The Singularity of Mechanism, The Starting Point of the Bull Market: Short Selling Rights Are the Missing Piece to Ignite the Next Altcoin Bull Run

- Core Argument: The article posits that the core driver of cyclical booms in financial markets (including cryptocurrency) is not narratives, but rather the evolution of trading mechanisms and the expansion of game theory strategies, particularly the introduction and popularization of shorting tools. The root cause of the current predicament in the altcoin market lies in the lack of effective shorting mechanisms for true price discovery. On-chain native spot leverage shorting could be the key infrastructure upgrade to break the deadlock and catalyze the next bull market.

- Key Elements:

- Historical patterns show that from Wall Street to crypto markets, the introduction of shorting mechanisms (e.g., US stocks in the 1860s, BTC perpetual contracts in 2019) has not led to market collapse in the long run. Instead, by increasing liquidity, attracting diverse participants, and building price trust, it has driven market scale expansion.

- The current altcoin market suffers from ineffective price discovery due to most projects lacking effective shorting tools. This creates a "long-only" one-way game, making prices easily manipulated and fragile, trapping the market in a death spiral of shrinking liquidity and eroding trust.

- Between 2023-2025, despite exchanges launching perpetual contracts for numerous altcoins, this mechanism failed to replicate its success with BTC/ETH due to poor underlying asset quality (e.g., high FDV/low float), high market maker risk, and whale manipulation. Instead, it exacerbated the market's trust crisis.

- Perpetual contracts, as "heavy infrastructure," are unsuitable for long-tail altcoins. They suffer from structural flaws like liquidity death loops, price de-pegging, easily manipulated funding rates, and an inability to generate genuine selling pressure.

- The solution proposed in the article is to develop on-chain native spot leverage shorting (via over-collateralized lending to borrow and sell tokens). This is seen as a lighter-weight mechanism that requires no centralized approval and can generate real selling pressure, potentially bringing true price discovery and sustainable liquidity to the altcoin market.

- The core conclusion is that the ignition point for the next altcoin bull market may not be a new narrative, but rather the evolution of infrastructure that grants convenient, decentralized shorting capability to a vast number of long-tail assets, thereby restoring diversity and health to market dynamics.

Original Author: danny (X: @agintender)

In the three hundred years of financial markets, there is a repeatedly verified pattern: bull markets are never ignited by a single narrative, but by the upgrade of trading mechanisms. Whether it's ICOs, perpetual contracts, AMMs, DeFi, NFTs... it's always mechanisms driving competition, and competition bringing capital into the cycle. It's the mechanism upgrades that bring prosperity.

Looking back at the starting point of every major market cycle, you'll find their commonality is not "the emergence of a good story," but "market participants suddenly gained a new way to compete."

What ignites the next round of prosperity is never the narrative, but the evolution of trading mechanisms each time.

This pattern, from Wall Street to Binance, from spot to futures, from DeFi summer to Hyperliquid, has never failed.

You can short it — aka the democratization of the right to short is the catalyst for the next altcoin bull market.

1. 1609: A Dutch Merchant Changed Financial History

1609, Amsterdam.

The Dutch East India Company (VOC) was the world's largest listed company at the time, monopolizing the Asian spice trade, with its stock price only going up. Everyone was buying, everyone was making money. The market had only one direction—up.

Then a merchant named Isaac le Maire did something everyone at the time considered insane: he borrowed VOC shares, sold them, betting they would fall.

This was the first recorded short sale in human history.

The Dutch government was furious. Parliament deemed it a malicious attack on a national pillar enterprise and legislated to ban short selling. le Maire was publicly condemned. But the story didn't end there—despite repeated bans, short selling never truly disappeared in Amsterdam. Because market participants discovered an undeniable fact: with short selling, prices became more real. Overvalued stocks could no longer sustain false prosperity indefinitely.

Four hundred years later, the crypto market is replaying the same script. In a market with thousands of altcoins, there is only buying, no shorting. Prices reflect only the optimistic half; pessimistic voices are forcibly silenced. Every cycle is the same loop: FOMO pushes prices up, the bubble bursts, leaving a mess, waiting for the next narrative to restart.

But history has told us—the introduction of the right to short has never been the end of the market, but rather its beginning.

2. Two Hundred Years on Wall Street: How Shorting Went from "Public Enemy" to "Market Cornerstone"

1792-1840s: The Wild Era—A Primitive Market That Could Only Go Long

On May 17, 1792, 24 brokers signed the Buttonwood Agreement under a buttonwood tree on Wall Street, agreeing to trade stocks with each other. This was the precursor to the New York Stock Exchange (NYSE).

