Huobi Growth Academy | Crypto Market Macro Report: US-EU Tariff TACO Trade Reemerges, US-Japan Bond Yields Climb, Short-Term Pressure on Crypto Market

- Core View: The recent decline in the crypto market is not due to a deterioration in its own fundamentals. Instead, it is a phase of pressure experienced as a high-liquidity risk asset against the backdrop of tightening global macro liquidity and a rising interest rate center. This signals that crypto asset pricing is transitioning from a "narrative-driven" framework to a more mature "macro-driven" one.

- Key Factors:

- The US-EU tariff conflict, centered on Greenland's sovereignty, politicizes economic issues. Its unpredictability has increased risk premiums and uncertainty in global markets.

- The simultaneous surge in long-term bond yields in the US and Japan (US 10-year to 4.27%, Japan 30-year to 3.91%) has impacted the anchor point for global low-cost liquidity, triggering a systemic tightening of financial conditions.

- Rising interest rates and tightening liquidity are forcing institutional investors to reduce risk exposure and leverage. High-volatility, high-liquidity crypto assets have become the preferred "adjustment valve" for de-risking.

- During this shock, Bitcoin has exhibited the properties of a macro risk asset, showing high sensitivity to liquidity, rather than acting as a safe-haven asset like gold. Its price correction represents a market recalibration of its role.

- The current market correction is more a result of exogenous macro shocks. There has been no systemic credit crisis or on-chain liquidity freeze similar to 2022, and the market structure remains relatively orderly.

I. From Greenland to Global Markets: The Trump-Style TACO Trade Plays Out Again

Unlike previous tariff disputes centered on trade deficits, industrial subsidies, or currency exchange rates, the "pricing core" of this round of US-Europe friction lies not in economic ledgers but in sovereignty and geopolitical control: tariffs are merely the means, while territory and strategic depth are the true objectives. The immediate trigger was a joint military exercise conducted by eight nations—Denmark, Norway, Sweden, France, Germany, the United Kingdom, the Netherlands, and Finland—in Greenland. The Trump administration defined this as a challenge to US strategic interests in the Arctic and swiftly weaponized, politicized, and sovereignized the tariff tool—bundling trade measures with territorial claims through a binary threat of "either sell the island or face tariffs." It presented a clear and aggressive timeline: imposing a 10% punitive tariff on the aforementioned European countries starting February 1, with a potential increase to 25% by June 1. The sole condition for exemption was reaching an agreement on the US purchasing or securing long-term control of Greenland. Europe's response promptly amplified this uncertainty. Denmark reiterated that Greenland's sovereignty is non-negotiable, the EU swiftly initiated emergency consultations and prepared reciprocal countermeasures. Crucially, the EU possesses a countermeasure list totaling a staggering 930 billion euros—this is not a temporary emotional reaction but an institutionalized "anti-coercion toolbox." Consequently, markets are no longer facing a single-point friction but a potentially rapidly escalating transatlantic confrontation framework: both sides are "laying their cards on the table," yet the object of the game is not short-term trade interests but alliance order, resource control, and strategic presence.

However, Trump subsequently stated on Wednesday that he had reached a cooperation framework on Greenland with NATO and withdrew the tariff threats against the eight European nations. Simultaneously, during his keynote speech at the World Economic Forum in Davos, Switzerland, Trump called for "immediate negotiations" to acquire the Danish territory of Greenland, asserting that only the United States could ensure its security. Yet, he also hinted that he would not use military force to control the island. This once again played out the classic Trump-style TACO trade, leading to a broad rebound in US stocks. The crypto market also saw a slight rebound but did not fully recover the previous losses.

However, what truly amplified market volatility was not the specific figure of Trump's proposed 10% or 25% tariffs on multiple European countries, nor the recurring pattern of threatening tariffs only to compromise again. It was the institutional uncertainty it represents: the trigger for conflict is clear (the tariff timeline), yet its endpoint is unclear (sovereignty issues have no "reasonable price"); execution actions could be swift (executive orders can be implemented), yet negotiation cycles could be prolonged (alliance coordination and domestic politics take time); furthermore, there exists a repetitive rhythm of "maximum pressure—partial compromise—renewed pressure," forcing asset pricing to incorporate higher risk premiums. For global markets, such events first elevate volatility through the expectation channel: businesses and investors first reduce risk exposure, increase allocations to cash and safe-haven assets, and then observe whether policies are actually implemented. Once conflicts persist, supply chain costs and inflation expectations further transmit to interest rates and liquidity, ultimately spreading pressure to all "risk appetite-sensitive" areas such as stocks, credit, foreign exchange, and crypto assets. In other words, this is not a traditional trade friction but a geopolitical sovereignty conflict using tariffs as leverage. Its greatest harm to markets lies in escalating negotiable economic issues into difficult-to-compromise political problems—when uncertainty becomes the primary variable, price volatility shifts from "emotional disturbance" to "structural premium," which is precisely the pricing backdrop currently faced by global assets.

