21Shares Report: What’s Different About the Fourth Bitcoin Halving?

Original author: 21 Shares

Original compilation: Peng SUN, Foresight News

TL;DR

The net inflow of the U.S. Bitcoin spot ETF exceeded 10 billion US dollars, and the holdings exceeded 400,000, which has exceeded the annual supply (approximately 164,000) after the halving in April. The United States has a $7 trillion ETF market, four times that of Europe. As long as 1% of funds flow in, the market value of Bitcoin will double. The supply of Bitcoin is getting smaller and smaller, and the balance on exchanges is now 2.3 million, a five-year low. The BTC holdings of long-term investors who have held Bitcoin for more than 155 days dropped from 14.9 million to 14.29 million, accounting for nearly 70% of the total supply; the BTC holdings of short-term holders increased from nearly 2.3 million to 307 10,000 pieces, an increase of over 33%. Bitcoin has reached a record high, but whales holding more than 1,000 BTC have not sold. They believe that BTC still has huge room for growth. Comparing March and October 2021, whales sold Bitcoin at $60,000, and then BTC hit a record high. Looking at the MVRV Z-score, Bitcoin investors have been chasing gains over the past month, but it still suggests we may be in the early stages of a bull market. At present, the average net unrealized profit and loss (NUPL) is 0.6, and the market has not yet entered the extremely greedy stage. This is because the inflow of ETFs seizes the opportunity of expected market activities after the halving. If the situation is urgent, then Bitcoin is likely to rise in the next few weeks. Consolidate within. Bitcoin is no longer just a savings value, Ordinals, BRC-20 tokens, BTC L2, etc. will drive more demand for Bitcoin and expand its use cases.

In April 2024, Bitcoin will usher in its fourth halving. Judging from the situation, Bitcoins price performance will be excellent in the 12 months after previous halvings. However, this halving seems to be different from the past. On this occasion, Foresight News will compile the best of 21 Shares’ Bitcoin halving report, delving into the impact of the 2024 Bitcoin halving and its impact on the Bitcoin market, mining and the entire ecosystem.

What is the impact of Bitcoin’s four-year halving cycle?

Why does it halve every four years?

Although we do not know why Satoshi Nakamoto set a four-year halving cycle, this cycle coincides with major events such as the U.S. election, bringing uncertainty to the market. Since U.S. fiscal policy has a large impact on the global economy, the Bitcoin halving can be seen as an intention to provide stability to the volatile traditional financial system during a period of political transition.

Of course, these four years, while not an exact match, may serve as a psychological benchmark, such as traditional economic cycles, elections, or major sporting events.

How does the halving affect Bitcoin price?

The impact of Bitcoin halvings is getting smaller and smaller, and the growth brought about by each halving will decrease. Bitcoin skyrocketed by about 5,500% in the cycle after the first halving, by about 1,250% in the cycle after the second halving, and by about 700% in the current cycle.

In other words, Bitcoin’s steady growth over the years indicates a maturing market. Explosive growth is often accompanied by hype and speculation, while more sustained growth rates indicate increased stability and wider applications, similar to traditional assets such as gold.

However, there is a big difference in this cycle, which is the exogenous demand brought by ETF inflows, which caused Bitcoin to break through its all-time high before the halving, so it is likely to bring about a new round of growth that is different from the past. . Of course, this could also stem from supply shocks, which we explain further below.

How will the halving affect miners?

The impact of Bitcoin halving on miners includes several aspects, such as a reduction in block rewards, changes in profitability and operating costs, but these all depend on the Bitcoin price at the time.

For example, while block rewards may decrease, the price of Bitcoin will increase accordingly. For example, mining companies such as Marathon and Core Scientific will choose to refinance to avoid the shutdown of mining machines.

Of course, the miners were not miserable either. If miners exit the network, mining difficulty will decrease, thereby reducing electricity bills and making Bitcoin mining more cost-effective. At this time, miners will also rejoin the network, thereby increasing computing power. Conversely, some miners may sell Bitcoin, which we will explore further in conjunction with other alternative indicators that can help estimate their selling pressure.

