Trade Everything, Never Close: RWA Perpetual Contracts — The Final Piece for DeFi to Devour Wall Street (Part 2)

- Core Viewpoint: This article provides an in-depth analysis of the RWA perpetual contracts sector. It focuses on the order book model represented by the Hyperliquid HIP-3 ecosystem and its architectural differences from the liquidity pool model. It points out that strict US regulatory constraints (dual jurisdiction by the SEC and CFTC) currently force this field to rely primarily on offshore markets (Regulation S exemption) and partnerships with traditional brokers for growth, while simultaneously facing long-term challenges and opportunities presented by the New York Stock Exchange's (NYSE) plan to launch 24/7 trading.

- Key Elements:

- Architectural Game: The order book model (e.g., Hyperliquid) is market-driven for pricing, with oracles used only for risk control; the liquidity pool model (e.g., Ostium) uses oracles for direct pricing. Each involves trade-offs between usability and risk control.

- Core Case Study: Hyperliquid transformed into a high-performance clearing and matching infrastructure layer through its HIP-3 upgrade. Its ecosystem projects (e.g., Trade.xyz) dominate the trading volume in RWA perpetual contracts.

- Regulatory Barrier: In the US, perpetual contracts involving single stocks or narrow-based indices require dual licenses from both the SEC and CFTC, creating an extremely high compliance barrier that essentially acts as a de facto entry ban.

- Offshore Opportunity: The current main growth window lies in offshore markets, utilizing the Regulation S exemption and partnering with traditional CFD brokers. These brokers handle front-end customer acquisition and compliance, while the DEX serves as the back-end clearing engine.

- External Challenge: The New York Stock Exchange's plan to launch 24/7 trading could erode DeFi's monopoly advantage in "round-the-clock trading," forcing RWA projects to seek differentiation in areas like leverage ratios and permissionless access.

- Future Positioning: RWA perpetual contracts aim to provide a transparent, linear on-chain alternative for global leverage demand. In the long term, they may evolve into an efficient execution layer built on top of regulated traditional spot markets.

In the third section of the "Part One" article, we focused on analyzing projects like Synthetix, Gains Network, and Ostium. This article will continue from the previous one, expanding further to other representative cases.

III. Representative Projects and Architectural Trade-offs: Oracle Pricing + Liquidity Pool (Pool-based + Oracle pricing) vs. Order Book