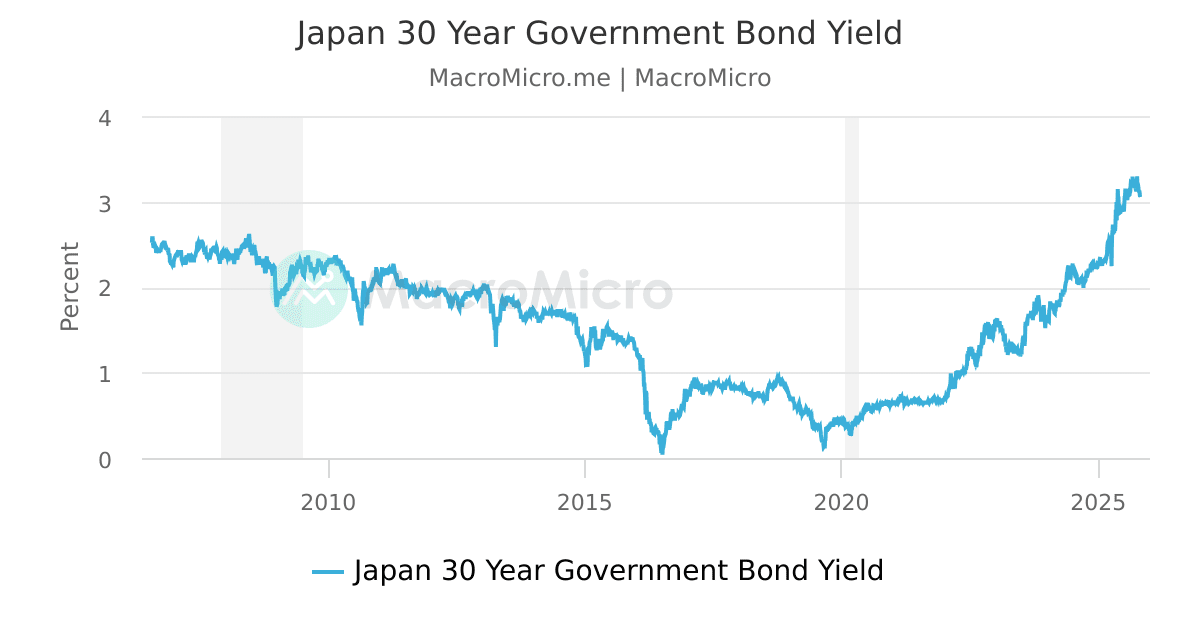

II. The Starting Point of the Interest Rate Shock: Synchronized Rise in US and Japanese Government Bond Yields

As geopolitical risks were rapidly repriced, the global bond market was the first to deliver the most direct and "systemically significant" response. In mid-January, Japan's 30-year government bond yield surged over 30 basis points in a single day, peaking at 3.91%, hitting a 27-year high. Almost simultaneously, the US 10-year Treasury yield climbed to 4.27%, reaching a four-month high. For global markets, this combination of "synchronized long-end rate increases in the US and Japan" is not a short-term emotional fluctuation but a structural shock substantial enough to alter the foundation of asset pricing, with impacts extending far beyond the bond market itself. First, it is essential to clarify that Japan's role in the global financial system has long been not merely that of an ordinary sovereign bond issuer but the anchor for global low-cost liquidity. Over the past two decades, through sustained ultra-loose monetary policy, Japan has exported massive, extremely low-cost yen funds to the world, becoming the foundational source for global carry trades and cross-border capital allocation. Whether it's emerging market assets, US and European credit products, or high-risk stocks and crypto assets, they all, to varying degrees, embed an implicit financing structure of "borrowing yen to invest in high-yield assets." Therefore, when Japan's long-term government bond yields rise sharply within a short period, its implication is not as simple as "Japanese bonds becoming more attractive." It is a deeper signal: the most stable and cheapest source of funding in the global financial system is beginning to loosen.

