With the rise of stablecoins, can Bitcoin's "currency payment dream" still be realized?

- 核心观点:比特币是数字美元革命的理想载体。

- 关键要素:

- 比特币高度去中心化,安全性强。

- 闪电网络提供即时结算和隐私保护。

- 稳定币创造美债需求,扩大美元使用。

- 市场影响:推动比特币成为全球金融基础设施。

- 时效性标注:长期影响

Original author: Juan Galt

Original translation: AididiaoJP, Foresight News

As the GENIUS Act solidifies the position of stablecoins backed by U.S. Treasuries, Bitcoin’s decentralized network makes it a more suitable blockchain for global adoption and counters the trend of declining demand for U.S. bonds in a multipolar world.

As the world shifts from a unipolar order dominated by the United States to a multipolar landscape led by the BRICS, the US dollar faces unprecedented pressure due to declining demand for bonds and rising debt costs. The GENIUS Act, passed in July 2025, marked a bold US strategy to address this situation: legislating the creation of a stablecoin backed by US Treasury bonds, thereby unleashing massive overseas demand for US bonds.

The blockchains that power these stablecoins will shape the global economy for decades to come. Bitcoin, with its unparalleled decentralization, the privacy of the Lightning Network, and robust security, is a superior choice to power this digital dollar revolution, ensuring low conversion costs when fiat currencies inevitably decline. This article explores why the dollar must and will be digitized via blockchain, and why Bitcoin must serve as its rails for a soft landing for the US economy from its perch as a global empire.

The end of the unipolar world

The world is transitioning from a unipolar world order (where the United States was the sole superpower, able to influence markets and dictate global conflicts) to a multipolar world, in which an Eastern alliance of nations is able to organize itself independently of US foreign policy. This Eastern alliance, known as the BRICS, comprises major countries such as Brazil, Russia, China, and India. The inevitable consequence of the BRICS's rise is a geopolitical realignment that poses a challenge to the hegemony of the US dollar system.

There are many seemingly isolated data points that suggest this realignment of the world order, such as the US military alliance with Saudi Arabia. The US no longer defends the petrodollar agreement, which stipulated that Saudi oil be sold exclusively in US dollars in exchange for US military support for the region. The petrodollar strategy, a major source of demand for the US dollar and considered key to US economic power since the 1970s, has effectively ended in recent years, with Saudi Arabia beginning to accept currencies other than the US dollar for oil-related trade, at least since the start of the war in Ukraine.

Weakness in the U.S. bond market

Another key data point in the geopolitical shift in the world order is weakness in the U.S. bond market, which is increasingly skeptical of the U.S. government's long-term creditworthiness. Some worry about domestic political instability, while others question whether the current government structure can adapt to the rapidly changing high-tech world and the rise of the BRICS nations.

Musk, who abruptly retired from politics in May after spending months with the Trump administration trying to restructure the federal government and the country's finances through the Department of Government Efficiency, is said to be among the skeptics.

Musk recently stunned the internet during an appearance at a summit, saying, “I haven’t been to Washington since May. The government is essentially hopeless. I applaud David Sachs for his noble efforts… But at the end of the day, if you look at our national debt… If AI and robots don’t solve our national debt problem, we’re screwed.”

If even Musk can't save the US government from its financial doom, who can?

These concerns are reflected in low demand for long-term U.S. bonds, which requires higher interest rates to attract investors. The yield on the 30-year U.S. Treasury bond is currently at 4.75%, a 17-year high. According to Reuters, demand for auctions of longer-term bonds, such as the 30-year bond, is also declining, with demand in 2025 being "disappointing."

