Coinbase Panorama Report: The Current Status, Risks, and Valuation of the Leading US Compliant Exchange

- 核心观点:Coinbase是加密行业龙头,兼具机遇与挑战。

- 关键要素:

- 合规与品牌优势显著。

- 收入多元化,抗周期增强。

- 财务稳健,现金充裕。

- 市场影响:推动行业合规化与主流化进程。

- 时效性标注:中期影响。

Original title: Coinbase Panorama Report: The Current Status, Risks, and Valuation of the Leading US Compliance Trading Platform

Original article by Alex Xu, Mint Ventures

1. Research Summary

As the global leader in cryptocurrency trading and services, Coinbase is one of the core targets for capturing the long-term development dividends of the cryptocurrency industry with its brand trust, broad user base, diversified products and early layout in compliance.

Specifically:

It has a long history and brand reputation in compliant operations, safety, and reliability, and has numerous institutional partners, which helps it attract a wider range of institutional and mass customer groups.

Diversified income streams, such as subscriptions and interest, are developing well, providing a more diversified business model that no longer relies solely on fees, and its resilience to cyclical fluctuations has improved compared to the past.

A healthy balance sheet with low debt and ample cash on hand provides the company with both a buffer and offensive capabilities in the face of technological innovation, international expansion, and headwinds.

Sovereign nations, such as the United States, tend to be more relaxed in their overall regulation of cryptocurrencies and encourage innovation. Long-term industry trends continue to point to growth, and blockchain and digital assets are expected to be increasingly integrated into mainstream finance. Coinbase has a strong position in key industry sectors.

However, although the fluctuations in its revenue and profits with the industry cycle have slowed down compared with the previous cycle, it is still difficult to avoid large fluctuations (see Section 6 Operations and Financial Performance for details). This situation has been very obvious in the financial reports of the latest two quarters.

In addition, Coinbase is in a highly competitive arena. In the domestic US market, it faces direct competition from Robinhood and Kraken, and overseas it has to fight with a large number of offshore crypto exchanges such as Binance. Decentralized trading platforms such as Uniswap and on-chain exchange Hyperliquid are also developing rapidly and are challenging the market share of traditional CEX.

It is worth mentioning that in this bull market cycle, Coinbase has risen by more than 11 times from its historical low in 22 years, which is far greater than the increase of BTC in the same period, and has also outperformed most crypto assets.

It can be said that the competitive challenges faced by Coinbase coexist with the opportunities of the times. This report is Mint Ventures' first coverage of Coinbase, and we will continue to follow it in the long term.

PS: This article represents the author's interim thinking at the time of publication. It may change in the future, and the views are highly subjective. There may also be errors in facts, data, and reasoning logic. All views in this article are not investment advice. We welcome criticism and further discussion from colleagues and readers.

2. Company Overview

2.1 Development History and Milestones

Coinbase was founded in 2012 by Brian Armstrong and Fred Ehrsam and is headquartered in San Francisco. Initially, the company focused on Bitcoin brokerage services and received one of the first Bitcoin trading licenses (BitLicenses) issued by New York State in 2014.

Since then, Coinbase has continuously expanded its product portfolio: in 2015, it launched the exchange platform "Coinbase Exchange" (later renamed Coinbase Pro), and in 2016, it began supporting the trading of various crypto assets, including Ethereum. In 2018, it entered the blockchain application field through the acquisition of businesses such as Earn.com, and brought in former LinkedIn executive Emilie Choi to lead the M&A expansion. In 2019, it acquired the institutional business of custodian Xapo, solidifying its leading position in custody services. That same year, the company's valuation exceeded $8 billion. On April 14, 2021, Coinbase successfully listed on the Nasdaq, becoming the first (and to date, only) major exchange in the crypto industry to do so, with a market capitalization of over $85 billion at one point. After its IPO, the company continued to expand its global presence and diversify its product line. In 2022, it acquired the futures exchange FairX and entered the crypto derivatives market, launching an NFT market (although trading volume subsequently declined). In 2023, it launched Base, the Ethereum Layer 2 network, strengthening its on-chain ecosystem. In the same year, while actively responding to US regulatory challenges, the company obtained licenses in multiple locations including Singapore, the European Union (Ireland), and Brazil, and in 2025 officially completed the acquisition of Deribit, a leading options trading platform.

After more than ten years of development, Coinbase has grown from a single Bitcoin broker to a crypto financial platform covering comprehensive businesses such as trading, custody, and payment.

2.2 Positioning and Target Customers

Coinbase's mission is to "advance global economic freedom" and its vision is to update the century-old financial system and enable fair and convenient participation in the crypto economy for everyone. The company positions itself as a secure and trusted one-stop platform for crypto assets, attracting mass users through easy-to-use products while also providing institutional-grade services to meet the needs of professional investors.

Coinbase's customer base can be roughly divided into three categories:

Retail users: Individual investors interested in crypto assets. In addition to trading major cryptocurrencies, Coinbase also offers users staking, earning returns, and accessing various other features. Its monthly transacting users (MTU) peaked at 11.2 million in Q4 2021, and even during the trough of 2022–2023, it maintained over 7 million quarterly active users. In Q1 2025, MTUs were approximately 9.2 million, before falling slightly to approximately 9 million in Q2 2025.

Institutional Clients: Coinbase has been focusing on the institutional market since 2017, offering services such as Coinbase Prime brokerage and Coinbase Custody. Its clients include hedge funds, asset managers, and corporate treasuries. By the end of 2021, its institutional client base exceeded 9,000, including 10% of the world's top 100 hedge funds. These institutional clients contribute the vast majority of the platform's trading volume (approximately 81% in 2024). Despite lower fees, they generate stable custody fees and trading revenue.

Developers and Ecosystem Partners: Coinbase considers developers and blockchain projects to be ecosystem customers, supporting blockchain network development through infrastructure like Coinbase Cloud (node services and APIs), and collaborating with new projects through investment and coin listings. Furthermore, the stablecoin USDC was jointly launched by Coinbase and Circle, with Coinbase serving as both the issuing partner and primary distribution platform, sharing a significant portion of the interest margin and channel fees earned from Circle.

Overall, Coinbase has the dual advantages of being public-friendly and institutionally trusted, connecting both the retail and institutional markets and playing the role of a "bridge between fiat currency and the crypto world" in the crypto ecosystem.

2.3 Equity and Voting Rights Structure

The company adopts a dual-class share structure. Class A common stock is listed on the Nasdaq and carries one vote per share; Class B common stock is held by the founders and senior executives, with each share carrying 20 votes. Founder and CEO Brian Armstrong controls over 64% of the voting power through his holdings of approximately 23.48 million Class B shares, making Coinbase a highly controlled company. A small number of early investors, such as Andreessen Horowitz, also hold some Class B shares. In mid-2025, Armstrong converted and sold a small portion of his Class B shares, but still retained approximately 469.6 million votes equivalent to those of Class A shares. Because Class B shares are convertible into Class A shares at any time at a 20:1 ratio, the company's total share capital will fluctuate slightly with each conversion. This dual-class share structure ensures the founding team's control over the company's strategic direction, but it also means that common shareholders have limited influence over corporate governance. In general, Coinbase's equity structure is highly concentrated and the founders have a lot of say, which ensures consistency in the company's long-term vision and strategic direction.

3. Industry Analysis

3.1 Market Definition and Segmentation

Coinbase operates in the broad market for cryptocurrency trading and related financial services . Core areas include:

Spot trading: This refers to the matching of buying and selling crypto assets, and is Coinbase's primary business area. Based on the transaction objects, this market can be further divided into fiat-to-crypto (fiat on-ramp) and crypto-to-crypto trading. Based on customer type, this market can be further divided into retail and institutional trading.

Derivatives trading market: This includes leveraged derivatives trading such as cryptocurrency futures and options. This market has grown rapidly in recent years, with crypto derivatives accounting for approximately 75% of total trading volume in the first half of 2025 (source: Kaiko). Coinbase, a latecomer to the derivatives market, currently operates through regulated futures exchanges and overseas platforms.

Custody and Wallet Services: Provides secure storage solutions for institutions and individuals holding large amounts of crypto assets. The custody market is closely tied to trading, and clients conducting large trades on exchanges often require compliant custody services.

Blockchain Infrastructure and Other: This includes stablecoin issuance and circulation, blockchain operations (Base), payment settlement, staking, and other "blockchain finance" services. This segment expands revenue streams beyond exchanges, such as Coinbase, which earns interest and fees from USDC stablecoins and node staking.

3.2 Historical Scale and Growth Rate (Recent Five Years)

The overall crypto market fluctuates dramatically with the cycle. Measured by trading volume, global crypto trading volume surged from approximately $22.9 trillion in 2017 to $131.4 trillion in 2021, with an extremely high average annual growth rate. Subsequently, in 2022, trading volume fell to $82 trillion (-37% year-on-year) due to a market downturn, and continued to decline slightly in 2023, to $75.6 trillion. In 2024, driven by a new round of market enthusiasm, total trading volume for the year reached a new high of approximately $150 trillion, nearly doubling the 2023 level.

