空投史学研究:撸毛党的未来在哪里?

Original author: DefiOasis

Source: GeekWeb3

Introduction: One of the biggest values we have discovered in blockchain is the ability to observe the generation and distribution of funds/wealth in a highly transparent manner. Although this approach is still in its early stages with many flaws, the long-term vision of "transparent and decentralized asset creation and distribution" demonstrates tremendous positive value for society.

Text: Despite the bear market in 2023, many projects still distributed large-scale airdrop rewards to users. The FreeMoney in the bear market attracted users, and just taking Coingecko's data as an example, in the past year, projects like Arbitrum, Celestia, and Blur have distributed approximately $4.65 billion worth of airdrops to users based on the ATH (all-time high) price of airdropped tokens.

Now, six months have passed since GeekWeb3 published the airdrop knowledge article "Airdrop History and Anti-Witch Strategy: On the Tradition and Future of Airdrop Culture" in September 2023. During this time, the Web3 industry has undergone changes, and the airdrop distribution mechanism has also evolved with new characteristics and trends. This article will analyze and educate readers about the evolving airdrop mechanisms during this period, further showcasing the possible patterns and evolution of airdrop strategies in the future.

Point system as a reference for airdrops in most projects

The popularity of the airdrop point system can be largely attributed to the promotion by Iron Shun, the founder of Blur. From Blur to Blast, the measurement of user loyalty by project teams has transformed from initial transaction volume to the amount of user deposits and their duration.

Nowadays, the point system is deeply loved by major public chain ecological projects, such as Magic Eden, Marginfi, and Kamino on Solana, Bounce Bit and B²Network in the BTC ecosystem. The rise of the re-staking concept has further pushed the popularity of the point system to its peak. With mining Eigenlayer points as the core, projects like Swell, KelpDao, Ether.Fi have launched a points stacking battle, and there are now even dual or even triple mining of LST and LRT points.

In fact, the current mainstream points system can be divided into two categories: points based on transaction volume and points based on deposits.

Points based on transaction volume are commonly seen in NFT markets, derivatives exchanges, etc. These projects encourage users to generate trading volume and it used to be the gameplay for airdrop points. For users, trading volume points can be rotated multiple times with the same amount of funds, which to some extent encourages users to have multiple addresses, making it troublesome to identify witch attacks.

On the other hand, deposit points are another mainstream points model. This measurement method is used by lending platforms, public chain projects, and the popular re-staking concept projects. In this model, points mainly depend on the amount of funds and the retention time.

In order to maximize the attractiveness to funds/capital, these projects usually do not limit the types of funds they accept, but actively absorb the influx of multiple asset types. For example, in the second phase of Merlin Chain, users are allowed to stake Bitcoin or partial Ethereum assets, as well as BRC-20, Bitamp, and BRC-420 inscription assets.

In today's Web3 world where TVL data is king, the deposit point system effectively attracts funds through airdrop expectations, but it ties up users' funds for a long time and sets a withdrawal limit period of several months, resulting in significant opportunity costs for users. In this era where witch players are everywhere and real identities are difficult to distinguish, the deposit point system can greatly increase the cost of witch attacks, just like Proof of Stake.

The airdrop expectations of the deposit point system almost immediately contribute to the growth of TVL data, making it a breakthrough for Ethereum Layer 2. Since the launch of Layer 2 in the ZK series coincided with the bear market, the TVL performance of ZkSync and Starknet has been tepid. Manta, ZKFair, and others have followed suit with Blast and surpassed the aforementioned ZK giants in TVL data in a relatively short period of time, and they still maintain good data performance after the airdrop has ended.

In addition, projects that use a deposit scoring system usually employ some soft anti-witch methods, such as binding users' wallet addresses with social accounts like Discord and Twitter. However, even so, it is still not possible to completely prevent witch attacks.

Essentially, the deposit scoring system only significantly increases the cost of launching witch attacks by the "fleecing hunter". Some projects have come up with innovative approaches, using whether the user has made deposits and pledges for other projects as a reference data for distributing airdrops. For example, when Altlayer distributes airdrops, being a "pledger for Eigenlayer and Celestia" is a powerful restriction.

