Data extraction: ETFs are delaying the real bull market

Original|Odaily Planet Daily

Author: jk

Since the cryptocurrency market turned bullish this year, the emergence of ETFs has been seen by many as an important sign of mainstream financial market acceptance of digital assets. The approval of Bitcoin ETFs and other cryptocurrency-related ETFs has undoubtedly opened the door for traditional investors to enter this emerging market, bringing unprecedented liquidity and exposure.

However, these seemingly positive developments may hide potential risks to startup crypto projects and the health of the small cryptocurrency market. As a large amount of retail funds flow into these widely publicized financial products, funds that would otherwise flow to the primary and secondary markets are absorbed in large quantities, which may lead to a lack of attention for new projects or a lack of follow-up. This article will explore the "double-edged sword effect" of cryptocurrency ETFs and how it affects the capital distribution and market dynamics of the entire crypto ecosystem.

In short, is the popularity of Bitcoin and Ethereum ETFs at the expense of draining funds that would otherwise flow into new projects, thereby killing the future vitality of the cryptocurrency market? Is the bull market we are facing a real bull market?

Opinion: Capital concentration may deprive new projects of liquidity

The logic of the above argument can actually be explained from two directions.

First, it is a relatively healthy way for the cryptocurrency market: the approval and issuance of Bitcoin and Ethereum ETFs actually brought new funds and new attention to the industry, so that more people began to pay attention to the technical iterations and primary market projects in the cryptocurrency circle, thus bringing more people to join the market to make the market hotter. This is also the logic of the traditional bull market, that is, new projects and narratives bring more funds and players.

But looking at it the other way around: the issuance of Bitcoin and Ethereum ETFs will not only bring in new funds, but will also affect investor behavior and drain future liquidity from the market; many retail investors and investors who don’t know much about cryptocurrencies are likely to invest their funds directly in ETFs at the beginning of the bull market, and new projects will face the embarrassing situation of having no users and no audience who recognize the technical narrative.

In other words, if you are a novice investor who knows nothing about cryptocurrency, you now actually have a choice: put your money into the exchange, read a lot of technical articles and information, and try to get a market alpha after understanding it clearly, or directly top up ETFs to enjoy the beta of cyclical dividends? Obviously, the latter is easier for novices, but the former will make the cryptocurrency market more diversified.

Arthur Hayes actually briefly touched on this topic before the ETF was approved. He felt that it was fatal for one or a few large institutions to hold the vast majority of Bitcoin in the market, which could affect the consensus of Bitcoin becoming an unregulated decentralized currency, or the centralization effect of the control of mining groups. Today, just 5 months later, are we already witnessing a negative effect of capital concentration in ETFs: depriving new cryptocurrency projects of liquidity?

As the ETF storm blows, some are happy and some are sad?

Since both the pros and cons are logically plausible, let’s see which side the actual data leans towards.

The brilliant success of Bitcoin ETF

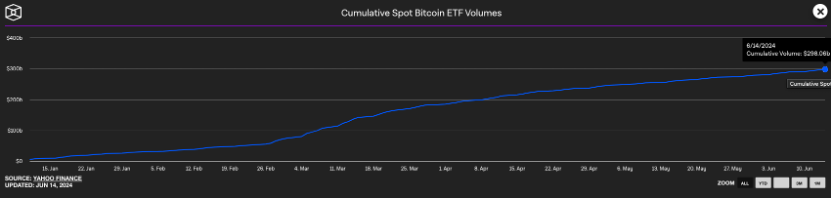

It goes without saying that Bitcoin ETF has been so successful so far. Although there have been several ups and downs, in general, since the beginning of this year, not only has the price of the currency been rising all the way, establishing a new support level, but the funds of the ETF have also been rising all the way. If we ignore the daily inflow and outflow of funds and only look at the amount of funds of the entire spot Bitcoin ETF from a macro perspective, the cumulative data is rising all the way:

Spot Bitcoin ETF accumulated funds, source: The Block

This figure currently reaches a total circulation of 298 billion US dollars. In other words, no matter how Grayscale sells, no matter how much net outflow is caused by the fluctuation of Bitcoin price in the middle, Bitcoin ETF as a whole has been absorbing funds. And part of this part of funds is the participation of new institutions, and the other part may be the funds that retail investors would have invested in the primary/secondary market. This money should have flowed to new projects; and the replacement of this part of liquidity is likely to become a nightmare for new projects.

Market data: Are we really in a bull market?

If we look at the data from a different angle, we can find some interesting points. According to Coinmarketcap data, since the beginning of 2024, the total market value of cryptocurrencies has fluctuated from 1.7 trillion US dollars to 2.4 trillion US dollars, which is a very gratifying data. But if we look at it separately, Bitcoin and ETH account for the absolute majority of this increase;

Market capitalization of each cryptocurrency sector, source: Coinmarketcap

At the beginning of the year, the market value of Bitcoin accounted for $886.7 billion, and now it is $1.3 trillion, with a market value increase of $413.3 billion, a growth rate of 46.61%. For Ethereum, this figure increased from $287.4 billion to $427.5 billion, an increase of $140.1 billion, a growth rate of 48.75%. Excluding the market value of stablecoins (described below), the market value of funds allocated to all other Altcoins, sector leaders, and new projects has only increased from $441.5 billion to $527 billion, with a market value increase of only $85.5 billion.

