Tiger Research: Analysis of the Current State of Retail Investors in Nine Major Asian Markets

- Core Viewpoint: Although the cryptocurrency market has expanded due to the influx of institutional capital, the conversion of retail investors ("crypto-curious individuals") in Asian markets faces bottlenecks. The report points out that regulatory uncertainty, security risks, tax burdens, insufficient ease of use, and negative social perception are the five core obstacles, with significant variations across countries. Exchanges need to adopt localized compliance, security transparency, and educational strategies to address these challenges.

- Key Elements:

- Structural Market Changes: Institutional capital has dominated growth following the approval of US spot ETFs, but retail trading volume and user numbers have declined, the appeal of altcoins has weakened, and Bitcoin's market dominance stands at approximately 60%.

- Five Core Obstacles: Factors hindering potential investors from entering the market include regulatory uncertainty, security risks (e.g., hacking), tax burdens, product complexity and difficulty of use, and the social perception that views cryptocurrency as "gambling."

- Significant Differences Across Asian Markets: For example, South Korea has active trading but interest has shifted to the stock market; Japan has secure regulation but a high tax rate of up to 55%; Hong Kong has clear regulations but high service thresholds, primarily targeting professional investors.

- Exchange Response Strategies: The primary task is to obtain local operating licenses, followed by enhancing transparency and security trust through technologies like Proof of Reserves and cold wallet storage ratios, and deepening customized education in local languages, currencies, and regulations.

- Competition from Traditional Finance: Traditional brokerages provide familiar entry points through products like ETFs. Cryptocurrency exchanges need to clearly articulate their unique value propositions, such as a broader range of tokens, DeFi, and on-chain experiences.

This report is written by Tiger Research. Although the cryptocurrency market is growing rapidly, the number of retail investors is declining. We analyzed the entry barriers in nine Asian markets with the largest potential user bases and the countermeasures taken by exchanges.

1. The Market Has Grown, But Retail Has Shrunk

Since the US approved spot ETFs in 2024, institutional capital has flooded in. Companies are adding Bitcoin to their balance sheets. Exchanges have begun tokenizing US large-cap stocks. The barriers between traditional finance and crypto are breaking down on both sides. The market size has expanded significantly.

But retail is moving in the opposite direction. Retail trading volume and user numbers are declining across countries.

In previous cycles, high-yield altcoins attracted a large number of new users. But that driver is gone. Altcoin volatility is not what it used to be. Bitcoin's market share has reached about 60%. There is currently no mechanism to attract new users, only existing users remain.

However, major exchanges are adopting a series of strategies to attract new users.

Exchanges refer to these potential investors as "crypto-curious": they know about crypto, are interested, but haven't invested yet. Considering the population size and internet penetration rates in major Asian countries, the number of these potential investors reaches tens of millions. As existing user growth hits a bottleneck, the crypto-curious will become the key factor determining the industry's next phase of development.

Volatility is the most frequently cited barrier. But volatility is a surface symptom, not the root cause. Stocks are also volatile, but people still buy them because there is government regulation, funds are protected, and society views them as legitimate investments. Crypto lacks these three things.

Five core barriers prevent crypto-interested people from investing:

- Regulatory Uncertainty: Legal protection is unclear. Some countries have clear rules, while others do not.

- Security Risks: Fear of exchange hacks, funds disappearing, or assets being frozen.

- Tax Burden: Tax rates are difficult to predict, and policies may change.

- Ease of Use: It's hard to know where and how to start. Staking, DEX trading, and other complex mechanisms increase friction.

- Social Perception: Crypto trading is seen as "gambling."

Each of the eight Asian markets analyzed in this report faces different bottlenecks.