What will miners do before the halving?

Miner deposits to exchanges are an important indicator. Typically, miners sell BTC to cover operating costs such as electricity bills and hardware expenses. However, in this halving cycle, miners are selling less than in previous cycles.

Throughout February 2024, miners deposited an average of 127 BTC to exchanges, which was nearly 70% less than the previous cycle: between February and March 2020, miners deposited 417.4 BTC to exchanges. However, it is important to note that miners must pay their operating costs in US dollars, and the increase in Bitcoin prices after the adoption of the ETF is also the reason for the reduced BTC selling volume.

The Halving Effect: Bitcoin’s Four-Year Cycle Compass

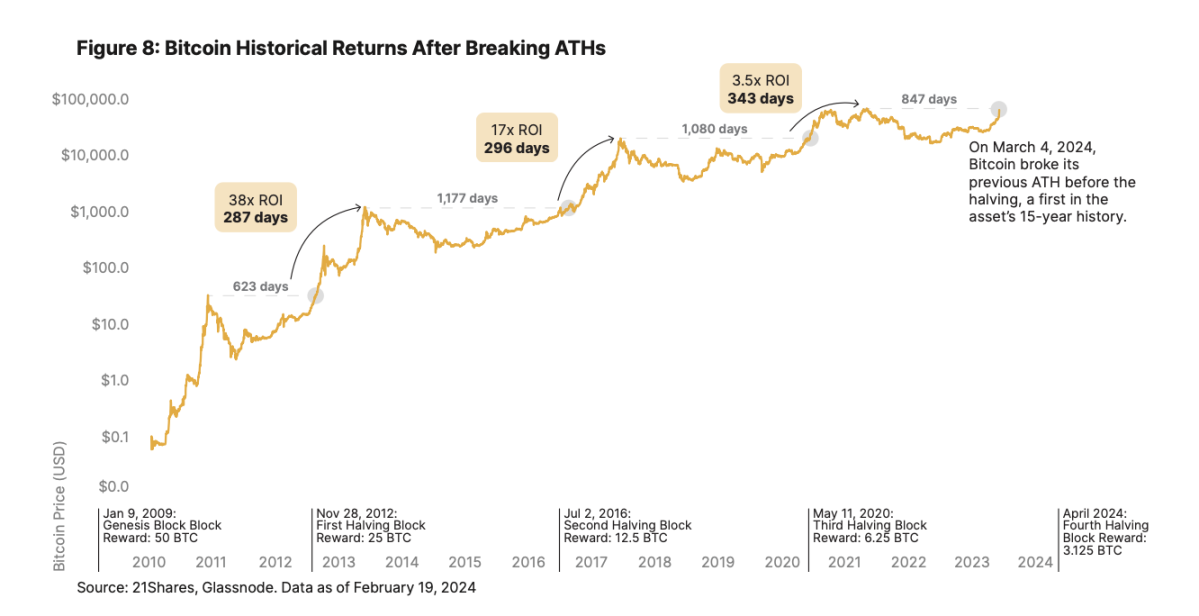

Historically, Bitcoin has performed very well in the 12 months following the halving. On average, Bitcoin takes 172 days after a halving to break through its previous ATH value, and 308 days after a breakout to reach a new cycle top.

However, with Bitcoin currently trading around its ATH, it looks like this cycle may play out differently, as in the past, Bitcoin has traded an average of 40% higher than its previous high in the weeks leading up to the halving. % -50%. In addition, Bitcoin also had the strongest monthly positive line in history in February.

What’s different about this halving cycle?

This time the Bitcoin halving seems different from the past. More and more institutions are adopting Bitcoin, and the scope of Bitcoins use is becoming wider and wider. Let’s explore the current supply and demand situation of Bitcoin so that we can better analyze the differences.