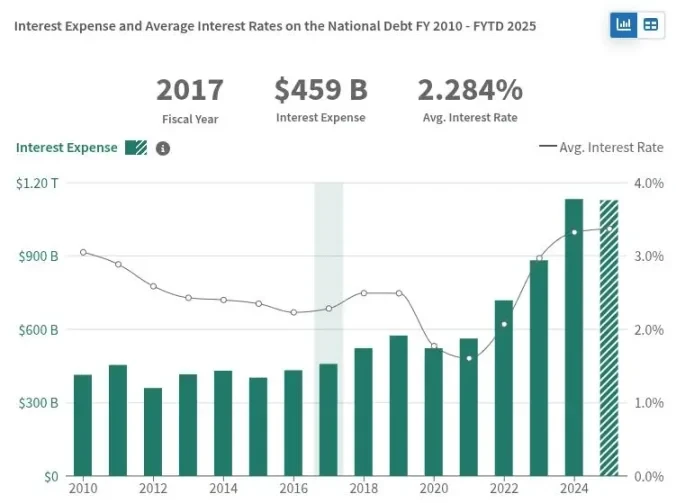

The weakening demand for long-term U.S. bonds has a significant impact on the U.S. economy. The U.S. Treasury must offer higher interest rates to attract investors, which in turn increases the interest the U.S. government must pay on its debt. Today, U.S. interest payments approach $1 trillion annually, exceeding the nation's entire military budget.

If the US fails to find enough buyers for its future debt, it may struggle to pay its current bills and will be forced to rely on the Federal Reserve to purchase these debts, which would expand its balance sheet and the money supply. While the impact would be complex, it is likely to lead to dollar inflation, further damaging the US economy.

How sanctions have hammered the bond market

Further weakening the U.S. bond market was the 2022 manipulation of the bond markets it controls against Russia in response to its invasion of Ukraine. At the time of the Russian invasion, the United States froze Russian Treasury reserves held overseas, which had been intended to be used to repay Russian debts to Western investors. In an effort to force Russia into default, the United States also reportedly began blocking all attempts by Russia to repay its debts to foreign bondholders.

A U.S. Treasury spokeswoman confirmed at the time that certain payments were no longer allowed.

"Today is the deadline for Russia to make another debt payment," the spokesman said.

"Effective today, the U.S. Treasury will not allow any payments on Russian government dollar debt to be made from accounts held at U.S. financial institutions. Russia must choose between depleting its remaining dollar reserves or new sources of revenue, or defaulting on its obligations."

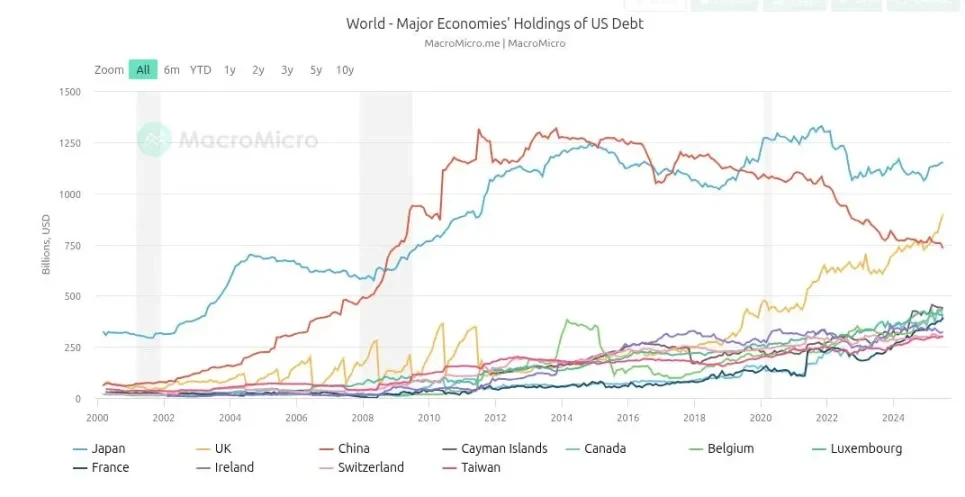

The United States effectively weaponized the bond market against Russia by employing its foreign policy sanctions regime. But sanctions are a double-edged sword: Since then, foreign demand for U.S. bonds has weakened as countries at odds with U.S. foreign policy seek to diversify their risk. China has led this trend away from U.S. bonds, with its holdings peaking at over $1.25 trillion in 2013 and declining rapidly since the start of the war in Ukraine, currently nearing $750 billion.

