The Four Periodic Narrative Changes of the Ethereum Ecosystem

The flexibility of the Ethereum application layer is known to enable innovation, narrative generation, and software development. They can generate both hype and creativity, as well as some malicious activity that affects the end-user experience. But overall, most innovations foster long-term adoption and bring new capital and talent to the ecosystem.

first level title

4 Main Narratives of the Ethereum Ecosystem

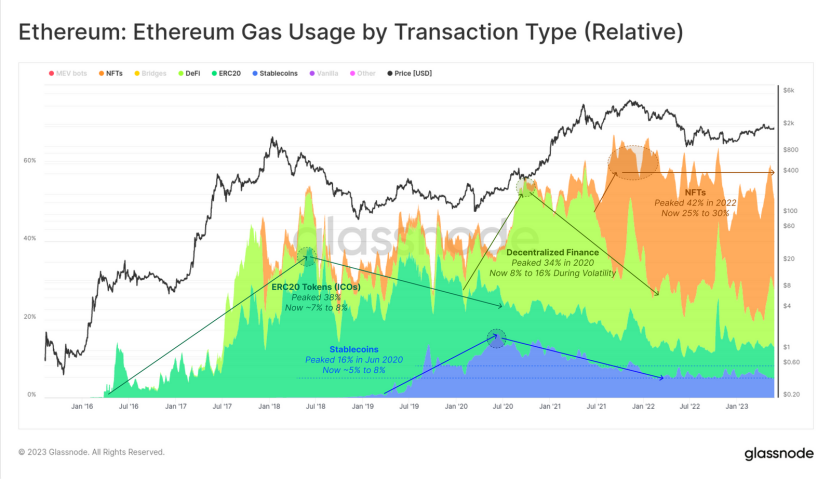

ICO:The ICO boom saw the crypto market peak in 2017 and 2018, during which time 40% of gas consumed came from ERC-20 token transfers. Although the demand for ERC-20 token transfers has been decreasing, it still contributes a certain share of gas consumption (7% -8%). This is due to the popularity of Memecoin and new token distribution methods (such as Yield Farming and airdrops) ) drive.

Stablecoins:Stablecoins:

NFT:Since the middle of 2020, user demand for stablecoins has surged, and gas consumption accounted for up to 16%, which has now fallen back to 5%-8%. However, the decrease in stablecoin gas consumption reflects more of a change in their utility than a decrease in real demand. Currently, stablecoins are used more as a hedge and store of value than as a method of payment.

DeFi:DeFi emerged in 2020, aiming to create original finance and tools on the chain without traditional intermediaries. DeFi's gas usage accounted for as high as 30% from June 2020 to 2021, and currently accounts for between 8% and 16%, with a slight recovery recently.

first level title

Gas consumption of DeFi activities

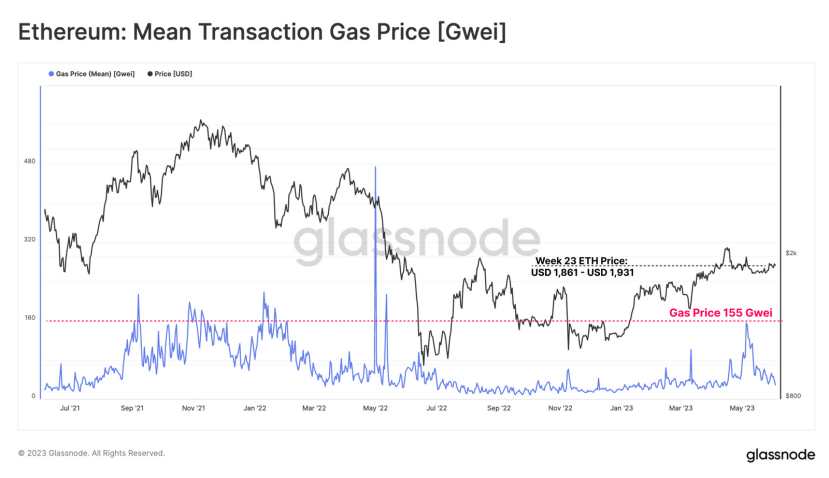

Since March of this year, ETH price has been oscillating in a relatively stable range. At this stage, the average gas fee is 76 GWE. But gas prices experienced a more pronounced rise in May, with the average gas fee reaching 155 GWEI in early May, almost reaching the level of the 2021-2022 bull market cycle.