Demand Side: ETF Buying Pressure

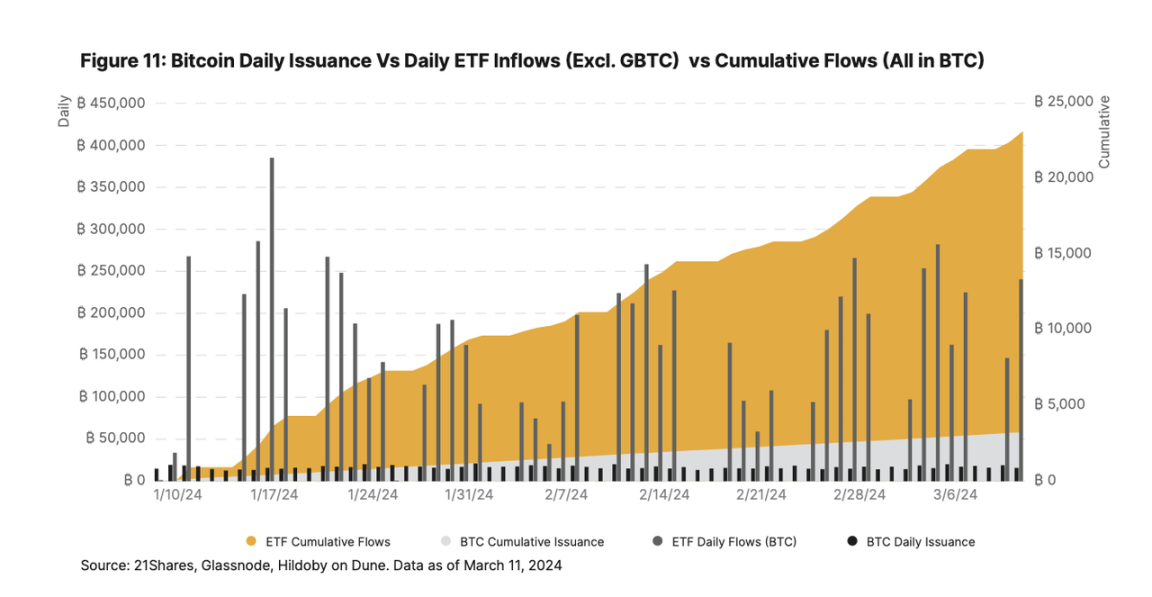

U.S. spot ETFs have shown growing interest in Bitcoin as the currency has continued to grow in recent weeks, attracting more than $10 billion in net inflows to date. In other words, the 14-day average inflow of approximately 2,500 Bitcoins (approximately US$150 million) is 3 times the daily new output of BTC (900 Bitcoins), and will be close to 5.5 times (450 Bitcoins) after the halving.

As can be seen in the figure below, the ETF holds more than 400,000 Bitcoins, which has exceeded the annual supply of Bitcoin after the halving in April (approximately 164,000 Bitcoins). Furthermore, according to Glassnode’s average of highly liquid and liquid assets, plus short-term holder supply and exchange balances, current demand already covers approximately 4.5% of Bitcoin’s available supply, totaling approximately 4.7 million BTC.

In addition, the United States has a $7 trillion ETF market, four times that of Europe. Before ETF approval, 77% of asset managers were unwilling to invest in Bitcoin. In the United States, registered investment advisors manage approximately $114 trillion in assets, and they are required to wait 90 days after the launch of new products before they can invest. Therefore, as long as 1% of funds are allocated to Bitcoin, it will trigger a massive Capital flows in, doubling Bitcoin’s market value and making supply tighter.

Currently, banks such as Wells Fargo and Merrill Lynch already offer spot Bitcoin ETFs to some wealth management clients, while Morgan Stanley is said to be evaluating Bitcoin funds for its brokerage platform. Cetera was also one of the first wealth managers to launch a formal policy on a Bitcoin ETF, signaling the beginning of a new wave of demand.