Once Japan no longer stably exports low-cost funds, the risk-reward ratio for global carry trades deteriorates rapidly. Previously established high-leverage positions reliant on yen financing will face dual pressures of rising funding costs and amplified exchange rate risks. In the initial stages, such pressure often does not directly manifest as an asset crash but first prompts institutional investors to proactively reduce leverage and cut exposure to high-volatility assets. It is precisely at this stage that global risk assets exhibit a characteristic of "undifferentiated pressure"—not due to deteriorating fundamentals but a systemic rebalancing triggered by changes in funding sources. Secondly, the concurrent overlay of US-Europe tariff conflicts further heightens expectations for imported inflation, providing a "rational narrative" for rising interest rates. Unlike past trade frictions centered on consumer goods or low-end manufacturing, the potential tariffs in this round affect high-value-added, difficult-to-substitute sectors such as advanced manufacturing, precision instruments, medical equipment, and the automotive supply chain. The US has a structural dependence on European countries in these areas, and tariff costs will almost inevitably transmit through the supply chain to end prices. At the market expectation level, this means the interest rate pricing logic previously built on a "falling inflation core" is being re-evaluated. Even if tariffs are not fully implemented in the short term, the inflation risk itself—being "possible and difficult to quickly reverse"—is sufficient to elevate the risk premium on long-term rates.

Thirdly, the US's own fiscal and debt issues provide a structural backdrop for the rise in long-end US Treasury yields. In recent years, the US fiscal deficit and national debt have continued to expand, and market concerns about long-term debt sustainability have not truly dissipated. If tariff conflicts escalate further, they could not only raise inflation expectations but also be accompanied by more fiscal subsidies, industrial support, and security expenditures, thereby increasing the fiscal burden. In this environment, long-end US Treasuries are caught in a typical "tug-of-war": on one hand, geopolitical uncertainty and market risk aversion drive capital into the bond market; on the other hand, inflation and debt concerns demand higher term premiums to compensate for risk. The result is an elevation in both yield levels and volatility, making the risk-free rate itself "no longer risk-free." The combined effect of these three forces is a systemic upward shift in the global risk-free rate anchor and a passive tightening of financial conditions. For risk assets, this change is highly penetrating: rising discount rates directly compress valuation space, rising funding costs inhibit new leverage, and liquidity uncertainty amplifies market sensitivity to tail risks.

The crypto market is under pressure precisely within this macro context. It must be emphasized that Bitcoin and other mainstream crypto assets are not being "singled out"; rather, they are assuming the role of high-volatility, high-liquidity risk assets during the process of rising interest rates and tightening liquidity. When institutional investors face margin pressure or risk exposure constraints in traditional markets, the first assets to be sold are often not those with poor liquidity and high adjustment costs, but those that can be quickly liquidated and have the greatest price elasticity. Crypto assets precisely possess these characteristics. Furthermore, the upward shift in the risk-free rate anchor is also altering the relative attractiveness of crypto assets. In a low-interest-rate, high-liquidity environment, the "opportunity cost" of assets like Bitcoin is low, and investors are more willing to pay a premium for their potential growth. However, when US and Japanese long-end rates rise in sync, and safe assets themselves begin to offer more attractive nominal returns, the allocation logic for crypto assets inevitably needs reassessment. This reassessment does not imply long-term bearishness but means that, in the short term, prices need to adjust through pullbacks to realign with the new interest rate environment. Therefore, from a macro perspective, the synchronized rise in US and Japanese government bond yields is not a "bearish story" for the crypto market but the clear starting point of a transmission chain: rising interest rates → tightening liquidity → declining risk appetite → pressure on high-volatility assets. Within this chain, the crypto market's correction reflects more the outcome of changing global financial conditions rather than a deterioration in its own fundamentals. This also determines that as long as the trend in interest rates and liquidity has not fundamentally reversed, the crypto market will remain highly sensitive to macro signals in the short term, and the true directional choice still awaits the marginal changes of this interest rate shock.