If we want to really examine the metrics used to measure the bull market, especially the funds that actually flow into the cryptocurrency market rather than into ETFs, we need to look at the inflow of stablecoins . And in the case of stablecoins, this metric has clearly not performed as well. Since the beginning of the year, the market value of stablecoins has increased from $128.7 billion to $154.9 billion, an increase of $26.2 billion, a growth rate of 20.36%. Although the growth is high, if we compare the data from the last bull market, the market value of stablecoins in March 2022 was $181 billion.

If we look at it in more detail, we can look at the market value of stablecoins backed by fiat currencies, which has risen from $122.6 billion at the beginning of the year to $149.1 billion today, an increase of only $26.5 billion, or 21.62%. (Comparatively speaking, the market value of stablecoins exchanged for fiat currencies at the peak of the last bull market was $155 billion, which has reached the peak scale of the last bull market, but the significance of this data is limited, because there were considerable algorithmic stablecoins represented by UST in the last bull market).

According to the argument of "100,000 Bitcoin" in this bull market, the current on-site funds have not even reached the peak level of the previous bull market from the perspective of stablecoins. In other words, without the impact of ETFs, it seems that not so much funds have entered. So, are we really in a bull market?

“Triple Kill”: The crowding-out effect of substitutes

From a macroeconomic perspective, the current cryptocurrency market belongs to the risk asset market, which is not particularly optimistic in the overall environment. The reason is that the high interest rate environment we are currently in will definitely reduce investment in risk assets. As interest rates rise, the borrowing costs of venture investors themselves increase, and interest expenses increase, so the scale of venture capital fundraising and investment is bound to shrink. Secondly, high interest rates will screen out projects with insufficient returns on investment. Projects whose return on investment does not exceed the risk-free rate will not receive investment. These projects that may obtain funds in a low-interest rate environment may not receive funds in a high-interest rate environment.

In short, if I can earn around 5% from Treasury bonds risk-free in a high-interest rate environment, why would I take the risk of entering a risky asset market that could experience a 20% drawdown?

So let’s take a look at the alternatives facing the cryptocurrency market today:

1. In terms of interest rates, the most direct risk-free alternative for US investors is the bank deposit rate. Currently, the interest rate for Marcus current deposit accounts released by Goldman Sachs has reached an annualized yield of 4.4%. At the same time, the current interest rate for one-year Treasury bonds for retail and institutional investors has reached 5.07%.

2. The second alternative is the US stock market. Currently, among the three major US stock indexes, the Nasdaq index has achieved a growth of 19.8% from the beginning of the year to date, while the S&P 500 index has grown by 14.52%. The growth of these indexes has ETFs directly targeting US dollar investors. At the same time, if you bet on monster stocks such as Nvidia (+173.78%) or GameStop (+72.17%), the returns will be higher. (I want to ask a soul-searching question here: Everyone knows that the AI boom will start in 2023, so why did you miss Nvidia in 2024?)

Trends of the three major U.S. stock indexes. Source: Google Finance

3. The Bitcoin and Ethereum ETFs themselves.

Therefore, the result is: investors have a lot of alternatives to choose from, and new funds that could have flowed into the primary and secondary markets of the cryptocurrency circle are diverted by traditional finance and ETFs, and the popularity of new projects in the secondary market continues to decline.

Here are some new coins from the top exchanges this year (previously X user @silverfang 88 also made a summary):

Altlayer, Manta, Dymension, Pixel, Portal, Saga, Renzo, Polyhedra, Zeus, Merlin are all currently below the price at the time of issuance. Most of these projects were very popular in the primary market, and many of them have very practical technical narratives. They still have the current trend in the secondary market, which is not only affected by the shipment of airdrop users, but also inseparable from the transfer of funds of most users.

And what about the future?

ETFs of the future?

From the news, we can see that there are still several ETFs in the planning;

XRP: Ripple CEO Brad Garlinghouse said he expects a spot XRP ETF to appear in 2025.

Solana: William Quigley, co-founder of Tether and WAX, said that after the approval of Bitcoin and Ethereum spot ETFs in the United States, Wall Street’s “greed” will bring more and more such products. Quigley predicts that due to Wall Street’s relentless pursuit of profits, ETFs for other mainstream cryptocurrencies such as Solana and Cardano will also emerge in large numbers.

Dogecoin: BitMEX founder Arthur Hayes and Real Vision CEO Raoul Pal recently shared insights on the potential of a Dogecoin ETF on Coin Bureau’s YouTube podcast. Arthur Hayes said that the Dogecoin ETF could be launched by the end of this cycle, and said that his prediction is based on the substantial growth rate of the doge-themed meme coin over the years, highlighting Dogecoin’s status as the oldest meme coin in the cryptocurrency space, giving it an advantage over other meme-based cryptocurrencies.

If these ETFs are approved, will it be good or bad for the crypto market? Judging from the data, it may not be a good thing.

In summary, while cryptocurrency ETFs bring mainstream recognition and additional liquidity to the crypto market, they also raise concerns about increased market concentration. This trend of funds concentrating in a few large assets is likely to inhibit the growth of emerging crypto projects. In this context, we need to be extra cautious about the outlook and judgment of the crypto market.