2. Analysis of Crypto Interest in Major Asian Markets: Different Obstacles for Each Country

2.1 Northeast Asia: South Korea, Japan, Hong Kong

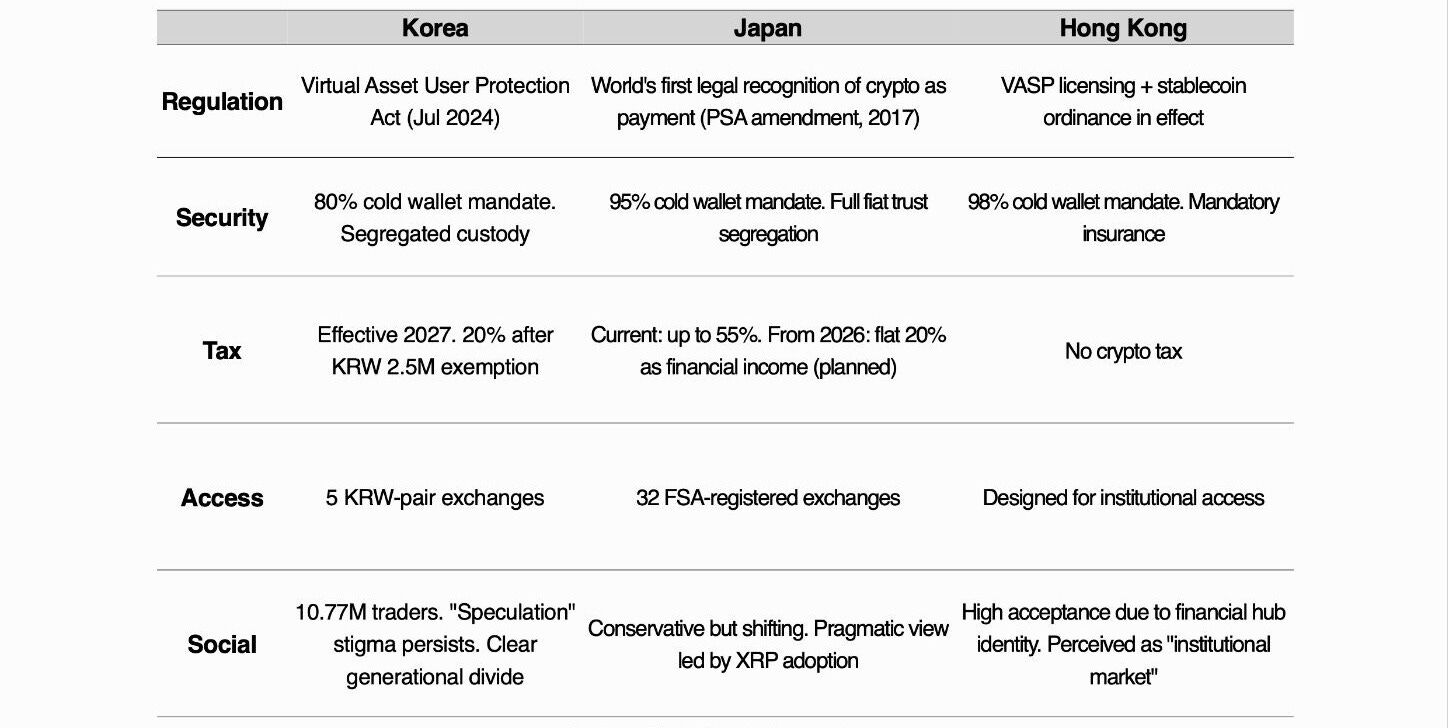

Comparison of Northeast Asian Countries

Northeast Asia is the region with the fastest-developing crypto regulation. These three markets have either already established dedicated legal frameworks or licensing systems, or are about to launch them.

But the regulatory direction and the nature of each market are starkly different. South Korea has a strong culture of speculative trading. Japan exhibits a unique trading structure centered on XRP. Hong Kong is focused on building a global hub centered on institutional investors.

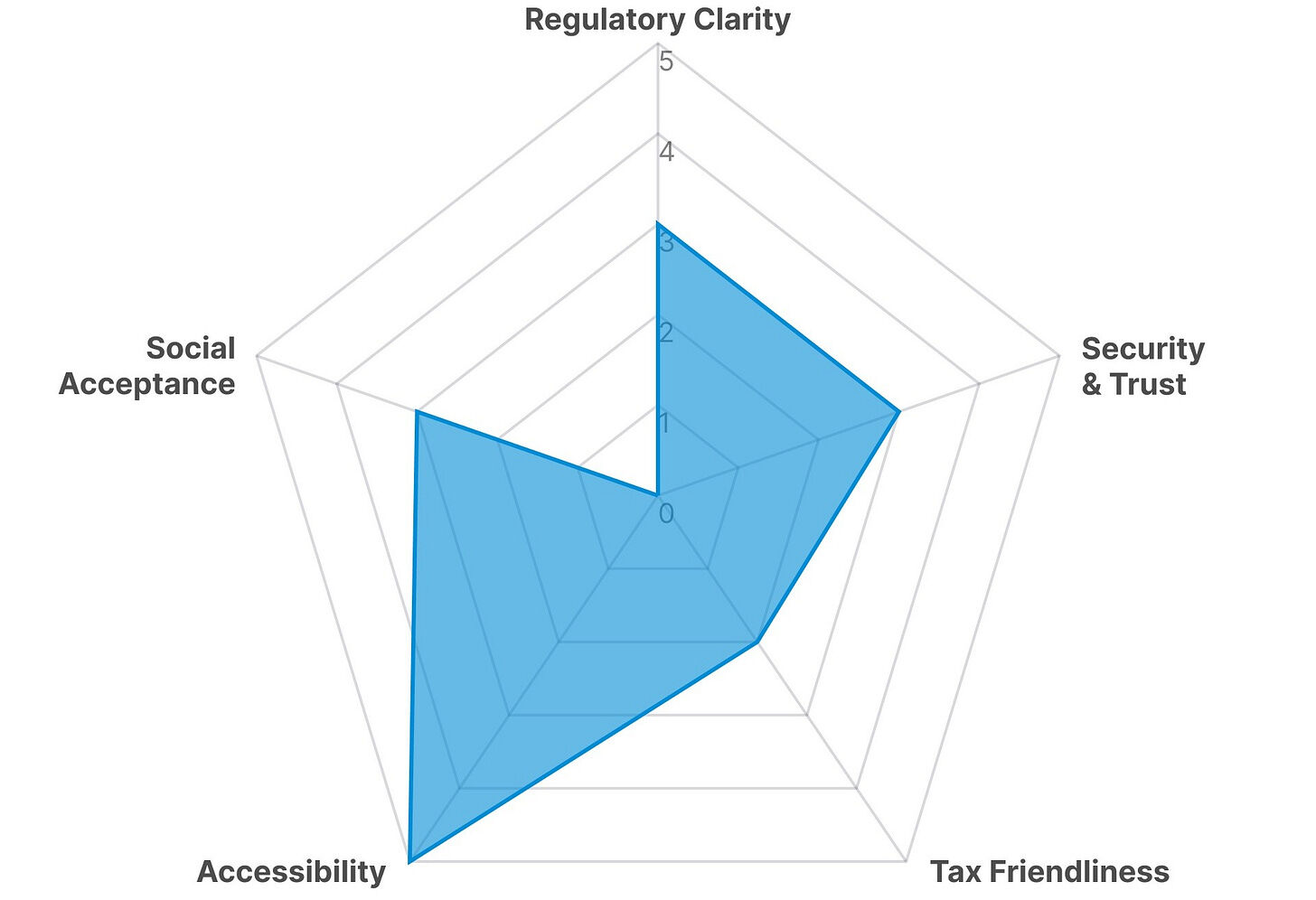

2.1.1. South Korea: Second in User Numbers, But User Count is Declining

South Korea's Retail Crypto Investment Environment: Five Key Indicators

In Asia, South Korea has the most active fiat-to-crypto trading.

