Trend Research: The storm is coming, and the market will promote ETH to achieve value discovery

Recently, with the good performance of cryptocurrency stocks such as CRCL and HOOD, many investment friends have raised some valuable questions, "If the stablecoin bill is really passed, where will the market growth appear?", "Why do SBET and BMNR soar when they take advantage of the popularity of Ethereum?", "Does the opportunity of RWA have anything to do with Ethereum?", "Why are you firmly optimistic about ETH regardless of short-term price fluctuations?", We have given fragmented answers to different questions. This article will organize them systematically and summarize them from the underlying logic and a longer-term perspective. It will also serve as a supplement to the previous report.

“The rise of ETH is not driven by the purchase or publicity of one or two institutions. It is the common choice of mainstream institutions when changing their layout, and the critical point of trend change is coming soon.”

1. Start with the data

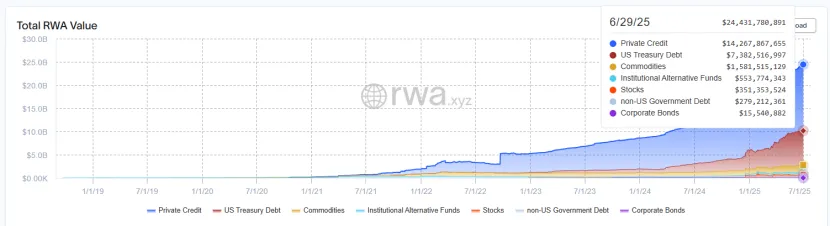

Stablecoins have achieved a development speed that exceeds market expectations, with a total market value of $258.3 billion, a record high. The US "Genius" Act passed the Senate vote and entered the Republican-led House of Representatives stage. Trump requires the US Stablecoin Act to complete the legislative process before the August congressional recess. Hong Kong's "Stablecoin Ordinance" has been passed and will take effect on August 1. US Treasury Secretary Bessant predicts that if the US Stablecoin Act is passed, the market value of stablecoins will grow rapidly to more than 2 trillion in the next few years (10 times the current level). Asset tokenization is one of the fastest growing markets besides stablecoins. RWA has grown from 5.2 billion in 2023 to the current 24.3 billion US dollars, an increase of 460%.

At present, the total market value of traditional finance exceeds 400 trillion, the total market value of the crypto market is 3.3 trillion, the total market value of stablecoins is 0.25 trillion, and the total market value of RWA is 0.024 trillion. According to industry forecasts such as Standard Chartered Bank, Redstone, and RWA.xyz, by 2030-2034, 10%-30% of the world's assets may be tokenized, that is, the scale will be 40-120 trillion, and the total market value of RWA is expected to expand to more than 1,000 times its current value.

What other businesses are the BlackRocks, which are the most active in promoting stablecoins and cryptocurrency ETFs, planning?

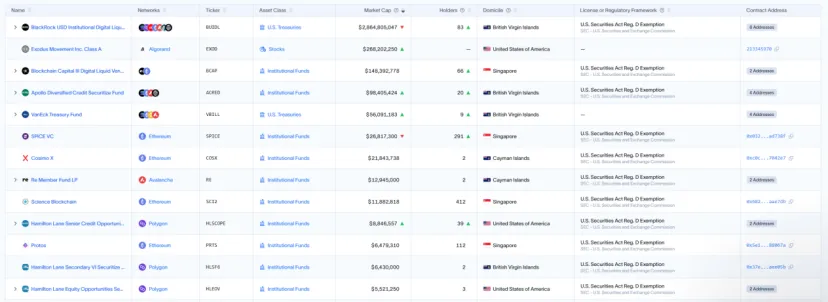

(1) BlackRock BUIDL Fund: BUIDL (BlackRock USD Institutional Digital Liquidity Fund) is a blockchain-based tokenized USD-pegged fund launched by BlackRock. It uses tokenized form to represent underlying assets (mainly U.S. Treasury bonds). Its current AUM has reached US$2.86 billion (11.7% of the RWA market), and 95% of its funds are deployed on Ethereum.

(2) Securitize: An asset tokenization company led by BlackRock and Jump, with participation from Coinbase and other institutions. In addition to issuing BUIDL with BlackRock, it has also cooperated with a number of traditional financial institutions to issue a variety of tokenized products: working with Hamilton Lane to tokenize its private equity funds; working with VanEck to explore the issuance of tokenized investment products; working with Apollo to tokenize some of its private credit and alternative investment products; and assisting KKR in fund tokenization. The market value of tokenized products issued by Securitize reached US$3.7 billion (15% of the RWA market), 80% of which are deployed on Ethereum.