Industry scale is highly correlated with crypto asset prices and volatility. For example, during the 2021 bull market, various token prices soared, leading to active speculative trading and a nearly 196% year-on-year increase in trading volume. In contrast, during the 2022 bear market, prices plummeted and trading volume plummeted by nearly 40%. Regarding user scale, the number of global cryptocurrency holders also fluctuates with market conditions, but the overall trend is upward. According to Crypto.com research, the number of global crypto users has grown from approximately 50 million in 2018 to over 300 million in 2021. After a decline in 2022, it will rebound to around 400 million by the end of 2023.

Coinbase's business has grown along with the industry: in terms of trading volume, its platform's trading volume rose from $32 billion in 2019 to $1.67 trillion in 2021, then shrank to $830 billion in 2022 and further to $468 billion in 2023. In terms of active users, Coinbase's monthly trading users increased from less than 1 million in 2019 to an annual average of 9 million in 2021, before falling back to an average of 7-9 million per quarter in 2022-2023.

In summary, the scale of the industry has shown a medium- to long-term growth trend with significant fluctuations over the past five years.

3.3 Competitive Landscape & Coinbase Market Share (Recent Five Years)

There are many competitors in the crypto trading industry, and the landscape changes with market evolution.

Globally, Binance has rapidly risen to become the largest exchange by trading volume since 2018. Its global spot market share surpassed 50% at the peak of the bull market; at the beginning of 2025, it maintained a roughly 38% share, ranking first. Other major players include OKX, Coinbase, Kraken, Bitfinex, and regional leaders such as South Korea's Upbit. In recent years, rising stars such as Bybit and Bitget have also gained significant market share. Coinbase's global market share fluctuates between 5% and 10%. For example, in the first half of 2025, Coinbase accounted for approximately 7% of the total spot trading volume of the top ten exchanges globally, comparable to OKX, Bybit, and others. In comparison, Binance alone holds several times this share. It's important to note that, due to its focus on the regulated US market, Coinbase avoids extensive altcoin speculative trading, resulting in its global ranking being often surpassed by more aggressive platforms with high-volume listings. However, in the fiat-compliant market, particularly the US, Coinbase holds a clear advantage. Since 2019, Coinbase has consistently ranked first in US trading volume and further increased its US spot and derivatives market share in 2024. With the collapse of competitor FTX in 2022, Coinbase's position in the US has become more solid.

Competitive landscape dynamics

There have been several notable changes over the past five years:

The market share of trading platforms has shifted from concentration to dispersion. After the FTX debacle in 2022, Binance’s market share rose from 48.7% (Q1) to 66.7% (Q4). Since then, the market share has begun to diverge, with Bybit, OKX, Bitget and other platforms starting to increase their market share, and competition has become more intense.

Increased compliance pressure has led to regional differentiation – with fewer competitors in the US market (remaining with only a few such as Coinbase and Kraken), and the rise of Asian platforms (such as Upbit in South Korea and Gate in Southeast Asia);

3.4 Forecast of industry scale and growth rate in the next 5-7 years

Looking ahead to the next five to seven years, the crypto trading industry is expected to continue growing, but the rate of growth will depend on multiple factors and scenario assumptions. Industry research reports (from Skyquest, ResearchAndMarkets, Fidelity, and Grand View Research) generally predict that the crypto market will maintain a double-digit compound annual growth rate. Under the baseline scenario (assuming a stable macroeconomic environment and no significant deterioration in the regulatory environment), the global crypto market capitalization is expected to rise from the current approximately $3 trillion to approximately $10 trillion by 2030, with a corresponding significant increase in trading volume. However, as the market matures, volatility is likely to decline, and trading volume growth will be slightly lower than market capitalization growth, with an average annual growth rate of approximately 15%.

Key growth drivers for the crypto industry include:

Asset price trends: If leading assets such as Bitcoin continue to hit new highs, it will drive the overall market upward. Rising prices and increased volatility will stimulate trading activity, thereby amplifying trading volume.

Derivatives Penetration: Derivatives already account for approximately 75% of the market and are expected to continue to expand. For example, institutional investors are increasingly favoring hedging instruments like futures, while retail investors are also likely to gradually embrace leveraged trading, which will inflate overall trading volume. We assume that by 2030, the proportion of derivatives will rise to 85%, which would increase total trading volume by approximately 1.2 times.

Institutional Entry: If more traditional financial institutions (asset management companies, banks, etc.) enter the crypto market, it could bring trillions of dollars in new capital. For example, the approval of more ETFs, institutional access (currently many institutions are still not allowed to directly hold crypto assets, including ETF shares), and sovereign wealth fund allocations will significantly expand market depth. This will drive simultaneous growth in trading volume and custody demand. Fidelity and other institutions predict that institutional capital is expected to increase the total crypto market capitalization by hundreds of billions of dollars annually over the next few years.

Regulatory Clarity: A clear regulatory framework will reduce market participation concerns and attract more participants. In an optimistic scenario, with appropriate regulation established across major economies (e.g., widespread licensing in developed economies, legalization and expansion of ETFs), the user base and activity will increase. In a pessimistic scenario, if regulatory pressures are implemented (e.g., restrictions on bank support and stricter capital requirements), market growth may be limited or even stagnant. With the passage of the Genius Stablecoin Act in the United States and the passage of the Clarity Act in the House of Representatives, their demonstration effect could gradually radiate to developed economies worldwide. We are eagerly awaiting the overall clarity of crypto policy in the future.

Scenario breakdown: We can construct three scenarios to predict the industry scale in 2025-2030:

Baseline Scenario: Assuming macroeconomic stability, friendly but still cautious regulation in major countries, and gradual investor acceptance of crypto assets, crypto market capitalization will grow by approximately 15% annually, with trading volume increasing by approximately 12%. By 2030, global annual trading volume could reach approximately $300 trillion, with industry revenue (transaction fees) growing in line with trading volume. Market share for leading compliant platforms like Coinbase will steadily increase. This scenario demonstrates healthy industry growth without a frenzy or bubble.

Optimistic scenario: Assume a boom similar to the "internet finance" boom: major economies (particularly the United States) thoroughly clarify industry regulations, large institutions and enterprises enter the market en masse, and crypto technology achieves widespread adoption (e.g., DeFi scale and adoption rates soar). Asset prices soar (for example, Bitcoin could reach $1 million by 2030, as ARK Invest has long-term forecasts), global market capitalization grows by over 20% annually, and trading volume increases by 25% annually. Based on this scenario, total trading volume could reach $600-800 trillion by 2030. Regulatory giants like Coinbase reap enormous profits from this explosive growth, significantly raising the ceiling for the industry.

Pessimistic Scenario: Assuming an unfavorable macroeconomic environment or severe regulatory constraints, for example, major countries introduce stringent restrictions, leading to a prolonged period of sluggishness and volatility in crypto assets. The industry's scale could stagnate, grow only slightly, or even experience years of contraction. In the worst-case scenario, annual trading volume growth could fall to single digits or even stagnate and decline, with total trading volume likely hovering between 100 and 150 trillion yuan by 2030. While regulated exchanges like Coinbase may see their market share increase (due to the withdrawal of shady platforms or a reduction in their share under strict regulation), the absolute growth in business scale will be limited.

Overall, I tend to hold a slightly optimistic outlook: Over the next 5-7 years, the crypto trading industry is expected to continue its cyclical growth, with its overall scale increasing annually. Crypto users and industry conglomerates have become a formidable force in the eyes of political powers worldwide and are one of the primary drivers of the Republican Party's upset victory over the Democratic Party in the 2024 US election. Since this battle, the Democratic Party has become noticeably more moderate on crypto legislation requiring bipartisan cooperation. Many Democratic lawmakers voted in favor of the Genius Act (enacted in both chambers) and the Clarity Act (in the House of Representatives), both of which were passed by Congress.

4. Business and product lines

Coinbase currently has diversified businesses, and its main sources of income can be divided into two major segments: trading and subscriptions and services, under which it has multiple product lines.

