Navigating the Bear Market: A Guide to Identifying True "Cash Flow" Tokens

- Core Thesis: Through rigorous screening of a vast number of tokens, research reveals that very few assets in the current crypto market genuinely create sustainable cash flow for holders and possess investment value. Furthermore, yield is highly concentrated in a handful of projects, leading the author to conclude that Bitcoin (BTC) offers a superior risk-reward ratio.

- Key Findings:

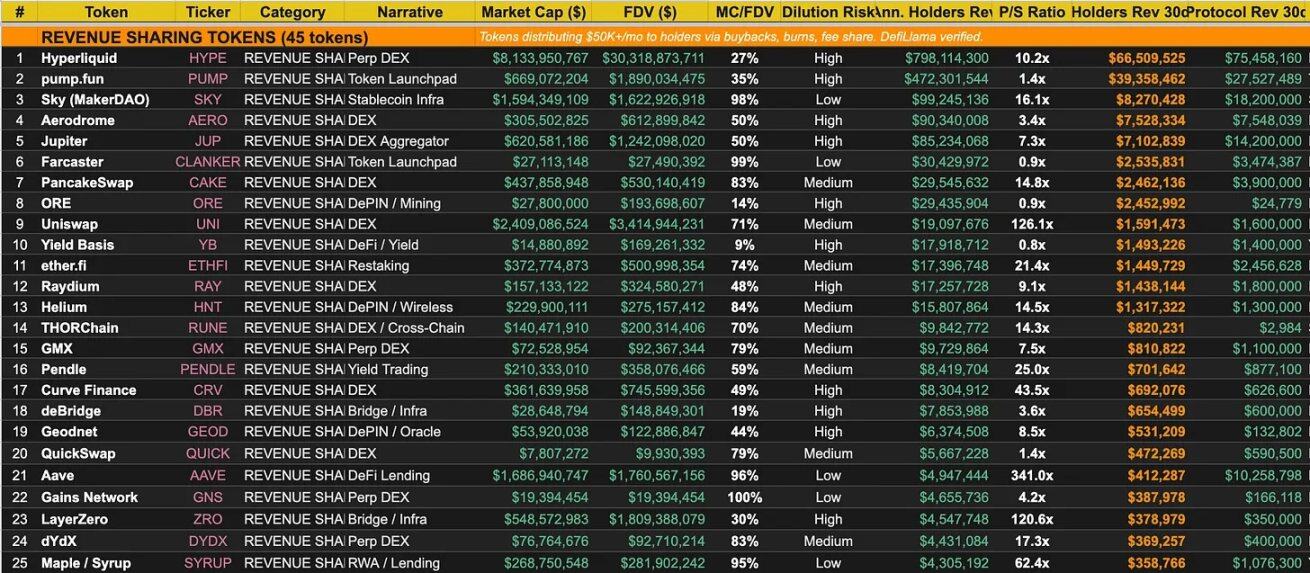

- Out of 17,148 tokens, only 132 were identified as "investable assets." Among these, merely 45 provide holders with significant yield, with a total annualized sum of approximately $1.8 billion.

- Yield distribution is highly concentrated, with just two projects—Hyperliquid and Pump.fun—contributing 69% of all holder yield.

- Some projects exhibit extremely low Price-to-Sales (P/S) ratios, such as Pump.fun (1.4x) and Aerodrome (3.4x), far below those of Uniswap (121x) and Aave (341x).

- There exists a group of projects with protocol revenue that do not yet distribute it to holders (e.g., Lido, CoW Protocol). Their potential future initiation of dividends represents a latent investment opportunity.

- Exchange tokens (e.g., BNB, LEO) and major L1 public chains (BTC, ETH) are viewed as lower-risk choices for navigating bear markets due to their liquidity and resilience.

Original Author: Ignas | DeFi Research

Original Compilation: Saoirse, Foresight News

CoinGecko tracks 17,148 tokens.