(3) Franklin Templeton BENJI Fund: BENJI (BENJI Tokenized Fund) is a tokenized fund launched by Franklin. It converts traditional assets (money market funds or bonds) into digital tokens, realizes the digitization and splitting of assets, allows small investors to participate, and supports smart contract functions for profit distribution or reinvestment. Currently, the AUM is US$743 million (3% of the RWA market), 59% of the funds are deployed on Stellar, and 10% are deployed on Ethereum.

There are more traditional finances promoting asset chain and asset tokenization business. The current wave of institutional adoption represents the finalization of years of infrastructure construction towards production-scale deployment.

Re-examining RWA

RWA (Real-World Assets) refers to the digitization of tangible or intangible assets in the real world (such as real estate, artworks, bonds, stocks, commodities, etc.) and mapping them to digital tokens or assets on the blockchain through blockchain technology or tokenization. In a broad sense, I think that RWA in the industry mainly corresponds to the on-chain and tokenization of any assets other than blockchain native assets, so that the ownership, circulation and settlement of the underlying assets are all completed through the blockchain.

Tokenization has the following structural advantages:

1. Programmability - Smart contract-driven asset management innovation: Programmability means encoding the rules, conditions and execution logic of assets into automated, verifiable code through smart contracts on the blockchain. Tokenized assets can be embedded with functions such as dividends, redemption, and pledge, eliminating manual intervention. It enables assets to shift from static holding to dynamic management, and evolve from manual data transmission to on-chain automated updates.

2. Settlement Revolution - Efficiency Improvement and Risk Control: Tokenization achieves point-to-point instant settlement through blockchain, replacing the lengthy T+2 settlement cycle that has plagued the traditional financial system for many years. The two parties to the transaction can directly transfer ownership through tokens without the need for centralized intermediaries, reducing counterparty risks and capital requirements.

3. Liquidity Revolution - The core of traditional finance embracing encryption: Tokenization will significantly improve asset liquidity by dividing traditionally low-liquidity assets (such as real estate, private equity, etc.) into standardized small tokens, trading them in the secondary market and combining them with the gradually mature DeFi system. The unique 7*24 trading environment of blockchain further amplifies this effect.

Every time an asset is put on the chain, settlement efficiency is improved and idle assets are used by DeFi. "The faster the value is liquidated, the more frequently funds are reinvested, which further expands the overall economic scale. The business model will no longer rely on charging for the [flow] process, but will create new sources of income through the [momentum] effect" (-Sumanth Neppalli). This is the core of traditional finance merging with encryption.

4. Global accessibility - breaking geographical barriers to capital fragmentation: Tokenization relies on the distributed nature of blockchain, allowing global investors to access tokenized assets through the Internet without the need for complex cross-border intermediaries or local accounts, which significantly expands the investor base while reducing distribution costs. The global application of stablecoins is the best testimony, and this trend is being derived in more markets such as the stock market.

What assets are being tokenized?