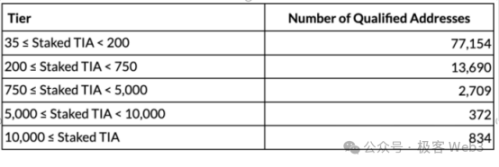

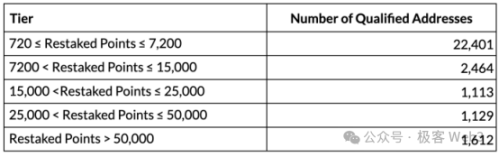

Altlayer uses a hierarchical approach for airdrops, and the distribution of points is based on the amount of TIA the user has pledged on the Celestia mainnet. Clear hierarchical divisions are made, and the amount of airdrop you can receive is determined by the amount of deposit you have made in networks like Celestia in the past, not by the number of accounts you have. However, the airdrop quota for an individual account is still limited. You can only receive rewards after meeting the minimum deposit amount, and both the lower and upper limits of the rewards are clearly defined. This fundamentally realizes the incentive layering of POS.

Although such methods of distributing airdrops resist airdrop hunters, large token holders can still split their deposits into multiple parts (similar to those who run Ethereum validators often divide their ETH holdings into multiple parts, 32 ETH each, to meet the minimum pledge threshold for each validator, and then run multiple validators).

On the other hand, to meet the expected conditions for airdrops, small-cap investors often need to consolidate funds from multiple addresses into a single receiving account. However, for the project team, money is power, and the "bourgeois" witches are valuable.

Actually, "everything can be based on a point system". In addition to the above two mainstream point calculation methods, there are also comprehensive point calculation schemes such as LineaDeFiVoyageXP, B²Buzz by B²Network, bsquaredOdyssey, and tasks released on Galxe, which are based on user transaction volume, funds duration, sign-ins, social media interactions, and inviting others to form teams. These systems consider multiple factors in order to comprehensively capture the user's contribution to their ecosystem.

Points, essentially, are a promise of airdrops, similar to options. You pay a certain cost today and can expect a return of XX in the future.

However, unlike DeFi mining with clearly marked APY, users under a point system base all their actions on conditions such as "unreleased token economic models, undisclosed airdrop allocation plans, and unpredictable market futures." It's like blind mining, and accumulating points is actually a game between users and project teams that stems from information asymmetry, testing the user's research and investment capabilities.

At the same time, airdropped points are fundamentally subject to infinite inflation. For users with less funds, the involvement of larger holders dilutes their airdrop shares. Of course, this is similar to Ethereum validators' staking. Those holding a large amount of staked funds will receive more dividends (this rule has remained constant throughout history).

Whether it's based on transaction volume or funds duration, point systems that solely measure in terms of funds undoubtedly direct the majority of rewards to larger holders. Some projects add blind boxes and random point lottery systems similar to lotteries in order to redistribute rewards to smaller funding users, seeking a balance between larger and regular users.

However, point systems have been criticized for becoming increasingly similar to existing playstyles on Web2 platforms. Obtaining points requires undertaking various complex tasks. This begs the question in the community: Are users experiencing the ecosystem or becoming slaves to project work?

Airdrops increasingly focus on core players, "sunshine inclusion" for multi-chain users

Nevertheless, the wide net-style airdrop with multiple criteria and screenings can cover as many users as possible, making different groups happy and winning project teams the support of the community. However, as the intensity of "lumbar rubbing" work increases, project teams can only rely on layer-by-layer screening to accurately distribute incentives to real users, gradually leading to the demise of wide net-style airdrops on EVM chains.

However, non-EVM ecosystem projects like Sei, Celestia, and Dymension have opened up new ideas for wide net-style airdrops. They target multi-chain user bases and distribute airdrops in a "sunshine inclusion" manner, with core distribution focused on high-quality players on the chain.

Generally speaking, the airdrop project party has multiple considerations for these high-quality users. They will consider the top-level active users on protocol platforms that have cooperation relationships with themselves on multiple chains such as EVM and Solana and have abundant funds. They will also assess the on-chain user activity based on various dimensions such as user interaction amount, transaction frequency, and gas consumption during a certain period of time. This is how they find truly high-quality active players.

