Adam Cochran: Crypto Wealth of 2023

This article comes from TwitterThis article comes from

, Original author: Adam Cochran, compiled by Odaily translator Katie Koo.

The annual Crypto "sweeping goods" list is here again. You don’t have time to research individual assets every time the market drops sharply, and you risk missing out on a great buying opportunity. As a long-term investor, I expect that there may be a sharp drop, so I will have to continue to hold it. I expect some assets to go to zero, so I will adjust the purchase list in time as the situation changes.

Every Crypto shopping list starts with establishing a theme and buying plan. The theme is the catalysts that will drive the market over the next 3-5 years, and the purchase plan refers to the size of each asset to be purchased, and under what conditions. Every year I share my shopping list and discuss the catalysts that I think will drive the growth of the assets on the list. This buying list is based on personal circumstances, risk tolerance and timelines.

Let me show you a table first, and feel the misery of Crypto in 2022:

Notice:

Notice:

2. I would definitely rebalance some positions if people followed suit directly, but I think these are "long term winners".

Summarize:

Summarize:

1. Real external income remains the most important factor.

2. However, assets are so depressed that some "growth" style tokens are facing difficulties.

3. Focus on real revenue "catalysts", novel infrastructure and user experience.

Real revenue refers to projects that are used by users outside the project and generate revenue, especially if not supported by ongoing emission incentives, which ultimately incur costs to users. Another important highlight is the user experience.

Not just design, but any tool that makes the process of using blockchain technology easy for users. Just like web browsers or search engines made the internet easy to use, we need tools that make encryption easy to use. These can be cross-chain bridges, multi-chain applications, automated tools, smart wallets, etc. Anything that makes complex systems of decentralized liquidity easier to use or build.

1. Ethereum

(1) Ethereum doesn’t need any reason to be at the top of the list. It has the most users, is deflationary when used, and has a dozen scaling solutions coming soon.

(2) I think long-term investing in ETH is like buying internet infrastructure after the dot-com bubble burst. Everything in the industry is in pain and may be overhyped long term, but that doesn't mean it's useless.