Supply side: increasingly insufficient liquidity

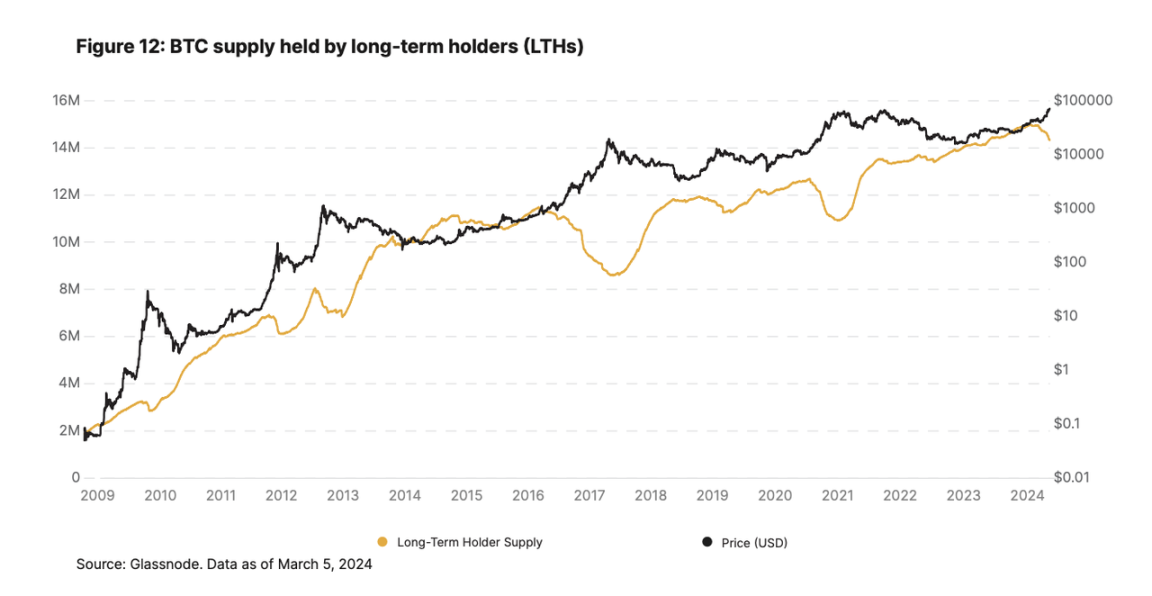

Investors who have held Bitcoin for more than 155 days have a very firm belief in Bitcoin. Long-term Bitcoin holders surged to an all-time high (14.9 million coins) in December before falling back to the current level of around 14.29 million coins (nearly 70% of the total supply).

Similar to what happened in 2017/18 and 2020/21, in this cycle since the adoption of ETFs, long-term holders have gradually sold at high prices.

However, although the BTC holdings of long-term holders fell from 14.9 million to 14.29 million (a decrease of 4%), the BTC holdings of short-term holders surged from nearly 2.3 million to 3.07 million, an increase of Over 33%. A balance has developed between the two groups, which typically occurs in the early stages of a post-halving bull run, but is now occurring earlier due to exogenous demand for ETFs, resulting in market forces approaching neutrality.