The market then was similar to today's altcoin market: you could only buy, hold, wait for dividends, wait for the new year. No leverage, no shorting, no standardized settlement process. Daily trading volume was likely less than $500,000, with only a few dozen participants. The market was tiny because there was too little one could do.

Price volatility was driven entirely by bullish sentiment. Good news came, everyone bought, prices soared. Bad news came, everyone wanted to sell, but because the market was too shallow, they couldn't, and prices crashed. With no shorts covering on the way down, there was no natural support; the bottom depended entirely on when the last bull gave up.

Doesn't this resemble the 2024~2025 Meme, high FDV, low Float altcoin market?

1850-1860s: Shorting Takes Center Stage—Fear and Prosperity Arrive Simultaneously

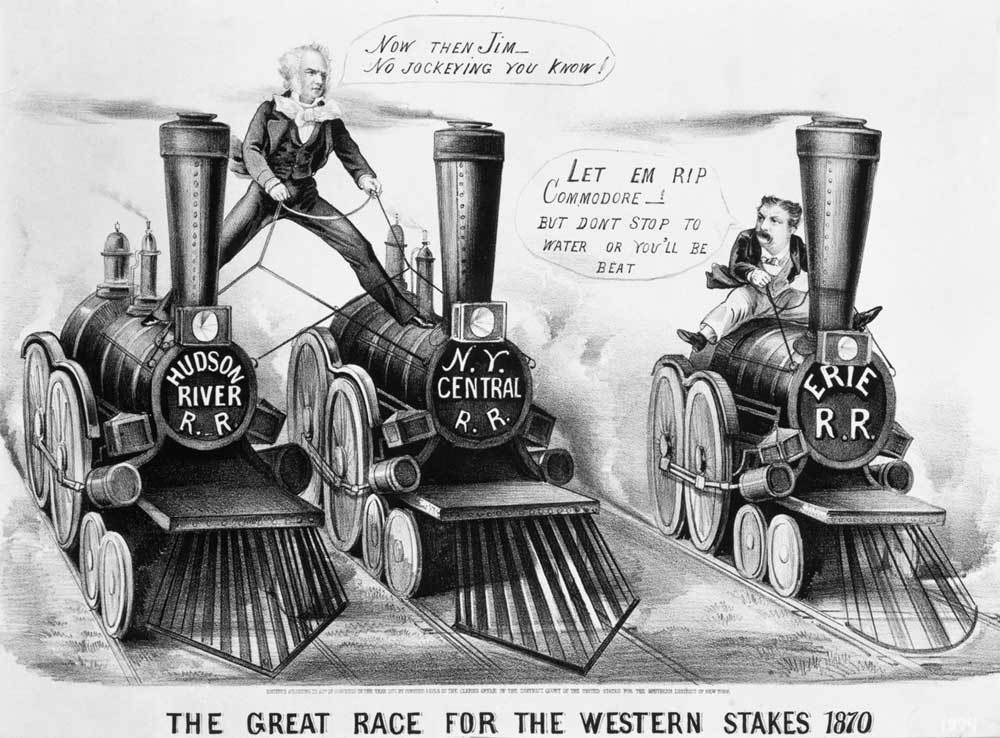

In the 1830s-1840s, a trader named Jacob Little made a fortune shorting and was called "Wall Street's first great bear." But shorting truly became a mainstream weapon in the decade around the Civil War.

Daniel Drew, Jay Gould, Cornelius Vanderbilt—these names defined Wall Street of that era. They waged epic long-short battles around railroad stocks: Drew shorted Erie Railroad, Gould and Fisk teamed up to snipe Vanderbilt's long positions. These battles were bloody, chaotic, full of fraud, but the objective result was—shorting went from a secret weapon of the few to a standard tool on Wall Street.

The societal reaction was identical to that in 1609 Holland. Congressmen called short sellers "enemies of the state," newspapers said they "profited from others' disasters." Public fear of shorting has hardly changed in four hundred years.