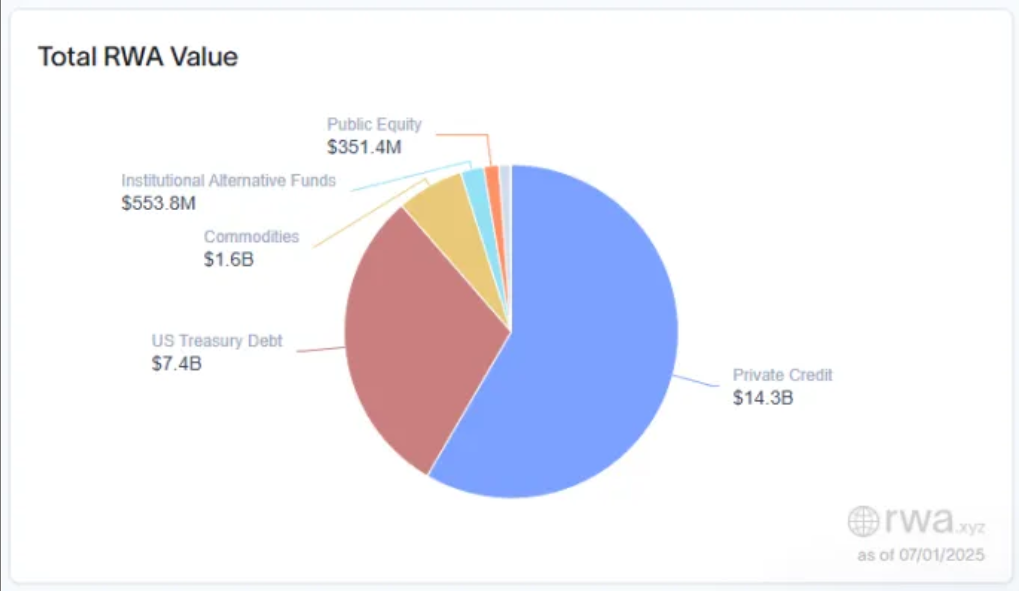

1. Private credit - the largest RWA tokenization area: Contrary to most people's perception, private credit is currently the largest market for asset tokenization, with a total size of US$14.3 billion, accounting for 58.8% of the total RWA size. Figure, Tradable, and Maple are providing active loans of 10.6 billion, 2 billion, and 800 million, respectively.

2. Treasury bonds - the starting point of tokenization for traditional institutions: The tokenized treasury bond market has reached $7.4 billion, accounting for 30% of the total RWA size. Representative examples include BlackRock’s BUIDL, Franklin Templeton’s BENJI, Superstate’s USTB, and Ondo Finance’s USDY. Traditional financial institutions have begun to explore the development of derivative financial products on the chain and DeFi integration based on tokenized treasury bond products.

3. The tokenized stock market is accelerating: On June 30, the crypto exchanges Kraken and Bybit announced the launch of tokenization of US stocks and ETFs through xStocks, achieving 5*24 hours trading. Although it is not a stock native to the trading blockchain, it can participate in spread trading through stock tokenization, breaking the geographical boundaries of the US stock market. Robinhood announced that it is building the "Robinhood Chain" on the Arbitrum blockchain, aiming to support the decentralized management of future asset ownership. This marks its transformation from a traditional broker to a blockchain-native platform. It divides stock tokenization into three stages to integrate blockchain to gain composability advantages. At the same time, Coinbase positions tokenized stocks as a "top priority", and its chief legal officer Paul Grewal is actively seeking approval from the US Securities and Exchange Commission (SEC) to provide blockchain-based stock trading services, and will use its Base Layer 2 network as a potential infrastructure for future tokenized stock settlement. This year, we may witness these leaders launch popular stocks native to the blockchain.

4. Commodity tokenization is dominated by gold: Gold accounts for almost 100% of tokenized commodities. Paxos Gold (PAXG) leads with a market value of approximately $850 million.

5. Active exploration of private equity tokenization: Private equity is the ultimate goal of tokenization. This technology can solve decades of structural problems and change the extremely poor liquidity of traditional private equity.

3. Stablecoin-RWA-DeFi

Stablecoin is the most important underlying foundation for the integration of traditional finance into the chain. It makes currency programmable and decentralized, and is the basis for the circulation and settlement of all financial assets on the chain. In an interview with Dr. Xiao Feng, Chairman of Hashkey Group, and Professor Meng Yan, they also shared that "the US President's team and Congress are relatively frank and transparent about the motivation for stablecoin legislation. The first is to modernize the US payment and financial system, and the second is to consolidate and enhance the status of the US dollar and create trillions of dollars in demand for US Treasury bonds within a few years." "Bitcoin national reserves are second to the United States, and the US dollar stablecoin is first, which is the core interest of the United States."

The rapid development of RWA this time is due to the fact that institutional compliance is constantly exploring new ways of integration and promoting the legislation of the Digital Asset Market Structure Act. When the legislation of the stablecoin and market structure bill is completed, a large number of assets will be quickly pushed onto the chain, and transactions, income, settlement and other links will be run on the native blockchain, with stablecoins as the basic currency unit and value carrier.

After a large number of assets are put on the chain, DeFi will begin to play a role, integrating the newly put on the chain assets with the increasingly mature DeFi protocols to achieve efficiency, automation, and compliance. It will promote the creation of derivative products and the generation and distribution of high-liquidity income. This cycle may be a new round of booming development opportunities for the entire DeFi ecosystem since the DeFi Summer.

The case for the integration of RWA and DeFi

1. Securitize connects DeFi system through sTokens:

Securitize, the world's largest issuer of tokenized assets, does not support the use of native tokenized securities in direct DeFi protocols due to compliance considerations. The tokens must first be deposited in sVault to mint a DeFi-compatible version, sTokens, which can then be connected to the existing DeFi ecosystem.

BlackRock BUIDL and Euler Protocol: Securitize’s sBUIDL (a derivative token of BUIDL) has been connected to the Euler lending protocol on Avalanche. After holders deposit sBUIDL into the sToken Vault, they can borrow other assets while continuing to receive daily returns on BUIDL.