But in the current crypto market environment, how many truly meet the following criteria as "investable assets"?

- Can generate yield for holders;

- Have protocol revenue, even if not currently distributed;

- Strong narrative and market recognition, capable of surviving a bear market.

I tried to figure this out.

Most data comes from DefiLlama, CoinMarketCap, and protocols reflecting market heat (Dexu, Moni, Lunarcrush, etc.).

I used Claude Code to process the data, trying to minimize personal bias —

I would have excluded some tokens (like XRP, ADA, BCH, etc.), but they have survived multiple cycles and maintain vitality due to ample liquidity.

Claude still made quite a few errors; debugging took 10 times longer than writing the article, so the table data is for reference only (link at the end).

Final results:

- A total of 12 categories, 132 investable tokens were filtered;

- Among them, 45 distribute dividends to holders (excluding those with extremely low yields);

- Annualized yield flowing to holders: $1.8 billion.

These classifications are entirely based on my subjective judgment of "can survive and have future potential," you may disagree.

The first key finding: The truly investable crypto market is pitifully small.

And the tokens that truly make money for holders are almost monopolized by two projects. More on that later.

It's funny, while compiling this list and checking tokens one by one, I came to this conclusion:

After repeatedly thinking about what to do in crypto, examining old and new tokens, and researching new narratives, I believe the option with the best risk-reward ratio (R/R) in the crypto world is:

Buy Bitcoin (BTC) directly.

Then use "play money" to constantly try new crypto protocols while continuously learning to use AI tools.

New opportunities will always emerge.

Most Worthwhile Tokens to Invest In: Revenue-Sharing Tokens

The dominant market narrative currently is:

Projects without revenue will eventually die!

Even ETH struggles to escape this "value by revenue" narrative.

Therefore, the most investable tokens are those that distribute revenue to holders through buybacks, burns, fee sharing, etc.

I set the threshold broadly: 30-day holder yield on DefiLlama ≥ $50,000.

These 45 tokens bring $153 million in monthly yield to holders,

Annualized total: $1.8 billion.

Top 10 Revenue Sharing:

Note: Revenue sharing ≠ Holder yield on DefiLlama.