In the second half of 2025, Korean Won trading volume reached $663 billion, almost on par with global USD volume, ranking second globally. The number of eligible KRW traders was 11.13 million, about 21.5% of the population.

Korean users have shown strong willingness for crypto trading. However, despite an 11% increase in user numbers from the previous period, daily average trading volume and fiat deposits have declined. The stock market is becoming a more attractive investment option, and interest in crypto is waning.

Users are also migrating to offshore exchanges to access unlisted tokens and leverage products. Crypto taxation is scheduled for implementation next year. As the proposed rules differ from current equity tax treatment, it could still be scrapped, but if implemented as planned, trading demand is expected to decline further.

Nevertheless, South Korea's position as the world's second-largest trading market, combined with the aggressive investment sentiment of Korean traders, creates an environment unmatched by other Asian markets. If crypto can achieve the same tax treatment as stocks, and exchanges can adopt diversified investment strategies, then South Korea's well-developed infrastructure could make it the fastest market to convert crypto-curious individuals into crypto investors.

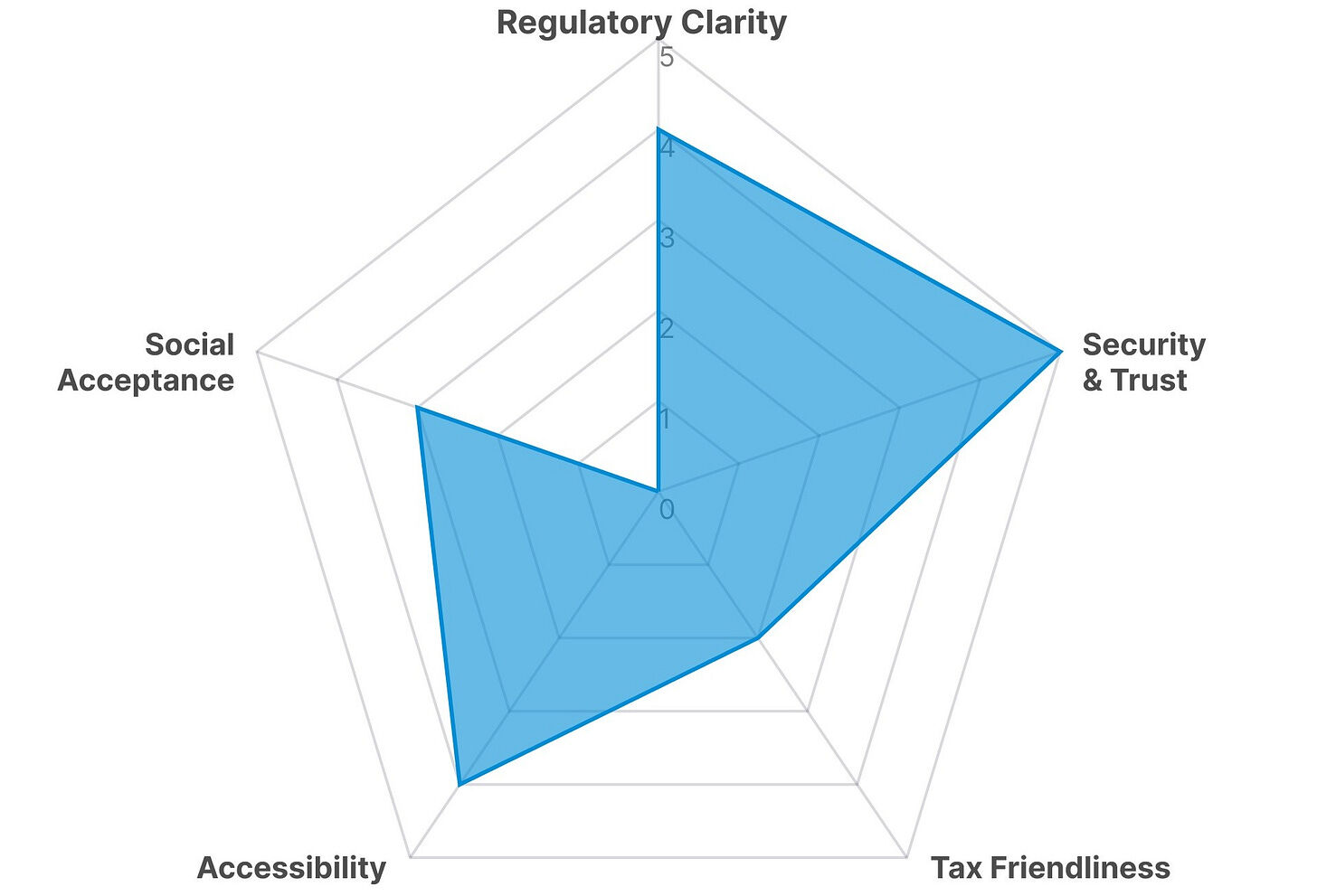

2.1.2. Japan: The Safest and Most Expensive

Japan's Retail Crypto Investment Environment: Five Key Indicators

Japan is Asia's safest crypto market, and also the most expensive.

After the Mt. Gox hack in 2014, which lost about 850,000 Bitcoins, Japan became the first country to establish an exchange licensing system. This lesson shaped Japan's current exchange licensing regime. Exchanges must store over 95% of client assets in cold wallets and keep all client fiat in fully segregated trust accounts.