III. The True State of the Crypto Market: Not a Crash, but Temporary Pressure

Rising interest rates themselves do not directly "attack" the crypto market, but they form a clear and repeatable transmission chain through changes in liquidity and risk appetite: tariff threats elevate inflation expectations, inflation expectations push up long-end rates, rising rates increase credit and funding costs, financial conditions tighten as a result, ultimately forcing capital to systematically reduce risk exposure. In this process, price volatility is not the starting point but the result; the true driving force is the change in funding sources and capital constraints. Among these, the offshore US dollar market plays a crucial yet often underestimated role. As US-Europe tariff conflicts combine with geopolitical uncertainty, the risk premium for global trade finance and cross-border settlement rises, increasing the cost of obtaining offshore US dollars. This change is not necessarily reflected in explicit policy rates but more in interbank lending, cross-currency basis spreads, and funding availability. For institutional investors, this means stricter margin requirements, more conservative risk exposure management, and reduced tolerance for high-volatility assets. When volatility and correlation rise in traditional markets, institutions often do not prioritize selling assets with poor liquidity, high exit costs, or complex regulatory structures. Instead, they choose to reduce positions in those assets with **high volatility, high liquidation efficiency, and the most "portfolio-friendly" adjustment characteristics**. Under the current structure, crypto assets precisely possess these two features, thus assuming the primary "pressure relief valve" role during macro shocks.

It is precisely against this backdrop that Bitcoin failed to exhibit safe-haven properties similar to gold during this shock. This phenomenon is not anomalous but a natural outcome of the evolution of its asset attributes. Unlike its early narrative packaging as "digital gold," Bitcoin in its current stage more closely resembles a macro risk asset highly dependent on US dollar liquidity. It cannot operate independently of the US dollar credit system, and its price is highly sensitive to changes in global liquidity, interest rate levels, and risk appetite. When offshore US dollars tighten, long-end rates rise, and institutions need to quickly replenish margins or reduce portfolio volatility, Bitcoin naturally becomes a priority for reduction. In stark contrast, gold and silver have continued to strengthen during this shock, driven not by short-term return expectations but by safe-haven premiums stemming from central bank demand, physical attributes, and "de-sovereignization" characteristics. In an environment of escalating geopolitical games and repricing of sovereign risk, such "stateless" assets are more likely to gain favor with capital. It must be emphasized that this is not a "failure" of Bitcoin but a market recalibration of its role. Bitcoin is not a safe harbor in a crisis but an amplifier within liquidity cycles; its strength lies not in hedging extreme risks but in its high sensitivity to recovering risk appetite during liquidity expansion phases. Understanding this helps avoid harboring unrealistic expectations during macro shocks.

From a structural perspective, despite a relatively significant price correction, the current crypto market has not replayed the systemic risks of 2022. The market has not experienced credit crises at major exchanges or with stablecoins, nor has it observed consecutive liquidation cascades or on-chain liquidity freezes. The behavior of long-term holders remains relatively orderly, with their distribution of holdings reflecting more rational profit-taking rather than forced selling. Bitcoin did trigger some liquidations after breaking below key price levels, but the overall scale and chain reaction are significantly lower than in the previous bear market, resembling more a portfolio rebalancing under macro shock rather than a collapse of the market's own structure. In other words, this is a phase of pressure dominated by exogenous shocks, not a crash triggered by internal imbalances within the crypto system.

IV. Conclusion

The market volatility triggered by the escalation of US-Europe trade friction and the synchronized rise in US and Japanese government bond yields is, in essence, not a "single-point risk event" for any specific asset or market. It is a systemic repricing process centered on global liquidity, the interest rate anchor, and risk appetite. In this process, the decline in the crypto market does not stem from a deterioration in its own fundamentals, nor from institutional or credit-level failures. It is the natural result of the role it currently plays within the financial system—namely, as a high-liquidity, high-elasticity risk asset highly sensitive to macro conditions, it bears the brunt of pressure during phases of tightening liquidity and rising interest rates. From a longer-term perspective, this round of adjustment does not negate the structural revaluation process the crypto market is undergoing in 2026. On the contrary, it clearly reveals an ongoing change: crypto assets are gradually shedding the early stage of "narrative-driven, sentiment-priced" and entering a more mature, more institutionalized pricing framework. Within this framework, prices are no longer primarily driven by stories, slogans, or single events but begin to internalize as a function of macro liquidity, interest rate structure, and changes in risk appetite. For investors, the real challenge lies not in judging short-term price movements but in whether they can promptly update their analytical frameworks to understand and adapt to this long-term trend of transitioning from a "narrative market" to a "macro market."