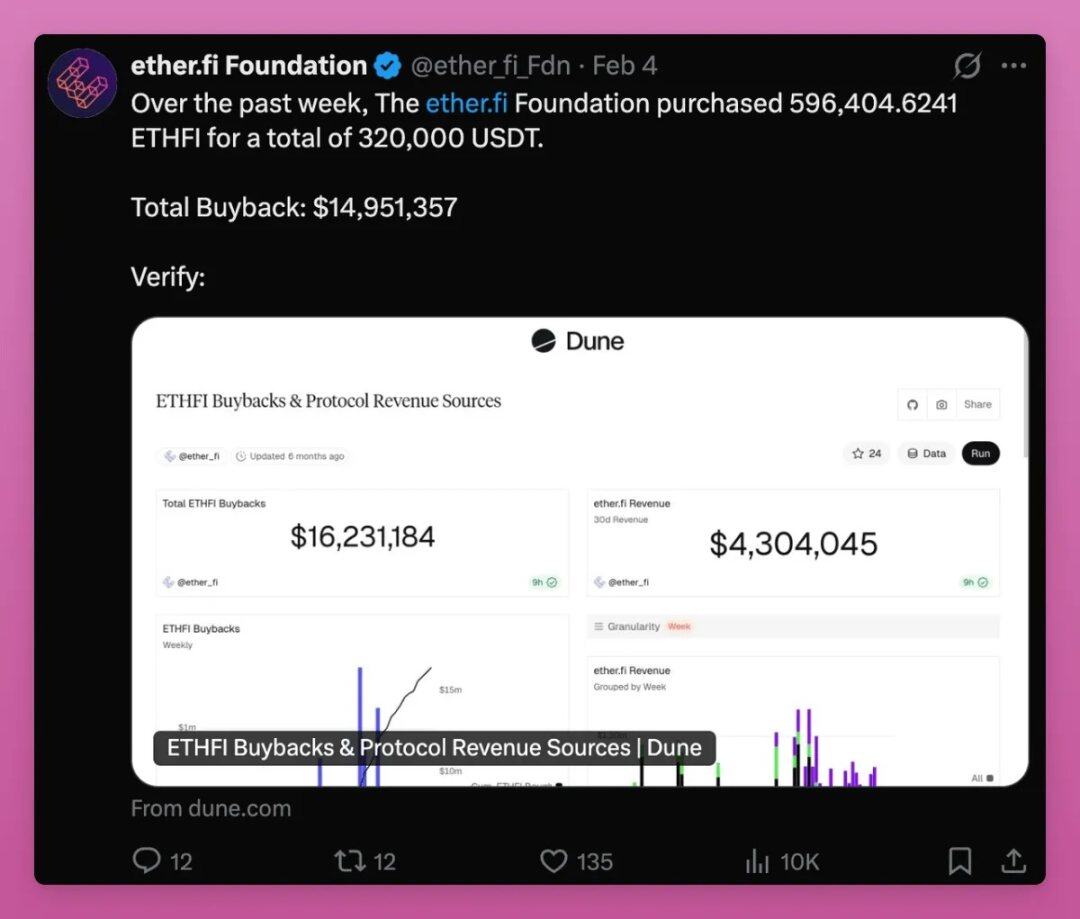

Example: EtherFi isn't on the holder yield leaderboard, but it has buybacks.

L1 public chains like Tron are categorized separately.

After the top five, monthly yield quickly drops below $3 million.

If the crypto market continues towards the "token = stock" logic,

Then the P/S (Price-to-Sales ratio, market cap / revenue) will become increasingly important.

- Pump.fun: 1.4x

- Aerodrome: 3.4x

By traditional finance standards, these are extremely cheap.

At the current revenue rate, they could earn back their entire market cap in less than 3 years.

Whereas:

- Uniswap: P/S as high as 121x

- Aave: P/S even higher at 341x

Because the market values them far beyond just "current revenue."

Aave recently finally started buybacks, but only distributes $412,000 monthly, while protocol monthly revenue is $10 million. Future governance changes may alter this.

Tokens with the lowest P/S (Price-to-Sales) ratio:

- Farcaster’s Clanker: 0.9x

- ORE: 0.9x

- Yield Basis: 0.8x

- Pump.fun: 1.4x

- QuickSwap: 1.4x

They can all earn back their market cap from revenue within 3 years.

The most important conclusion:

Hyperliquid + Pump.fun = 69% of all holder yield!

Out of 45 tokens, just two projects contribute over 2/3 of the cash flow.

This concentration is very thought-provoking.

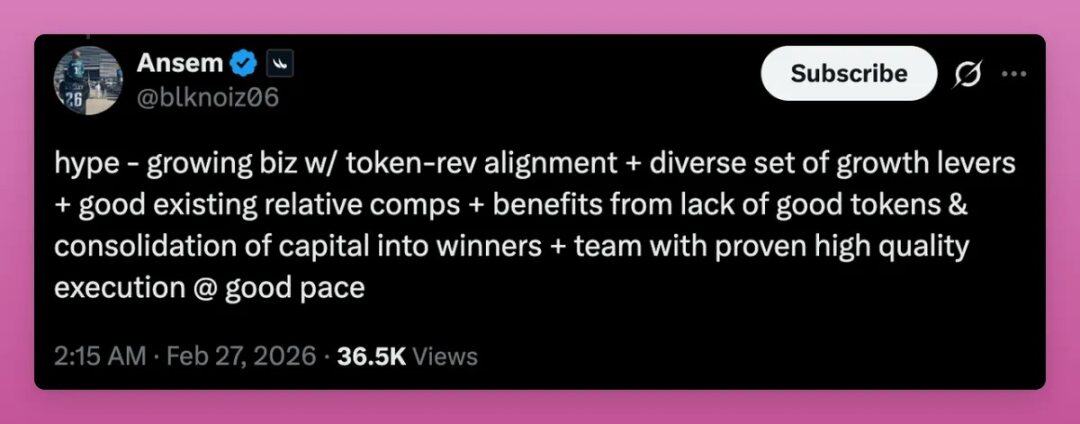

Ansem's tweet well summarizes the HYPE investment thesis:

HYPE:

- Business is continuously growing, token is highly tied to revenue;

- Possesses diversified growth levers;

- Existing comparable projects perform well;

- Benefits from scarce quality tokens and market concentration of capital towards top projects;

- Team has strong execution, steady pace, and impressive track record.

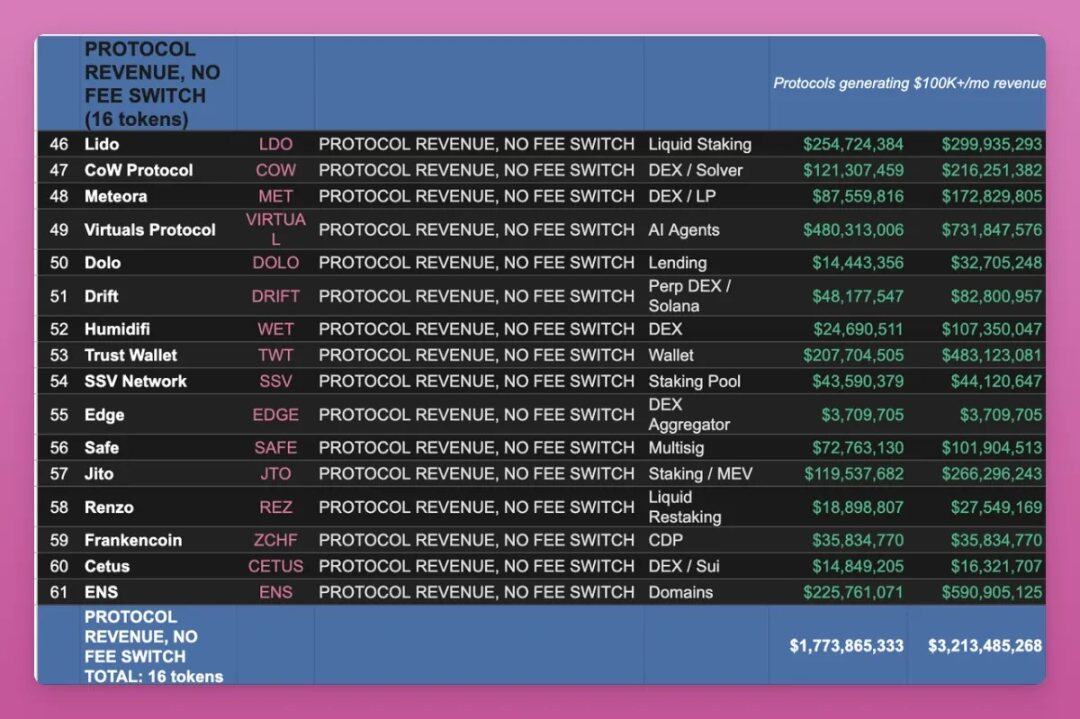

Protocols with Revenue, But No Dividend Distribution

This category has 16 tokens, with monthly protocol revenue ≥ $100,000, revenue stays in treasury.

Leading projects:

- Lido: $4.3 million monthly, TVL $32 billion (proposed staking dividends last year);

- CoW Protocol: $3 million monthly;

- Meteora (Solana): $2 million monthly;

- Virtuals Protocol: $1.4 million monthly;

- Drift: $868,000 monthly.