The following is an overview of each major business model, core indicators, revenue contribution, profitability and future plans:

· Trading Brokerage (Retail Trading): This is Coinbase's original and core business, providing crypto asset buying and selling services to individual users. Coinbase acts as a broker and matchmaking platform, allowing users to buy and sell cryptocurrencies with a single click through the app or website. Coinbase charges high fees for retail transactions (previously 0.5% of the transaction value plus a flat fee, but after 2022, this will be based on a spread and tiered fee structure; see the PS below for details). Consequently, retail customers have historically contributed the vast majority of the company's trading revenue. For example, in 2021, retail trading volume accounted for approximately 32% of total volume but contributed approximately 95% of revenue (decreasing to 54% in 2024). Key metrics include Monthly Trading Users (MTUs), average trading volume per user, and trading fee levels. MTUs peaked at 11.2 million during the 2021 bull market; they declined to 7 million in 2022-2023 due to the market downturn. The retail trading business is highly profitable, and transaction fee income drives the company's net profit margin high during bull markets (46% in 2021, compared to 42.7% in the past year). However, during bear markets, shrinking trading volume has led to a sharp decline in revenue from this business (retail trading revenue fell by ~66% year-on-year in 2022), dragging down overall profitability. Note: The "spread" in retail trading, charged across the "One-Click Buy/Simple/Convert/Card Spending" transaction categories, refers to the fees embedded in the asset quote—the buy price you pay is slightly above the market price, and the sell price is slightly below the market price. This difference is the "spread." Advanced trading (order maker/taker) uses a tiered fee structure, with higher trading volume over the past 30 days resulting in lower maker and taker fees.

Future Plans: Coinbase is expanding its retail product offerings to increase user stickiness. These efforts include launching the Coinbase One membership service (which offers value-added benefits such as zero-fee credits), continuously listing new tokens (48 new trading assets will be added in 2024, including popular memecoins to attract traffic), and improving the user experience (such as a simpler interface and educational content). The company is also exploring features such as social trading and automated investing. As the market recovers, retail trading will remain the cornerstone of revenue, with its growth dependent on growing crypto market popularity and Coinbase's increasing market share.

Professional Trading and Institutional Brokerage: This segment includes trading services for high-net-worth and institutional clients, such as Coinbase Prime and Coinbase Pro (now integrated into a unified platform). These specialized platforms offer deep liquidity, lower fees, and API access to attract large traders and market makers. While institutional trading accounts for 80-90% of total trading volume (e.g., institutional trading volume reached $941 billion in 2024, representing 81% of total volume), fees are limited to a few ten-thousandths to one thousandth of a percent, resulting in a relatively limited direct revenue contribution (institutional trading revenue accounted for only approximately 10% of total trading revenue in 2024). However, the indirect benefits of institutional business are significant: institutions often retain significant assets in Coinbase custody and participate in staking, contributing to custody fees and interest income. Furthermore, having active institutional investors contributes to the platform's liquidity and pricing advantages, enhancing the trading experience for retail clients.

In terms of core metrics, the number of institutional clients and assets under custody (AUC) are key areas of focus. Coinbase's AUC reached a high of $278 billion in Q4 2021, then fell to $80.3 billion by the end of 2022 amidst market declines. It rebounded to around $145 billion by the end of 2023. Institutional custody maintained strong momentum into 2025: Coinbase's average assets under custody reached $212 billion in Q1 2025, a $25 billion increase from the previous quarter. The second quarter saw a new high of $245.7 billion. Regarding profitability, while institutional trading itself does not directly contribute much to profits, services such as custody and financing can generate additional revenue.

Future Plans: Coinbase is focusing on derivatives to meet the diverse needs of institutions. It plans to launch perpetual futures products overseas in 2023 and obtain futures commission merchant certification in the United States through its brokerage, beginning to offer Bitcoin and Ether futures to US institutions. Coinbase has also established Coinbase Asset Management (formed from the 2023 acquisition of One River Asset Management) and plans to issue crypto investment products such as ETFs and basket indices to increase institutional participation. To strengthen its crypto derivatives offering, Coinbase announced the acquisition of Deribit, a leading global crypto options exchange, at the end of 2024. The transaction value is approximately $2.9 billion, consisting of $700 million in cash and 11 million shares of Coinbase Class A common stock. This acquisition, one of the largest mergers and acquisitions in the crypto industry, is intended to rapidly enhance Coinbase's position and scale in the global crypto derivatives market. As the industry's leading options platform, Deribit's trading volume reached $1.2 trillion in 2024, a 95% year-on-year increase. By integrating Deribit, Coinbase has gained a dominant share of the Bitcoin and Ethereum options markets (Deribit holds over 87% of the Bitcoin options market). This acquisition further expands and complements Coinbase's derivatives product offerings (covering options, futures, and perpetual contracts), solidifying its position as the preferred platform for institutional investors entering the crypto space.

Custody and Wallet Services: Coinbase Custody is an industry-leading, compliant custodial service, primarily providing cold storage and safekeeping for institutional investors. Its custodial business model primarily relies on a custody fee (typically a few basis points of assets held annually) and withdrawal fees. By 2024, Coinbase's custodial assets accounted for 12.2% of the global crypto market capitalization. Its reputation has been further enhanced by the selection of major products such as Grayscale as its custodian. While revenue from this custodial business is consolidated into the "Subscriptions and Services" category in financial reports and is relatively small (US$142 million, representing 2.2% of total revenue of US$6.564 billion for the year), it holds significant strategic significance: custody ensures the security of high-net-worth clients' assets and supports their ability to conduct large-scale transactions on exchanges. Furthermore, Coinbase's wallet service (Coinbase Wallet), while not directly revenue-generating, contributes to the ecosystem and attracts users to on-chain transactions such as DeFi. In terms of profitability, the custody business itself has a high profit margin (almost pure income except for relatively fixed security operation and maintenance costs), and it works in tandem with the trading business. It has been steadily increasing in recent years (in the fourth quarter of 2024, custody fee income reached US$43 million, a month-on-month increase of 36%), providing the company with a more stable source of fee income.

Future Plans: Coinbase will continue to invest in enhancing the security of its custody technology to meet regulatory requirements (e.g., Custody Trust, regulated under the New York Trust License). Coinbase also plans to expand its custody business to more asset classes and regions, such as supporting institutional staking services and ETF custody (Coinbase has been selected as the custodian for several Bitcoin spot ETFs in 2024).

Subscription and service revenue (staking, USDC interest, etc.): This is a diversified revenue segment that Coinbase has focused on cultivating in recent years. It mainly includes:

Staking: Users stake their cryptocurrency on a blockchain through Coinbase, earning block rewards. Coinbase takes a commission (typically around 15%). Staking provides users with passive income, while the platform reaps a share. Since the opening of staking for major cryptocurrencies like Ethereum in 2021, this revenue stream has grown rapidly.

Interest income from stablecoins (USDC): Interest income from USDC has become a significant component of Coinbase's revenue in recent years. In 2023, with rising interest rates and an expansion of USDC reserves, Coinbase earned approximately $695 million in interest from USDC reserves (approximately 22% of total revenue for the year, significantly higher than in previous years). In 2024, due to continued increases in USDC market interest rates and circulation, Coinbase's annual USDC-related interest income increased to approximately $910 million, a 31% increase from 2023. In 2024, USDC interest income accounted for approximately 14% of the company's total revenue, a decrease in proportion but a record high in absolute terms. The Q2 2025 financial report shows that Coinbase's stablecoin interest income has reached $333 million, accounting for 22.2% of quarterly revenue. This stable interest income primarily comes from a 50/50 split between Coinbase and Circle on the interest income generated from USDC reserves. Coinbase receives 100% of all interest earned on USDC stored on the Coinbase platform. As a result, USDC interest has become the fastest-growing and largest single business within Coinbase's subscription and services revenue segment, providing the company with a recurring revenue stream beyond transaction fees.

In 2023, Coinbase and Circle strengthened their strategic partnership, significantly adjusting the existing joint operating model of Centre (the co-founded joint governance body). First, Coinbase acquired an equity stake in Circle for the first time, becoming a minority shareholder. It was disclosed that Circle acquired the remaining 50% stake in Centre Consortium held by Coinbase for approximately $210 million in stock, in exchange for Circle shares of a corresponding value. This transaction increased Coinbase's stake in Circle (the specific percentage was not disclosed, but it gave Coinbase a financial stake and a certain degree of influence). Subsequently, Centre Consortium, the governing body for USDC, was dissolved, and the issuance and governance of USDC was transferred to Circle. Although Circle fully assumed full management of USDC, Coinbase's influence in the USDC ecosystem, as a key shareholder and partner, actually increased: under the new agreement, Coinbase has substantial participation and veto power over major USDC strategies and collaborations. For example, Coinbase holds a veto over Circle's proposed new USDC partnership, ensuring its interests align with the direction of USDC's development. Furthermore, adjustments to the revenue sharing mechanism (such as the aforementioned interest revenue sharing) further align the incentives of both parties in promoting USDC. A series of initiatives have enabled Coinbase to more actively promote USDC adoption: including promoting USDC listings on more blockchains and offering USDC discounts and incentives (such as increasing the yield on USDC holdings) across its international exchange and wallet products. In summary, the 2023 equity investment and agreement adjustments significantly strengthened the alliance between Coinbase and Circle on USDC. Coinbase not only participates deeply in USDC governance through its shareholding, but also fully supports the adoption of USDC through its business operations, jointly aiming to expand the market influence and market capitalization of this compliant stablecoin.

