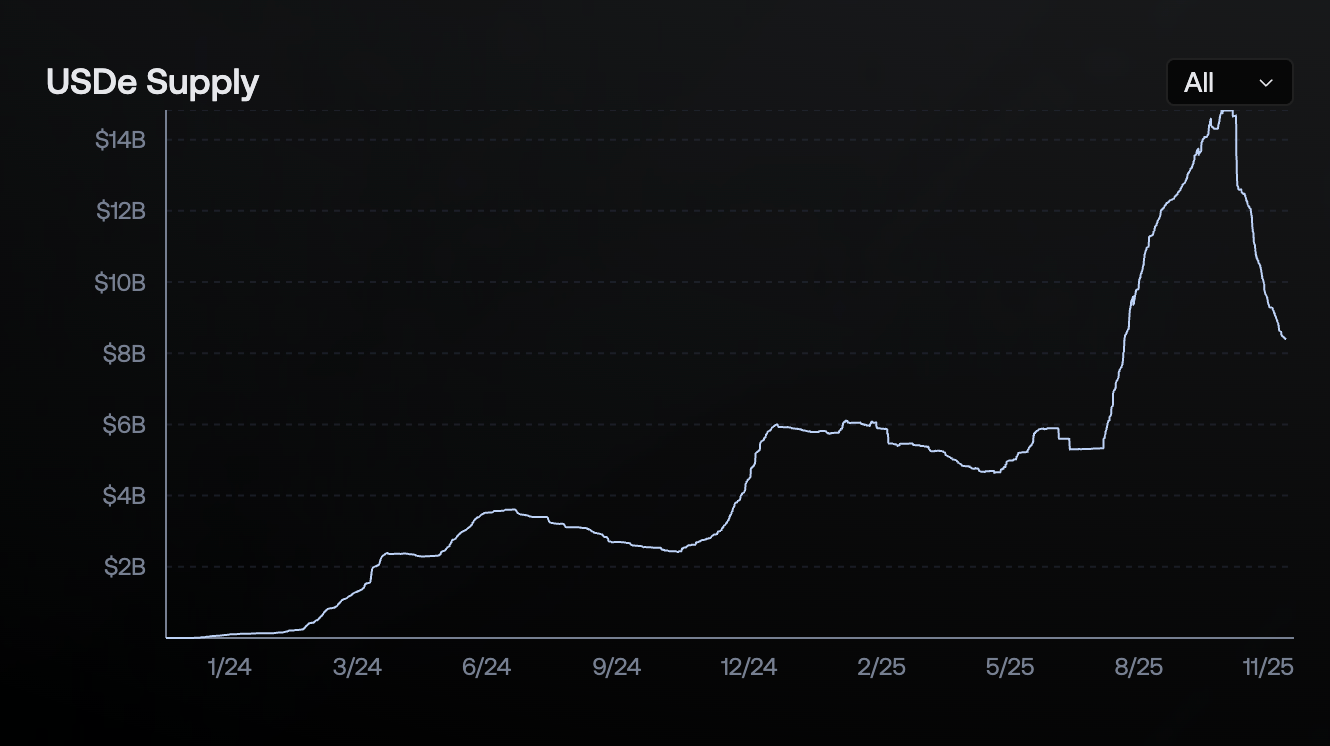

USDe issuance plummeted by $6.5 billion; will Ethena still dare to use it?

- 核心观点:Ethena资金外流主因是收益率下降。

- 关键要素:

- USDe流通量较峰值缩水65亿枚。

- 套利空间缩小致年化收益降至4.64%。

- 循环贷风险意识提高加速资金撤离。

- 市场影响:引发对Delta中性稳定币模型可持续性质疑。

- 时效性标注:中期影响

Original article | Odaily Planet Daily ( @OdailyChina )

Author|Azuma ( @azuma_eth )

Ethena is experiencing the largest outflow of funds since its inception.

On-chain data shows that the circulating supply of Ethena’s main stablecoin product, USDe, has fallen to 8.395 billion, a decrease of about 6.5 billion from the peak of nearly 14.8 billion in early October . Although it cannot be described as a “halving”, the decline is still quite alarming.

Coinciding with the recent spate of DeFi security incidents, especially the collapses of two interest-bearing stablecoins, Stream Finance (xUSD) and Stable Labs (USDX), which claimed to use a similar Delta neutral model to Ethena, there are rumors that the trigger for their collapses may have been the forced disruption of their neutral balance by the CEX's ADL during the bloodbath on October 11. Coupled with the vivid memory of USDe briefly deviating from its peg on Binance, there is currently a large-scale FUD (Fear, Uncertainty, and Debt) sentiment surrounding Ethena.

- Odaily Note: For the story of Stream Finance and Stable Labs and their related impacts, please refer to " On-Chain Finance, Danger! Run !"

Is USDe still safe?

Given Ethena's current market size, any unforeseen event could potentially trigger a black swan event comparable to Terra's collapse... So, is Ethena actually in trouble? Is the capital outflow truly driven by risk aversion? Is it still safe to continue allocating funds to USDe and its derivatives?

To put it simply, I personally believe that: Ethena's current strategy is still operating normally; while the risk aversion surrounding DeFi has exacerbated the outflow of funds from Ethena to some extent, it is not the main reason; USDe's current security situation remains relatively stable, but I suggest avoiding revolving loans as much as possible.

There are two main reasons why we approve of Ethena's current operational status.

Firstly, unlike most interest-bearing stablecoins that fail to clearly disclose their position structure, leverage ratios, hedging exchanges, and even liquidation risk parameters, Ethena sets an industry benchmark in transparency . You can clearly see reserve information and proof, position distribution and percentage, and implementation returns directly on the Ethena website.