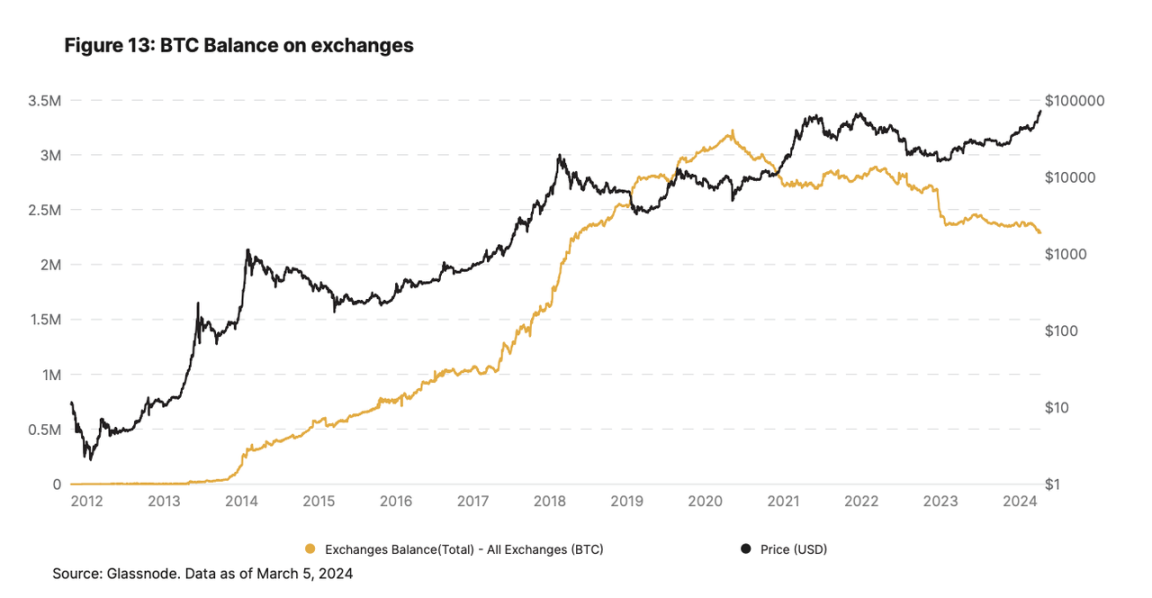

In this case, the exchange balance of BTC will hit a five-year low, reaching 2.3 million, which further illustrates that the supply of BTC is declining sharply.

If this trend continues, Bitcoin’s supply side will become increasingly illiquid, setting the stage for tight supply and a potential parabolic bull run.

On-chain changes before halving

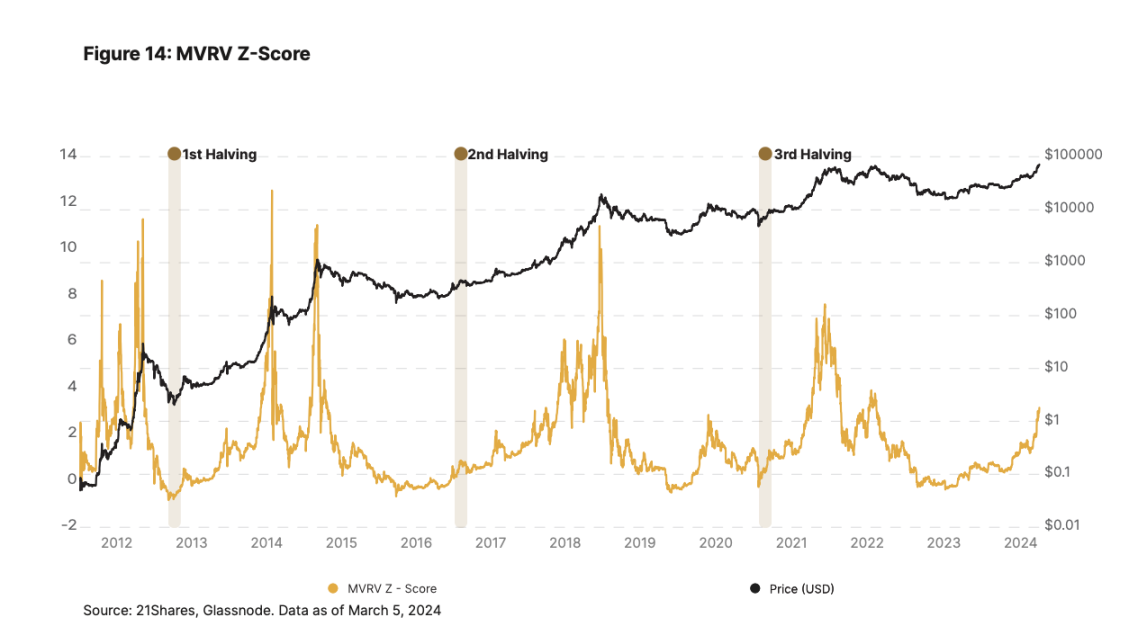

Market value to actual value ratio (MVRV – Z value)

The market cap to actual value ratio is a metric used to evaluate Bitcoin’s valuation by comparing its current market cap to its actual value. The actual value is the total value of all BTC based on its last transaction price, which basically represents the average acquisition price of all BTC in circulation. The Z-score normalizes the MVRV metric by measuring the standard deviation of current MVRV from the historical average. If the market capitalization is several times higher than its actual value, it indicates that BTC is considered overvalued, which is historically a signal of a market peak, and vice versa.