Lido vs ether.fi is an interesting comparison:

- Lido TVL is 10x higher, revenue 3x higher, but LDO holders get nothing;

- ether.fi distributes $1.5 million monthly to holders via buybacks.

If you're navigating a bear market, you want the one that pays you.

The investment logic for these assets is:

These protocols will eventually flip the "dividend switch."

Lido has been talking about it for years.

Jito generates $5.3 million in total monthly fees, but only $544,000 goes to the treasury.

The gap between total fees and holder yield is both opportunity and risk.

Overview of Other Sectors

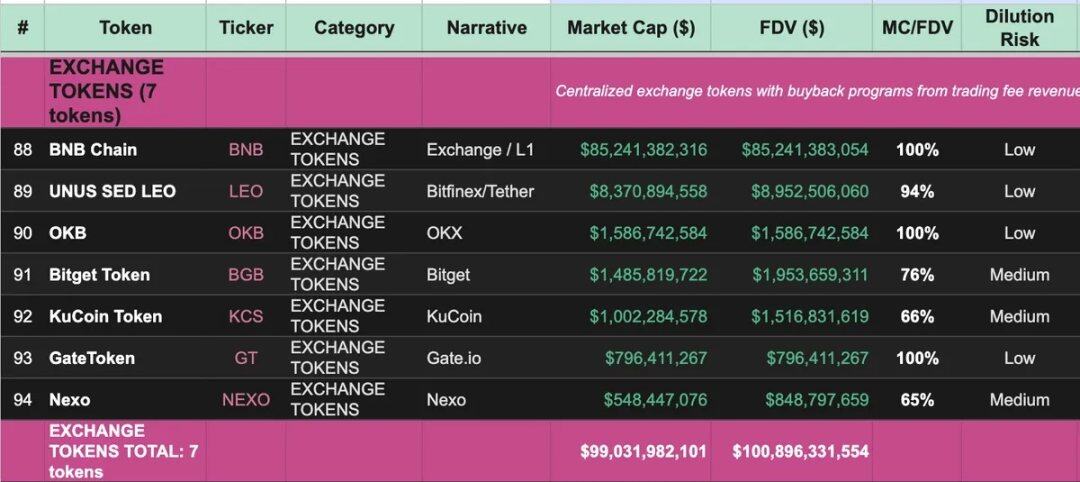

Exchange Tokens (7, total market cap $99 billion, including BNB)

Make money in both bull and bear markets. CEX trading volume may decline but won't go to zero.

- BNB: $85 billion;

- LEO, OKB barely dropped during the 2022 and 2024 bear markets.

Many have buyback plans, just not reflected in DefiLlama data.

High circulating supply of CEX tokens further reduces downside risk.

L1 Public Chains (19, total market cap $1.8 trillion)

L1s are the base layer.

- BTC: $1.36 trillion

- ETH: $245 billion

I relaxed standards for XRP, ADA, and especially Cosmos because they've survived multiple cycles, have believers and liquidity, and possess enduring vitality.

You might hate Tron TRX, but it generates $26 million in monthly fees — more than Solana and Ethereum.

It has performed strongly this cycle too, you can check the charts.

L1 public chains won't disappear, but valuation volatility will be extreme. DYOR.

AI & Compute (8, total market cap $5.1 billion)

Most have no real revenue, with one exception:

Venice (VVV): The only AI token supporting buyback & burn via subscription and API revenue, 43% of supply already burned.

- Bittensor: $1.9 billion market cap, 128 subnets, no protocol revenue;

- Render, Akash: Sell GPU compute power, cheaper than centralized platforms;

- Grass: Provides decentralized network data for AI training.

Note: Some AI tokens not on this list are surging now, may be suitable for short-term trading, but whether they count as "investable" is debatable.