While this episode demonstrated the devastating effectiveness of sanctions, it also deeply damaged confidence in the bond market. Not only was Russia prevented from repaying its debts under the Biden administration's sanctions, harming investors as collateral damage, but the freezing of its foreign treasury reserves showed the world that if you, as a sovereign nation, go against U.S. foreign policy, all bets are off, including in the bond market.

The Trump administration has moved away from sanctions as a primary tactic, as they harm the U.S. financial sector, and has shifted to a foreign policy approach based on tariffs. These tariffs have had mixed results so far. While the Trump administration has touted record tax revenues and private sector infrastructure investment at home, Eastern countries have accelerated their cooperation through the BRICS alliance.

Stablecoin Strategy Playbook

While China has reduced its holdings of U.S. bonds over the past decade, a new buyer has emerged, rapidly rising to the top. Tether, a fintech company born in the early days of Bitcoin, now owns $171 billion worth of U.S. bonds, nearly a quarter of China’s holdings and more than most other countries.

Tether, the issuer of the most popular stablecoin, USDT, boasts a circulating market capitalization of $171 billion. The company reported a $1 billion profit in the first quarter of 2025. Its business model is simple yet remarkable: it purchases short-term US Treasury bonds, backs them 1:1 with USDT tokens, and pockets the interest from the US government. With 100 employees at the beginning of the year, Tether is said to be one of the most profitable companies per capita in the world.

Circle, the issuer of USDC, the second-most popular stablecoin on the market, also holds nearly $50 billion in Treasury bills. Stablecoins are used around the world, particularly in Latin America and developing countries, as alternatives to local fiat currencies, which suffer from far greater inflation than the US dollar and are often hampered by capital controls.