Bitcoin’s current MVRV Z-value is approximately 3, in stark contrast to a value of approximately 6 in February 2021. However, Bitcoin appears to be exhibiting a slight deviation in this cycle compared to previous halvings. Specifically reflected in the substantial increase in the actual price of Bitcoin, the average MVRV over the past 30 days was 2.4, while the average MVRV over the same period in the past three cycles was 1.07. This suggests investors may be chasing gains in the near term, as realized prices reflect the last price each Bitcoin traded at. While MVRV is elevated compared to historical averages, it still suggests that we may be in the early belief stages of a Bitcoin bull run; BTC prices are no longer just about market sentiment as the adoption of ETFs may have preempted the trend and the narrative surrounding the halving.

Net unrealized profit or loss (NUPL)

We observe something similar with Net Unrealized Profit and Loss (NUPL), a metric that assesses the profitability of Bitcoin holders by comparing the market cap of their current holdings to the original purchase price, which is a good indicator of market sentiment. 0 represents extreme fear and 1 represents extreme greed.

Currently, the average NUPL is 0.6, indicating that Bitcoin’s greed has not yet reached its peak, unlike the average of 0.7 during the period between February and March 2021 when Bitcoin rose to $60,000.

However, comparing Bitcoin’s current average NUPL with that before the three previous halving events (two months before), we can see that the bullish sentiment in the Bitcoin market is growing, with Bitcoin’s current average NUPL at 0.6, compared with the previous few halving events. The average NUPL over the period is 0.42. This further supports our view that ETF inflows are preempting expected post-halving market activity, and if the time comes, Bitcoin is likely to consolidate in the coming weeks.

Judging from the on-chain data, the performance of this cycle has been slightly different, and the cycle may be tilted to the left.

Halving coincides with favorable market structure

While 2024 is Bitcoin’s “halving year,” it also coincides with other positive factors for Bitcoin, resulting in a mix of supply and demand dynamics worth watching:

Improving macro environment: As the Federal Reserve has kept interest rates stable over the past two meetings, the market expects a 39% probability of at least one rate cut by June 2024 and a 51.9% probability of one rate cut by December 2024, according to the CME FedWatch tool. Uncertainty over rate cuts will persist as a range of conflicting data points to persistent inflation.

ETF buying pressure: The approval of U.S. spot ETFs is very beneficial to the market structure of Bitcoin. Since its launch, it has attracted a net inflow of more than 10 billion U.S. dollars. It has held more than 400,000 BTC so far, which is more than the year after the halving. Chemical issuance is more than 240% higher.

Long-term holders causing illiquidity in BTC supply: If the impact of the supply halving wasn’t big enough, as of March 15, 2024, long-term holders (i.e. those who have not moved their BTC investments for at least 155 days) The supply of Bitcoin held by investors) has stabilized at around 14.29 million BTC, accounting for approximately 70% of the circulating supply of BTC.

Bitcoin has hit an all-time high, but whales remain unmoved: Despite Bitcoin’s staggering rise since the launch of the ETF, whales holding more than 1,000 BTC did not sell when the market strengthened. Even when Bitcoin reached $60,000 (in March and October 2021, whales sold Bitcoin at $60,000 and then BTC hit an all-time high), investors still showed confidence in Bitcoin, indicating that they believed in the current There is still huge room for growth. Even though 99.6% of Bitcoins circulating supply was profitable as of March 1, everyone is still bullish.