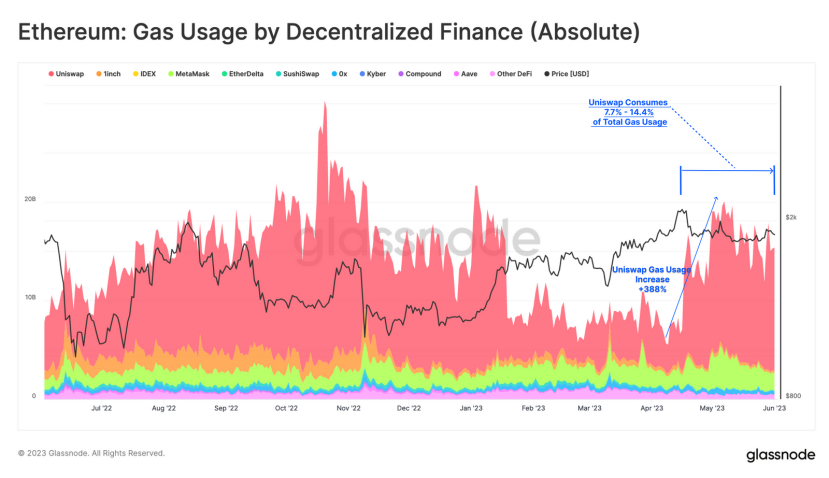

Smart contract interactions are more frequent, and the gas consumed by contract interactions is equivalent to several times that of token transfers. Gas consumption associated with DeFi protocols spiked as much as 270% in late April.

Many people's first reaction when they see this data may be: the recent hype about Memecoins such as Pepe and Hex is the main reason for the increase in gas usage. In fact, through a detailed analysis of Uniswap’s trading volume, it can be found that the highest trading volume in the past 30 days is mainly related to assets with higher market capitalization, such as ETH, stablecoins, WBTC and Coinbase’s pledged derivative cbETH.

first level title

Arbitrage bots are taking over DEX?

Comparing the addresses marked as the top 10 traders revealed only one trader whose address was not associated with the MEV bot. In the past month, Jaredfromsubway.eth, a well-known MEV robot, has traded as much as $3 billion.

Although the number of bots among global traders needs further research to be determined, the top 10 data by trading volume also shows that there is indeed a fairly high proportion of automated arbitrage traders on Uniswap.

One way to rationalize automated arbitrage traders is to consider the exponential range of arbitrage opportunities available to Ethereum DEXs:

1) As the price of each token (+ slippage) changes, the resulting gas fee will justify the arbitrage trade.

2) Every DEX liquidity pool that provides token transactions provides a platform for arbitrage transactions.

3) The number of potential arbitrage trading opportunities is directly related to the number of DEX liquidity pools and the number of tokens available for trading.

If one considers that many bots are involved in arbitrage trading, or “sandwich attacks,” UNISWAP’s normal trading volume could account for around two-thirds of all DEX activity.

With the sideways fluctuation of the encryption market, the overall trading volume of the cryptocurrency market has remained sluggish recently, while the use of DeFi has become more and more automated, and there are a large number of arbitrage, MEV, and algorithmic transactions in DEX trading behavior.

To a certain extent, this highlights the trend of using Staked ETH as the main asset in the Ethereum ecosystem, but also establishes a local threshold, that is, tokens must compete to attract capital inflows. According to the Ebunker index, the current APR of ETH Staking is about 6%, of which MEV contributes more than 1/6.

first level title

New products in the Ethereum ecosystem

Over the past two years, two major new products and services have emerged in the Ethereum ecosystem: GameFi and Staking. Both have aroused varying degrees of interest from investors. GameFi once outperformed DeFi in mid-2022, but the speed of decline is also very fast. Since the beginning of 2023, staking has been on an upward trend, with the total market capitalization rising from $505 million in January 2023 to $3.2 billion in April 2023.

Thanks to the burning mechanism of EIP-1559, they will burn a lot of ETH for Ethereum no matter how the narrative switches on Ethereum. The common promotion of these narratives actually completes the big narrative of the Ethereum chain itself. And when Ethereum becomes a more mainstream platform due to narrative, these small narratives will eventually benefit. This is the "super positive cycle" of Ethereum.

Ebunker official website: https://www.ebunker.io