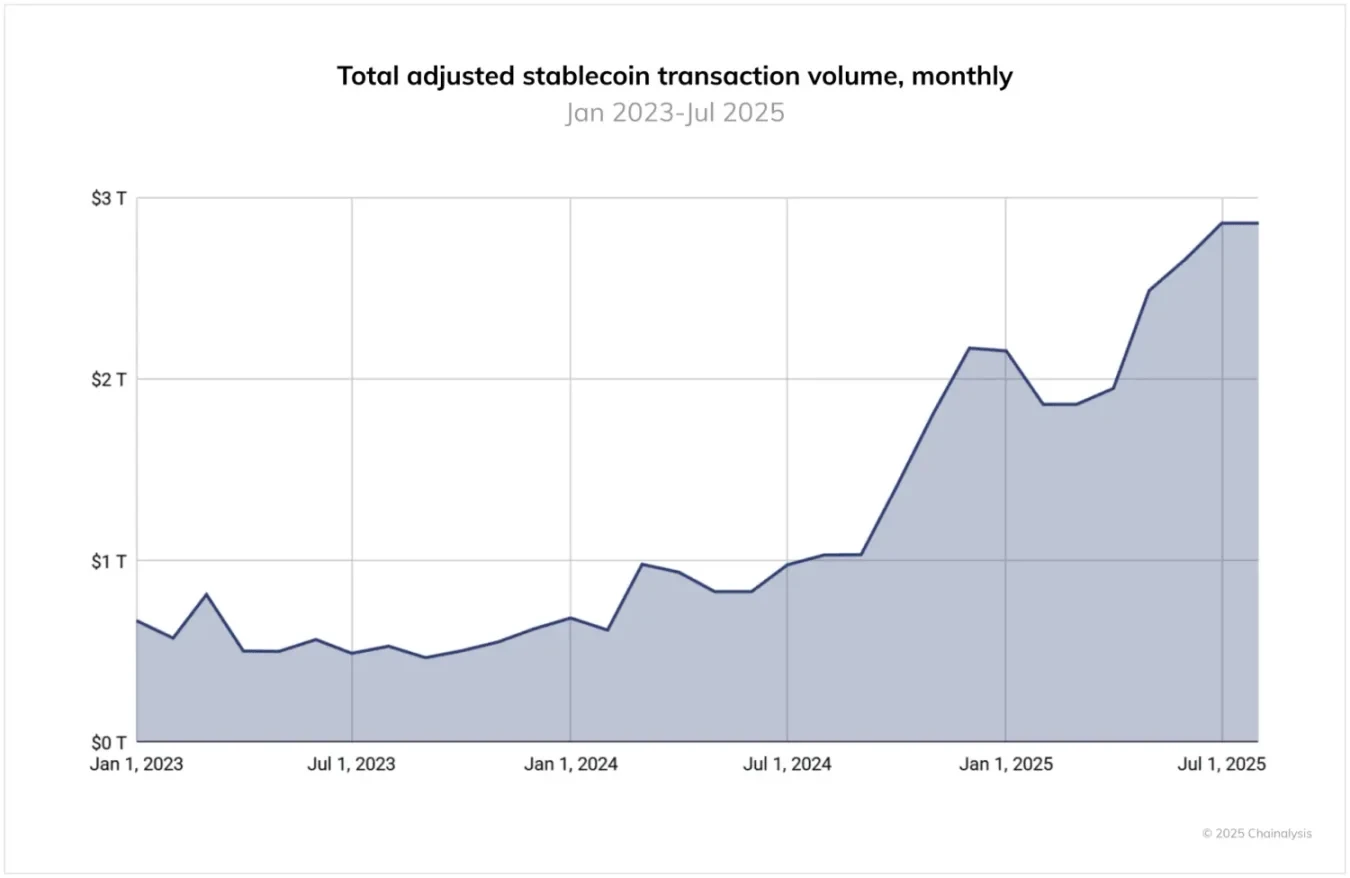

Stablecoins are no longer niche, geeky financial toys; they process trillions of dollars in transactions. A 2025 Chainalysis report noted: "Between June 2024 and June 2025, USDT processed over $1 trillion per month, peaking at $1.14 trillion in January 2025. Meanwhile, USDC processed between $1.24 trillion and $3.29 trillion per month. These volumes highlight the continued centrality of Tether and USDC to crypto market infrastructure, particularly in cross-border payments and institutional activity."

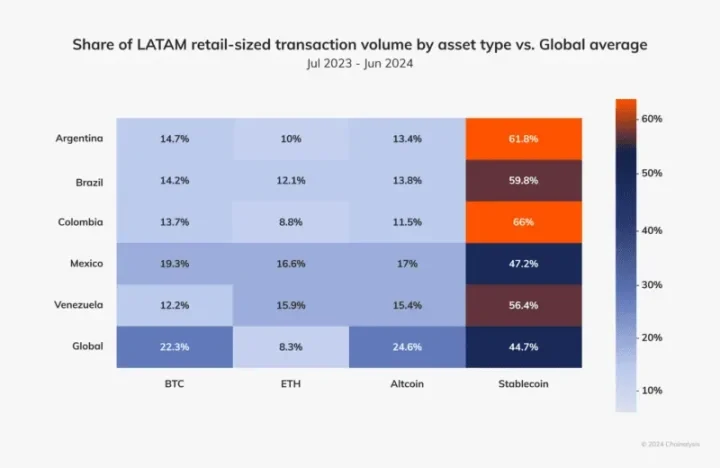

For example, according to a 2024 Chainalysis report focused on Latin America, Latin America accounted for 9.1% of the total crypto value received between 2023 and 2024, with annual usage growth rates ranging from 40% to 100%, with more than 50% of this being stablecoins, demonstrating strong demand for alternative currencies in the developing world.

The United States needs new demand for its bonds, and that demand will come in the form of the dollar, because most of the world's population is trapped in fiat currencies that are far inferior to the US. If the world shifts to a geopolitical structure that forces the dollar to compete on equal terms with all other fiat currencies, the dollar may still be the best of them all. Despite its flaws, the United States remains a superpower with staggering wealth, human capital, and economic potential, especially when compared to many smaller countries and their questionable pesos.