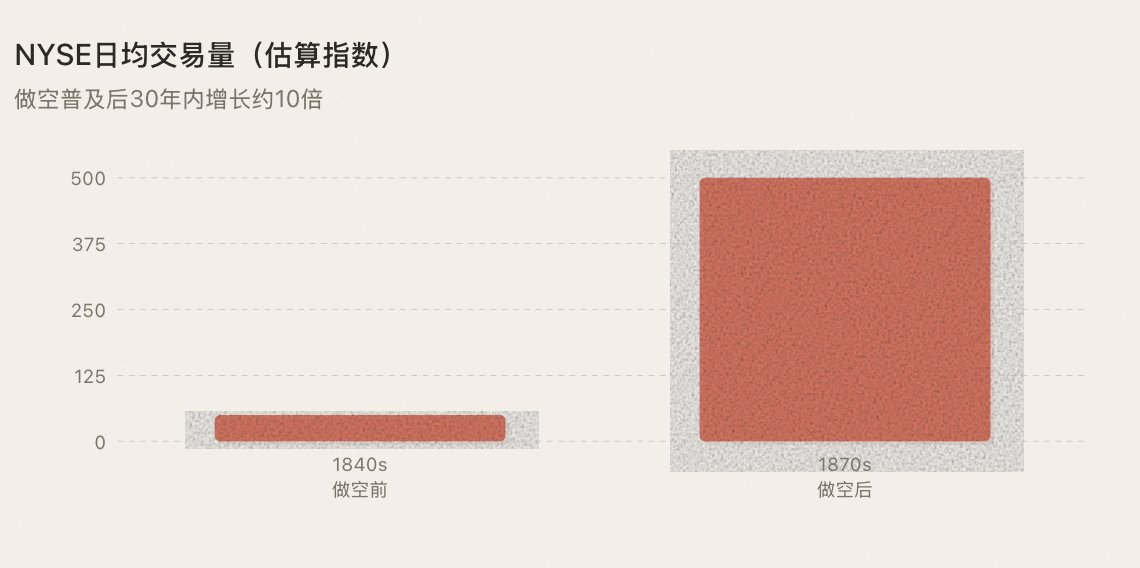

But the market's response was also the same as four hundred years ago, positive and vigorous: 📷

Every short sale created a sell order, but also a future buy order that must be executed (short covering). Trading volume increased, spreads narrowed, more people were willing to enter. Wall Street began transforming from a small circle of dozens into a real capital market.

1929 Crash → 1938 Uptick Rule: The Peak of Fear, and the Turning Point

October 1929, Wall Street crashed. The Dow Jones Industrial Average lost nearly 90% in two years. Public anger needed an outlet, and short sellers became the most convenient target—even though the real culprits were the insane leverage bubble and systemic banking collapse.

1934, the U.S. Securities and Exchange Commission (SEC) was established. Shorting again faced the danger of being completely banned. But the SEC made a historic choice: in 1938, it did not ban shorting but introduced the "uptick rule" (Rule 10a-1)—short sales could only be executed on an uptick in price, preventing bears from continuously hammering the price down.

The significance of this choice cannot be overstated. It established a principle that continues to this day: shorting should not be eliminated; shorting should be regulated. Rules are not the enemy of shorting; rules are the prerequisite for shorting to gain legitimacy.

With rules, shorting was no longer a gray area. Institutional capital, which had been wary of shorting, now had the protection of a legal framework, making them more willing to participate on a large scale. Regulation did not kill shorting; regulation made shorting safer, more credible, attracting more capital into the market.

This is a lesson the crypto market still hasn't truly learned to this day.

1973: Option Standardization—From One Direction to Four Directions

On April 26, 1973, the Chicago Board Options Exchange (CBOE) opened. On the first day, only call options for 16 stocks could be traded. Put options were added in 1977. That same year, Fischer Black and Myron Scholes published the Black-Scholes option pricing model, which changed financial history, providing a mathematical foundation for options trading.

The significance of options lies in this: they expanded the market's competitive dimensions from two (buy/sell) to four (buy call/buy put/sell call/sell put). For the first time, investors could express their market views with great precision—not just "up or down," but "at what time, at what speed, up or down by how much."

More crucially, options gave institutional investors a complete hedging arsenal. The great bull market of the 1980s (the S&P 500 rose over 2200% between 1982-2000) was directly triggered by Volcker controlling inflation, Reagan's tax cuts, and deregulation, but options provided the risk management infrastructure that allowed institutions to increase their positions. If you can hedge, you dare to go heavy; the more people dare to go heavy, the more capital inflows, and the bull market arrives.

For the wealthy and institutions, controlling drawdowns is more important than how much can be earned—uncontrollable risk means big money cannot enter.

