Institutional adoption isn't about building up, it's about sucking Crypto dry

- Core Viewpoint: The current so-called "institutional adoption" is essentially a strategy by traditional financial institutions (TradFi) to extract value from the crypto economy. Its core goal is to convert on-chain assets into their own Assets Under Management (AUM) and stable fee streams, rather than supporting the development of the native ecosystem.

- Key Elements:

- TradFi has become the primary winner: USDT and USDC generate approximately $10 billion in net interest spread annually, flowing to companies like Tether, Coinbase, and Circle; BlackRock's IBIT Bitcoin ETF reached about $100 billion in AUM in roughly 18 months, becoming a highly profitable product for them.

- Shift in institutional profit logic: Early institutions focused on crypto's advantages in reducing operational costs; post-2024, institutions (with IBIT as the benchmark) primarily package crypto into products like ETFs as new, high-margin revenue streams.

- On-chain capital becomes the new frontier for AUM competition: The roughly $300 billion stablecoin supply, nearly $100 billion DeFi TVL, and tens of billions in RWA products, with their 2-4% low yields, are seen as under-monetized cash flows that can be packaged and monetized by institutions.

- Macro capital landscape squeeze: The AI capital expenditure supercycle requires trillions of dollars, siphoning liquidity from other asset classes and intensifying fierce competition among asset managers for all AUM channels, including crypto.

- Industry faces an existential crisis: If the crypto economy does not build powerful native financial institutions (e.g., on-chain asset management, risk management), it will become a mere liquidity sub-account for TradFi, leading to a continuous outflow of economic value.

Author | Meltem Demirors

Compiled by | Odaily(@OdailyChina)

Translator | Ding Dang(@XiaMiPP)

Institutions have finally "entered crypto"—but they're not here to buy you out. They're here to turn the crypto economy into a fee-generating machine for their AUM (Assets Under Management) accumulation. This is not a judgment or criticism, just an observation of facts.

The following thoughts primarily address crypto as a digital currency/token economy, rather than blockchain purely as financial infrastructure (the latter, in the vast majority of cases, does not require a native token, as evidenced by the architecture of most DeFi governance tokens today).

This is a view I've held since last year's Digital Assets Summit, where my opening keynote was titled "Believe in Something". Everything that has happened in the past twelve months has not changed my mind, only made the picture clearer.

Recently, my friend Evgeny from Wintermute and Dean from Markets Inc. wrote two excellent articles discussing what so-called "institutional adoption of crypto" actually means and its impact on market cycles. This inspired me to write a third piece, building on their work and adding a new perspective—the changing capital landscape and the erupting AUM war.

If you're short on time, read this one-sentence summary:

"Institutional adoption" is not a mission; it's an extraction strategy. The only real question left is: Can crypto build and fund its own institutions fast enough to keep economic value on-chain, rather than letting it continuously leak into the hands of TradFi?

TradFi is Already Extracting Most of the Value from the Crypto Economy

Just follow the money flow to see who the real winners are in the current crypto world: not DeFi protocols, but the very financial companies Satoshi Nakamoto sought to replace in the Bitcoin whitepaper.

- Just the two major stablecoins, USDT and USDC, generate approximately $10 billion in annual net interest spread revenue, accruing to Tether (a private company), Coinbase, and Circle (public companies). While these companies are certainly important participants in the crypto economy, their primary allegiance is to their own shareholders.

- Cantor Fitzgerald—led by current US Secretary of Commerce Howard Lutnick—earns hundreds of millions of dollars annually by holding US Treasuries for Tether and organizing trades around digital asset companies and investment products.

- US President Trump, his family, and partners have also cumulatively profited billions of dollars through an expanding portfolio of crypto projects and token vehicles.

- BlackRock's Bitcoin ETF, IBIT, grew to approximately $100 billion AUM in about 18 months, becoming the fastest-growing ETF in history and one of the company's most profitable products (more on this later).

- Apollo Global Management and its peers are quietly channeling crypto collateral and corporate treasury balances into their own credit and multi-asset funds.

