The Stream Finance collapse raises some serious questions.

- 核心观点:DeFi协议因高杠杆与风控缺失引发系统性危机。

- 关键要素:

- 外部基金经理亏损9300万美元。

- xUSD脱锚暴跌,流动性池抽空。

- 连锁反应致DeFi锁仓量骤降200亿。

- 市场影响:加速行业向透明度与稳健性转型。

- 时效性标注:中期影响

Recently, the decentralized finance (DeFi) protocol Stream Finance disclosed that its commissioned external fund managers (Curators) suffered losses of approximately $93 million and suspended all deposit and withdrawal operations the following day. Following this incident, its synthetic stablecoin xUSD quickly became unpegged, plummeting from $1 to approximately $0.1. Its liquidity pool was almost completely emptied within two days, triggering a series of chain reactions in the market. Multiple lending protocols related to xUSD, xETH, and xBTC were affected, with approximately $1 billion of funds flowing out of the market. Simultaneously, the total value locked in DeFi decreased from approximately $150 billion to $130 billion in a short period, and the market capitalization of the stablecoin sector shrank by over $2.5 billion during the same period.

Currently, Stream Finance remains in the withdrawal suspension phase and has not yet announced a repayment plan. This event marks the largest systemic crisis in DeFi since the Terra UST collapse. This crisis has forced the market to re-examine the fragile structure and growth model of DeFi. The high-yield cycle model of the past has been disproven under tightening liquidity, and the market is now shifting its focus to transparency, robustness, and sustainability. The following analysis from CoinW Research Institute will delve into the causes, transmission mechanisms, and impact on the future structure of DeFi, aiming to provide more insights for the industry's development.

I. The Beginning and End of Stream Finance's Collapse

1. The hidden dangers of a cycle of lending

Stream Finance's core mechanism amplifies returns through revolving lending and synthetic asset structures. Users deposit mainstream assets like USDC , ETH , and BTC into the protocol to obtain corresponding synthetic assets such as xUSD, xETH, and xBTC. These assets are then used as collateral to borrow more native assets and repeat the process, achieving higher returns through a leveraged cycle. On the surface, this mechanism improves capital efficiency, but its essence is a highly leveraged model heavily reliant on external market conditions and the stability of collateral assets. Once the lending spread narrows, collateral fluctuates, or liquidity dries up, the positive feedback of enhanced returns quickly transforms into a negative feedback loop of liquidation. For example, if a user borrows $50,000 from the lending protocol using $100,000 worth of xUSD as collateral, and xUSD drops from $1 to $0.50, the collateral is instantly worth only $50,000. If the decline continues, it will directly lead to losses and a chain of liquidations.

A greater risk lies in the protocol's extremely weak transparency and risk management mechanisms. Stream Finance has not publicly disclosed complete proof of reserves or leverage limits, and discrepancies have long existed between the protocol's assets and verifiable on-chain data. Furthermore, Stream Finance's officially announced "market-neutral strategy" is not a completely risk-free hedge, but rather a strategy to balance price fluctuations by simultaneously holding long and short positions. Its stability relies on stable market prices and funding conditions; once sharp fluctuations or insufficient liquidity occur, this "neutral" structure will become unbalanced, and the addition of leverage will amplify losses, potentially triggering a chain reaction of liquidations. Because its synthetic assets (especially xUSD) are widely used as collateral in other lending protocols, de-pegging will not only trigger internal runs but also create transmission risks at the ecosystem level, causing liquidity and trust to evaporate rapidly in a short period.