Japan has 32 FSA-registered exchanges, with a cumulative account number of 12 million and total client deposits of ¥5 trillion. Compared to other parts of Asia, the signal of "safe to enter" is stronger in Japan.

But once you enter the crypto market, taxes follow. Currently, crypto gains are classified as miscellaneous income with a maximum tax rate of 55%. Earning ¥100 million means paying ¥55 million in tax. The same stock gain would be taxed at about 20%, or ¥20 million. That's a 2.7x difference. Asia's safest market imposes Asia's highest tax.

This contradiction is the core obstacle for Japan's crypto-curious. Confidence in safety matters, but safety comes at a cost. You can enter crypto, your funds are protected, but you might end up with nothing.

Its market structure is also unique. From July 2024 to June 2025, the total trading volume of XRP in JPY on exchanges was about $21.7 billion, 4.6 times that of Bitcoin ($4.7 billion). Japan is the only market globally where a single altcoin's trading volume exceeds Bitcoin's.

This is the result of the strategic partnership between SBI Holdings and Ripple. In Japan, XRP is not seen as a speculative asset but as a crypto asset with actual utility. In a savings-oriented, speculation-averse society, crypto finds its footing differently than in South Korea.

However, social adoption of crypto remains slow. Among individual investors with investment experience, only 7.3% hold crypto assets. In contrast, companies are actively embracing crypto. Metaplanet, dubbed the "Asian MicroStrategy," is accumulating Bitcoin as a strategic asset, and SBI Holdings plans to list a BTC+XRP dual-asset crypto ETF on the Tokyo Stock Exchange.

The key variables are two reforms scheduled to take effect in April 2026. One reform reclassifies crypto assets under the Financial Instruments and Exchange Act (FIEA). The other reform unifies the tax rate on financial income to 20%, the same as for stocks. If both reforms take effect simultaneously, the biggest obstacle for Japan's crypto-curious will disappear.

Since these changes have been announced in advance, there is no reason for the crypto-curious to enter the space now and risk a potential 55% tax rate.

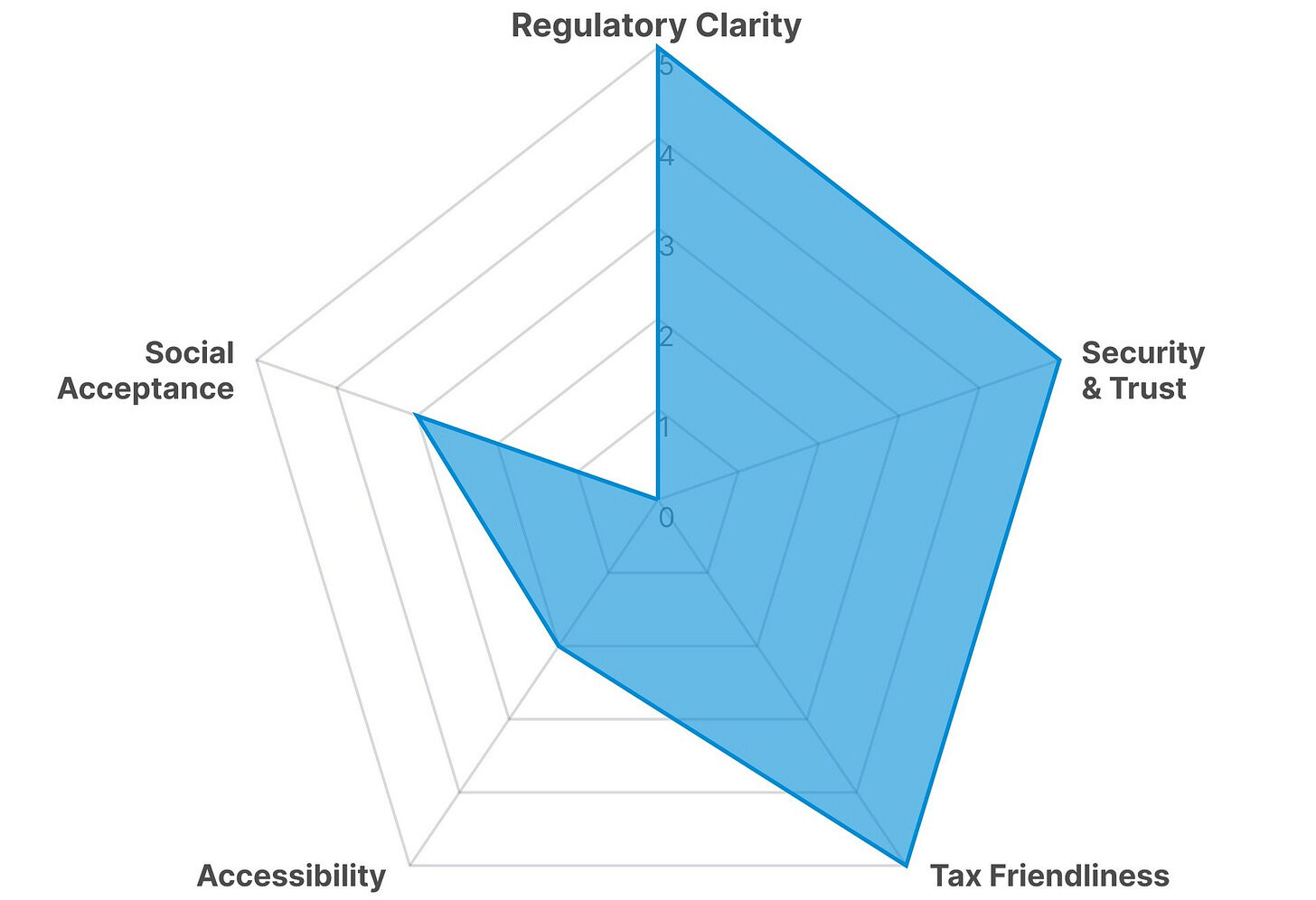

2.1.3. Hong Kong: Three Barriers Cleared, But the Path is Still Blocked

Hong Kong's Retail Crypto Investment Environment: Five Key Indicators

Hong Kong has done a better job than any other Asian market at removing key barriers for the crypto-curious. Regulation is clear, security standards are high, and there is no tax burden. No other Asian market meets all three requirements at the highest level simultaneously.