The second point concerns the imbalance caused by ADL (Alternative Demand) in neutral strategies, as mentioned earlier. Rumors suggest Ethena has ADL exemption agreements with some exchanges, but this has never been confirmed, so we'll leave it aside for now. Even without exemptions, Ethena is practically less affected by ADL. Its publicly available strategies show that Ethena primarily uses BTC, ETH, and SOL as hedging assets (BNB, HYPE, and XRP have very small proportions). These three assets experienced relatively low volatility during the October 11th crash, and their counterparties have greater capacity to withstand the impact. ADL is actually more likely to occur in the more volatile altcoin market with lower counterparty capacity. Therefore, those protocols that are currently experiencing collapses are often those that lack transparency (possibly due to overly aggressive or even completely non-neutral strategies).

The main reasons for Ethena's capital outflow can also be attributed to two points. First, as market sentiment cooled (especially after October 11), the basic arbitrage space between the futures and spot markets narrowed, causing the protocol yield and the annualized yield of sUSDe (which had dropped to 4.64% as of this writing) to decrease simultaneously . Compared with the base interest rates of mainstream lending markets such as Aave and Spark, it no longer had a significant advantage, so some funds chose other interest-earning paths. Second, the price fluctuation of USDe on Binance on October 11 increased market awareness of the risks of revolving loans. In addition, the decline in yields on both the off-chain (CEX reduced subsidies) and on-chain ends led to a large number of funds being released from revolving loans and withdrawn.

Based on the above logic, we believe that Ethena and USDe are currently maintaining a relatively stable operating state. Although the outflow of funds in this round exceeded expectations to some extent due to the impact of extreme market conditions and market security events, the main reason can still be attributed to the reduced attractiveness caused by the shrinking arbitrage space under the cold market sentiment. This is precisely determined by the design logic of Ethena - the protocol yield and the attractiveness of funds will fluctuate in tandem with the fluctuation of the market environment.

An even more severe test: scalability

Compared to the temporary outflow of funds, the more serious problem facing Ethena is that its Delta-neutral model, which relies on the perpetual contract market, seems to have reached a bottleneck in terms of scalability.

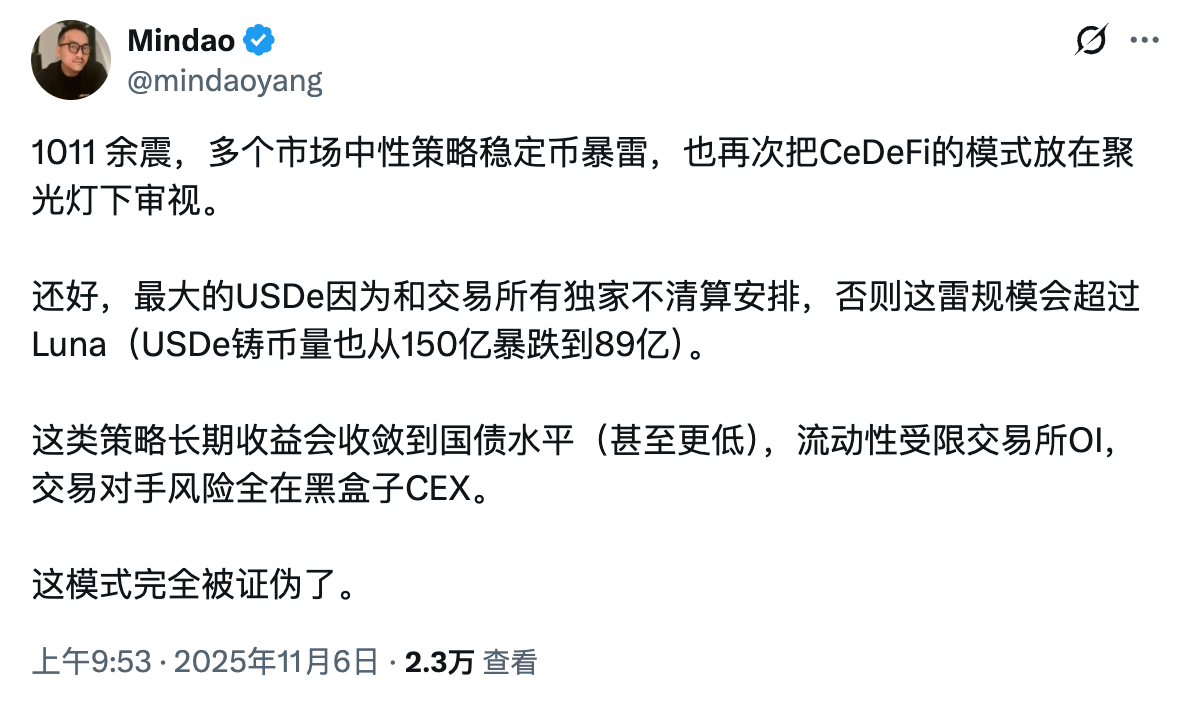

On November 6th, DeFi expert Mindao commented on the recent collapses of neutral strategy stablecoins, stating: "The long-term returns of this type of strategy will converge to the level of government bonds (or even lower), liquidity is limited by exchange-traded inquiries (OI), and counterparty risk is entirely contained in the black box of centralized exchanges (CEXs). This model has been completely disproven... They cannot scale and will ultimately remain niche financial products, unable to compete with fiat stablecoins."

This is similar to The Truman Show. Ethena once thrived in a small, limited world, but this small world was confined by factors such as the size of the perpetual contract market positions and the liquidity and infrastructure of the trading platform. In contrast, USDT, which Ethena aspires to challenge, exists in the unrestricted world outside . This inherent difference in growth environment may be the biggest challenge facing Ethena.