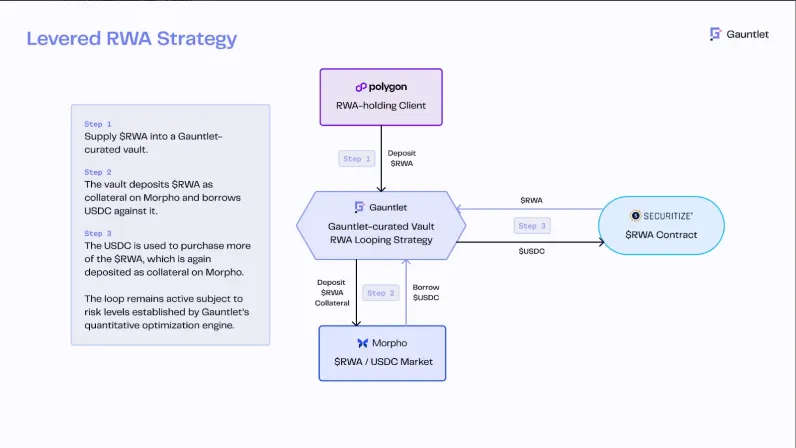

Apollo ACRED and Morpho Protocol: The sToken version of ACRED (sACRED) runs on Polygon PoS through Morpho. Holders can borrow USDC with sACRED as collateral, which is automatically reinvested to amplify returns.

2. Ethena’s USDtb merges with BUIDL to obtain a stable lower limit of income

Ethena Risk Committee approved USDtb as the primary backing asset when the Delta Neutral Funding Strategy reaches a local minimum. 90% of USDtb’s reserves are held in BlackRock’s BUIDL Fund, which has a dual function: providing low-risk collateral for margin trading on centralized exchanges and providing compliant treasury exposure in adverse funding environments.

“USDe’s addition of USDtb support indirectly catalyzes the explosion of sophisticated DeFi yield strategies, particularly Pendle’s robust money markets for split principal (PT) and yield tokens (YT) — instruments that traditional finance views as interest rate markets. USDtb support provides critical yield floor stability (typically 4-5% APY) during periods when crypto derivatives funding rates turn negative or significantly compress. This predictable minimum yield foundation is critical to PT token valuation and AAVE’s oracle system, enabling a more accurate pricing model and a safer liquidation mechanism for zero coupon bond mechanisms.”

Currently, traditional financial institutions are starting from stablecoins and based on tokenized treasury bond products, and are beginning to explore the development of on-chain derivative financial products and the compliant integration of DeFi.

4. ETH is the mainstream choice of institutions at present

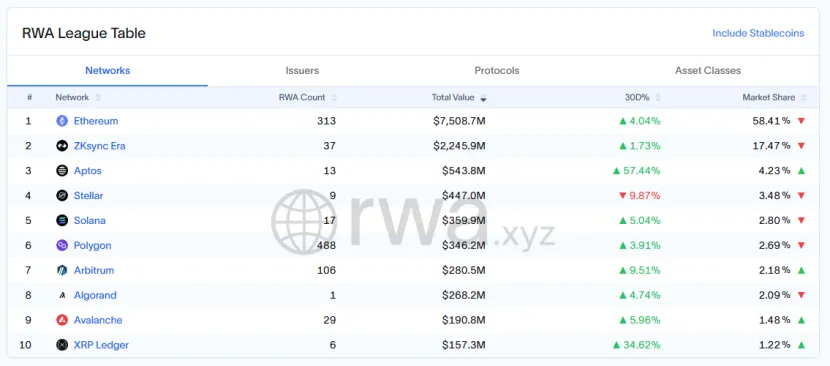

Judging from the current data, ETH is still the main public chain for institutions to tokenize assets. The tokenized market value on ETH is 7.5 billion US dollars, accounting for 58.41% of the total scale. The tokenized market value on ETH's L2 ZKsync Era is 2.245 billion, accounting for 17.47%. Among other public chains, Aptos, which ranks first, has a tokenized market value of 540 million US dollars, accounting for about 4.23%.

From the underlying logic, there are three reasons why institutions prefer ETH as the main position for asset chaining:

1. Ethereum has the highest security among all public chains. It has a cumulative security record of ten years, and has never had any serious problems such as downtime. When Ethereum upgraded from Pow to PoS, its ability to complete the core architecture upgrade without downtime was described as "changing the engine of an airplane in flight." The stability demonstrated by its excellent technical foundation and organizational integration capabilities is in line with the prudent principle of institutions in laying out new businesses.