The SFC has implemented a VASP licensing regime since 2023. In February 2025, the SFC released the ASPIRe roadmap outlining future regulatory direction. In August of the same year, the SFC announced a stablecoin regulatory regime, with the first licenses expected in early 2026.

Exchanges must store over 98% of client assets in cold wallets. Exchanges must purchase mandatory insurance and undergo annual cybersecurity audits. Crypto is not taxed. In 2024, Hong Kong approved Asia's first batch of Bitcoin/Ethereum spot ETFs.

Regulation, security, and tax issues are largely resolved. The remaining issue is accessibility.

As of February 2026, 12 platforms hold SFC licenses, but their services primarily target professional investors with assets of HK$8 million (approx. ₩1.3 billion) or more. Unlike in South Korea where users can download an app and buy immediately, Hong Kong's regulatory system does not permit this. Hong Kong's regulatory quality is among the best in Asia, but the threshold to enter this regulatory framework is low.

Social perception occupies a unique position. Due to the city's status as a global financial hub, the "gambling" stigma is far less than in South Korea or Japan. But there is a widespread perception that crypto is "for professionals." While there is no social prejudice, there is also a lack of social validation. This psychological distance is too great for the crypto-curious to think, "Maybe I should give it a try."

The path for change is opening. The SFC introduced a shared liquidity framework allowing licensed platforms to access offshore order books. Staking services have received conditional approval. A trader and custodian licensing regime is planned for legislative consultation in 2026. The range of available products and channels is expanding.

In a nutshell: Hong Kong has solved three of the five barriers, but the fourth—access—negates the advantages of the other three. No matter how safe and tax-free it is, if you can't get in, it's meaningless. Hong Kong's task is to widen the gate so more people can experience the trust it has already built.