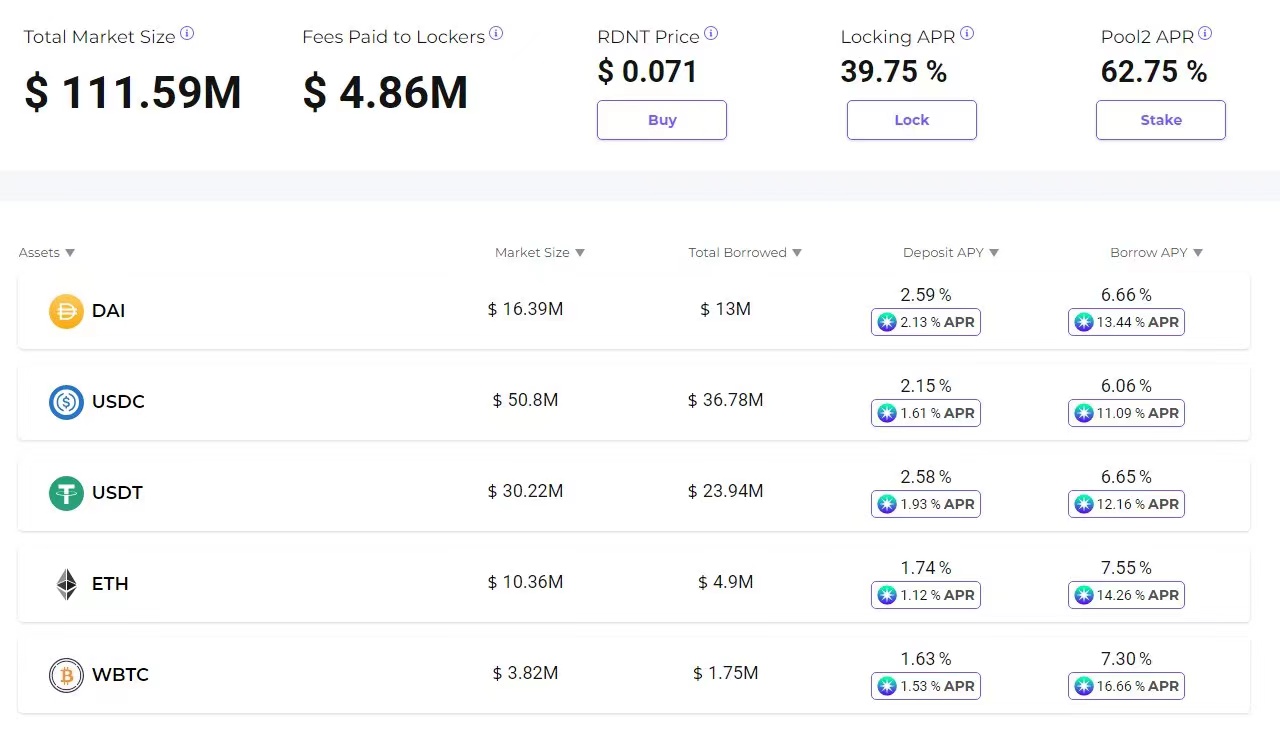

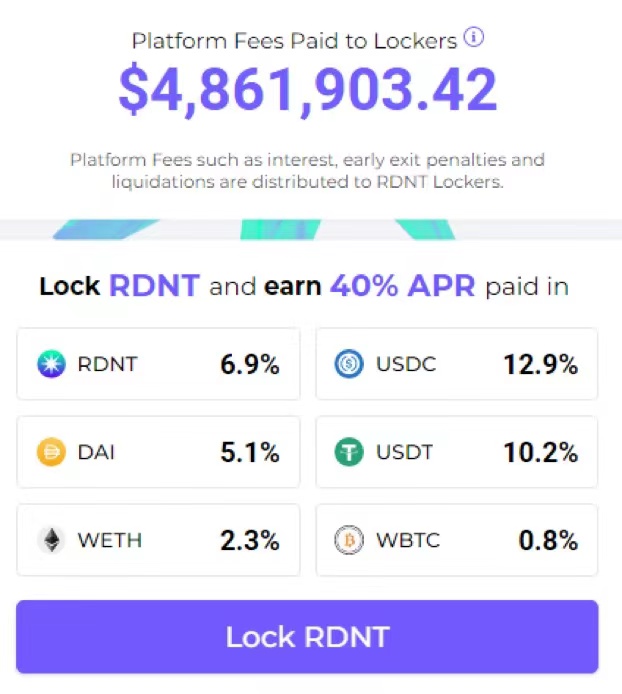

2. Radiant Capital(RDNT)

(3) I personally believe that one day the Ethereum blockchain will become a ubiquitous data layer. Optimistic about Ethereum will be a rare opportunity for participants to realize the freedom of wealth.

(1) Radiant Capital is one of the new projects I'm most excited about this cycle. It adopts the existing money market model and builds a cross-chain model locally so that it is fully operated by the community.

(2) Radiant Capital first launched on Arbitrum, which is built on LayerZero, which will allow it to have a native cross-chain marketplace. Users will be able to deposit collateral on one network and borrow and lend seamlessly on another.

(3) Stake your native tokens on Arbitrum and borrow on Polygon to enter the next farm. Use your OP tokens as collateral to borrow USDC for mainnet farming. Users will be able to borrow, settle and pay fees across marketplaces.

(4) The team was built entirely from scratch, with no VC funding or seed rounds, and unlike Aave or Compound, which charge developers fees, Radiant’s protocol rewards all fees to stakers. This means that stakers get a good average annual return (currently 39.75%), but it's not all from diluting tokens, but from real use cases, and is paid in real valuable assets, most of which are in the form of USDC pay.

(5) In terms of valuation, the current valuation of RDNT is only $2 million, and the FDV (fully diluted valuation) is $70 million, but over time, most of the FDV is paid to stakers, The degree of dilution is not actually equivalent. Considering that Compound has a market cap of $365 million ($529 million FDV) and Aave is $1.2 billion ($1.3 billion FDV), there is plenty of room for growth here. But more importantly, even though Aave and Compound are multi-chain, their liquidity is "split".