Other subscription services: These include Coinbase Earn (earn rewards for watching learning content), Coinbase Card debit card fee rebates, and Coinbase Cloud's blockchain infrastructure services. While these services are currently small in scale, they offer synergies and align with the company's focus on building a comprehensive crypto platform. For example, Coinbase Cloud provides nodes and exchange interfaces for institutions and developers, and will power the launch of multiple blockchain projects in 2024. Long-term, it has the potential to become the "AWS of crypto."

The subscription and services segment's revenue share has increased from less than 5% in 2019 to 40-50% currently, becoming a stable source of revenue for the company during periods of trading slump. With interest and fees as the primary components, costs are very low, resulting in a gross profit margin approaching 90%. Coinbase will continue to drive growth in its subscription business, for example by launching more subscription packages for frequent users, expanding the range of assets supported by staking, and deepening the global adoption of USDC (including innovations such as using USDC as margin for US futures trading). This segment is expected to become a key stabilizer for the company against market volatility.

Decentralized business: Base Layer-2 network

Positioning and Vision: Base, an Ethereum L2 based on the Optimism OP Stack, was launched by Coinbase in August 2023. Its goal is to smoothly transition over 100 million Coinbase users to the on-chain ecosystem. The official roadmap from January 2025 emphasizes "sequencer decentralization by the end of 2025" and sharing network revenue through community governance.

-Key operating indicators: As of August 2025, the value of deposited assets on the Base chain is approximately US$15.46 billion, with 30.7 million monthly active addresses, 9.24 million 24-hour transactions, and US$204,000 in 24-hour on-chain fee income, ranking first in all L2 revenue.

Revenue Contribution: Coinbase categorizes Base sequencer fees as "other transaction revenue." In 2024, Base contributed approximately $84.8 million in revenue to Coinbase (according to TokenTerminal data, details not disclosed in official financial reports). So far in 2025, Base has contributed $49.7 million. Besides transaction fees and interest income, Base has become one of Coinbase's most promising on-chain revenue engines.

Other potential business lines: Coinbase is also exploring new opportunities, such as the NFT digital collectibles marketplace (Coinbase NFT launched in 2022, but user activity was low, leading the company to reduce investment in this area in 2023), and payment and merchant tools (Coinbase Commerce, which allows merchants to accept crypto payments, is primarily a strategic development). While these businesses currently have limited financial contributions, their strategic significance lies in completing the ecosystem and strengthening user reliance on the Coinbase platform.

The table below shows Coinbase's revenue composition and proportion in 2024:

Summary of business and product lines

Coinbase's business has expanded from a single exchange to a multi-faceted platform driven by trading, custody, staking, and stablecoins. This diversification not only reduces over-reliance on transaction fees (non-transactional revenue will account for 40% in 2024) but also strengthens customer stickiness (users keep their assets on the platform to earn staking interest and use stablecoins, reducing their willingness to migrate elsewhere). Synergies are created across these businesses: trading generates asset retention, which in turn generates staking and interest income, which in turn encourages users to trade more. This "flywheel effect" is one of the moats Coinbase strives to build. However, the company also needs to balance regulatory considerations and resource investment to ensure the compliance and sustainability of each business. For example, staking and lending must comply with securities laws, and stablecoin reserves must be transparent. Overall, Coinbase's product portfolio is comprehensive, and it is the first in the industry to establish the prototype of a comprehensive crypto-financial services platform, providing it with a relatively stable revenue structure and growth path amidst fierce competition.

5. Management and Governance

In terms of company management, we focus on several dimensions: 1. The background of senior executives and the stability of core members; 2. The level of past strategic decision-making.

5.1 Background of the Core Management Team

Brian Armstrong – Co-founder, Chief Executive Officer (CEO), and Chairman of the Board, holding a majority voting stake. Born in 1983, he previously worked as a software engineer at Airbnb. He founded Coinbase in 2012 and is one of the earliest entrepreneurs in the crypto space. Armstrong focuses on long-term mission and product simplicity, and is known internally for his principled approach (e.g., the company's 2020 statement on apolitical culture).

Fred Ehrsam – Co-founder and Director. A former Goldman Sachs foreign exchange trader, he co-founded Coinbase with Armstrong in 2012 and served as its first president. He left day-to-day management in 2017 to found Paradigm, a prominent crypto investment fund, but has remained on the board, providing input on industry trends and company strategy.

Alesia Haas – Chief Financial Officer (CFO). She joined Coinbase in 2018. Previously, she served as CFO of the hedge fund Och-Ziff (now Sculptor Capital) and a senior executive at OneWest Bank. She has extensive experience in traditional finance and capital markets. She led the company through its IPO financial preparations, emphasizing financial discipline and decisively implementing two rounds of layoffs in 2022 to control costs. Haas also leads Coinbase's subsidiary, Coinbase Credit, exploring crypto lending.

Emilie Choi – President and Chief Operating Officer (COO). She joined Coinbase in 2018 as Vice President of Business Development and was promoted to President and COO in 2020. Prior to joining Coinbase, she led mergers and acquisitions and investments at LinkedIn, including the acquisition of SlideShare, and was known for her strategic expansion. At Coinbase, Choi drove a series of acquisitions (Earn.com, Xapo Custody, Bison Trails, etc.) and international expansion, and is considered one of the most influential executives outside of Armstrong. She also oversees day-to-day operations management, talent, and strategic project execution.

Paul Grewal – Chief Legal Officer (CLO). Joined in 2020, Grewal is a former deputy general counsel at Facebook and a former federal judge. Grewal is responsible for handling legal and regulatory matters for Coinbase, including its 2023 legal battle with the SEC. His team plays a key role in compliance and policy lobbying.

Other key executives: The Chief Product Officer position was previously held by Surojit Chatterjee (a former Google executive), who led product development from 2020 to 2022 and departed in early 2023. The product team has since been divided among various department heads. Greg Tusar and others have held the Chief Technology Officer (CTO) position, which is now shared by senior engineering executives. Chief People Officer (CPO) LJ Brock oversees recruiting and culture development, playing a key role in the company's cultural transformation. Also worth mentioning are Chief Marketing Officer Kate Rouch (former Facebook Marketing Director), who brings cross-disciplinary experience to Coinbase, hailing from both Silicon Valley tech and Wall Street.

The overall management team profile: a young and entrepreneurial founder combined with professional managers from traditional financial and tech giants. This diverse team helps Coinbase achieve both technological innovation and regulatory compliance. Executives all hold significant equity or stock options, with Armstrong receiving a special CEO performance-based equity incentive plan, encouraging him to achieve the company's market capitalization target within 10 years.

5.2 Personnel and Strategic Stability

Coinbase has experienced ups and downs in personnel and strategy, but has generally remained consistent:

Executive Turnover: Most of the core founding team remains with the company (Armstrong and Ehrsam serve on the board). However, some executives have departed in recent years: former Chief Product Officer Chatterjee, for example, left in early 2023; the Chief Technology Officer and Chief Compliance Officer positions have also undergone several changes. Some personnel turnover is related to market conditions: the 2022 bear market and declining performance led to management streamlining. After Armstrong announced his "no politics" policy in 2020, approximately 60 employees (including the former Chief Human Resources Officer) accepted layoffs. Despite this, the company's overall senior management retention rate is high—the CEO, CFO, and COO have all been in their positions for many years and led the company to IPO, and the head of legal affairs is also stable. This indicates that the management team is relatively mature and key positions are not frequently shaken up.

Strategic Coherence: Coinbase's core mission (building a trusted crypto-financial system) has remained unchanged since its founding. While strategic priorities may adjust with industry evolution, the overall trajectory is relatively clear: early on, it focused on Bitcoin brokerage and expanding its user base; subsequently, it expanded into various currencies and international markets; and since 2020, it has clearly pursued a two-pronged approach—serving both retail and institutional investors, while also increasing subscription revenue to diversify its business model. Even during market downturns (such as 2018 and 2022), management persisted in investing in new products (such as the USDC stablecoin in 2018 and the NFT platform and derivatives portfolio in 2022), demonstrating confidence in the long-term trend of crypto. Of course, there have been corrections: for example, after NFT products flopped, the company reduced resources in 2023; and, due to reckless expansion, it was forced to lay off approximately 2,100 employees (approximately 35% of its workforce) twice in fiscal 2022. Management, having learned from these mistakes, has improved operational efficiency. Overall, Coinbase has strong strategic execution capabilities, has not experienced any disruptive shifts or major failures, and its decisions are generally consistent with industry developments.