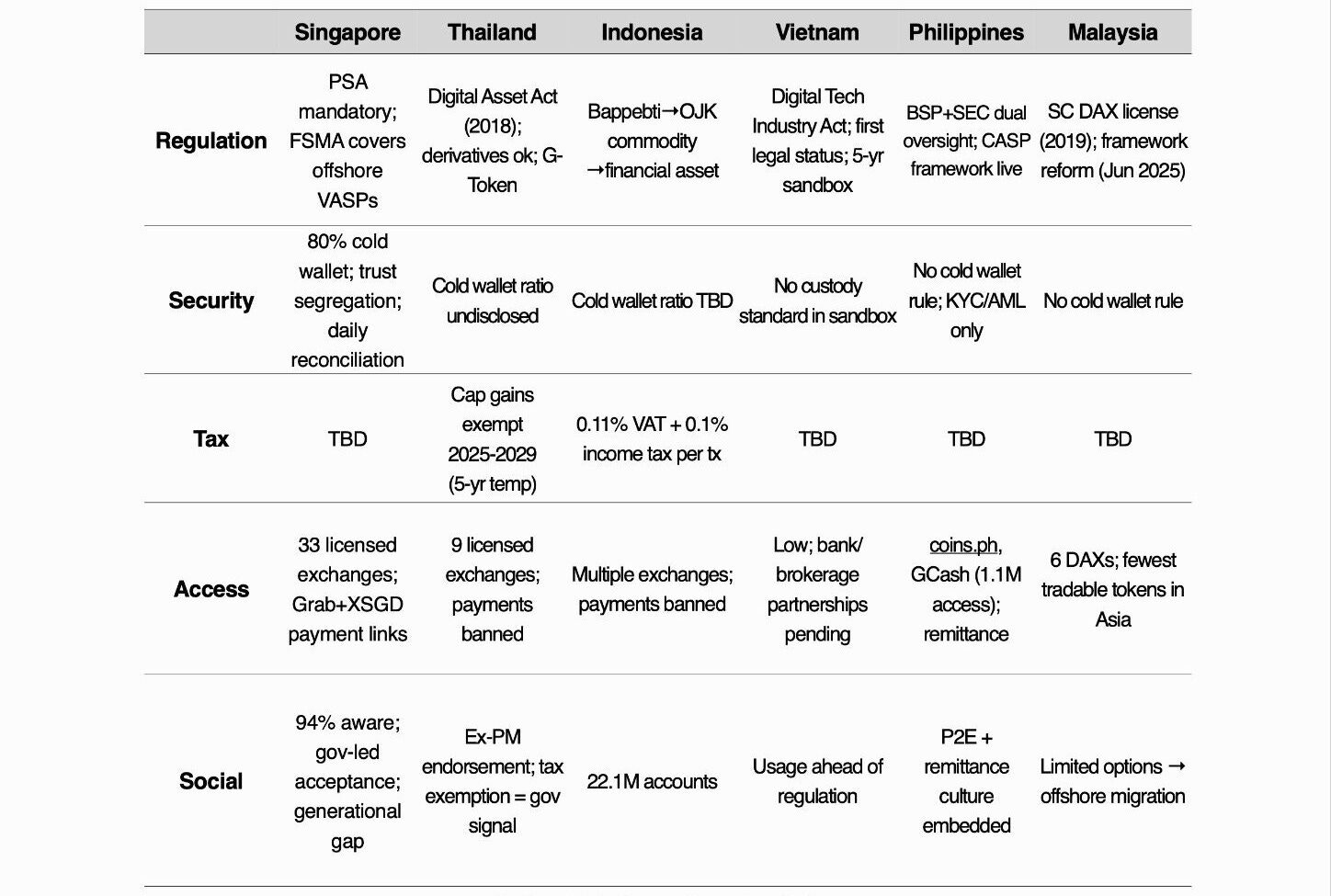

2.2 Southeast Asia: Singapore, Thailand, Indonesia, Vietnam, Philippines, Malaysia

Southeast Asian Country Comparison Options

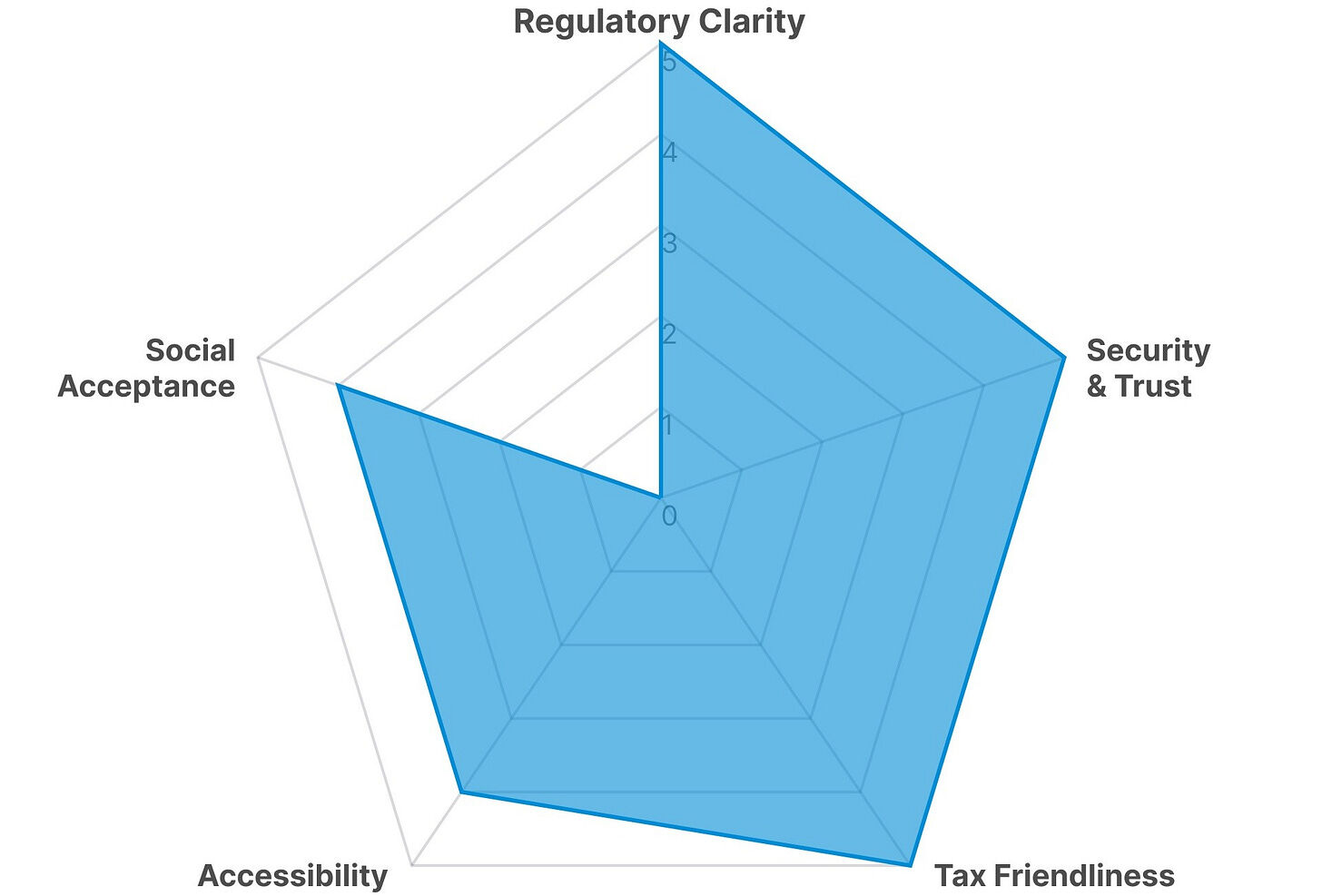

2.2.1. Singapore: All Conditions Met, But 65% Still Choose Not to Enter

Singapore's Retail Crypto Investment Environment: Five Key Indicators

Among the eight markets covered in the report, Singapore is the most balanced across all five barrier dimensions (regulation, security, tax, convenience, and social perception), with no dimension being particularly weak.

The Monetary Authority of Singapore (MAS) operates Asia's most unified licensing regime. In June 2025, MAS extended licensing requirements to operators serving only overseas clients. Exchanges must segregate client assets in trust accounts. Singapore has completed its mutual evaluation with the FATF. Singapore does not tax crypto.

Practical applications of crypto are expanding. Grab has integrated stablecoin XSGD payments. MAS has piloted tokenized government bonds, and the three major banks have tested interbank loans based on CBDC. Within the regulatory framework, crypto is gradually permeating daily finance.

In theory, the crypto-curious should have no reason to stay out. However, the data tells a different story. Public awareness of crypto in Singapore is at a record high of 94%, but the actual holding rate is only 29%. The remaining 65% are merely crypto-curious.