Latin America has demonstrated a deep desire for dollars, but supply is a challenge as local governments resist traditional banking access to the currency. Obtaining a dollar-denominated account in many countries outside the United States is challenging. Local banks are often heavily regulated and answer to local governments, which also have an interest in maintaining their pesos. After all, the United States isn't the only government known for printing money and protecting its currency's value.

Stablecoins solve both of these problems; they create demand for U.S. bonds and enable the transfer of dollar-denominated value to anyone, anywhere in the world.

Stablecoins leverage the censorship-resistant nature of their underlying blockchains, a feature that local banks cannot offer. Therefore, by promoting stablecoins, the US can reach unreached foreign markets, expanding its demand and user base, while also exporting dollar inflation to countries that have no direct influence on US politics, a long-standing tradition in the history of the US dollar. From a strategic perspective, this sounds ideal for the US and is a simple extension of the way the US dollar has operated for decades, simply built on new financial technologies.

The US government understands this opportunity. According to Chainalysis, “The stablecoin regulatory landscape has evolved significantly over the past 12 months. While the US GENIUS Act has not yet taken effect, its passage has already driven strong institutional interest.”

Why Stablecoins Should Overtake Bitcoin

The best way to ensure Bitcoin escapes mediocre fiat currencies in the developing world is to ensure the US dollar uses Bitcoin as its rails. Every dollar stablecoin wallet should also be a Bitcoin wallet.

Critics of the Bitcoin-to-Dollar strategy would argue that this goes against Bitcoin's libertarian roots, that Bitcoin is supposed to replace the dollar, not enhance it or bring it into the 21st century. However, this concern is largely centered on the United States. It's easy to condemn the dollar when you're paid in it and your bank account is denominated in dollars. It's easy to criticize it when the 2-8% dollar inflation rate is your local currency. In too many countries outside the United States, an annual inflation rate of 2-8% is a blessing.

A large portion of the world's population suffers from fiat currencies far worse than the US dollar, with inflation ranging from low double digits to high double digits, even triple digits. This is why stablecoins have already gained mass adoption in the developing world. The developing world needs to get off this sinking ship first. Once they're on a stable ship, they may start looking for ways to upgrade to the Bitcoin yacht.

Unfortunately, despite their origins as Bitcoin, most stablecoins today don’t run on top of it, a technical reality that creates significant friction and risk for users. The majority of stablecoin trading volume today runs on the Tron blockchain, a centralized network run by Justin Sun on a handful of servers, making him an easy target for foreign governments that don’t like the spread of dollar-denominated stablecoins within their borders.

The blockchains upon which most stablecoins operate today are also completely transparent. The public addresses that serve as user accounts are publicly traceable, often linked to users' personal data by local exchanges, and easily accessible to local governments. This provides leverage that foreign countries can use to counter the spread of dollar-denominated stablecoins.

Bitcoin doesn't face these infrastructure risks. Unlike Ethereum, Tron, Solana, and others, Bitcoin is highly decentralized, with tens of thousands of nodes worldwide and a robust peer-to-peer network for transmitting transactions, easily circumventing any bottlenecks or obstructions. Its proof-of-work layer provides a separation of powers not found in other proof-of-stake blockchains. For example, Michael Saylor, despite holding a significant amount of Bitcoin (3% of the total supply), has no direct voting power in the network's consensus politics. This is not the case with Vitalik and Ethereum's proof-of-stake consensus, or Justin Sun and Tron.

Furthermore, the Lightning Network, built on top of Bitcoin, unlocks instant transaction settlement, benefiting from the security of Bitcoin's underlying blockchain. It also provides users with significant privacy, as all Lightning Network transactions are designed to be off-chain and leave no trace on its public blockchain. This fundamental difference in payment methods allows users to maintain privacy when sending funds to others. This reduces the number of threat actors capable of violating user privacy from anyone with access to the blockchain to, at worst, a handful of entrepreneurs and tech companies.