3.3 Orderbook Representative: Hyperliquid HIP-3 Ecosystem

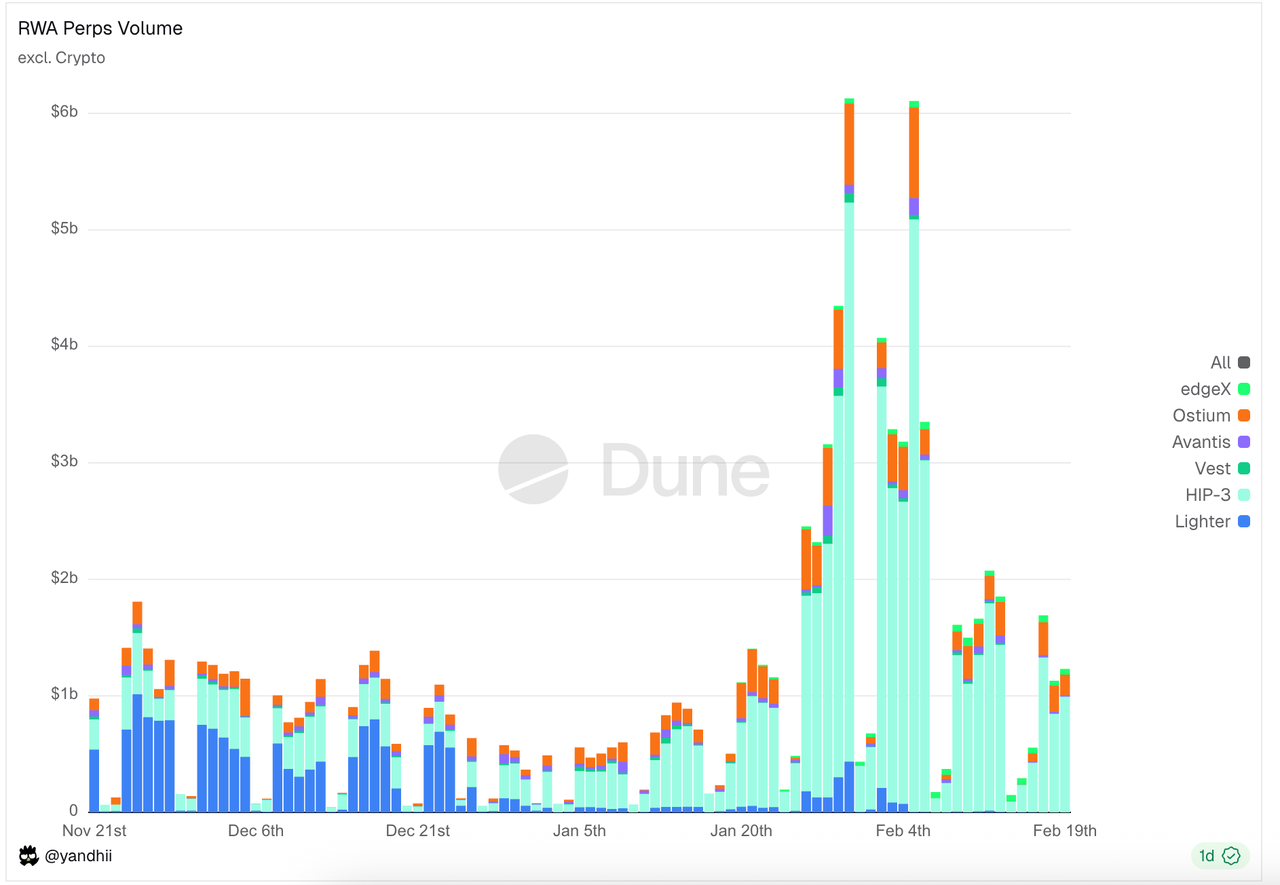

In the order book (Orderbook) track, the Hyperliquid HIP-3 ecosystem occupies the vast majority of trading volume and open interest. Outside the Hyperliquid ecosystem, platforms like Lighter and Vest Markets are also competing.

Data Source: https://dune.com/yandhii/rwa-perps

Hyperliquid & HIP-3: Decentralized Nasdaq Infrastructure

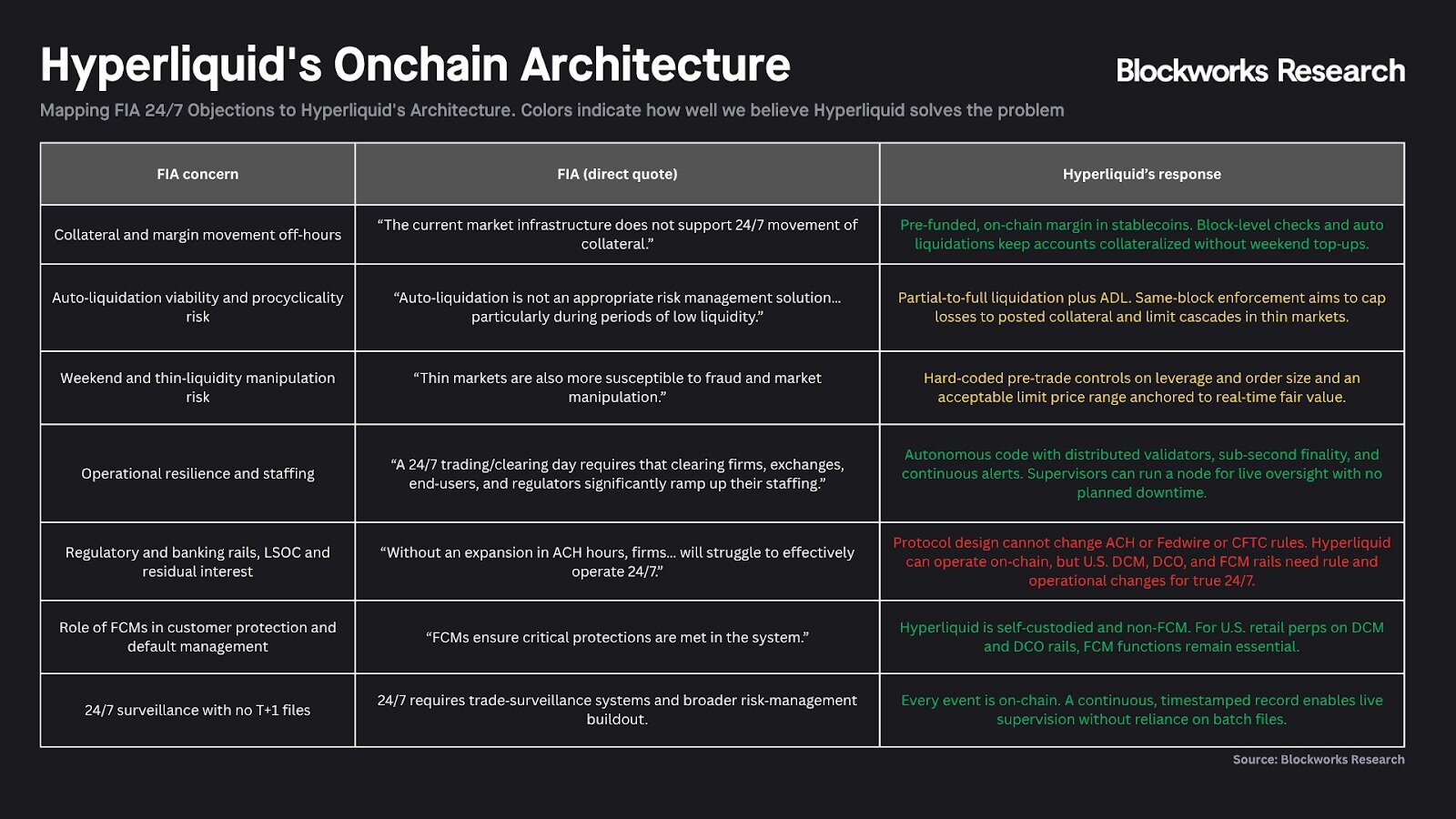

Through the HIP-3 upgrade, Hyperliquid has completed its strategic transformation from a single perpetual contract exchange to a "high-performance clearing and matching infrastructure layer." Its core vision is to split the functions of DCM (Designated Contract Market) and DCO (Derivatives Clearing Organization) from traditional finance on-chain. Under this architecture, the Hyperliquid chain itself plays the role of a unified DCO, providing the underlying matching engine, risk control, and fund settlement; while third-party teams act as "Deployers," taking on the DCM role, responsible for front-end customer acquisition, market operations, and asset listing. This layered design aims to create a "decentralized Nasdaq," carrying perpetual trading for various assets through a unified settlement layer.