2. Causes of the default and latest developments

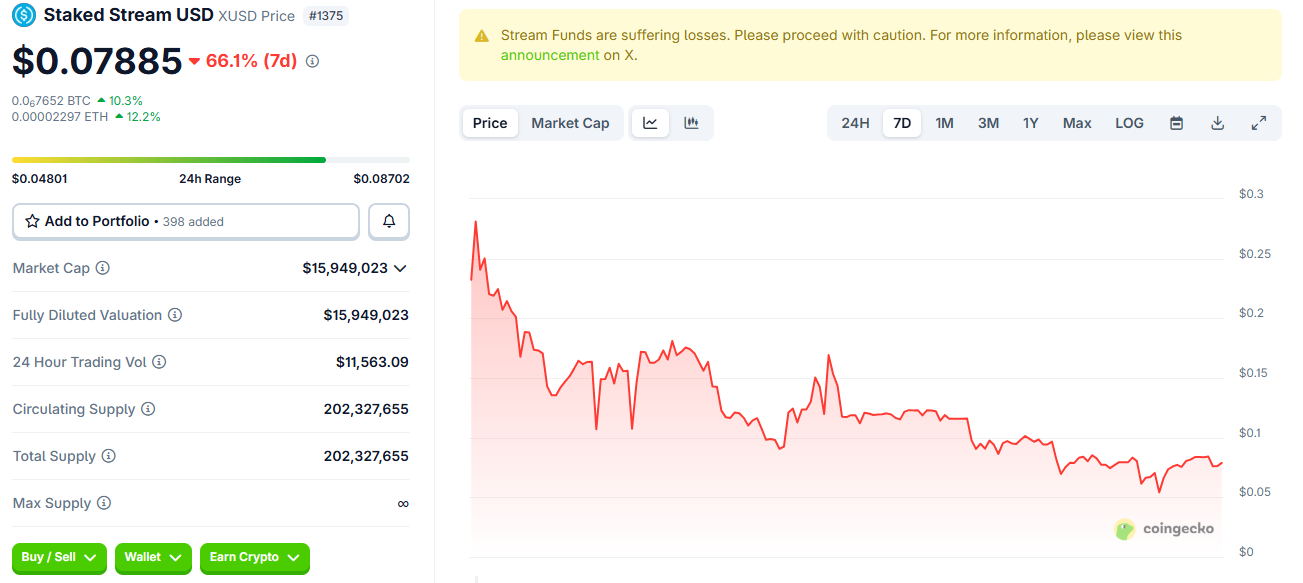

The immediate trigger for this collapse was a liquidity crisis stemming from a combination of external asset management errors and the leveraged structure of the protocols. On November 3, Stream Finance disclosed that its outsourced fund managers had incurred losses of approximately $93 million; subsequently, on November 4, it suspended all deposit and withdrawal operations. Due to the highly cyclical use of protocol assets, this off-chain loss rapidly weakened collateral capacity, triggering liquidations and a panic run. Within just 48 hours, xUSD plummeted from $1 to approximately $0.1, liquidity pools were almost completely emptied, and multiple protocols initiated emergency shutdown and redemption procedures due to the decline in xUSD's value.

As of now, Stream Finance remains in the withdrawal suspension phase and has not yet announced a repayment or redemption plan. The xUSD price has plummeted to approximately $0.079, and market confidence has virtually collapsed. This incident resulted in an outflow of approximately $1 billion from the market, making it one of the largest single systemic risk events in the DeFi sector in 2025. The collapse of Stream Finance not only exposed structural shortcomings within DeFi regarding leverage management, asset disclosure, and liquidity safeguards but also served as a wake-up call for the entire industry.

Source: coingecko

II. Market Chain Reaction

1. Trust Crisis in DeFi Protocols

The collapse of Stream Finance spread like an on-chain contagion, quickly impacting multiple DeFi protocols. According to on-chain tracking data from the DeFi research group YAM, the debt between these protocols reached a staggering $284.9 million. TelosC had the largest exposure, approximately $123.6 million, almost half of Euler's total exposure; MEV Capital had allocated approximately $34 million across multiple lending markets; and Re7 Labs had a total risk of approximately $27.4 million. These institutions, having formed a highly leveraged chain due to over-reliance on synthetic assets issued by Stream, were quickly wiped out after the market derailed.