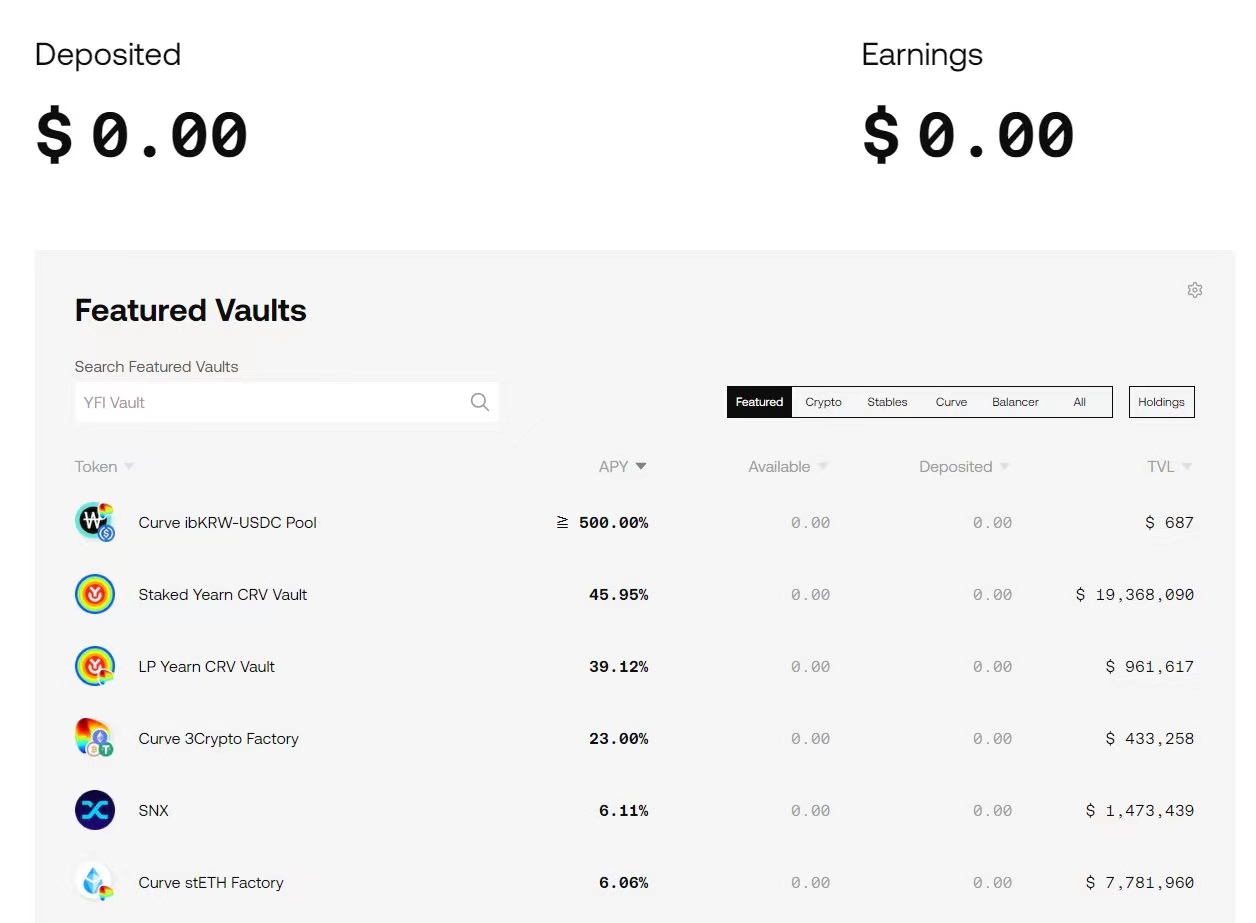

3. Yearn Finance(YFI)

(6) Although Aave hopes to launch a cross-chain function called Portal in its V3, it has not yet launched and will be limited by the Aave structure. However, Radiant has cross-chain design in mind from the beginning. I think the $5B+ opportunity is easy for whichever team can build a strong market share in the cross-chain lending space, and Radiant is off to a great start. This market has been difficult to enter, and if they can pull it off, the rewards could be big.