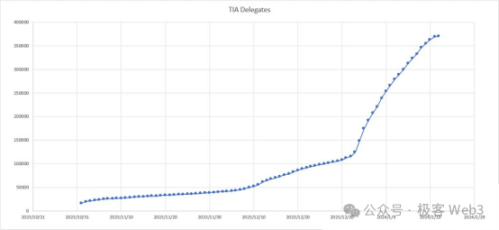

On the other hand, airdrops are often distributed to long-term staking users, especially staking whales, represented by the ATOM, TIA, and INJ stakers in the Cosmos ecosystem. Strictly speaking, staking airdrops are not a new practice. In the previous cycle, ATOM stakers received airdrops of multiple high-quality assets in the Cosmos ecosystem. However, the benefits of these airdrops were often overlooked due to the downturn in ATOM's price, which offset the airdrop profits for holders during the bear market.

(Profit of early Celestia stakers causing community FOMO, image source: @jaga 1117)

Thanks to the popularity of modular blockchain narratives, projects that claim "staking gets airdrops" have emerged one after another. Coupled with the hype around re-staking concepts, staking has once again become a popular narrative. Under the narrative of staking airdrops, different communities are spreading severe FOMO emotions, with people basically searching for the next "golden opportunity." For example, Pyth Network received more than 100,000 users' staking funds even before announcing actual APY and airdrop profits. However, as staking addresses and amounts increase, the minimum threshold for airdrops is expected to gradually rise.

The popularity of staking has also led to a nested staking ecosystem among project parties. When Project A distributes airdrops to Token stakers on partner platform B, A also introduces staking functionality for its own Token, making stakers believe that by staking and locking on the A platform, they can receive airdrops from other project parties such as C and D. This airdrop expectation (actually PUA) effectively absorbs funds from airdrop receivers on the A platform.

In this chain of conditions, an unlimited nesting of A-B-C-D Stake can be formed, and people are ultimately trapped in the expectation of Token staking, where they pay the opportunity cost of funds and receive airdrop returns. Considering that the tokens obtained from airdrops are often different from assets bought on the secondary market, the holding cost and psychological pressure are much lower in this case. Therefore, people are more willing to lock their funds on platforms with staking airdrop expectations in the long term.

In addition to the large holders who pledge tokens, some project teams may give airdrops to blue-chip NFT holders in the community, such as PudgyPenguins, BoredApeYachtClub, CryptoPunks, Comomos' BadKids on the Ethereum mainnet, and MadLads on Solana. These NFT holders are generally OG users of their respective communities.

The conclusion is that although airdrops used to be distributed to everyone, now the core recipients of airdrops are high-quality active users and large token holders. On another level, multi-chain "sunshine and inclusive" airdrops are typically used as marketing strategies for non-EVM chain ecosystems or new ecosystems, with the main goal of gaining reputation and capturing players from other ecosystems. The project teams still aim to help the growth of the ecosystem's data, increase on-chain user activity, and retain funds by allocating these airdrops to users who have made contributions as much as possible.

Future Airdrop Rules as Reference Conditions

In addition to the above points, we have identified some trends that may become reference conditions for future airdrops:

1. Airdrop allocation linked to NFTs with official backgrounds: NFTs with official backgrounds are gradually becoming the new standard for project airdrops. Although these "rights-based" NFTs do not actually have explicit airdrop allocations, through frequent mentions or indirect endorsements by project teams on social media, they have unwittingly become a tacit rule for project airdrops.

After the holders of Altlayer's AltlayerOGBadge and OhOttie!NFT series received large airdrop allocations, under the spread of FOMO within the community, the official NFTs of project teams such as EigenLayer, zkSync, Berachain, which have not yet conducted airdrops, have become important chips that people believe must be seized next.

However, whether these NFTs are collectibles or serve as proof for airdrops requires users to have strong predictive abilities and have examined the attitudes of project teams over the long term. At the same time, these "rights-based" NFTs have also become potential channels for project teams to monetize before issuing tokens, and there are quite a few cases of front-running behavior.