Strategic Consistency: Quantifying Coinbase's strategic consistency, such as tracking its early investments in key technologies and markets, reveals that Coinbase has consistently positioned itself for most major industry trends: supporting Ethereum as early as 2015 (capitalizing on the smart contract trend), launching a stablecoin in 2018 (betting on the future of compliant stablecoins), applying for a futures license in 2021 (foresight into the derivatives market), and subsequently entering the market with proprietary L2 trading. These decisions have been highly consistent with subsequent industry developments, demonstrating strong management judgment. Of course, the company has also made mistakes, such as missing out on the booming DeFi decentralized trading market of 2019-2020 (failed to capitalize on the decentralized finance market, including DEXs, until its subsequent entry into the market through the development of Base). However, given Coinbase's emphasis on compliance, this may have been a deliberate strategic trade-off.

5.3 Strategic Capability Review

Key examples of management successes and failures in key decisions include:

Strategic Success Stories: Early Compliance Planning – Coinbase prioritized compliance from the outset, proactively applying for US FinCEN registration and state licenses in 2013. This decision proved to be a wise one: by the time competitors were forced to exit the US market due to compliance issues, Coinbase had already established a regulatory moat and built deep trust with US users (Coinbase has never experienced a major theft of customer funds), expanding its market share in the US. Another success was its IPO timing – management capitalized on the 2021 bull market peak with a direct listing, providing the company with ample capital and brand recognition, while also rewarding early investors and employees and stabilizing team morale. Another example is its acquisition strategy – the 2019 acquisition of Xapo's institutional custody business made Coinbase one of the world's largest crypto custodians, seizing an early advantage in the institutional market. These achievements demonstrate management's strategic vision and strong execution.

· Strategic Mistake Example: Expansion Too Rapidly Leading to Layoffs – During the bull market of 2021, Coinbase’s employee size surged from approximately 1,700 to nearly 6,000 at the beginning of 2022 (currently around 3,700+), and many departments were overstaffed. Armstrong publicly admitted that being “overly optimistic” about staff expansion led to decreased efficiency. As the market cooled in 2022, the company had to carry out two large-scale layoffs, which took a toll on morale. Another setback was the poor performance of the new product NFT Marketplace – Coinbase invested resources to launch the NFT trading platform in April 2022, hoping to replicate OpenSea’s success. However, due to its late entry and lack of differentiation, coupled with the overall cooling of the NFT market, the platform’s monthly trading volume remained sluggish for a long time, and the company eventually almost gave up operations. Management’s attempts in some areas fell short of expectations, and there were deviations in market analysis, but the overall losses were limited and they were able to stop losses in time.

Overall, Coinbase has good management, a relatively stable core team, and strategic decisions that align with industry trends. It hasn't missed any major industry opportunities. Although there have been issues with out-of-control costs and some product exploration failures, the merits outweigh the flaws.

6. Operational and financial performance

In this section, we will focus on Coinbase's revenue, profit, costs, and assets and liabilities, and evaluate the company's profitability and stability.

6.1 Overview of Profit and Loss Statement (5 Years)

Coinbase's revenue and profit performance are highly dependent on the crypto market, showing a "roller coaster"-like fluctuation:

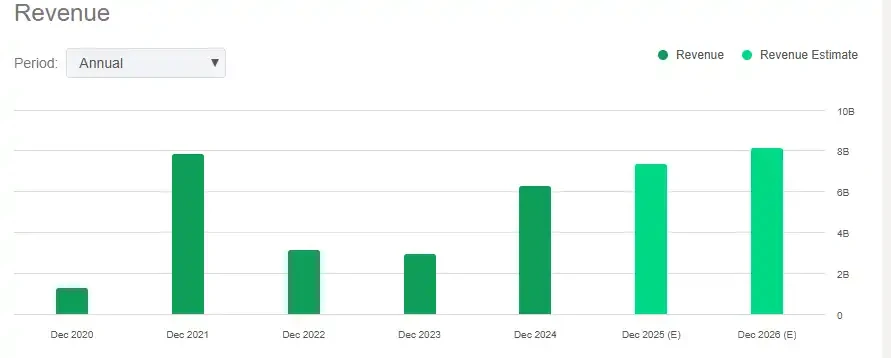

Revenue: Total revenue was only $534 million in 2019. In 2020, driven by Bitcoin's mini-bull run, it increased to $1.28 billion (+140%). With the full-blown bull market in 2021, revenue soared to $7.84 billion (+513% year-on-year). Revenue plummeted to $3.15 billion (-60%) during the 2022 bear market, and fell further to $2.92 billion in 2023. In 2024, as the market rebounded, revenue rebounded strongly to $6.564 billion, doubling from 2023. In the first quarter of 2025, Coinbase continued its strong momentum from late 2024, achieving total revenue of approximately $2.03 billion, a 24% year-on-year increase. Revenue declined again in the second quarter of 2025, reaching approximately $1.5 billion, a sharp 26% drop from the $2.03 billion in Q1 2025. This is primarily due to a 16% drop in crypto market volatility in the second quarter, and a decline in trading volume due to weakened investor appetite. Coinbase's revenue remains highly dependent on market fluctuations, subject to significant short-term volatility. However, the company's total revenue in the first half of the year still grew by approximately 14% compared to the same period last year. Overall, the company's revenue has experienced a roller-coaster ride over the past five years, demonstrating significant cyclical resilience: From 2019 to 2024, revenue is projected to grow at a compound annual growth rate of approximately 40%, but annual fluctuations can reach over ±50%. Bull market surges and bear market halvings are expected to continue into the first half of 2025.

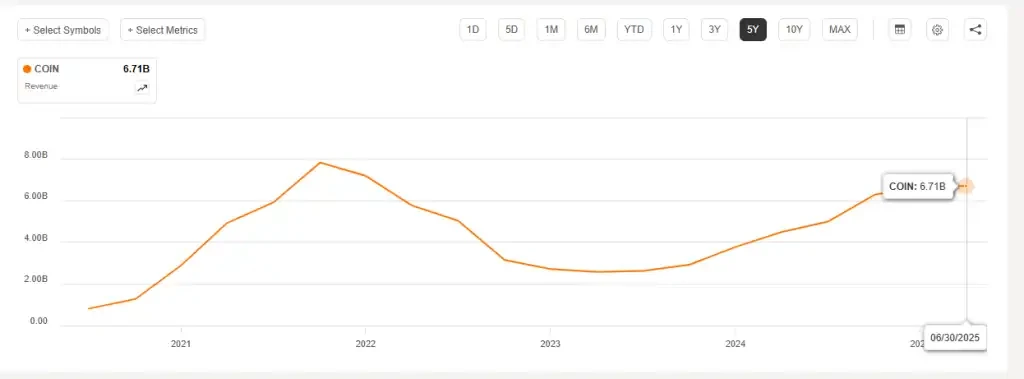

Coinbase revenue (TTM) trends, September 2020-June 2025, Source: seekingalpha

Coinbase revenue (TTM) trends, September 2020-June 2025, Source: seekingalpha

Coinbase annual revenue (including forecasts), 2020-2026. Source: seekingalpha

Revenue Structure: Transaction fees have always been the primary source of revenue, but their proportion has gradually declined. In 2021, transaction revenue reached 6.9 billion, accounting for approximately 87%. This figure dropped to 2.4 billion in 2022, representing 77%. In 2023, transaction revenue reached only 1.5 billion, representing 52%. In 2024, transaction revenue rebounded to approximately 4 billion, representing approximately 61%. Correspondingly, subscription and service revenue (staking, interest, custody, etc.) increased from less than 5% in 2019 to 48% in 2023, before declining slightly to approximately 35% in 2024 (totaling 2.3 billion). In the first quarter of 2025, transaction fee revenue reached approximately 1.26 billion (up 17.3% year-on-year), accounting for over 60% of quarterly revenue. Subscription and service revenue reached 698 million (up 37% year-on-year), contributing over 30% of revenue, primarily driven by rising interest income from the USDC stablecoin and user growth for the subscription product, Coinbase One. In the second quarter of 2025, trading revenue and subscription revenue saw a shift in direction: Trading fee revenue for the quarter was approximately 764.3 million yuan, accounting for approximately 54% of total revenue; subscription and services revenue reached 655.8 million yuan, a year-on-year increase of 9.5%, rising to approximately 46% of the total, almost matching the size of trading revenue. Subscription growth was primarily driven by USDC interest and custody services. In the second quarter, average USDC reserve balances increased by 13% quarter-over-quarter to $13.8 billion, contributing significant stablecoin interest income. Meanwhile, staking and institutional custody fees saw steady growth, and Coinbase's subscription revenue continued to reach record highs. In the first half of 2025, subscription/services revenue accounted for approximately 44% of the company's total revenue, a significant increase from 35% for the full year of 2024, further solidifying Coinbase's diversification. This shift in revenue structure reduces the company's reliance on trading fees, helping to mitigate the impact of market volatility on revenue.