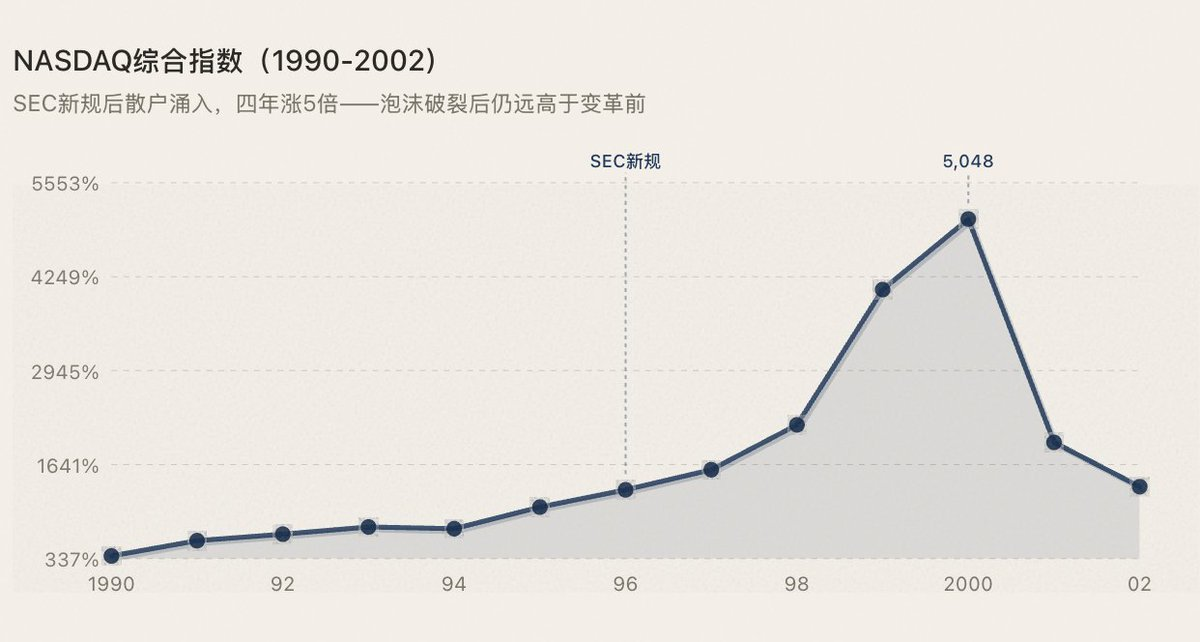

1996-1997: Retail Breaks Down the Door

NASDAQ has been an electronic exchange since its founding in 1971—the first in human history. The real change in 1996-1997 was two things: the SEC's Order Handling Rules broke the market makers' monopoly on quotes; online brokerages (E*Trade, Ameritrade) slashed trading commissions from $50-100 to under $10.

The bubble eventually burst, but NASDAQ's market cap after the bubble was still far higher than before the changes—because the increase in participants brought by infrastructure upgrades is irreversible.

1993-2010s: Maturation of a Complete Ecosystem

Many think ETFs are a product of the last decade, but the first ETF—SPY (tracking the S&P 500)—was listed on the American Stock Exchange in 1993. In 2001, the SEC mandated decimalization, shrinking bid-ask spreads from $0.125 directly to $0.01, significantly reducing trading costs. Between 2005-2010, high-frequency trading (HFT) rose, once accounting for over 60% of daily U.S. stock trading volume. Quantitative strategies, ETF arbitrage, long-short hedging—all directional strategies had standardized tool support.

By this point, the U.S. stock market's competitive tool system was fully mature. Going long, shorting, hedging, arbitraging—every type of strategy capital could find its own entry method. Result:

The pattern is actually as clear as it can be: whenever a new trading mechanism allows more people to participate in the market in more ways, prosperity arrives. (As shown in the chart below)

3. Eight Years in the Crypto Market: Two Hundred Years of Evolution Completed in Eight

The mechanism upgrades that took Wall Street two hundred years to complete, from Binance's launch in 2017 to the maturity of perpetual contracts, took less than eight years. But evolution stalled at the altcoin layer.

2017—The Buttonwood Moment

Binance launched, only spot. What you could do was the same as the brokers in 1792: buy, hold, wait for it to rise.

The ICO bubble was the best mirror. Everyone was buying, prices could only go up. Then buying dried up—in a market with no shorts, there's no short covering to provide natural support, prices free-fall, the bottom depends on when the last bull gives up. Altcoins crashed across the board. This is identical to the market characteristics of the 1792 Buttonwood era.