Meanwhile, Elixir Finance was particularly affected. Approximately 65% of the core collateral for its stablecoin deUSD came from Stream Finance, and Elixir provided Stream with a $68 million loan. After Stream's collapse, Elixir effectively played the dual role of creditor and collateral dependency, creating a classic circular dependency. When xUSD crashed, the collateral value of deUSD was almost wiped out, and the pegging mechanism completely failed. On November 6th, Elixir announced the permanent cessation of deUSD services and established a 1:1 USDC redemption channel for remaining holders. Subsequently, protocols such as Morpho were also affected.

2. On-chain capital flight

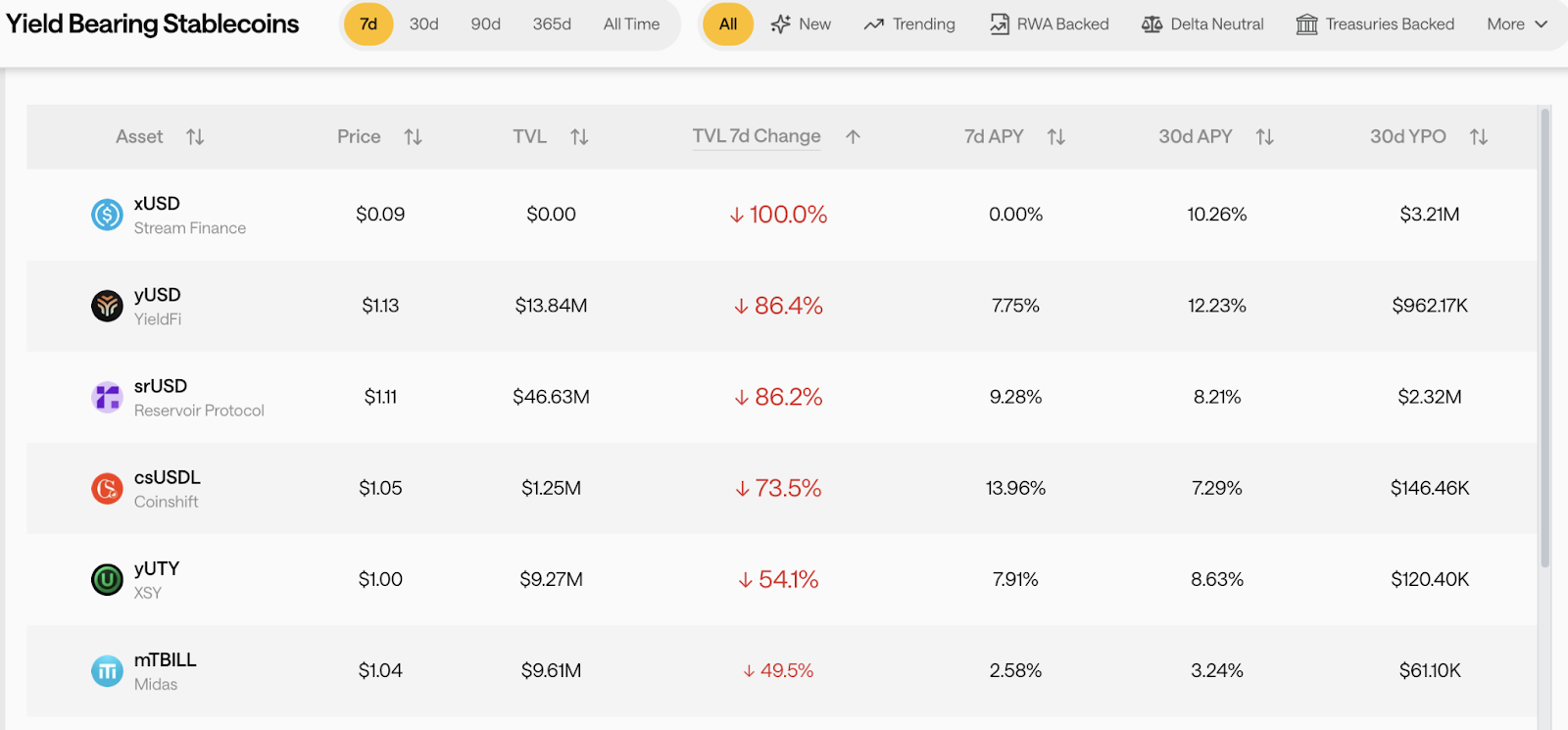

The Stream Finance incident triggered a chain of liquidations that quickly escalated into a wave of capital flight from the industry. In the first week of November, the total value locked (TVL) in DeFi plummeted from approximately $150 billion to $130 billion in a short period, while the total market capitalization of stablecoins shrank by about $2.5 billion during the same period. The yield-based stablecoin sector was hit the hardest, with xUSD's TVL nearly reaching zero, and the TVL of similar assets such as yUSD, srUSD, and csUSDL falling by about 80% within a week. Some liquidity pools experienced outflows exceeding 60%, and market risk aversion rapidly intensified.

Source: stablewatch

In addition, on-chain wealth management and yield aggregation protocols have also been impacted, with the capital structure rapidly shifting from high-yield and high-leverage to stable-yield and low-risk options. Funds are clearly flowing to larger, more transparent, and more reputable protocol layers. Currently, the size of related liquidity pools managed by major fund managers has shrunk by nearly $2 billion in just one week. Overall, this event has not only weakened trust in specific products and protocols but has also prompted a profound restructuring of risk pricing and capital allocation across the entire DeFi ecosystem.

Source: defillama

III. Related Thoughts

1. The False Stability of Yield-Based Stablecoins

The Stream Finance incident revealed a long-standing structural paradox in yield-generating stablecoins: while masquerading as stable, they inherently embed a high-risk return logic. The returns of products like xUSD and deUSD largely rely on leverage cycles, outsourced fund management, and market spreads. They perform steadily in favorable market conditions, but their anchoring mechanism collapses rapidly once the collateralized assets fluctuate or the strategy fails. This incident signifies that the risk of these assets has moved from theory to real-world impact, exposing that their "stability" is more of a facade. In essence, yield-generating stablecoins are closer to yield certificates with principal risk. Their prosperity is built on leverage expansion and speculative liquidity; once liquidity contracts, the system's vulnerabilities are exposed.