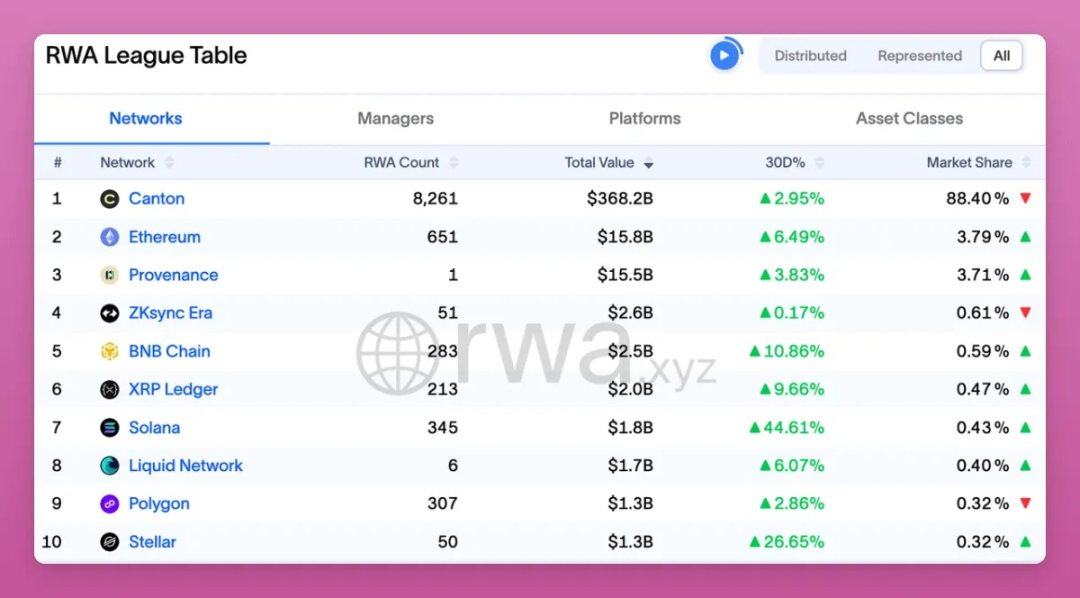

RWA Tokenization (7, total market cap $13.5 billion)

Growing quietly, I believe the real RWA bull market hasn't arrived yet.

Canton Network holds 88.57% of on-chain RWA, approximately $372 billion in tokenized assets. However, real-world assets are not as simple as they appear.

Chainlink is the key oracle for the RWA infrastructure layer, but LINK's staking rewards come from inflation and a fixed reward pool, not protocol revenue sharing.

Chainlink has decent revenue, but it flows to node operators and the treasury, not directly to holders.

Privacy Tokens (2, total market cap $9.7 billion)

High-risk sector: Either becomes increasingly important as regulation tightens, or gets outright banned.

But demand remains steady regardless of market cycle.

- Monero: $6.2 billion

- Zcash: $3.6 billion

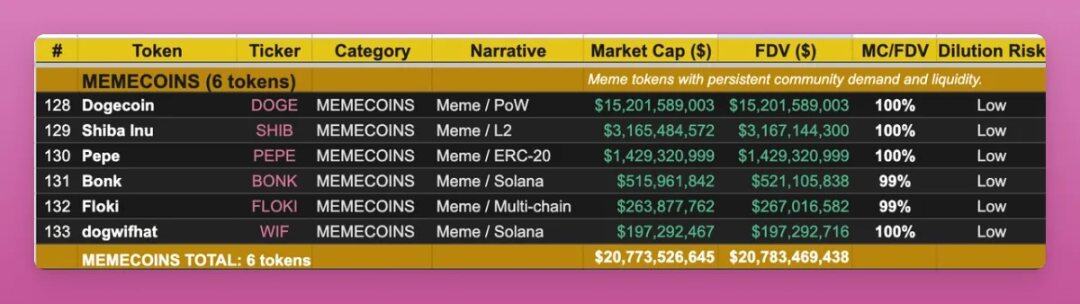

Meme Coins (6, total market cap $20.8 billion)

Categorizing them as "investable" might be controversial.