Profit: Coinbase, benefiting from its high-gross-margin business model, is highly profitable when trading volume is high. In 2019, it reported a loss of 30 million yuan. In 2020, it achieved a net profit of 322 million yuan (with a 25% net profit margin). In 2021, net profit climbed to 3.624 billion yuan (with a net profit margin of approximately 46%), exceeding the combined profit of all previous years. In 2022, it suffered a massive loss of 2.625 billion yuan (with a net profit margin of -83%), its worst year on record. In 2023, it reported a slight profit of 95 million yuan (with a net profit margin of 3%), returning to profitability. In 2024, net profit reached 2.579 billion yuan (with a net profit margin of approximately 39%), second only to its peak in 2021. This shows that Coinbase's profits and losses fluctuate significantly in tandem with its revenue. Net profit in the first quarter of 2025 was $66 million, seemingly a significant decline compared to the previous quarter. However, this was primarily due to the decline in the fair value of crypto assets, equity incentives, and litigation expenses in the first quarter. Excluding after-tax fair value gains and losses on crypto asset investments and other one-time items, adjusted net profit for the quarter was $527 million, more reflective of core operating results. In contrast, Coinbase's profits saw a dramatic jump in the second quarter of 2025: GAAP net profit reached $1.429 billion, a year-on-year surge (compared to just $36 million in Q2 2024), with a net profit margin of approximately 95%. However, this exceptionally high profit was primarily due to non-recurring gains: the company recognized a $1.5 billion strategic investment gain from the revaluation of its stake in stablecoin issuer Circle, as well as a $362 million gain on its crypto asset portfolio. After deducting the aforementioned one-time gains, Q2's adjusted net profit was only approximately ¥33 million (adjusted net profit requires adding back nearly $438 million in taxes and fees resulting from two non-recurring gains), significantly lower than the ¥527 million in Q1 2025, reflecting a significant weakening of the company's core business profitability due to declining trading volume. Overall, Coinbase's profits continue to fluctuate significantly with revenue: net profit can reach over 30% to 40% of revenue during booming markets, while losses can occur during downturns without strict cost control. However, after significant losses in 2022, the company was able to quickly return to break-even in 2023 through layoffs and cost reductions, demonstrating a degree of cost flexibility and operational resilience.

Expense Structure: From a cost perspective, Coinbase's costs are primarily comprised of operating expenses (R&D, sales, and general administration), with direct transaction costs being relatively small . Sales and marketing expenses typically account for less than 10%, and have been reduced to below 5% since 2022, reflecting a relatively restrained marketing investment. R&D and general administration expenses together account for approximately 20-30%, including significant equity incentive expenses: for example, a one-time share reform charge upon IPO in 2021, and continued annual equity expenditures (employee stock options) of approximately $300-500 million from 2022 to 2023. The expense ratio (operating expenses/revenue) significantly dilutes in bull markets (only approximately 22% in 2021) but soars in bear markets (reaching over 100% in 2022). In 2023, after layoffs and cost reductions, the expense ratio dropped back to 70%. Starting in 2024, the company will continue to strictly control expenses, aligning human resources and project investments with business needs. Notably, a major data breach occurred in Q2 2025, resulting in approximately $307 million in litigation and compensation expenses, causing total operating expenses for the quarter to surge 15% quarter-over-quarter to $1.52 billion. (Excluding this one-time item, core operating expenses actually maintained a downward trend.) Meanwhile, stock-based compensation (SBC) expenses remain a significant expense component and warrant continued monitoring. Annual SBC expenses are projected to be approximately $300 million to $500 million in 2022-2023. In Q2 2025 alone, SBC expenses reached $196 million, a slight increase of 3% from Q1. If this trend continues, annual SBC expenses could exceed $700 million. Overall, Coinbase's fee structure is relatively flexible, allowing personnel and project expenditures to adjust with market conditions. However, the dilutive effect of stock-based compensation should be carefully considered.

6.2 Profitability and Efficiency (5 years)

Coinbase's earnings quality and operating efficiency are assessed using a combination of ratios:

Gross profit margin: It has consistently remained high at 80-90%, reflecting the high profitability of its transaction fee-based business. For example, the gross profit margin was approximately 88% in 2021, 81% in 2022, and then rose to 84% in 2023 despite declining revenue (due to a high interest rate share in the revenue structure, with no corresponding costs). It reached 85% in 2024. In Q2 2025, despite a decline in trading volume, the gross profit margin remained approximately 83%. This demonstrates that regardless of market conditions, Coinbase converts a significant portion of every dollar of revenue into gross profit, leading its peers (compared to the 50-60% gross profit margins of traditional securities brokers).

Net profit margin: volatile. In 2021, the net profit margin was 46%, comparable to the most profitable tech companies; in 2022, it was -83%, a significant loss; in 2023, it recovered to a positive 3%; and in 2024, it reached 39%. In Q2 2025, the adjusted net profit margin, excluding non-recurring items, was only approximately 2%. On average, Coinbase's net profit margin is around 30-40% in normal/booming markets, providing strong profit leverage; however, it may incur losses in a downturn, requiring prompt cost reductions to recover losses.

ROE/ROA: Due to profit fluctuations, return on equity (ROE) and return on assets (ROA) fluctuate significantly. In 2021, ROE exceeded 60% (due to high profits and limited net asset expansion from the IPO); in 2022, it fell to -40%; in 2023, ROE was less than 2%; and in 2024, ROE rose to approximately 25%. Regarding return on assets, ROA was approximately 20% in 2021 and approximately 15% in 2024, indicating a slight decline in efficiency following balance sheet expansion. Overall, Coinbase's ROE in profitable years was significantly higher than that of traditional financial companies, but its stability was less pronounced.

Per-person Efficiency: Due to significant fluctuations in employee headcount, we use revenue/employee to measure efficiency. During the 2021 bull market, due to a business boom, per-person annual revenue reached approximately $1.9 million per employee. This figure plummeted to below $500,000 per employee in 2022, and rebounded to the $800,000-$1 million per employee range in 2023 following layoffs. This still exceeds the per-person revenue levels of most traditional financial institutions, placing it in the upper-middle range and demonstrating the economies of scale of its digital platform model. We anticipate that with a reasonable headcount (currently approximately 3,700 employees), per-person revenue will stabilize at around $1 million in the future, and could exceed this level in the event of another super-bull market.

Comparison of per capita revenue of trading financial institutions (2024)

Comparison of per capita revenue of trading financial institutions (2024)

6.3 Cash Flow and Capital Expenditure (5 Years)

Coinbase's operating cash flow is also cyclical, but generally remains positive:

Operating Cash Flow: 2021 saw very strong OCF, with a full-year net operating cash inflow of approximately 10 billion yuan (due to the accumulation of deposits from a surge in client transactions), resulting in significantly positive free cash flow. In 2022, operating cash outflows of approximately 2 billion yuan were recorded, reflecting losses and changes in working capital. In 2023, operating cash flow returned to positive levels, reaching approximately 520 million yuan, driven by cost reductions and interest income. OCF surged in 2024, with reported full-year net operating cash inflows of 2.5 billion yuan, more than doubling year-over-year. This was driven in part by a return to profitability and growth in client funds.

Cash Flow from Investing Activities: Coinbase is not an asset-heavy company, with relatively low capital expenditures (CapEx). Its primary investments are in acquisitions and platform R&D. From 2019 to 2021, annual capital expenditures averaged only tens of millions of dollars (for servers, office space, and other expenses). This increased to approximately $150 million in 2022 (as the company purchased office buildings and expanded its data center capacity). In 2023, CapEx was further reduced, by approximately $50 million. Regarding acquisitions, Coinbase spent significantly around 2021 (e.g., approximately $100 million on the acquisitions of Bison Trails and Skew). Acquisitions slowed from 2022 to 2023. In 2024, the company made small acquisitions of One River Asset Management, among others. Overall, investing cash flow was a net outflow, but the outflow was small and did not impact cash flow from the core business. In addition, the company announced a major acquisition plan for the derivatives exchange Deribit from the end of 2024 to the beginning of 2025: the total transaction price is approximately 2.9 billion, including approximately 700 million in cash payment (the rest is the issuance of approximately 11 million shares).

Free Cash Flow: Considering operating cash flow minus capital expenditures, Coinbase's free cash flow in profitable years is very impressive: $9.7 billion in 2021, negative in 2022, returning to positive around $400 million in 2023, and around $2.56 billion in 2024, demonstrating ample cash flow generation. Coinbase will invest excess cash in safe assets (such as short-term government bonds) or hold some crypto assets.