Figure: The above summarizes Hyperliquid's aspiration to become "a more open, transparent, and efficient financial system" in response to the CFTC's skepticism about perpetual contracts and 24/7 trading. For example: Replacing traditional DCO reliance on the banking system with 24/7 automated clearing protocols, eliminating bloated FCM intermediaries through non-custodial technology, and reconstructing DCM regulatory logic using real-time on-chain data illustrate how blockchain technology can directly overcome the physical time differences and efficiency bottlenecks of traditional finance.

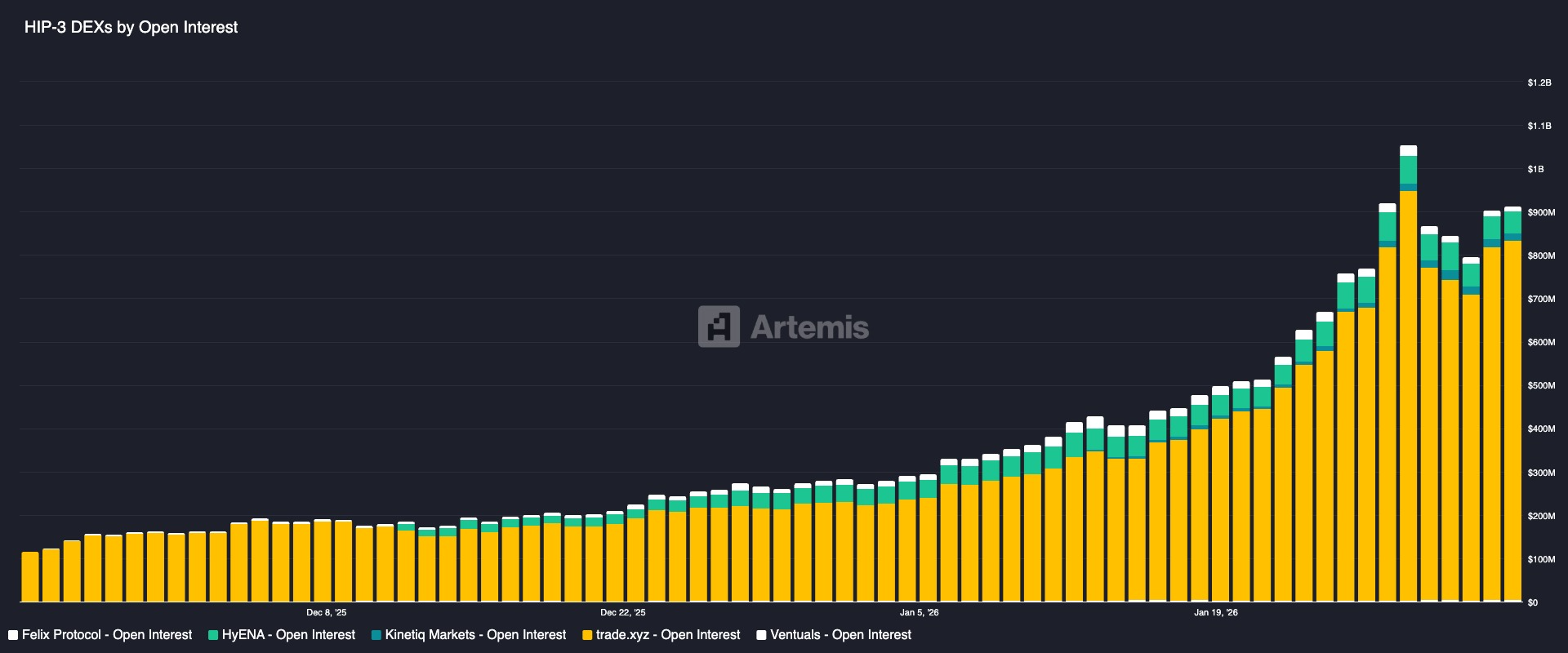

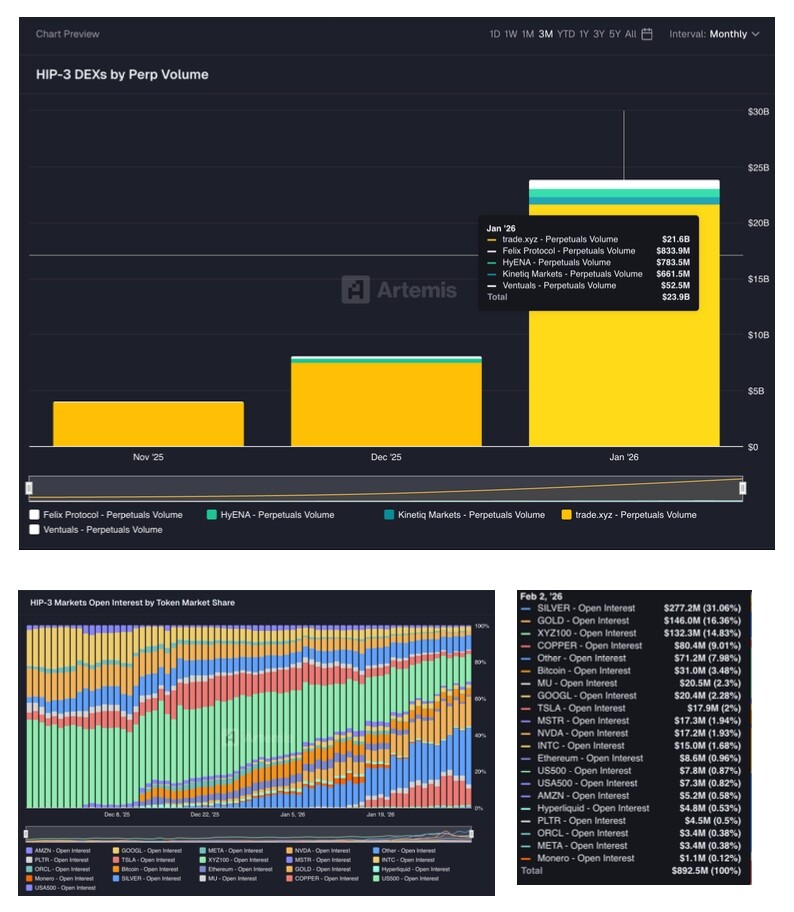

HIP-3 Ecosystem RWA Perps Projects

Project Overview

- Trade.xyz was built by HyperUnit, an asset layer team officially partnered with Hyperliquid. It was the first to launch the XYZ100 perpetual contract tracking the Nasdaq 100 index and several leading US tech stocks. With rich asset bridging (supporting cross-chain liquidity injection for mainstream assets like BTC, ETH, SOL via HyperUnit), Trade.xyz currently leads in trading volume among all HIP-3 perpetual exchanges, contributing about 90% of the market's trading volume.

- Markets.xyz is an RWA Perps Dex launched by the team behind Kinetiq, a Liquid Staking project on Hyperliquid. Markets has a slightly different positioning from Trade: it focuses on indices and has launched various index/macro perpetual contracts (covering S&P 500, US tech indices, Euro, US Treasury indices, energy indices, etc.). Another differentiator is its use of USDH as the margin quote currency, significantly reducing trading fees and increasing rebates to compete with Trade on cost advantage (USDH is a Hyperliquid-native stablecoin issued by the Native Markets team, which has implemented fee waivers and rebate campaigns in distribution to compete with the asset cross-chain project Unit).

- Felix started as a lending and stablecoin protocol on Hyperliquid, issuing the synthetic dollar feUSD via CDP and providing the "Felix Vanilla" matching lending market. After the launch of HIP-3, Felix expanded its business scope, becoming one of the HIP-3 perpetual market deployers. Felix's settlement currency also uses the USDH stablecoin.

- Dreamcash is a mobile-focused product incubated and developed by Beam, positioning itself as a mobile trading terminal for RWA perpetual contracts.