Users can also run their own Lightning nodes locally and choose how to connect to the network, and many do so, taking privacy and security into their own hands. These features are not seen in the blockchains that most people use for stablecoins today.

Compliance policies and even sanctions could still be applied to dollar-denominated stablecoins, whose governance is anchored in Washington, using the same analytical and smart contract-based approaches used today to deter criminal use of stablecoins. Fundamentally, a stablecoin like the US dollar cannot be decentralized; after all, it is centralized by design. However, if the majority of stablecoin value were transferred via the Lightning Network instead, user privacy could be maintained, protecting users in developing countries from organized crime and even their local governments.

End users care about transaction fees—the cost of transferring funds—which is why Tron has dominated the market to date. However, with the launch of USDT on the Lightning Network, this situation may soon change. In a Bitcoin-Dollar world order, the Bitcoin network will become the medium of exchange for the US dollar, which will remain the unit of account for the foreseeable future.

Can Bitcoin withstand all this?

Critics of the strategy also worry about the potential impact of a Bitcoin-for-Dollar strategy on Bitcoin itself. They wonder whether placing the dollar on top of Bitcoin would distort its underlying structure. The most obvious way a superpower like the US government might want to manipulate Bitcoin is by forcing it to comply with sanctions regimes, which they could theoretically do with the proof-of-work layer.

However, as mentioned earlier, the sanctions regime has arguably reached its peak, giving way to an era of tariffs, which seek to control the flow of goods rather than capital. This strategic shift in US foreign policy, post-Trump and post-Ukraine war, has actually taken some pressure off Bitcoin.

As Western companies like BlackRock and even the U.S. government continue to hold Bitcoin as a long-term investment strategy, or as President Trump puts it, as a “strategic Bitcoin reserve,” they are also becoming aligned with the future success and survival of the Bitcoin network. Attacking Bitcoin’s censorship-resistant properties would not only undermine their investment in the asset, but also undermine the network’s ability to deliver stablecoins to the developing world.

In a Bitcoin-dollar world order, the most obvious compromise Bitcoin would have to make is abandoning the unit of account dimension of currency. This is bad news for many Bitcoin enthusiasts, and rightly so. The unit of account is the ultimate goal of hyperbitcoinization, and many of its users live in that world today, calculating economic decisions based on the ultimate impact on the number of satoshis they hold. However, for those who understand Bitcoin as the soundest money ever created, nothing can truly take away from this. Indeed, the belief in Bitcoin as a store of value and medium of exchange will be strengthened by this Bitcoin-dollar strategy.

Sadly, after 16 years of trying to make Bitcoin a unit of account as ubiquitous as the US dollar, some are realizing that in the medium term, the US dollar and stablecoins are likely to fulfill that use case. Bitcoin payments will never disappear, and companies led by Bitcoin enthusiasts will continue to rise and should continue to accept Bitcoin as a payment method to build their Bitcoin reserves, but stablecoins and US dollar-denominated value will likely dominate crypto commerce for decades to come.

Nothing can stop this train

As the world continues to adjust to the rise of Eastern power and the emergence of a multipolar world order, the United States may have to make difficult and critical decisions to avoid a protracted financial crisis. Theoretically, the United States could reduce spending, pivot, and restructure to become more efficient and competitive in the 21st century. The Trump administration is certainly attempting to do so, as demonstrated by its tariff regime and other efforts to bring manufacturing back to the United States and cultivate local talent.

While there are a few miracles that might solve America’s fiscal woes, like sci-fi labor and smart automation, or even a Bitcoin dollar strategy, ultimately, even putting the dollar on a blockchain won’t change its fate: becoming a collectible for history buffs, a rediscovered token of an ancient empire fit for a museum.

The dollar’s centralized design and dependence on American politics ultimately doom it as a currency, but if we’re realistic, its demise may not occur for 10, 50, or even 100 years. When that moment does arrive, if history repeats itself, Bitcoin should be there as the running track, ready to pick up the pieces and fulfill the prophecy of hyperbitcoinization.