Financing Cash Flow: In 2021, the company raised approximately 3.25 billion yuan through convertible and corporate bonds, while also issuing no new shares in its IPO (no proceeds were raised through its direct listing). There were no major financing activities in 2022. In 2023, Coinbase proactively repurchased or repaid a portion of its bonds, repurchasing 413 million yuan in debt at a discount, reducing interest expenses. The company has no dividend plan, with only small-scale share repurchases in late 2022 and 2023 to hedge equity incentives. Its overall financial policy is conservative and prudent.

Cash reserves: In the first quarter of 2025, Coinbase's cash and cash equivalents reached US$9.9 billion. The cash and cash equivalents announced in the second quarter were US$7.539 billion, a significant decrease, but still relatively abundant.

6.4 Balance Sheet Health (5 Years)

Coinbase has a relatively strong balance sheet, characterized by high liquidity and low leverage:

Debt Level: The company issued two bonds during the 2021 bull market: a 1.25 billion yuan convertible bond due in 2026 and a 2 billion yuan senior note due in 2028 and 2031. This resulted in peak long-term debt of approximately 3.25 billion yuan. The company did not raise any further debt in 2022-2023, and the repayment/repurchase of bonds by the end of 2023 reduced debt to approximately 2.8 billion yuan. With an adjusted EBITDA of approximately 3.35 billion yuan in 2024, net debt/EBITDA is approximately zero (in a net cash position), or gross debt/EBITDA is less than 0.9x, indicating extremely low leverage. Overall debt-to-equity has remained low since its IPO. Notably, Coinbase has not borrowed from banks as of 2024. Its debt is all public market bonds, eliminating the risk of loan withdrawal and with long-term maturities, minimizing short-term debt repayment pressure.

Liquidity: Coinbase boasts a substantial cash and cash equivalent position and an exceptionally high quick ratio. Excluding customer deposit liabilities (which have corresponding customer assets), the company's core operating liquid assets far exceed its current liabilities. In its 2025 semi-annual report, its quick ratio (excluding customer-related liabilities) exceeded 3.19x, meaning its cash and cash equivalents covered all short-term liabilities by more than three times. Of particular note is its highly liquid USDC reserves (convertible at a 1:1 ratio to the US dollar daily). Despite a brief USDC depeg in 2023, the company promptly fulfilled customer redemptions, avoiding any liquidity squeeze.

Asset Quality: Assets primarily consist of cash, cash equivalents, and short-term investments (such as high-rated bonds), accounting for over 60%. The company's crypto holdings are relatively modest, with a fair value of 1.839 billion in Q2 2025. The fair value of crypto assets held was 1.261 billion (68.6%), comprising 11,776 BTC, 340 million (18.5%), and 238 million (12.9%) in other crypto assets. This is manageable relative to the company's net assets, and price fluctuations will not significantly impact solvency.

Overall, Coinbase boasts a high level of financial security, including low leverage, ample liquidity, and the ability to withstand multiple stress tests. This strong balance sheet also enables Coinbase to make countercyclical investments during market downturns. For example, during the industry downturn of 2022-2023, the company maintained its R&D investment and international expansion, which will benefit its long-term competitive position.

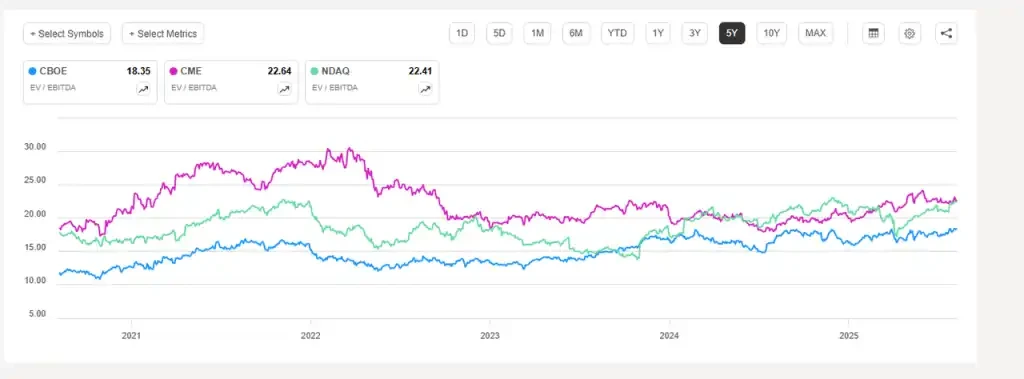

6.5 Industry Comparison

Compare Coinbase's financial metrics for Q2 of 2024 and 2025 with those of other publicly listed or comparable exchanges.

We selected Robinhood, Kraken, and Binance as our comparison targets:

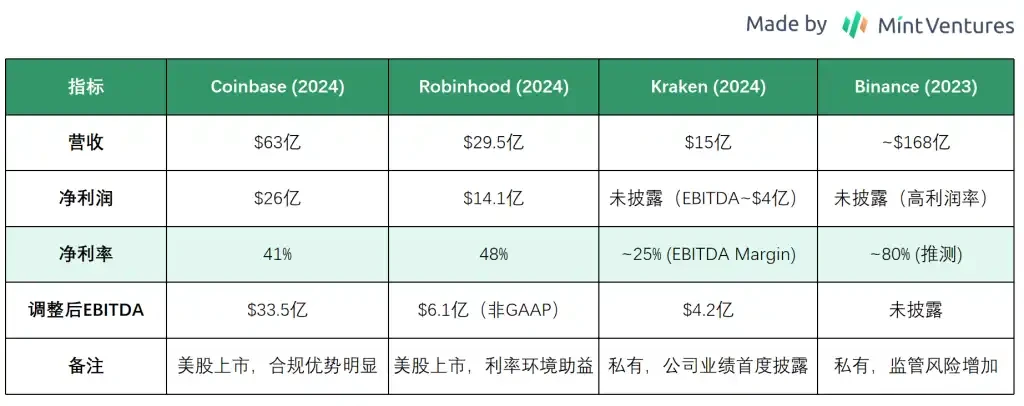

Robinhood (US stock brokerage and crypto trading platform): Net revenue in 2024 is expected to be approximately $2.951 billion, a year-on-year increase of 58%, achieving its first full-year profit in history with a net profit of $1.411 billion (compared to a loss of $541 million in 2023). Thanks to interest income driven by high interest rates and a rebound in trading, Robinhood's gross profit margin in 2024 will reach 94%, with a net profit margin of approximately 48%. Revenue in the first quarter of 2025 was $927 million (a 50% year-on-year increase), with a net profit of $336 million. With improved performance, Robinhood's stock price has risen significantly since the end of 2024, with a current market capitalization exceeding $95 billion.

Kraken (a long-established US crypto exchange, privately held): Surging trading volume in 2024 drove revenue to approximately $1.5 billion, a 128% year-over-year increase, nearing a record high. Full-year adjusted EBITDA is expected to be approximately $400 million, with an EBITDA margin between 25% and 30%. By the end of 2024, Kraken's platform assets will reach $42.8 billion, with 2.5 million monthly active paying users and an average annual revenue per user exceeding $700. In Q1 2025, Kraken achieved revenue of $472 million (up 19% year-over-year and down 7% quarter-over-quarter), while Q2 revenue reached approximately $411.6 million, a further -13% quarter-over-quarter decrease. As a privately held company, Kraken's latest valuation has not been disclosed, but media reports indicate that it sought funding at a valuation exceeding $10 billion in 2021. Kraken's private equity price on the Hiive private equity trading platform is $42.8, corresponding to a valuation of approximately $9.1 billion. This represents a rapid increase in value over the past three months, nearly doubling. The doubling of revenue in 2024 indicates a significant increase in actual business scale, and its valuation multiple relative to revenue is likely lower than that of fellow publicly traded companies Coinbase and Robinhood.

Binance (the world's largest privately listed crypto exchange): As an industry leader, Binance's trading volume and user base far surpass its peers. While its financial data is not regularly disclosed, previous industry analysts estimate 2023 revenue to be approximately $16.8 billion, a 40% increase over the previous year and approximately 2.7 times Coinbase's revenue during the same period. Binance reportedly achieved over $12 billion in revenue and nearly $10 billion in profit in 2022, reflecting impressive profitability and business scale (with a profit margin of approximately 80%). Due to its private nature, Binance does not have a publicly available market capitalization or valuation multiple; however, based on its revenue and profit volume, even with a lower valuation multiple, its implied market capitalization could still reach hundreds of billions of dollars. Regarding the regulatory environment, Binance has faced compliance pressure and litigation challenges in the United States, Europe, and other regions, adding uncertainty to its future growth and potential IPO prospects. Overall, Binance leads the industry in absolute scale with its overwhelming market share, but compliant listed platforms such as Coinbase have higher market confidence reflected in their valuation levels (such as price-to-sales ratio, EV/EBITDA multiples, etc.), which is related to regulatory transparency and differences in business models.