2. It has the most mature DeFi ecosystem, the best liquidity, and the most mature DeFi protocol. Most of the most innovative product mechanisms exist on Ethereum. After institutions are on the ETH chain, they can quickly access the mature DeFi system and enjoy the best liquidity.

3. Extremely high decentralization and global business reach are also the interest balance center for large institutions and global investment. One of the reasons why stablecoins are so strategically important to the United States is that stablecoins achieve decentralized global reach through the chain, breaking the national currency barriers that were divided by politics in the past, and pushing the equivalent of the US dollar to the world through the Internet. The same is true for asset tokenization. For example, the recent tokenization of US stocks has enabled people who could not invest in and trade US stocks in the past to bypass national access and participate in US stocks through the chain. Thanks to the best liquidity and influence, ETH is the preferred public chain for global business reach. At the same time, thanks to its decentralized characteristics, it is the interest balance center for large institutions and global investors. Large institutions in sovereign countries are not willing to choose a public chain that is completely dominated and controlled by another country to issue products and participate in large financial activities.

See what Etherealize says

EF has undergone significant functional differentiation and specialization, with internal reorganization into three business groups and the separation of specific functions to external organizations, thus Etherealize was born. It is positioned as the "institutional marketing and product pillar" of the Ethereum ecosystem, focusing on handling the connection with traditional finance and Wall Street to accelerate the adoption of Ethereum in institutions.

Etherealize believes that ETH should not be evaluated as a tech stock, but as a whole new category of assets: ETH is digital oil - an asset that powers, guarantees and reserves the new financial system of the Internet

“The traditional financial system is at the beginning of a structural transition from analog infrastructure to a digital-native architecture. Ethereum has the potential to become the foundational software layer — similar to an operating system, such as Microsoft Windows — upon which the world’s new financial system will be built.

When this happens, ETH will become the base asset for a comprehensive global platform that will encompass the future of finance, tokenization, identity, computing, AI, and more. This inherent complexity makes ETH harder to define, especially relative to simpler store-of-value assets like Bitcoin — but it also makes ETH more strategically valuable and means ETH has greater long-term potential.”

At the same time, ETH is not just a cryptocurrency, it is a multifunctional asset, whose functions include: computing fuel; value storage asset with income; original settlement collateral; deflationary asset; embodiment of tokenized economic growth; reserve trading pair; strategic reserve asset.

Therefore, ETH cannot be accurately valued using a discounted cash flow approach. Instead, ETH must be viewed from the perspective of a strategic store of value and utility-driven scarcity. ETH powers the digital economy, secures the digital economy, captures value from its growth, and is inherently scarce due to its supply dynamics and issuance cap. As the global economy transitions to a tokenized infrastructure, ETH will become indispensable, not just as a fuel, but as the native asset of the currency and settlement layer of the future financial system.

Why is ETH lagging behind BTC?

The answer is simple: Bitcoin’s narrative has been embraced by institutions, while Ethereum’s narrative has not. In contrast, Ethereum’s value proposition is harder to define — not because it is weaker, but because it is broader. Bitcoin is a single-purpose store of value asset, while Ethereum is the programmable foundation that supports the entire tokenized economy.

The process of accelerating ETH repricing is happening:

1. Demand surge: Institutional adoption and deployment of tokenized assets and financial infrastructure on Ethereum has begun at a rapid pace, as evidenced by the data in this article.

2. The demand for native crypto income is accelerating: As institutions tend to build on ETH on a large scale, it is only a matter of time before Ethereum ETF staking comes into being. The emergence of institutional physical subscription/redemption models will also greatly increase institutions’ interest in ETH staking income.

3. Strategic hoarding of ETH: A competition is underway in the Ethereum ecosystem to hoard ETH as a monetary premium value storage asset. Recently, Bitmine Immersion Technologies, a US-listed company, raised $250 million to launch its ETH financial strategy, pushing its stock price up from $4 to a maximum of $74 in two days, an increase of more than 180%.

4. ETH as an institutional treasury asset: ETH’s unique characteristics — original collateral, neutrality, yield, and global utility — make it the preferred treasury reserve asset for institutions and globally.

In short, ETH is not the only option for institutions to enter the blockchain in the long term, but it is the best solution for large-scale asset on-chain. Combining data, examples, underlying logic and recent Big News, the trend of ETH being re-emphasized is imminent.

References

1. Beyond Stablecoins

2. "Real-World Assets in Onchain Finance Report"

3. "The Bull Case for ETH"

4. "Dialogue with Dr. Xiao Feng: US Dollar Stablecoin and RWA"