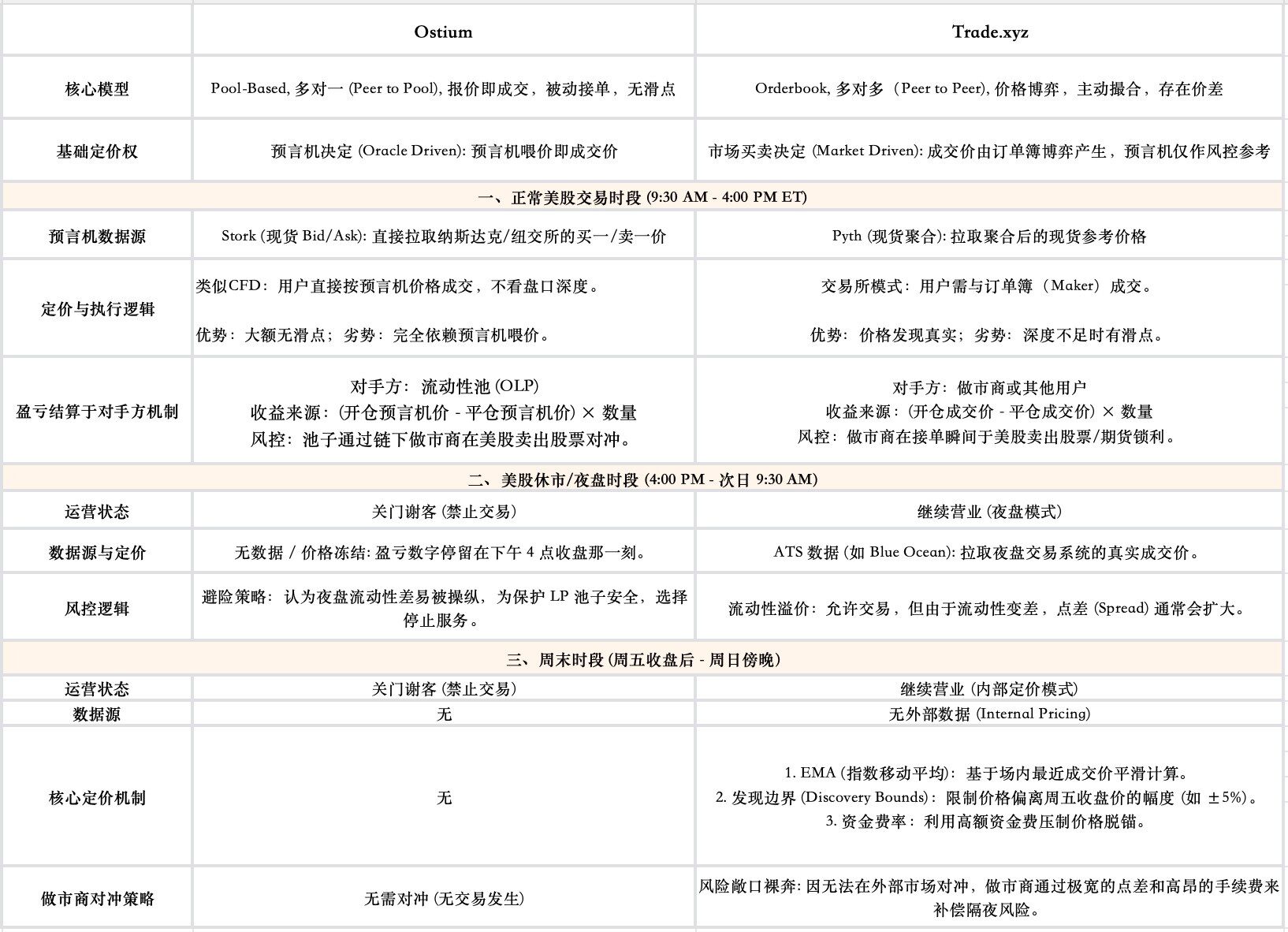

Core Pricing Mechanism: Market-Driven Pricing + Oracle Risk Control

For 24/7 RWA Perps projects built on the Orderbook model, the core technical challenge is how to provide a fair and robust price when the underlying asset's market is closed. Taking Trade, the leading project in the HIP-3 ecosystem in this field, as an example, its core design lies in a dual-track mechanism of market pricing and oracle risk control.

- The Core of Price Discovery: Determined by the Market, Not the Oracle

Unlike Pool-based models that directly use oracle quotes as transaction prices, Trade's transaction price is entirely generated by the博弈 between buyers and sellers on its order book. The oracle here does not play the role of a "price setter" but rather a "referee," with its provided prices mainly used for risk control.

- Mark Price: Used to Calculate User Position P&L and Determine Liquidations

The system's profit/loss calculation, funding rate, and forced liquidation do not use the instantaneous transaction price but rely on a more robust mark price. Trade's mark price is generated by taking the median of the following three components: oracle price, long-term deviation mean, and immediate order book price. This design aims to smooth market noise and prevent malicious manipulation, ensuring users' accounts are not incorrectly liquidated due to flash crashes on the order book.

- Oracle Data Source Switching for 24/7 Operation: To achieve 24/7 operation, the oracle's data source seamlessly switches based on US stock trading hours: referencing external oracles like Pyth during normal trading hours; referencing night session transaction prices provided by ATS (Alternative Trading Systems, like Blue Ocean) during night sessions; and activating internal pricing mode during weekend market closures.

3.4 Ostium vs. Trade: Pricing Logic and Oracle Role Comparison

Ostium chose stronger security and price accuracy, sacrificing some usability (unavailable on weekends). Trade chose usability and博弈性, sacrificing some price stability (may depeg or have high funding rate volatility on weekends). The role of the oracle also differs significantly between the two project models. In Ostium's Pool-based model, the oracle is the price setter (determining transactions), while in Trade, the oracle is the referee (only influencing funding rates and responsible for determining liquidations, not how transactions occur).

Chapter IV: Analysis of Regulatory Constraints on RWA Perps

4.1 Core Logic of US Derivatives Regulation: Underlying Asset Classification Determines Compliance Path

In the US financial regulatory system, the first step in determining whether a derivative can be listed and how is to ascertain the legal nature of its underlying asset. This directly determines the jurisdiction of regulatory authority and, consequently, the type of license the exchange must obtain.

For assets like gold, silver, foreign exchange (FX), and Bitcoin, US law defines them as "commodities." Perpetual contracts based on such assets fall under the category of commodity futures, and their regulatory path is relatively singular and clear: they fall entirely under the jurisdiction of the Commodity Futures Trading Commission (CFTC). Exchanges only need to register as a Designated Contract Market (DCM) and connect to a Derivatives Clearing Organization (DCO) to conduct business.

However, once the underlying asset of a perpetual contract becomes a single stock or a narrow-based security index, the situation changes fundamentally: Derivatives involving single securities or combinations of a few securities must be jointly regulated by both the SEC and the CFTC.