But like Bitcoin, they survive on community.

- DOGE: $15.2 billion market cap, exists for over a decade;

- SHIB, PEPE, BONK, FLOKI, WIF also made the list.

If the market rebounds, they might outperform high-yield tokens.

Because they have no revenue cap, they have no ceiling.

And they are almost fully diluted, with less selling pressure.

Other Categories

- L2 Public Chains (7, total market cap $3.7 billion);

- DePIN (5, total market cap $500 million): Decentralized storage, data collection;

- Oracles / Infrastructure (7, total market cap $1.8 billion);

- Stablecoin Infrastructure (4, total market cap $1.1 billion): Ethena leads.

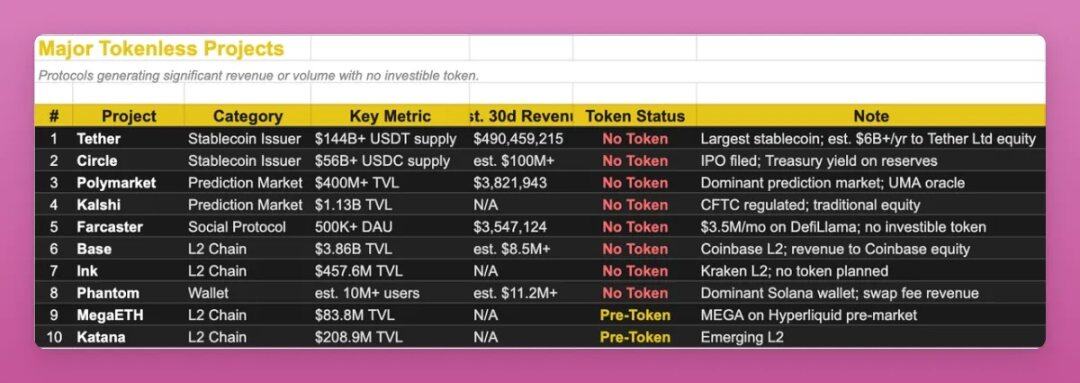

Super Profitable Projects Without Tokens

Some of the most profitable crypto businesses have no investable token.

- Tether: $6 billion+ annual revenue, more than the sum of those 45 yield tokens, all goes to shareholders;

- Polymarket: $3.8 million monthly revenue, no token;

- Base: Revenue goes to Coinbase shareholders, may issue token in the future;

- Phantom: Millions of users, extremely high fees;

- Circle: USDC issuer, gains reflected in IPO;

- Kalshi: Regulated by CFTC, no token;

- Farcaster: Already acquired, airdrop expectations significantly lowered, but may still issue token.

So, How to Use This Information?

The ideal assets to hold during a bear market meet four points:

- Have holder yield

- Low P/S ratio (market cap / revenue)

- High MC/FDV (market cap / fully diluted valuation)

- Sustained, stable demand

Very few tokens meet all.

Closest matches:

- PUMP: 1.4x P/S, 33% MC/FDV

- AERO: 3.4x, 50%

- JUP: 7.3x, 51%

- SKY: 16x, 98%

- CAKE: 15.1x, 96%

Low-risk choices:

Exchange tokens: LEO, OKB, GT

Almost fully diluted, supported by exchange profit buybacks, most stable performance in bear markets.

High risk, high reward:

HYPE: Yield far ahead, but MC/FDV only 25%.

Drops to 41% after Coingecko's new statistics exclude long-term non-circulating and burned tokens.

Tradable opportunities:

Watch for governance changes:

Bet on projects with revenue that haven't yet flipped the "dividend switch."

Focus on:

Lido, Meteora, Drift, CoW Protocol

Everything else, depends on conviction.

Do you believe AI compute will be on-chain?

Do you believe RWA tokenization will continue to grow?

I believe so, but are these tokens the right bets?