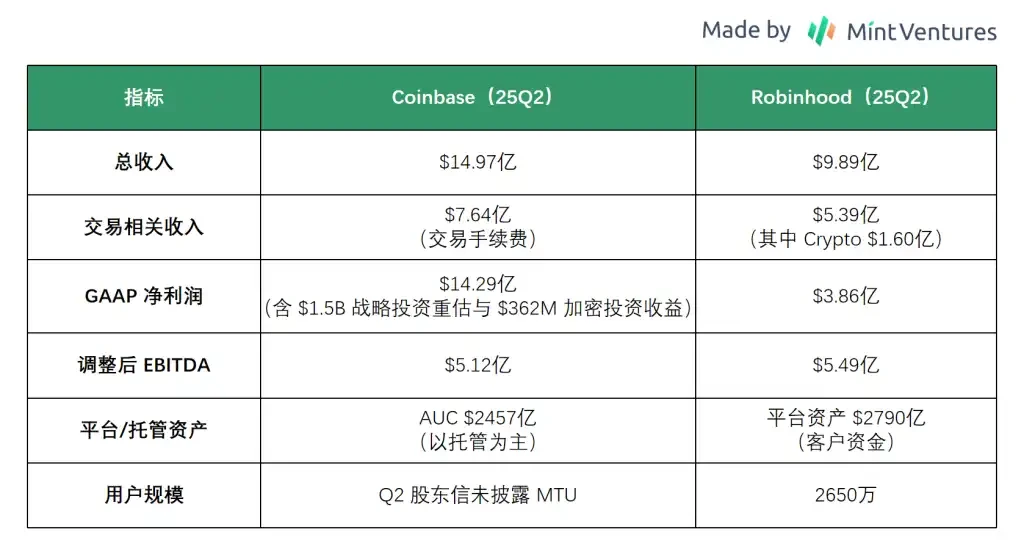

Let’s compare Coinbase and Robinhood’s Q2 data over the past 25 years:

Overall, the two companies' revenue and other indicators are relatively similar. Coinbase's market capitalization is currently $79.8 billion, while Robinhood's is $101.8 billion. However, their revenue structures differ significantly. Coinbase's revenue comes from trading + subscriptions/custody/stablecoins/derivatives; Robinhood's revenue comes from brokerage fees + interest income (the interest spread earned on user funds deposited in banks + margin trading income) + subscriptions/options/crypto trading. In recent years, Robinhood has rapidly expanded its platform assets and user base, and has also acquired Bitstamp to promote internationalization, making it a direct competitor to Coinabase both in the United States and globally.

In summary, Coinbase's financial performance reflects the high-growth, high-volatility characteristics of the industry. However, thanks to effective cost control and a solid balance sheet, the company has maintained its resilience during downturns and achieved exceptional profitability during peak periods. This resilience presents both an investment advantage and a risk: if the crypto market continues to improve, Coinbase could potentially achieve the same profit peaks as in 2021. Conversely, if the market weakens, the company will need to tighten its spending to avoid a repeat of the losses seen in 2022. Currently, even in the event of a renewed bull market, the company has maintained a lean staff and maintained good cost control. Future efforts will require careful attention to whether the expansion of its subscription business can mitigate cyclical impacts and further strengthen the company's financial performance.

7. Competitive Advantage and Moat

Coinbase's ability to gain a foothold and become a leader in the fierce competition in the crypto industry is closely related to the multiple moats it has built:

Brand trust and compliance advantages

As one of the earliest exchanges to enter the regulatory compliance arena, Coinbase has built strong brand credibility. It is one of the few exchanges in the United States to hold state licenses (since 2013, it has obtained money transmitter licenses in 46 states/territories, legally operating in all 50 states), FinCEN registration, and a New York trust charter. Since its inception, Coinbase has experienced no significant user asset losses. This has established Coinbase as a secure and trustworthy exchange among users, a strength further emphasized following the collapse of peers like Mt. Gox and FTX, as well as thefts from numerous crypto exchanges. For large institutions and mainstream users, Coinbase is often the first, or even only, choice. For example, in the United States, regulatory restrictions restrict many traditional funds to using licensed exchanges, giving Coinbase a natural market share. Coinbase also proactively cooperates with regulatory bodies (such as Know Your Customer and Anti-Money Laundering), earning a positive reputation among policymakers and lobbying for favorable regulations. The barriers created by brand and compliance are difficult for newcomers to replicate quickly and cost-effectively. ( License application cycles typically take 12–18 months, accompanied by ongoing annual inspections for capital adequacy, anti-money laundering, and cybersecurity. New entrants face hundreds of millions of dollars in compliance costs to obtain licenses in all states .) Even if a new platform is technologically competitive, without regulatory backing and a years-long, accident-free track record, it will be difficult to challenge Coinbase's position among conservative funds and novice users in the short term. This trust advantage also carries a premium: Coinbase can charge relatively higher fees because users are willing to pay for security and reliability.

Network Effects and Liquidity

Exchanges have significant network effects: more users and trading volume lead to deeper liquidity and a better trading experience, which in turn attracts even more users. After years of operation, Coinbase has amassed a massive global user base and massive trading volume. According to statistics, 67% of US cryptocurrency holders have used Coinbase. This high reach makes Coinbase the gateway platform to the crypto space. New coins and projects seeking to reach a broad user base often target Coinbase. A large user base also means a deep order book and tight bid-ask spreads, which are crucial for the trading experience. Especially during periods of volatile price fluctuations, platforms with deep liquidity can better accommodate large trades without slippage, further solidifying professional traders' reliance on Coinbase. Network effects are also reinforced through word-of-mouth: more users lead to a stronger referral effect, with new traders more likely to choose platforms their friends use, creating a positive cycle. It's extremely difficult for competitors to disrupt this virtuous cycle unless they offer radically differentiated services in a specific niche (such as zero fees or support for specialized assets). Currently, Coinbase's network effects in the European and American markets appear relatively solid.

Economies of scale & diversified business stickiness

Coinbase's scale advantage lies not only in its liquidity network effects, but also in its cost advantages and business mix. As a publicly listed company, Coinbase can raise sufficient funds to invest in system security, product development, and compliance teams, which translates into lower per-transaction costs. Smaller platforms often cannot afford expensive compliance and security investments. Coinbase's operational efficiency improves as its customer base expands, creating a moat of economies of scale. Furthermore, the company's diverse business segments (trading, custody, staking, stablecoins, etc.) mutually reinforce user stickiness. Users on Coinbase not only trade, but also deposit coins to earn interest, participate in staking to earn returns, and use USDC for payments. These multiple needs are met on the same platform, increasing migration costs.

Technical and security barriers

While the technical barriers to entry for trading are relatively low compared to high-tech industries, Coinbase has built significant technical advantages through years of development in areas such as high-concurrency matching, wallet security, and multi-chain support. Its trading engine has been tested during peak bull markets (for example, daily trading volumes reached tens of billions of dollars in 2021), demonstrating its robustness in handling extreme trading surges. Regarding wallet security, Coinbase has experienced no major hacks to date, a record that many competitors of its caliber struggle to claim (even Binance has experienced thefts in the hundreds of millions of dollars). Furthermore, Coinbase has independently developed numerous internal systems, such as tools for analyzing and monitoring suspicious transactions, preventing market manipulation, and professional APIs, providing reliable technical support to institutions and partners. These achievements are not easily replicated. Especially in terms of security and risk management, any new platform can face significant reputational damage if it encounters even a single serious vulnerability. Coinbase's years of investment in security have established a strong barrier in the minds of users.

Moat Sustainability Discussion

Can these moats be sustained over the long term? Let's evaluate each one individually:

In terms of brand and compliance, as more mainstream institutions become involved and regulatory rules are introduced, Coinbase's existing licenses will become more valuable. Its first-mover advantage is likely to expand further, as it has established a strong reputation and has experience and scale advantages over later entrants in license application and compliance costs. However, regulatory uncertainty may still pose challenges (for example, in the worst-case scenario, a change in government and Congress could lead to a shift in US regulatory style, limiting Coinbase's core market).

The network effect is likely to be robust. Unless Coinbase experiences a crisis of trust or prolonged technical outages, user churn is unlikely. However, it's important to note that the rise of decentralized finance (DeFi) may weaken the network effect of centralized platforms among some professional users (some turning to DEXs like Uniswap and on-chain exchanges like Hyperliquid for independent trading). However, the current DeFi experience and liquidity are not sufficient to significantly impact Coinbase. Furthermore, Coinbase's aggressive development of Base and its smart crypto wallets is a hedge against this trend.

Economies of scale and diversified stickiness will become increasingly significant as the company expands its business. As Coinbase grows, its cost structure becomes more favorable, and user ARPU increases—a positive cycle. However, there are also risks: too many business lines can distract management attention, and the regulatory requirements for different businesses are complex, requiring the company to ensure that "the ship is big enough to withstand leaks."