The requirement for simultaneous joint regulation by the SEC and the CFTC is the primary reason why there are currently no compliant stock perpetual contracts in the US market. The background of this regulation dates back to a regulatory turf war between the SEC and the CFTC in the 1980s: at that time, the SEC and CFTC fought over regulatory authority for the emerging stock futures contract products. The final resolution to this dispute was the Shad-Johnson Agreement signed by both parties in 1982, which, in an almost "one-size-fits-all" manner, directly prohibited the trading of single-stock futures and narrow-based stock index futures on US exchanges. The original intention of the ban was to avoid continued friction between the agencies. Although the Commodity Futures Modernization Act (CFMA) of 2000 amended this ban, allowing such contracts to be traded in the market in the form of "Security Futures Products," the attached conditions were extremely stringent: the product must be subject to dual regulation by both the SEC and the CFTC. This became the fundamental legal obstacle hindering innovation in equity-based derivatives.

Any platform wishing to offer stock perpetual contracts to US retail clients cannot hold just a single license but must simultaneously complete the following two registrations:

- Register with the CFTC as a Designated Contract Market (DCM) or a Swap Execution Facility (SEF)

- Register with the SEC as a National Securities Exchange

This means the platform must simultaneously meet two sets of compliance standards formulated by different agencies, which may conflict in areas such as margin calculation, information disclosure, and trade reporting. This extremely high compliance threshold and operational cost essentially constitute an "entry ban" for single-stock perpetual contracts, resulting in the near absence of such compliant retail products in the US today.

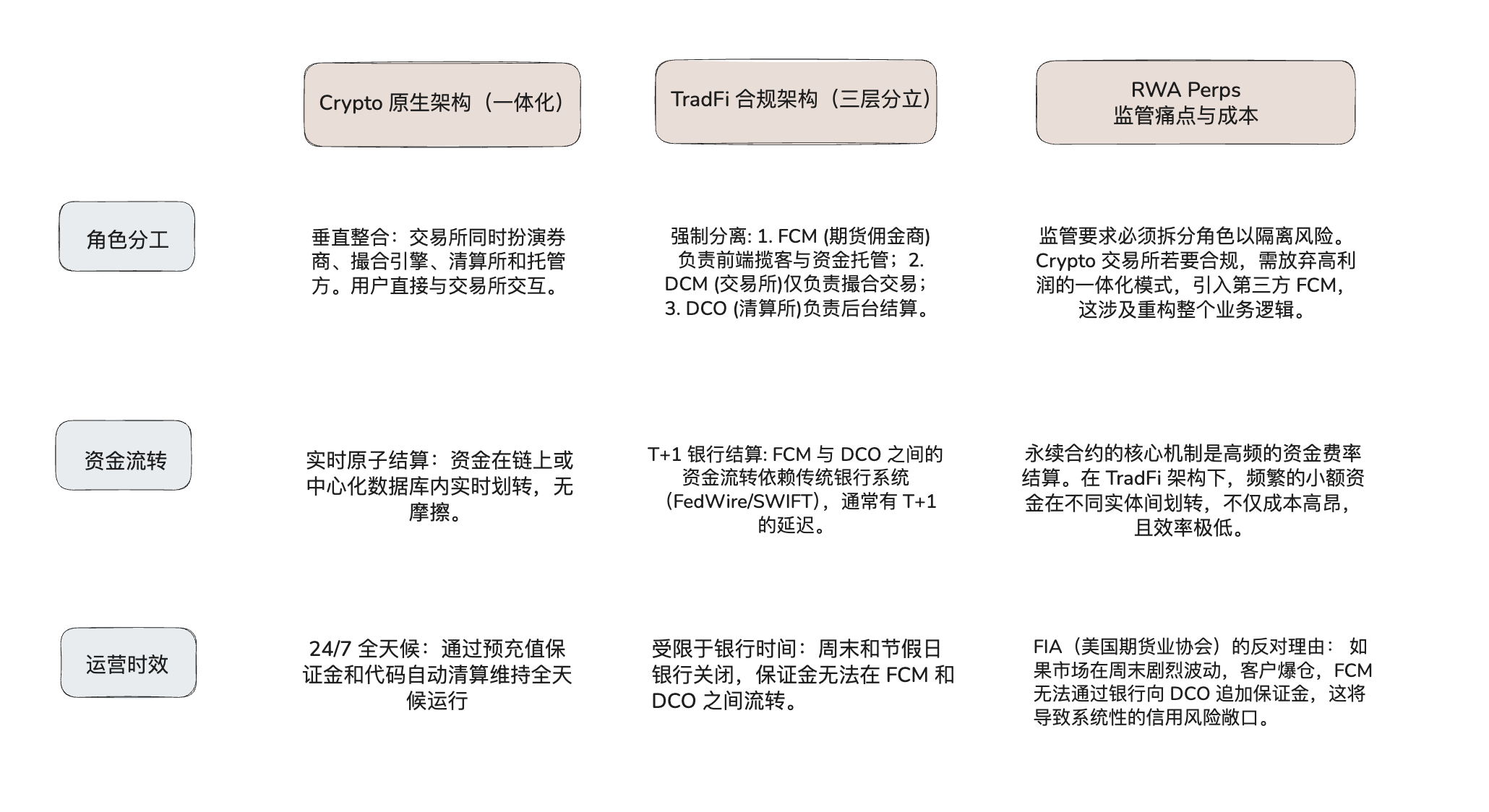

4.2 Conflict in Exchange Architecture: Why Compliance Migration Costs Are Extremely High

If US exchanges like Coinbase or Robinhood truly want to launch Equity Perps products, in addition to facing the difficulty of obtaining the aforementioned legal licenses, they must also confront conflicts in their underlying infrastructure architecture.