A deeper problem lies in the fact that the value system of these stablecoins has long been detached from real economic activity. Their returns primarily derive from on-chain fund circulation and interest rate arbitrage, rather than basic needs like payments or settlements. Therefore, their stability does not stem from real transaction support but relies on continuous capital inflows and market confidence. When yield-driven mechanisms replace functional needs, the anchoring logic loses its foundation. To rebuild trust, these assets should return to real-world use cases and verifiable reserves, through transparent collateral structures, on-chain reserve proofs, and strict redemption mechanisms, ensuring stability is built on actual capital and liquidity supply, rather than a narrative of high returns.

2. The Systemic Crisis and Reconstruction Path of DeFi

The ongoing Stream Finance incident presents the DeFi ecosystem with another dual test of trust and structural issues. In the past, the development of some DeFi protocols relied on a cyclical model of high yields, liquidity expansion, and re-collateralization, resulting in typical characteristics of over-financialization. Under this model, collateral assets are repeatedly used, yield certificates are constantly generated, and fund flows between protocols are nested. This structure is seen as a symbol of efficiency during market upturns, but when confidence wavers, liquidity contractions rapidly amplify systemic vulnerabilities, intensify liquidation pressures, and trigger chain reactions.

It's worth noting that the DeFi market's trust system has been severely damaged by the combined impact of the 10/11 market turmoil and the Stream Finance collapse. On-chain data shows that funds are continuously flowing out of mainstream protocols, liquidity in some high-yield pools is declining rapidly, and liquidation risks may not yet be fully released. This crisis not only reflects the risk management deficiencies of individual projects but also exposes deep-seated problems in the entire DeFi system, such as excessive leverage and lack of reserve auditing. To overcome this crisis of trust, DeFi must return to the essence of finance, establishing on-chain verifiable proof-of-reserve, independent risk isolation pools, and automated governance frameworks to rebuild a transparent, robust, and sustainable financial foundation. Only with visible risks and robust mechanisms can DeFi regain the long-term trust of capital and users.