2. Project teams tend to value developers in airdrops: Blast divided the airdrop allocations in half for regular users and developers, Celestia allocated one-third of the total airdrop amount to GitHub developers, and Staknet openly rewarded a large number of developers with airdrop allocations. More and more star projects are prioritizing airdrop distribution to developers, making "contributing code to the project" or "pretending to be legitimate developers" a new way to benefit, leading to a large number of low-quality projects appearing on the chain in order to obtain ecosystem rewards. This phenomenon may become more and more prominent in the future, but new countermeasures are expected to emerge (probably involving AI).

3. Collaborate with professional witch-hunting organizations to screen qualified users: Only recently, Celestia and Manta have collaborated with TrsutaLabs to screen users who meet the criteria. Linea provides options such as Nomis, GitcoinPassport, and Clique for the real person verification (POH) stage, and it seems that the project's collaboration with witch-hunting organizations has become a new trend.

Professional organizations integrate multi-chain data and the depth of users' participation in airdrop projects to analyze the witch risk of addresses more comprehensively. However, they have also been criticized for being excessively strict or not intelligent enough, resulting in the inadvertent killing of genuine users. For example, there is still the problem of being unable to identify the malicious transfer of "poisoning" innocent addresses that have been included in the witch database.

Unique "Innovation and Diffusion" of Furry Users

1. Spreading from EVM Chains to Other Chains

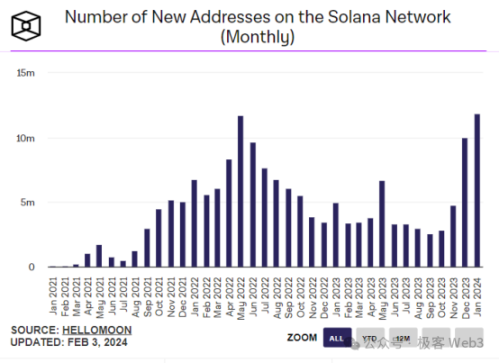

With the transparency of information and the maturity of the EVM chain ecosystem, the scarcity of airdrop shares on EVM chains, especially on overcrowded Ethereum Layer 2, has become common. Ordinary users cannot compete in terms of amount or activity, and the low input-output ratio has led the furry party to seek opportunities in other directions, focusing on Sui, Aptos, Solana, and other chains with good TVL or capital backgrounds.

The overflow effect of EVM chain users is demonstrated by the recent continuous increase in user activity and TVL data for chains such as Sui and Solana. By finding simple interactions like Jupiter in these ecosystems, similar to the UNI-style, users can obtain airdrop opportunities. This is even common in the BTC ecosystem.

(The wealth effect has made many new users active on the Solana chain again)

2. Shifting focus from high-value financing projects to small but refined ones

Projects with high-value financing often have a long airdrop distribution cycle due to their lack of cash flow. This extends the furry party's front line, as they make long-term investments that do not yield returns. In addition, a large financing amount implies project stability, which attracts many people to participate if there is a high level of certainty, thereby diluting the airdrop share.

In response to this, some furry participants are shifting their attention to small but refined projects. These projects often disclose smaller financing amounts, but they offer a higher cost-effectiveness for furrying because of the low number of participating users. Starknet, Layerzero, and ZkSync, which have been jokingly referred to as the "Three Stooges" by the long-term PUA community, have all experienced varying degrees of volatility and decline in active data.

There is another strategy for airdrops, which is to look for projects with backgrounds in major exchanges. Since the value of airdrop tokens depends on the expectations of major exchanges, many airdrop activities revolve around projects related to exchanges such as Binance, OKX, and Coinbase, such as Binance Labs Fund, Coinbase Ventures, and projects within the self-operated public chain ecosystems of major exchanges. Another type of opportunistic behavior revolves around top VCs such as Paradigm and a16z, which participate in financing but with smaller amounts and appear to be more niche projects.

In addition, some relatively obscure airdrop rules, such as continuous sign-ins for NFP and Arkham registrations, can also allow individuals to receive a satisfying proportion of airdrops. However, once obscure rules that have a wealth effect appear, they become rules that are fully recognized by the market, and it may not be feasible to try to "copy the homework" and form a sustainable path of dependence on such rules. This market, and even the world, is filled with uncertainty, and historical experiences may not necessarily apply to the vast future. All so-called "rules" and "conventions" are likely to be rewritten in the near future.