All things considered, the largest crypto assets are overall bullish, all things considered. Our conclusion is that this cycle may indeed be slightly different. Although investors should be reminded that Bitcoin is still a relatively unstable asset and may undergo a correction, it will be conducive to entering a new bull market.

After halving

We usually think that Bitcoin has only savings value, but after the halving, Bitcoin still has new vitality.

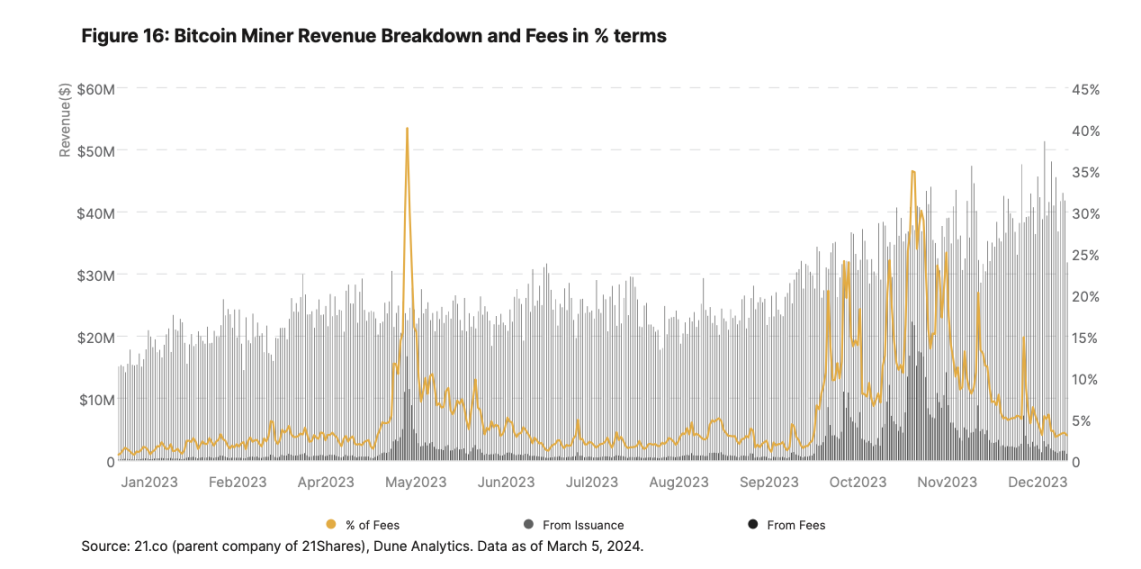

From a fundamental perspective, we expect innovations such as Ordinals and BRC-20 tokens to drive more demand for Bitcoin and expand its use cases. This is crucial as it ensures that miners can survive on transaction revenue while block rewards will continue to decrease in 2140. Since Bitcoin has a limited block size, when transaction demand increases, transaction fees also increase.

In 2023, miners transaction fee revenue increased from about 0.73% at the beginning of the year to more than 30% in December 2023, with daily transaction fees sometimes exceeding $15 million. Rising transaction fees could impact the price of smaller transactions and drive greater adoption of Bitcoin Layer 2 like Lightning Network, Stacks, and others.

However, Bitcoin expansion has also attracted market attention. Just like the early Ethereum Layer 2 solutions (Arbitrum, Optimism, Polygon, etc.), projects focused on Bitcoin expansion are also marching towards Bitcoin, and they have introduced various expansion solutions based on Optimitic Rollups and zkRollups. While their long-term development is unpredictable, they could help unlock more utility from Bitcoin and even achieve massive growth like Ethereum. It is worth noting that, led by two new Layer 2, Bitcoin TVL surged 7 times in March to $2.7 billion, ranking among the top 6 networks. Finally, from December 2023 to February 2024, Bitcoin accounted for 33% of NFT transaction volume, totaling US$2.76 billion, second only to Ethereum’s US$3.99 billion and exceeding Solana’s US$1.2 billion. It can be seen that Ordinals has a strong influence on Bitcoin The impact of the Internet is huge.