Cryptocurrency exchanges commonly adopt a "vertically integrated" monolithic architecture, while US regulations require a "three-tier separation" architecture based on risk isolation. If crypto exchanges want to be compliant, they must dismantle their existing efficient tech stack to adapt to traditional finance's clearing processes.

Comparative Analysis of Crypto and TradFi Market Architectures:

Therefore, for US exchanges to launch Equity Perps, they not only need to solve the legal issue of "dual licensing" but also need to resolve the physical contradiction between "24/7 trading demand" and the "non-24/7 banking settlement system." This infrastructure mismatch is currently the biggest sticking point.

4.3 Window of Opportunity for Offshore Markets: Regulation S

Due to the difficulty of breaking through domestic US regulatory restrictions in the short term, the vast majority of stock perpetual contract liquidity has been squeezed into offshore markets. Offshore exchanges (serving non-US clients) typically rely on the Regulation S exemption under US securities law for compliance. The core logic of this regulation is: as long as the issuance and sale of the security product occur entirely outside the United States, and the issuer does not engage in directed selling efforts targeting US persons, registration with the SEC is not required. This requires platforms to technically implement strict geofencing to block US IPs and explicitly prohibit US users in their legal terms.

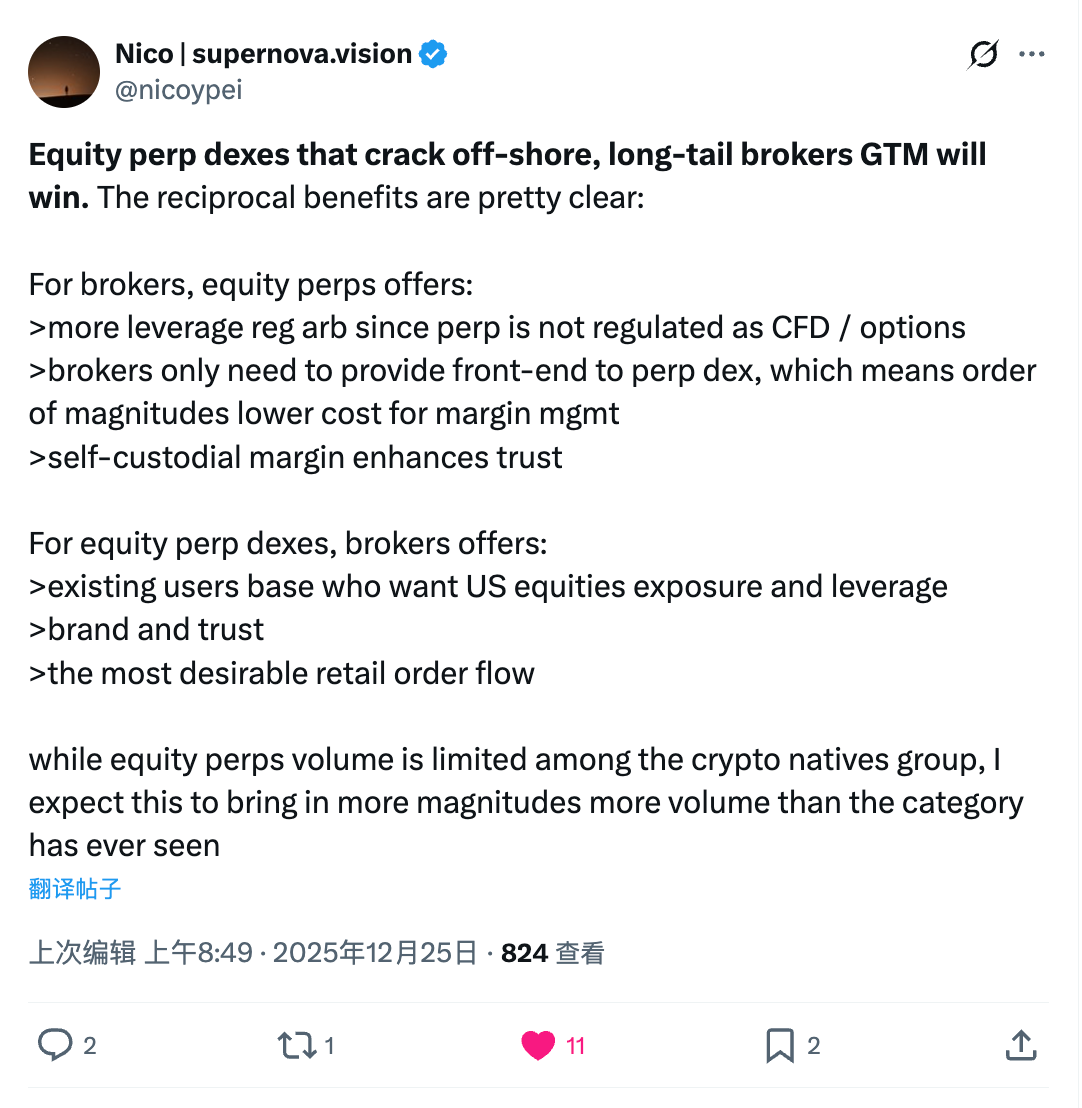

Against this backdrop, RWA Perps Dexes are facing a unique market window of opportunity. They have the chance to establish a mutually beneficial commercial distribution model by partnering with traditional long-tail brokers in offshore regions:

Mutually Beneficial Model: CFD Broker + RWA Perps Dex: This type of cooperation could be attractive to traditional brokers. Compared to traditional CFD businesses facing increasingly tight regulation (e.g., EU ESMA leverage restrictions), on-chain perpetual contracts often fall into regulatory gray areas and can offer higher leverage. More importantly, brokers only need to maintain front-end user relationships, outsourcing the complex margin management, clearing, and hedging risks to the on-chain protocol (back-end), which would significantly reduce their middle and back-office operational costs. Simultaneously, the DEX's self-custody nature solves the user trust issue regarding fund misappropriation by small and medium-sized brokers.

For Equity Perps Dexes, this model solves the most棘手 customer acquisition problem. Crypto-native users have relatively limited interest in US stock trading, while traditional brokers hold a large amount of real retail流量 seeking US stock exposure. By embedding themselves as a technological back-end into brokers, DEXes can maintain technological neutrality while having compliant brokers handle KYC/AML processes on the front end, potentially breaking through the original DeFi world to achieve scaled growth.

4.4 Potential Legal Risks

Although offshore and DeFi models are commercially viable, one must also be vigilant of the "long-arm jurisdiction" risk from US regulators. If offshore protocols cannot completely切断 ties with US users at the technical and compliance levels (e.g., through front-end screening or IP blocking), or if their business activities are deemed to involve the US market, they could still face severe regulatory penalties.

