BTC Volatility: Week in Review July 15–22, 2024

Key Metrics: (July 15 4pm -> July 22 4pm Hong Kong time):

BTC/USD +7.0% ($62,840 -> $67,240), ETH/USD +3.9% ($3,350 -> $3,480)

BTC/USD December (end of year) ATM volatility + 15% (59.5 -> 68.5), December 25 day RR volatility + 40% (5.2 -> 7.3)

Market events:

Trump's assassination attempt boosted his election odds (60% -> 70%)

Trump's continued pro-cryptocurrency rhetoric drives bullish sentiment in the market ("America's first crypto president")

JD Vance Selected as Trump's Running Mate (Pro-Crypto, Anti-Big Tech)

ETH/USD ETF is expected to be launched on July 23

The 2024 Bitcoin Summit will be held in Nashville, with Trump as the keynote speaker. Market rumors of the possible announcement of a strategic reserve of Bitcoin have brought a huge premium in the options market.

Biden drops out of presidential race, endorses Kamala Harris — BTC/USD rises further despite Trump’s election odds dropping from 70% to 63% (while Harris’s rise from 19% to 29%)

ATM Implied Volatility:

As bullish sentiment returns, implied volatility moves higher across the board, with a huge premium embedded in the BTC$ front curve for a 2024 Bitcoin peak — the daily volatility gap also reached 7% due to Trump’s keynote (this is reflected in the options expiring on July 27, but can currently be observed in the options expiring on August 2, where this implied volatility has risen from 50 to 67.5)

In the term structure chart, implied volatility is almost all rising, with the ATM implied volatility for September 27th rising from 51 to 64.5, while the ATM implied volatility for the year end rose from 59.5 to 68.5.

As prices continued to move higher, realized volatility remained subdued—observed high-frequency realized volatility remained around 43 during this period, while daily volatility was just below 50.

On the eve of the meeting (July 23-26), there was a significant volatility spread in the options expiring during the week, among which the uncertainty brought by the issuance of the ETH ETF was priced in the options expiring on July 24, with a premium of about 4%.

Looking further, we expect the risk premium to continue at least until the meeting. Although there is no upward breakout in the local area, we can still see a small retracement of implied volatility at the local highs.

Supply demand in the past week was heavily biased towards the demand side, mainly concentrated in the August-September bullish contracts, and the market expects that the Bitcoin Summit in 2024 will break the record high.

Skewness/Convexity:

Volatility skew rose significantly this week (tilted to the upside), reflecting renewed bullish sentiment and a repricing of tail risk premiums influenced by the above narrative. During the week, the 25d RR due on August 30th rose from 1.5 to 5.0, and once broke through the local high of 7.0!

Spot and implied volatility are highly positively correlated locally, with implied volatility rising as spot prices rise and falling from local highs when spot prices pull back. While this partially explains the rise in 25d RR, as mentioned earlier, realized volatility does not rise significantly when spot prices rise, indicating that the market has factored in a large amount of additional premium on the tail scenario of a sharp rise, especially considering that BTC has the opportunity to be used as a strategic reserve.

Since spot prices have reflected the expectation of a strategic reserve announcement at the 2024 Bitcoin Summit, the market may be disappointed if no such announcement is made. Therefore, as spot prices move higher, the short-term risk reversal of the event should weaken (which is indeed what we have observed in the past 24 hours)

Overall demand for options has clearly skewed to the upside over the past week, which has also exacerbated the implied volatility in the skew.

Overall, market demand for options last week was strongly bullish, which also exacerbated the skew in implied volatility.

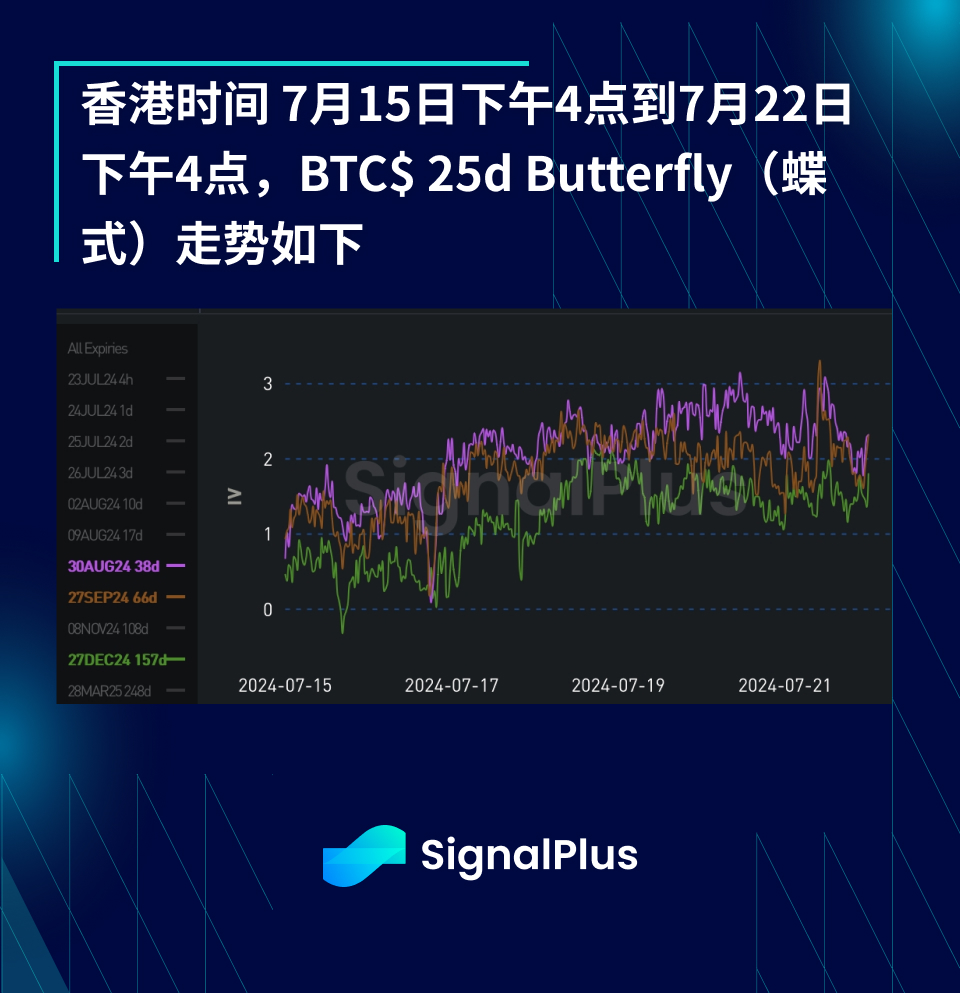

Over the past week, the convexity of the curve has become flatter than the risk reversal trend. The 25-day butterfly premium has risen as the underlying volatility has risen.

This is despite the extremely high IV volatility we have experienced over the past two weeks, while observing a strong correlation between risk reversal levels and spot (i.e. risk reversals favored calls when spot prices were rising, and favored puts when it fell to 54k three weeks ago).

Overall, while we continue to observe structural supply to the wing premium for Overlay and Call Spread strategies, this week we observed a higher proportion of Outright transactions (less wing supply)

Good luck this week!

You can search for SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time encryption information. If you want to receive our updates immediately, please follow our Twitter account @SignalPlus_Web3, or join our WeChat group (add assistant WeChat: SignalPlus 123), Telegram group and Discord community to communicate and interact with more friends. SignalPlus Official Website: https://www.signalplus.com