Conversation with Tom Lee and the Author of "The Big Short": The Crypto Bear Market is Wall Street's Prelude to "Seizing Power"

- Core Viewpoint: This conversation explores the current market dynamics, potential risks, and opportunities under the AI boom. It argues that while AI is revolutionary, market returns are not guaranteed, and analyzes retail investor behavior, the current state of gold and cryptocurrency markets, and future challenges.

- Key Elements:

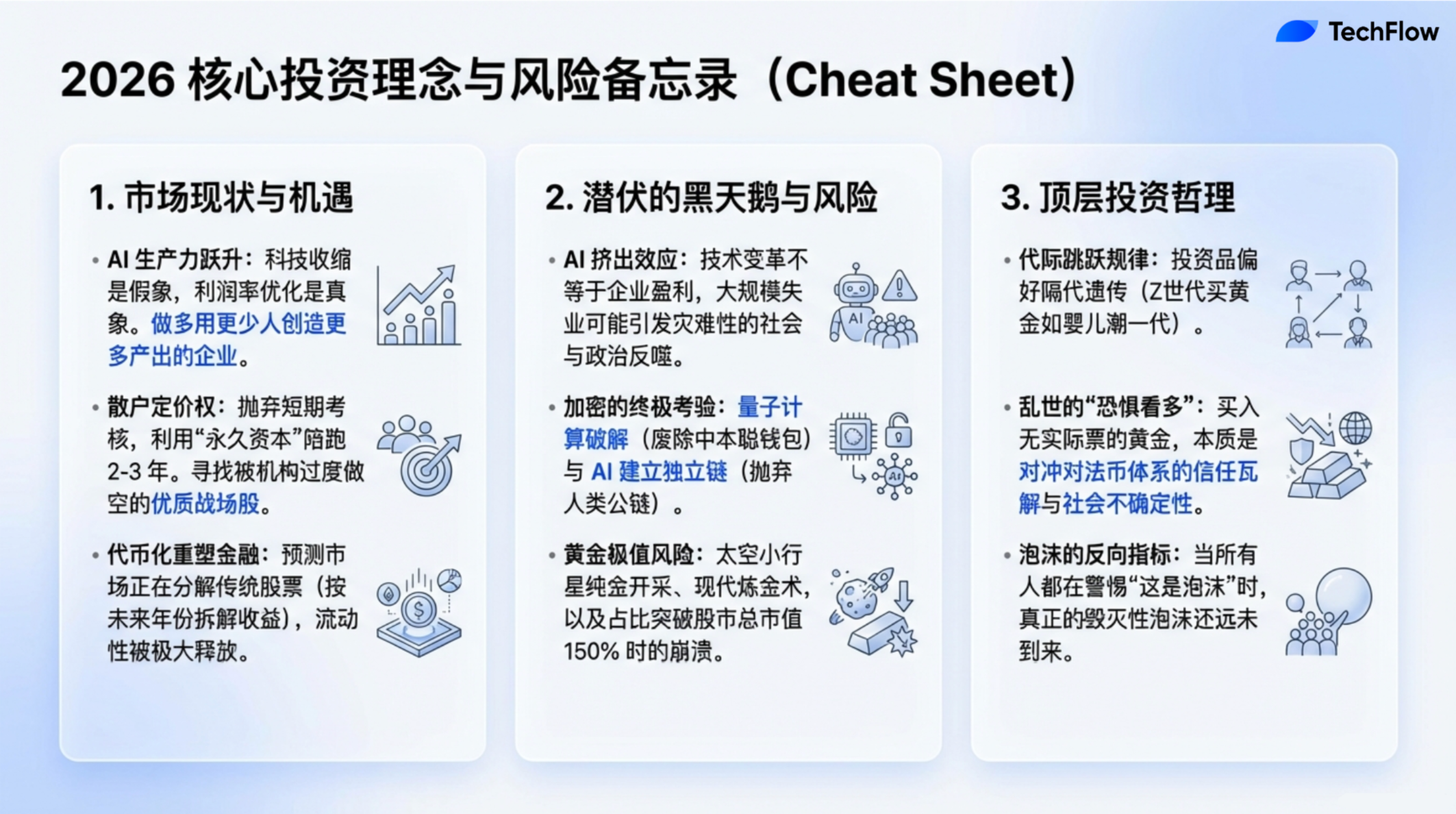

- AI-driven productivity gains may lead to short-term job losses and reduced demand for software stocks, but this is seen as a signal of economic efficiency optimization rather than purely negative.

