer just about "launching rockets" but is gradually being deconstructed into a clearer, more easily understood real-world industrial chain for capital markets. Especially beyond rocket launches, more and more truly viable and sustainable order-generating businesses are emerging:

Satellite manufacturing, in-orbit services, Earth observation, defense remote sensing, LEO communication networks, AI-powered image analysis and intelligence distribution. This means the value of commercial aerospace is no longer derived solely from a distant future vision but increasingly from verifiable orders, service capabilities, and customer demand.

Looking further, three deeper underlying logics are simultaneously driving this wave of revaluation.

First, the significant decline in launch costs is changing the entire industry's economic foundation. The maturation of reusable rocket technology is continuously lowering the unit cost of reaching orbit. The decrease in launch costs, in turn, lowers the barriers for satellite constellation deployment, in-orbit services, and data commercialization.

For many small and medium-sized commercial aerospace companies, this means that businesses that could previously only stay at the experimental validation stage are beginning to have the potential for scaled deployment and reaching breakeven. SpaceX itself is the biggest driver of this cost curve, which is precisely why its IPO expectations have such a strong spillover effect on the entire sector.

Second, commercial aerospace is beginning to converge with larger era-defining themes. The strongest market narratives today are essentially AI, defense, communications, and new energy. Space infrastructure intersects with all these narratives. AI requires a continuous stream of high-quality data and stronger edge perception capabilities. Defense systems increasingly rely on real-time reconnaissance, space communications, and distributed satellite networks. Global geopolitical competition further elevates the strategic value of aerospace capabilities.

When a sector begins to embed itself into multiple mainstream narratives simultaneously, it ceases to be an isolated niche concept and is more likely to become a thematic hub for repeated capital allocation.

Finally, the market is beginning to accept differentiated pricing within the commercial aerospace sector. In the past, mentioning space stocks defaulted to them being emotional thematic assets, moving up and down together. Now, as the industry matures, investors are beginning to realize that different companies' values are not on the same level. For instance, some sell satellite platforms, some sell image data, some sell defense order qualifications, some sell in-orbit service capabilities, and some sell shareholding elasticity in the new listing stage.

This indicates that the commercial aerospace sector is gradually transitioning from thematic linkage to "industrial chain layered pricing." Once a sector enters this stage, it often signifies that it is no longer just a short-term concept but begins to possess a foundation for long-term research and continuous trading.

3. What Does This Wave of Space Stock Gains Mean for Investors?

Therefore, on the surface, this rally was indeed ignited by rising expectations for SpaceX. But looking deeper, what truly drives the market to place new bets is that commercial aerospace is transforming from a long-term narrative sector into a "pricable sector" with industrial stratification.

This is the underlying shift in logic that the capital market is willing to seriously price.

However, after the hype, how far the rally can go ultimately returns to the test of fundamentals. MSX Research Institute believes that after short-term emotional catalysts, the depth and sustainability of this rally will depend on the following key variables:

- Substantive Progress in SpaceX's IPO Process: Confidential filing of the prospectus is just the first step. Each milestone—roadshow, pricing, listing—will continuously provide topic heat and capital attraction effects for the sector.

- Implementation Pace of U.S. Defense and Aerospace Budgets: Incremental project budgets for the new fiscal year have been confirmed, but which companies the contracts will flow to will be gradually revealed over the next two quarters. This is a primary source of stock differentiation, as companies with actual contract support will increasingly diverge in performance from those purely driven by sentiment.

- Cash Reserves and Financing Capabilities of Individual Companies: Most early-stage aerospace companies are still in the loss-making phase. Periods of rising stock prices are often also windows for financing. A signal worth special attention is: whether management chooses to replenish ammunition at high levels rather than cash out and exit—this is the most direct and hardest-to-fake indicator for judging insider confidence.

Of course, regardless of short-term developments, the direction of one thing is becoming increasingly clear: SpaceX's IPO will not be the end of this industrial story. More likely, it is the starting point for the entire commercial aerospace industrial chain truly entering the mainstream capital's field of vision.

Over the past decade, the stories in this sector mostly remained at the PPT and concept level, with capital often pricing "imagination." In the coming years, the market will increasingly use real revenue, landed contracts, and verifiable profit milestones to re-measure the value of these companies.

For investors, this presents both opportunity and requirement.

Sector-wide resonance windows are not common, but only a select few among them can truly weather the cycles.