Perhaps leading projects in each field are trying to invent new airdrop rules. These rules may bring about different innovations, but fundamentally, the recipients of rewards distributed by projects will always be loyal users who are "early adopters + deeply engaged + contribute large funds".

Debate: The Game between Airdrop Farmers and Projects

Recently, Starknet caused controversy when it referred to users focused on airdrops as "digital beggars" on social media and even created a "digital beggars" channel on its official Discord, which drew criticism from the community. Similar conflicts between project teams and airdrop players have occurred with Scroll, and later, personnel associated with Scroll and Starknet personally engaged with the community, even going as far as blocking users on social media, which sparked community anger. Although the individuals involved apologized later, it did not completely dispel the community's grievances. This PR controversy had a reverse marketing effect on the community and is worthy of being analyzed as a case study.

This public opinion incident revealed the delicate relationship between airdrop farmers and project teams. The unspoken rules and tacit understanding formed between airdrop enthusiasts and project teams seem to have created misunderstandings between the two parties. Many users believe that airdrops are their "earned income". They work hard and contribute transaction fees to generate income during the bear market, creating the illusion of on-chain prosperity for the projects. They believe they should receive "compensation". However, these users have strong intentions, and project teams may not necessarily fully acknowledge their contributions.

In the early days of airdrops when there were not as many airdrop enthusiasts and most users were genuine, project teams did not exclude the participation of low net worth users due to good user retention. But as mentioned above, due to the influx of many airdrop enthusiasts, this airdrop method, which enables mutual recognition between project teams and users, is diminishing.

In addition, airdrops should not be seen as the end point of a project. Some cases have shown that successful airdrop campaigns can stimulate user activity in a project. Jupiter has an annual airdrop program, and after the first airdrop distribution, Jupiter's daily active users (DAU) surpassed Uniswap at one point; Both Arbitrum's STIP funding program and Optimism Op Grants have kept their user activity data at a high level for a long time.

(Arbitrum and Optimism remain active after airdrops)

Some projects also take alternative approaches to lock funds, by supporting ecological projects or developers. Similar to Base, which does not distribute tokens openly, they use applications like friend.tech and Bold to attract major holders to deposit funds into their protocols and cultivate user stickiness. However, even excellent applications like Uniswap face the issue of stagnant Total Value Locked (TVL) before token issuance. It can be said that airdrops are a powerful move when the ecological community lacks contribution, growth is weak, or even regressive, but it should never be the last move.

(In the long bear market, a large number of "wool party" interactions contribute income to ZkSync)

Conclusion

A common complaint among community members is that the "wool party" supports on-chain data and helps projects survive in the bear market. On the other hand, many project teams ignore the "wool party" but indirectly collaborate with third parties or launch tasks to attract a large number of users for interaction, without announcing airdrop plans in a timely manner. This inconsistency often stirs up negative emotions within the community.

Airdrops with direct incentives to attract funds leverage the liquidity of users' deposited funds and promise airdrop rewards in the future. For users, they also need to consider the opportunity cost.

Airdrop standards have transitioned from interactive to deposit-based, with user's deposited funds becoming the primary criterion in the future, which may become the norm. This reflects the changes in the dynamics and demands between users and project parties. However, this game between project parties and users may be alleviated when the bull market is approaching and the overall crypto market sentiment improves. In the bear market, the prisoner's dilemma of airdrop distribution by projects may improve gradually as market funds become more abundant. Recently, there have been complaints about "staking protocols having more ETH than users' holdings". Along with the change in the pattern of fewer projects and more users, the attitude of project parties may shift from despising "freebie hunters" to competing for their attention.

The intention of project parties is not to confront the community, but rather to handle airdrop allocations more cautiously as thousands of studios join the "looting army". Nowadays, getting rich through airdrops is not realistic in most cases. It requires strong research and investment skills or great luck to identify the future value of niche projects. For freebie hunters, the golden era of widespread airdrops and easy money is already a thing of the past. The future narrative of airdrops and where it will lead has to consider the classic principle that "individual success relies not only on personal efforts but also on historical contexts".