Chapter V: External Variable: The Dual Impact of NYSE's 24/7 Plan

The news that ICE, the parent company of the New York Stock Exchange (NYSE), plans to launch a 7x24-hour trading market constitutes the biggest external variable for the RWA perpetual contract赛道. If this change materializes, it will have profound dual impacts on DeFi. If users can legally and safely trade Tesla stock 7x24 on a regulated platform like the NYSE or Interactive Brokers, the "24/7 trading" advantage that DeFi protocols rely on for survival could be somewhat diminished. At that point, DeFi may need to find new value propositions, such as higher leverage, permissionless access mechanisms, or complex financial products built on composability, to survive in direct competition with traditional financial giants.

Core Motivation and Mechanism Innovation: From "T+2" to "On-Chain 24/7"

The 24/7 trading platform planned by the NYSE aims to utilize blockchain technology to achieve tokenized trading of US stocks and ETFs. Its core innovation lies in using stablecoin deposits, instant clearing and settlement (T+0), and multi-chain custody to彻底打破 the traditional stock market's弊端 of "separation of trading and settlement," eliminating settlement risks exposed in events like GameStop. This move is a strategic defense by the NYSE against competition from peers like Nasdaq and to meet global capital's demand for 24/7 liquidity. It marks traditional exchanges evolving from "electronic order books" to "fully on-chain infrastructure," attempting to融合 DeFi's efficiency advantages under the highest regulatory standards.

Catalysis and Challenge for the RWA Ecosystem: The End of the Liquidity Bottleneck

NYSE's entry provides顶级背书 for RWA tokenization, solving the "liquidity drought" and "pricing断层" caused by traditional market weekend closures for on-chain assets. For the RWA perpetual contract market, 24/7现货 price feeds will significantly reduce arbitrage costs and funding rate volatility, improving market depth. Although NYSE's compliant "walled garden" model may squeeze the生存空间 of some non-compliant, synthetic asset-type projects, it also指明了方向 for compliant stablecoins and clearing facilities. Crypto-native RWA projects need to utilize the window period before the 2026落地 to form complementary or competitive positions with traditional giants through differentiated positioning (e.g., high leverage, no门槛, cross-protocol interoperability).

Future Landscape Outlook: Deep Integration of Traditional and Crypto Finance

Although the crypto community has争议 regarding the investment pressure and regulatory monitoring brought by "24/7全天候盯盘," financial上链 has become an irreversible trend. In the medium to long term, the介入 of traditional giants will reshape the value chain, forcing intermediaries like brokers and custodians to transform. The future market will evolve into a competitive and coexisting ecosystem: compliant platforms like the NYSE will provide highly credible underlying现货 liquidity, while DeFi protocols will continue to leverage flexibility in innovative derivatives and global asset allocation. As the boundaries between crypto and traditional assets blur, the global capital market will enter a new era driven by AI, real-time pricing, and atomic settlement.

Conclusion

- Structural Upgrade in Delta One