Every year, traditional financial institutions siphon tens of billions of dollars in assets and profits from the crypto economy—and in many cases, they capture more economic upside than the protocols that originally created the value.

The "institutional innovators" cheering for "adoption" at countless conferences and the trench warriors obsessing over memecoins on Twitter are more alike than you think. We need to stop licking boots and start using our brains.

How Do Institutions Actually Think?

Corporations have one core function: profit maximization. Cryptocurrency can achieve this in two ways:

- On the Cost Side: Distributed ledgers, on-chain collateral, and instant settlement can drastically reduce back- and middle-office operational costs, improving collateral liquidity and utilization (see my previous notes on fungible liquidity).

- On the Revenue Side: Packaging crypto into ETFs, tokenized funds, structured products, custody services, basis trade packages, lending, treasury management solutions... all throw off hefty fee streams, plus free hype from the crypto community on Twitter.

Over the past decade, institutions primarily focused on the first path.

When we founded DCG in 2015, I spent three full years pitching the advantages of Bitcoin's global ledger and final settlement mechanism to virtually every financial institution. At that time, financial services firms did not see crypto as a new revenue source. It was considered too risky; and the potential gains from peddling altcoins were insufficient to convince boards to take on the reputational and compliance risks.

After leaving DCG, I joined CoinShares in early 2018. At that time, the company's AUM grew from tens of millions to billions of dollars. The few independent investment managers who dared to embrace Bitcoin—such as Cathie Wood, Murray Stahl, Ross Stevens—were ultimately richly rewarded for their courage.

Early 2024 marked a watershed moment. Institutions began treating crypto as a tool for the second path: a new revenue source.

While there had been sporadic institutional participation before, the launch of BlackRock's IBIT Bitcoin ETF blew the dam wide open. IBIT became the most successful ETF ever, significantly boosting BlackRock's financials. Some key numbers:

- IBIT reached $70 billion AUM in its first year, becoming the fastest ETF in history to reach that scale, roughly five times faster than the previous record holder, SPDR Gold Shares (GLD).

- After IBIT options launched in late 2024, it attracted over $30 billion in new inflows, while competitor flows largely stagnated, giving it over half the market share of all Bitcoin ETF AUM.

- IBIT's current ~$100 billion AUM can generate hundreds of millions of dollars in annual fee revenue for BlackRock, making it even more profitable than the company's nearly trillion-dollar S&P 500 index fund.

The conclusion is clear: IBIT showed the entire playbook to every major asset manager and financial services institution—take Bitcoin or other digital assets → package them into traditional fund structures → list them → turn them into stable, lucrative fee streams. Everything that follows—DATs, tokenized treasuries, on-chain money market funds—is just running that same playbook over and over.

The AI Capex Supercycle: A Black Hole Consuming Capital

Switching gears slightly to discuss another mega-trend—this is also why we founded Crucible immediately after IBIT's launch in 2024. The energy-compute value chain is reshaping the global capital stack in real-time.

Building the AI economy—chips, data centers, power, factories, etc.—requires trillions of dollars in capital expenditure over the next decade, and that money has to come from somewhere. All liquid assets not directly tied to AI—crypto, non-AI stocks, even credit—are being sold to chase what are perceived as "must-have" AI plays.

Simultaneously, many LPs are overallocated in private markets, facing slower exits and distributions, and are quietly cutting back or delaying new private credit and PE commitments. This leads to longer, lumpier, and more unpredictable fundraising cycles, intensifying the war for quality AUM pipelines between asset managers and PE firms. The result is that anything that looks like a capital pool will be squeezed dry.

On-Chain Capital: The Next AUM Frontier

In this AUM war, crypto is no longer a quirky toy but trillions of dollars in potential management scale, sitting there in plain sight.

IBIT has proven that crypto is both a money printer and a "honey pot" for attracting institutional allocators. The Trump administration has also made it clear it will create an extremely permissive environment for all sorts of crypto innovation.