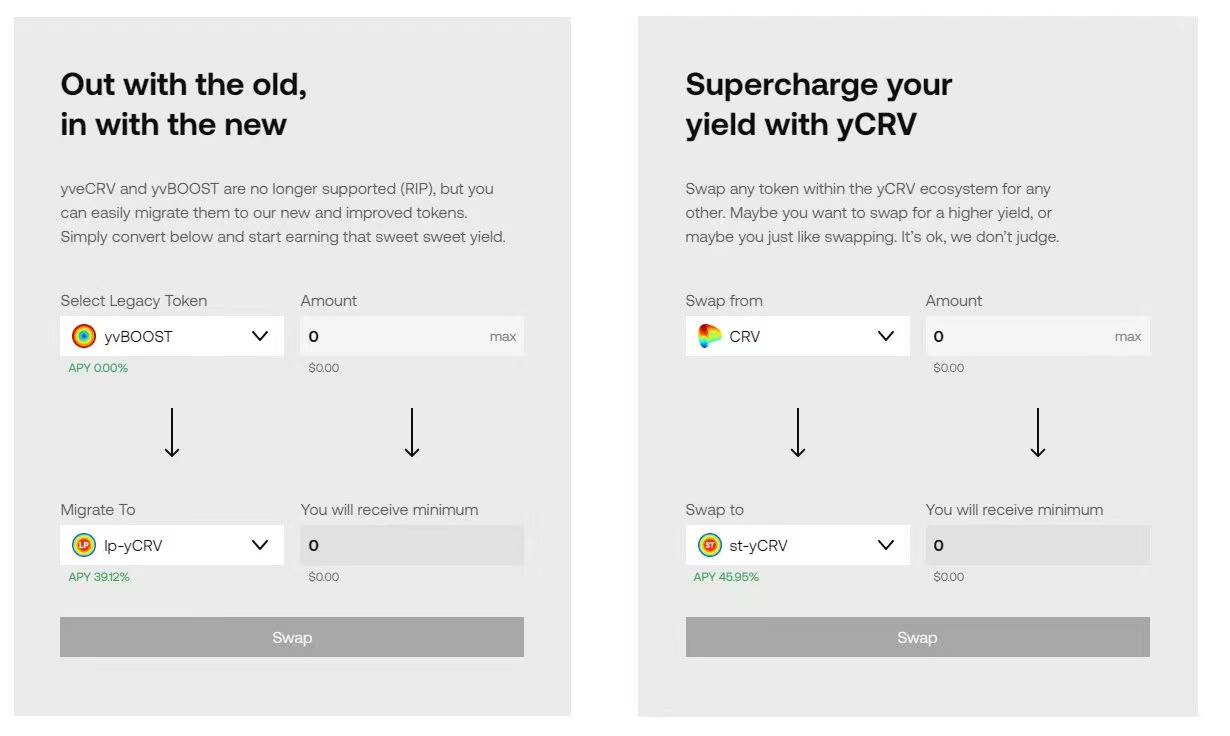

(1) Yearn is the undisputed leader in yield automation and vaulting, and more importantly, has undergone major changes in its competing offerings. Yearn recently completely refactored their product, including a new website: support new chains - lower fees - reintegrate CRV - rebrand YFI token.

(2) Yearn holds a large amount of CRV, in fact, has 44 million locked CRV, making it one of the largest Curve holders in the ecosystem. Having a say in the vote will help them earn higher returns in the strategic coffers.

Under the previous model, the way to get and reward CRV locked was inefficient, so they converted the old growth model to the new model yCRV, which currently pays up to 45% annual return when staking.

(3) But, more interestingly, locked veYFI will be able to vote on which treasuries get the voting rights assigned to them, and which treasuries get directly rewarded with YFI.

(4) You can think of it as Convex's Votium protocol, but it is directly integrated into the system, and it gains benefits from three places, not a single one:

1. Yearn treasury

2. YFI emissions from Yearn repurchase

3. CRV rewards

(5) The "bribes" are just getting started and people don't seem to realize it at all, as participation has been low, meaning it takes very few votes to generate new bribes.

(6) Yearn also started creating automated tools that allow any project to deploy an automated yield library for its pool and bribe the pool. With the increased number of templates, Yearn will be able to automate large pools of funds for any project.

4. Synthetix(SNX)

(7) Yearn treasuries have always been a key component of DeFi infrastructure, but now they will be scalable, bribeable, and profitable for project integration. Deploying the Yearn Gauge and acquiring YFI will become standard practice, just like the Curve War in the last cycle.

(1) Synthetix is a DeFi OG, Synthetix allows the creation of synthetic liquidity backed by assets and liabilities. Synthetix started as a simple lending protocol that allowed SNX to be staked and sUSD to be borrowed.