- Real market bubbles often form when no one questions them; the widespread discussion about an AI bubble today may indicate the peak has not yet been reached.

- Retail investors, using "permanent capital" and free from short-term performance pressure, have outperformed institutional investors pursuing high-frequency trading in recent years with their long-term holding strategies.

- Gold, as a "fear" hedge, has a market capitalization approaching that of the stock market, but faces "black swan" risks such as breakthroughs in mining technology, space resources, or alchemy.

- Cryptocurrency is experiencing a "storm" rather than a "winter," with the narrative shifting towards institutional assets, but it faces substantive threats like quantum computing cracking encryption algorithms.

- While innovative, new speculative forms like prediction markets and sports betting may bring social problems such as corroding sportsmanship and inducing youth gambling.

- If a key AI company collapses, the U.S. government might intervene or even nationalize it due to national competition considerations, rather than leaving it to market forces.

Compiled by: TechFlow

Guests: Tom Lee, Co-founder and Head of Research at Fundstrat; Michael Lewis, Author of "Moneyball," "The Big Short," "The Blind Side," and "Going Infinite"

Host: Liz Thomas, Head of Investment Strategy at SoFi

Podcast Source: SoFi

Original Title: AI Boom or Bubble? Michael Lewis, Tom Lee on the Risks and Rewards | The Important Part LIVE

Release Date: February 19, 2026

Key Takeaways

In a special live recording of "The Important Part," SoFi's Head of Investment Strategy, Liz Thomas, posed a question on many investors' minds: Will the market's rapid ascent slow down? Or will this rally continue? To explore these questions, she invited two leading thinkers in finance: Tom Lee, Co-founder and Head of Research at Fundstrat, and Michael Lewis, author of the New York Times bestsellers "Moneyball," "The Big Short," "The Blind Side," and "Going Infinite." The trio delved into the core issues facing investors in 2026.

In this captivating conversation, they analyzed several hot topics in the current market: Why have retail investors outperformed hedge funds in recent years? Has gold peaked? Does Bitcoin's 40% plunge signal a "crypto winter"? Tom Lee explained that despite recent declines in AI-driven software stocks, this might actually reflect rising corporate productivity. Meanwhile, Michael Lewis shared his contrarian bet on gold and explained his strategy of "betting on fear."

They also explored other major issues in today's financial markets, including: Will the Federal Reserve's independence be threatened following Kevin Warsh's nomination as Chair? Will the rapid development of AI lead to massive job losses? And could the federal government potentially take over struggling AI companies?

Finally, they turned their attention to the cryptocurrency space, analyzing potential "black swan" events and the valuable lessons about technological disruption that can be learned from the history of the frozen food industry.

Highlights

- A true bubble only forms when everyone believes "this is definitely not a bubble."

- The unemployment rate for college graduates is even higher than for their non-college-educated peers... But viewed from another angle, this could actually be a signal of rising economic productivity. Productivity is typically measured by creating more output with fewer human resources.

- AI might truly be as revolutionary as everyone says, but that doesn't necessarily mean it will bring widespread profits to the stock market. There's no inherent causal link between a technology's transformative nature and market returns.

- Retail investors can pick the right stocks mainly because their incentives are completely different from institutional investors... They are investing their own money, so they are more willing to hold a stock for two to three years.

- When I hold gold, I'm essentially investing in "fear." I buy gold because it hedges against current uncertainties... I'm buying insurance against future unease and anxiety.

- Looking back, there have only been three times when gold rose more than 9% in a single day, and all three marked the peak of gold prices. If history is any guide, gold may have already peaked.

- There's a financial adage from the late Art Cashion: "Bull markets don't die of old age; they are killed by the Fed."

- Although the methods have changed, human nature hasn't. The instinct of "I want to make more money, faster than others" remains the core driving force of this industry.

- In the next decade, whoever controls AI and its related ecosystem could become the global superpower. If AI's funding chain really starts to break, I believe even the Department of Defense has already simulated how to respond to such a situation.

- Since 1974, about 40,000 companies have gone public or been spun off. Of these, 90% of the stocks have fallen more than 50%, and of those that fell over 50%, 90% eventually went to zero. In other words, most stocks ultimately become worthless.