This 65% is not uninformed. They have knowledge, can access information, face no social discrimination, yet still choose not to participate. The biggest barrier they cite is market volatility (68%), and the top criterion for choosing an exchange is "trust and security" (65%), even higher than fees.

Singapore is a thought-provoking counterexample. Even when almost all institutional barriers are removed, 65% of people remain outside the crypto market. Other Asian markets should note that merely removing barriers does not guarantee conversion of the crypto-curious.

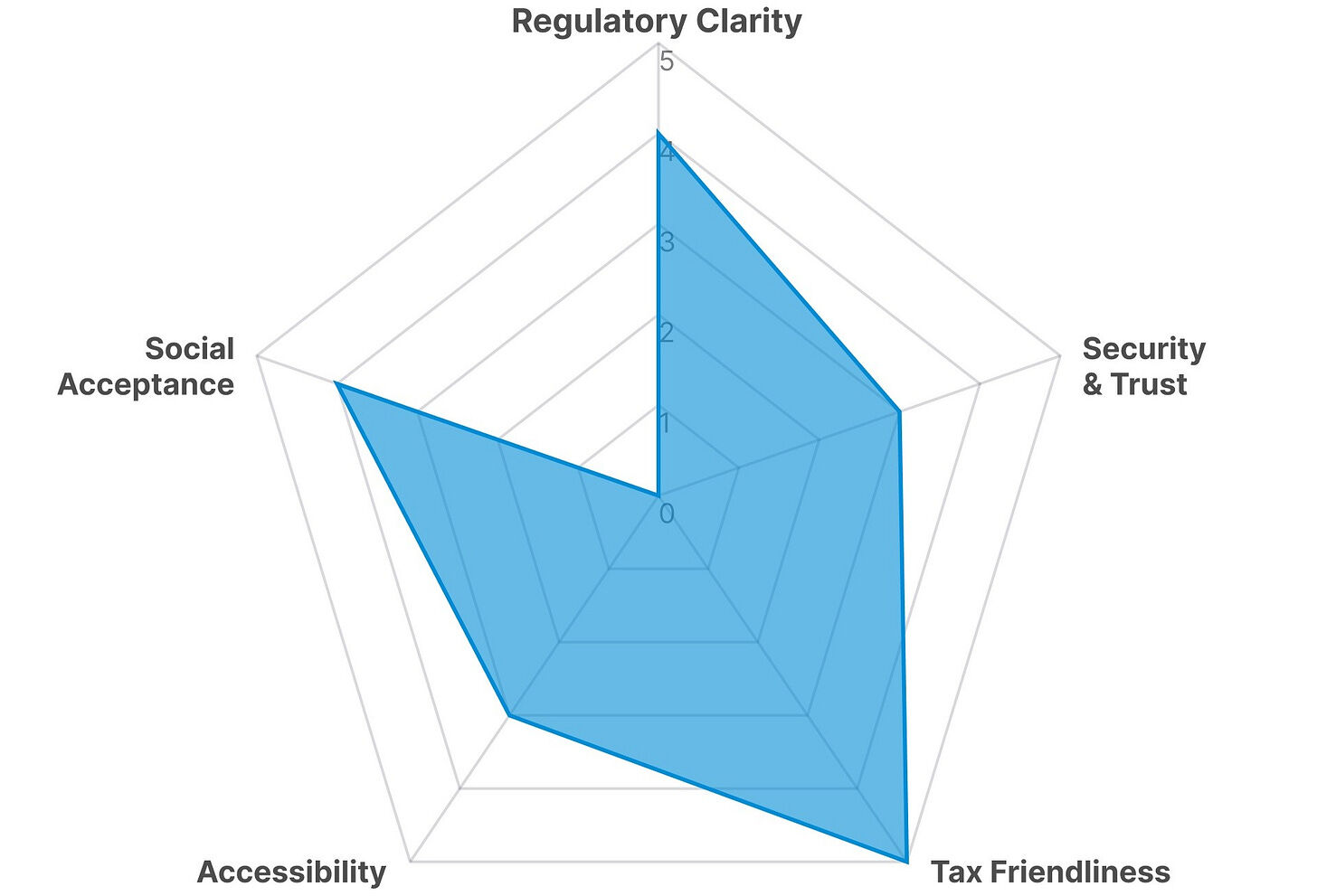

2.2.2. Thailand: Government-Led Market Opening

Thailand's Retail Crypto Investment Environment: Five Key Indicators

In Asia, Thailand is the market where the government most directly signals "it's okay to enter."

In January 2025, the government announced a five-year personal income tax exemption for crypto trading profits made through licensed exchanges. In the same month, the government allowed public and private funds to invest in crypto. Since then, the government has further reduced taxes, opened institutional capital channels, and issued digital assets.

Thailand's crypto user base is about 13 million, roughly 18% of the population. The Emergency Decree on Digital Asset Business enacted in 2018 established a legal framework early in Asia, and the Securities and Exchange Commission (SEC) has licensed 9 exchanges. THB-denominated stablecoin trading volume reached $9.4 billion, second only to KRW in the Asia-Pacific region. This is no longer just permission; it's active promotion.

Regulatory enforcement is a two-pronged strategy. In April 2025, the offshore regulator blocked 5 unauthorized foreign platforms including Bybit and OKX. In July of the same year, it allowed securities companies to offer investment token services and opened public consultation on crypto derivatives. The strategy is: crack down on the illegal, expand the legal.

The government also plays a significant role in shaping social perception. Former Prime Minister Thaksin Shinawatra publicly emphasized the need for crypto regulation and gave positive remarks on the crypto payment pilot in Phuket. The resulting perception is: "If the government exempts it from tax, it must be acceptable." Opening brokerage channels, allowing existing stock investors to invest in crypto through familiar avenues, also helps drive crypto conversion.