On-chain asset management and treasury scale already amounts to hundreds of billions of dollars:

- Approximately $300 billion in stablecoin supply, with ~60% in USDT and ~25% in USDC;

- Total DeFi TVL of ~$90–100 billion, spread across Ethereum, Solana, BSC, Hyperliquid, etc.;

- Real World Asset (RWA) products add hundreds of billions more through tokenized money market funds (like BlackRock's BUIDL), tokenized gold (like Tether Gold, PAXG), and consumer credit products (like Figure's tokenized HELOCs).

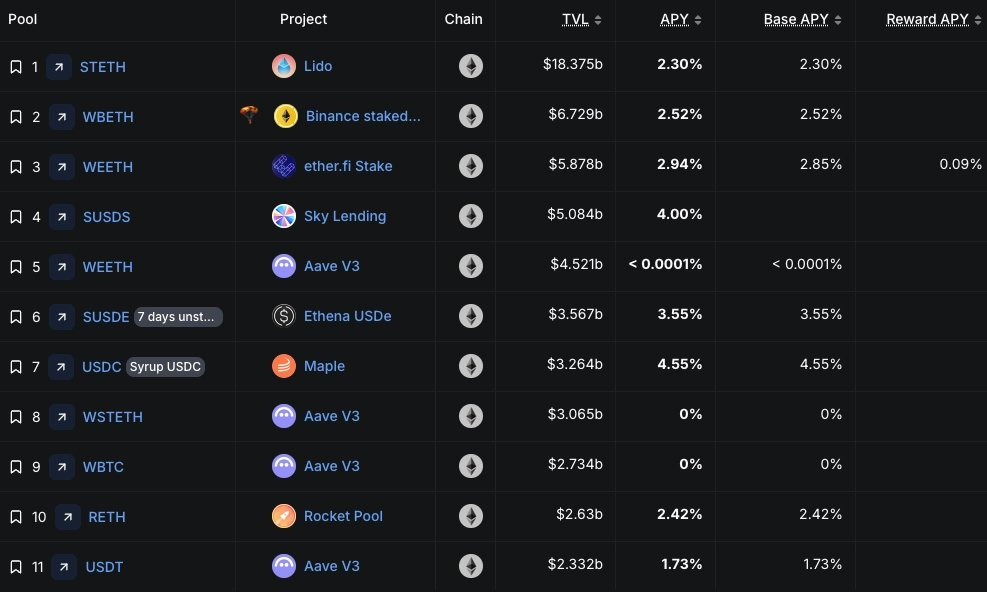

But the average yield on this on-chain capital is only 2–4%, while traditional money market funds offer 4.1%, and even Lido's $18 billion stETH pool yields only ~2.3%.

To a hungry asset accumulation machine, this isn't "DeFi TVL"; it's under-monetized cash flow—ripe for packaging, staking, re-lending, and fee extraction. For institutions, this is as natural as breathing.

Image from DefiLlama

Tokenization and regulated wrapper products have turned previously "untouchable" crypto capital into fee-generating AUM that fits within existing custody and risk frameworks. As companies, DAOs, and protocols accumulate large crypto treasuries and seek safer external yields, asset managers can repackage these assets into tokenized funds, money market funds, and structured products. For firms facing fundraising pressure and saturated traditional channels, "raiding" crypto balance sheets is one of the cleanest paths to growing fee-generating AUM.

A Wake-Up Call

Just as Western economies introduced populations that did not share their culture and values and are now suffering the social and economic consequences, crypto stands on the brink of a similar existential crisis. The crypto economy and its leading thinkers are introducing financial institutions that do not share our values—institutions that are not here to co-build native economic growth. Our industry will soon taste the same social and economic bitter fruit.

If left unchecked, the crypto economy will become just another liquidity silo for TradFi's AUM machines. The only way out is to accelerate the building and scaling of our own native institutions—on-chain asset managers, risk managers, underwriters, financial products, crypto-native allocators—to compete for treasury AUM, design products that truly serve crypto's long-term interests, and keep more economic value inside the crypto ecosystem rather than leaking it onto corporate P&L statements.

If we don't prioritize partnering with crypto-native institutions now, "institutional adoption" won't be a victory; it will be an annexation.

Believe in something. Otherwise, we'll be left with nothing.

Related Reading

The War Between Stablecoins and Banking Probably Doesn't Exist