AI: Crisis or Opportunity? The Duality of Productivity Transformation

Liz Young:

In recent years, global markets have experienced sustained rapid growth. Although there have been fluctuations in recent weeks, the overall trend remains strong. This phenomenon is largely attributed to the development of Artificial Intelligence (AI). AI has driven technological innovation, spawned new products, and brought in massive capital inflows. However, many investors are starting to feel uneasy, worrying whether the market is already overheated and whether development is too rapid. This sentiment of concern is spreading globally and is also the focus of our discussion today.

To better understand this phenomenon, we have invited Tom Lee, Co-founder and Head of Research at Fundstrat. He has long been optimistic about the market and is considered a representative of the "bullish" camp. Tom, why do you remain optimistic in the current environment?

Tom Lee:

There's a financial adage from the late Art Cashion, who said: "Bull markets don't die of old age; they are killed by the Fed." In other words, good performance in the stock market doesn't mean it can't continue to perform well. In fact, I believe we are approaching two important catalysts: First, the returns from AI are starting to materialize, and it is redefining winners and losers; second, a shift in Fed policy, which could bring new tailwinds to the market. Therefore, there are still many reasons this year for investors to continue buying stocks.

Liz Young:

Let's talk about recent market changes. Software stocks have fallen sharply, and the cryptocurrency market has also seen a significant correction. Does such market turbulence worry you? Does it shake your optimistic view of the market?

Tom Lee:

I think many people are paying attention to this phenomenon. Over the past two years, the development of AI has been like an unstoppable force, attracting massive investor attention and capital inflows. However, as you mentioned, something different has indeed happened this year. We've seen many stocks and sectors begin to contract. Taking the software industry as an example, it is currently facing declining demand and service repricing. At the same time, many research reports point out that Agentic AI and other AI technologies are gradually replacing traditional software solutions.

Furthermore, according to some reports, the number of jobs in the tech industry has decreased in the three years since ChatGPT was launched. More surprisingly, the current unemployment rate for college graduates is even higher than for their non-college-educated peers. This data looks like "bad news" and is precisely the focus of many headlines today. But viewed from another angle, this could actually be a signal of rising economic productivity. Productivity is typically measured by creating more output with fewer human resources.

From this perspective, the application of AI is demonstrating its potential to enhance productivity. For software companies serving businesses, if corporate spending on software decreases, this is actually a process of margin optimization. In other words, the efficiency gains from AI are gradually translating into actual profits. While these changes may bring short-term pain, in the long run, this is strong evidence of AI technology's productivity advantages.

Precursors of Market Overheating and Crash Risks

Liz Young: Michael, in your past works, you have repeatedly documented periods where markets went from sustained rallies to sudden crashes. Before each market crash, there were signals, such as excessive speculation or risk-taking. In the market cases you've studied, what are the common characteristics of excessive risk-taking? Do you think these signs exist in the current market as well?

Michael Lewis:

That's a very interesting question. Frankly, I've never been able to accurately predict the arrival of any market crash before it happened. My work is more like waiting until "the storm is almost over" and then "sorting through the wreckage." Looking back on my career, my first book, "Liar's Poker," documented the financial markets of the 1980s; later, I also wrote stories about the dot-com bubble and the 2008 financial crisis. But honestly, I never knew exactly when these events would happen. More importantly, I don't think anyone can truly accurately predict the timing of these crashes. There are always multiple possible interpretations in the market, and my personal investment strategy is to put money into index funds.

However, I have indeed found that after every market crash, there are always people who saw the problems beforehand, but interestingly, these people often cannot accurately predict the next crisis. For example, Michael Burry made the right call during the subprime mortgage crisis, but that doesn't mean all his future predictions will be correct. He mentioned on Twitter that he shorted Nvidia and Palantir, which also attracted widespread market attention. I've interviewed him; his logic is based on the capital expenditure cycle (i.e., the cycle of corporate investment in equipment, technology, etc.), believing that the valuations of these two companies have reached bubble highs. However, he also admits he cannot precisely predict the timing of a crash. Therefore, he chose a more conservative strategy—buying two-year put options. Put options have a low cost, so even if the judgment is wrong, the loss is limited. This strategy shows that even a visionary like Burry cannot fully grasp the market's short-term changes.