One key element is missing: payments. Using crypto as a payment method has been prohibited since 2022. The TouristDigiPay sandbox allows foreign tourists to exchange crypto for THB, and the Bank of Thailand runs a separate THB stablecoin sandbox. But Thai consumers still lack daily crypto payment experiences.

Thailand's most notable feature is that the government is removing barriers to crypto from the top down: tax exemptions, issuing G-Token, opening institutional channels, introducing derivatives. Such proactive government action is rare in Asia. The next task is how to transform crypto from a "trading asset" to a "consumption asset." Lifting the payment ban could be the next major turning point for crypto in Thailand.

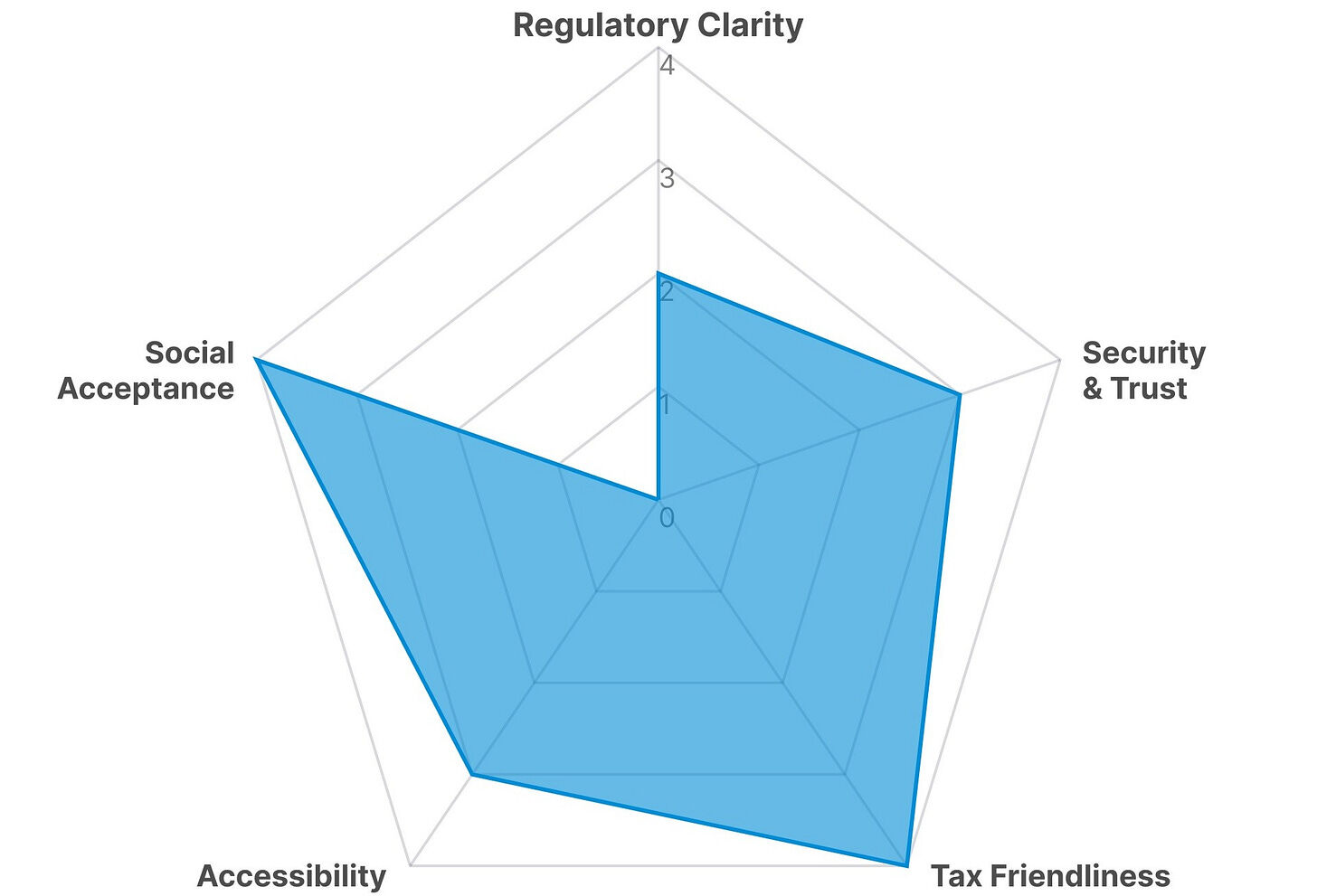

2.2.3. Indonesia: From Commodity to Financial Asset

Indonesia's Retail Crypto Investment Environment: Five Key Indicators

In January 2025, Indonesia changed the nature of crypto. Regulatory authority was transferred from the Commodity Futures Trading Regulatory Agency (Bappebti) to the Financial Services Authority (OJK), and crypto's classification changed from "commodity" to "digital financial asset." This is not a simple jurisdictional change. OJK regulates banks, insurance, securities, and pension funds. Crypto's status has been elevated to the same level as stocks and bonds.

The listing structure has changed from exchange discretion to a central exchange (Bourse) determining a list of crypto assets eligible for listing. Additionally, measures such as mandatory security personnel, prohibition of using loans as funding sources, and enhanced consumer and data protection obligations have been introduced. While regulation has tightened, it also signals that crypto is now a "government-recognized financial product."

Uncertainty during the transition period is inevitable. The transition period lasts until January 2027, during which regulatory interpretation gaps may appear. Similar to Thailand, using it as a payment method is prohibited due to currency law stipulating the Rupiah as the sole legal tender.

Indonesia's potential