2016-2019—The Shorting Weapon Arrives

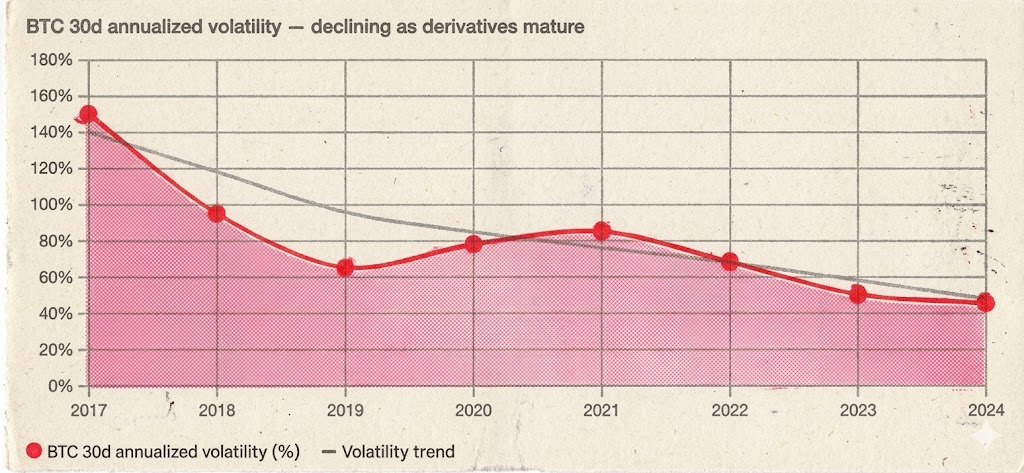

May 2016, BitMEX launched the XBTUSD perpetual contract—the crypto market's first shorting tool. September 2019, Binance launched the BTC/USDT perpetual contract, bringing shorting into the mainstream.

What happened? Exactly the same thing that happened after Wall Street introduced shorting in the 1860s: liquidity exploded, price discovery became two-way, volatility structurally decreased.

BTC's 30-day annualized volatility dropped from over 150% during the 2017 bull run to 60-90% during the 2020-2021 bull run—gains were larger, but volatility was more orderly. Sharp rises and falls still occurred, but situations of "low-volume gradual decline for three months" significantly decreased because shorts would cover at certain price levels, forming natural support.

More importantly, the scale of capital underwent a leap. With hedging tools, institutional capital was willing to enter on a large scale. You can't expect a fund manager overseeing billions of dollars to throw money into a market that can only go long and cannot be hedged. Perpetual contracts didn't just give retail the right to short; they gave the entire market an "institutions can enter" infrastructure.

The proportion of derivatives in total trading volume rose from less than 10% in 2017 to about 90% in March 2026—derivatives have completely dominated crypto market pricing power:

Shorting did not kill BTC. Shorting turned BTC from a $10 billion speculative product into a $2 trillion asset class.

2020-2021—DeFi Summer: Not Just a Narrative, Itself a Mechanism Evolution

The BTC and ETH options markets matured rapidly in 2020-2021 (primarily on Deribit). This was the crypto market's "1973 CBOE moment"—institutions could not only short but also hedge precisely and construct structured positions. The dimensions of strategies expanded from two to higher dimensions.

Furthermore, many categorize DeFi Summer as a "narrative"—like the NFT craze, the metaverse concept, just another wave of hype. But this is a fundamental misreading. The essence of DeFi Summer was not a narrative but a structural leap in trading mechanisms.

AMM (Automated Market Maker) rewrote the underlying logic of trading. Before Uniswap, trading required order books, market makers, centralized matching. AMM overturned all that—anyone could form a liquidity pool with two tokens, anyone could trade instantly, no need for counterparties to place orders, no need for anyone's permission. This is not a narrative; this is a paradigm shift in trading infrastructure. It gave thousands of long-tail tokens, which previously had no trading market at all, liquidity for the first time.

Lending protocols created on-chain leverage and loop strategies. Aave, Compound allowed users to collateralize assets to borrow another asset—this is essentially on-chain margin trading. More crucially, it spawned "recursive lending": collateralize ETH to borrow stablecoins, use stablecoins to buy more ETH, collateralize again... This strategy is called leveraged long in traditional finance, packaged as "yield farming" in DeFi, but the underlying logic is identical—it's a new way to compete, allowing participants to engage the market with multi-dimensional strategies.

Composability caused mechanism innovation to compound exponentially. AMM + Lending + Liquidity Mining + Cross-protocol Arbitrage—the combination of these "money legos" created a strategic space that never existed in traditional finance. Each new combination was a new way to participate, and each new way to participate brought new capital and new users.

So the 2020-2021 super bull market was not the result of two factors overlapping, but three: BTC and ETH perpetual contracts/options gave institutions entry and exit channels; DeFi's AMMs and lending protocols qualitatively changed on-chain trading mechanisms; the narrative was merely the surface packaging of these two layers of mechanism evolution.

Once again, the same pattern was verified: every evolution in trading mechanisms gave rise to the next round of prosperity.

2021-2023—Altcoin Perpetual Expansion

Binance began launching perpetual contracts for more and more altcoins. Every new token getting a perp saw a step-function jump in trading volume—not because "listing a perp" was bullish news, but because the