As for the common characteristics of excessive risk-taking you mentioned, I think the most prominent one is FOMO. Take my recent book "Going Infinite" as an example; it tells the story of Sam Bankman-Fried and FTX. The collapse of FTX is a classic case of FOMO. 180 venture capital firms rushed to invest in SBF without thorough investigation. They didn't even figure out what his business was really doing before pouring in huge amounts of money. This "act first, understand later" mentality is one of the hallmarks of excessive risk-taking.

Another common feature is distorted incentives. When I was writing "The Big Short," I interviewed some traders who made wrong decisions during the subprime crisis. They told me they engaged in high-risk investments because "everyone was doing it," and if they didn't follow the crowd, they would be seen as laggards. Additionally, they were tempted by huge bonuses; even if these investments ultimately failed, their bonuses wouldn't be clawed back. This flawed incentive structure led people to chase short-term gains even when they knew the risks.

If I were to venture a prediction, I think there are indeed some signs of a bubble in the current market. While AI is indeed a transformative technology, that doesn't mean everyone can profit from it. In fact, technological progress can sometimes even compress corporate profit margins. AI might truly be as revolutionary as everyone says, but that doesn't necessarily mean it will bring widespread profits to the stock market. There's no inherent causal link between a technology's transformative nature and market returns.

Why Retail Investors Are Outperforming Institutional Investors

Liz Young: Tom, I know you must have your own unique insights on this topic. I'd like you to talk about internet buzzwords like FOMO and HODL, which actually reflect the game between retail and institutions.

In this economic cycle, since the COVID pandemic, we've found that retail investors have repeatedly correctly predicted market direction, while institutional investors have, in some cases, appeared overly conservative. How do you think retail investors achieve this? Why are their judgments more accurate? Furthermore, in the current market environment, who do you think has the upper hand, retail or institutions?

Tom Lee:

At Fundstrat, our clients are mainly divided into two categories. One is our institutional research clients, including about 400 hedge funds; the other is family offices, investment advisors, and high-net-worth individuals served through FS Insight. We survey these clients every month on their top five most favored and least favored stocks. Since 2019, we've been conducting this analysis, and the results are very interesting: Retail choices are often correct; the top five stocks most favored by retail investors have performed exceptionally well. We are even considering turning this data into an investment product.

I think retail investors can pick the right stocks mainly because their incentives are completely different from institutional investors. Retail investment behavior doesn't directly affect their livelihood based on daily or weekly gains and losses. They are investing their own money, so-called "permanent capital" (i.e., investment capital available long-term), so they are more willing to hold a stock for two to three years.

When I first entered the industry, the typical holding period for institutional investors was one year, which was considered "long-term investing." But now, most institutions' holding periods have shortened to 30 days or less. Data shows the average holding time for a single stock is only about 40 seconds; some hedge funds even consider holding for 1 second or 5 seconds as "long-term holding." This high-frequency trading model dictates that institutional investors can only choose stocks with extremely high liquidity that can generate returns quickly, while retail investors tend to discover investment opportunities with long-term growth potential.

Liz Young: But don't you think this could trigger more FOMO? If retail choices are correct, won't institutions be forced to chase higher prices to catch up? Couldn't this make the market even more overheated?

Tom Lee:

That can indeed happen. There are usually some hot stocks in the market that are both favored by retail investors and heavily shorted by institutions. For example, Palantir is a classic battleground stock. Another example is Netflix in the mid-2000s when its stock price was only $2 to $4, later rising to $20. At that time, Netflix was heavily shorted by many institutional investors, but retail investors kept buying firmly. Another well-known example is GameStop. Stocks like Palantir and Tesla have also been typical "battleground stocks." Retail investors see the long-term potential of these stocks, while institutions tend to use them as tools for short-term arbitrage. When the price of these stocks reaches a certain critical point, their valuation gets reassessed, and the stock price can skyrocket rapidly. For example, in 2017, after Tesla was included in the Russell 1000 index, its stock price experienced a similar surge.

Michael Lewis: Can I ask a question? You mentioned a very interesting idea: you plan to develop an investment product based on retail investment choices?

Tom Lee:

We have collected 60 months of relevant data, recording the stocks most favored and least favored by retail investors. Additionally, we specifically focus on those "battleground stocks" that are favored by retail but shorted by institutions. We are planning to launch an ETF that will automatically buy the stocks retail investors consider most promising each month. You can think of it as a "professionally validated WallStreetBets." Unlike random discussions on Reddit, our data comes from paying users, our actual clients, reflecting real investment ideas. More importantly