(2) has now evolved to include Atomic Swap, a perpetual contract engine, and soon there will be a permissionless marketplace for building such agreements for unlocking your treasury rewards.

(3) With integrations with Curve, 1inch and other major players, Synthetix V2 "atomic swaps" generated huge volumes, you can see how their V2 adjustments caused volumes to spike even in a bear market of.

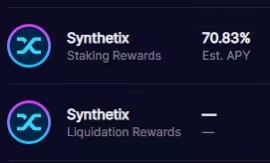

(4) In the last bull market, the V1 trading volume of atomic swaps exceeded $100 million per day. Synthetix is currently holding such a record every month in the bear market, but only between "atomic swaps" and perpetual contracts, which still means that the APY of Synthetix stakers will reach 70%+ under current market conditions.

(5) The current version of Synthetix is also only on the mainnet and Optimism, but V3 is targeted to launch sometime in the end of Q1/early Q2, it will support multi-chains, allowing cooperation like 1 inch Partners instantly use it on any chain to provide transactional liquidity.

(6) Currently, all markets come from a single collateral and a single source, but V3's new model will allow anyone to build their own protocol on top of Synthetix. They will decide on collateral, assets, models and returns. They can choose to issue Synthetix's own sUSD and use a treasury managed by Synthetix, or they can set up their own system against Synthetix's debt pool and decide which collateral to accept. Users can then decide which pool to stake, allowing any protocol to build a debt collateralization system.

(7) Money markets like Aave, perpetual contracts like Kwenta or GMX, AMMs like Uniswap, and Synthetix will provide liquidity services.

(8) The goal of Synthetix is to abstract these deployment complexities so that it can have templated versions, making launching your own DeFi protocol as easy as running a WordPress site or deploying a Shopify store.

5. Conic Finance(CNC)

(9) The goal of SNX is to become the liquidity layer supporting all DeFi. First, it will be limited to technical users, but I have high hopes for what this community can achieve by being one of the first Dapp-to-Dapp protocols.

(1) Conic may end up being one of the most important ecosystem projects you've never heard of. Conic is a key part of the Curve ecosystem, bringing the omnipool into balance.

(2) Conic has created an "omnipool" that allows users to deposit assets into Curve and spread them across different pools to optimize APY per dollar.

(3) In order for Curve to launch its crvUSD and take on multiple collaterals, its pool needs to be able to easily absorb liquidations. You can’t do that if a pool is illiquid, and that presents a huge risk of manipulation.

(4) And that's where the Conic comes in. Seek maximum yield by creating a liquidity fund that moves from one pool to another. This means that if some kind of collateral on crvUSD is liquidated, the omnipool can be redirected to this pool to absorb rewards.

(5) This will make Conic the layer that optimizes rewards and puts assets into the crvUSD system as collateral. Unlike its competitors in Curve War, Conic is also the only responsive system that dynamically adjusts focus to drive costs.

(6) More importantly, Conic's website is designed like a Mac UI desktop, knowing the complex infrastructure they are building, and their deep understanding of why crvUSD needs omnipools, I think Conic's team must have the Curve team member participation.

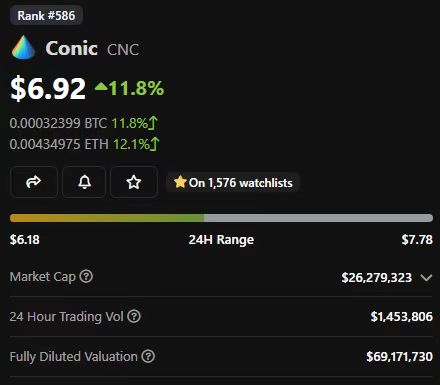

(7) Conic is currently preparing for release, so the risk is high. Considering that Convex currently earns about $3.8 billion in TVL, that would bring in $9.7 million per month even in this depressed market. It is valued at $370 million, roughly three times its annual revenue.

(8) If Conic can capture TVL, even in a bear market, the value of CRV does not grow, and there is a chance of 10 times growth.

(9) However, Conic can steal market share from any project that has a large CRV reserve or involves bribing votes for Curve or doing automated fee balancing.

6. Convex Finance(CVX)

(10) Currently, even in a bear market, the Votium protocol has about $1 million in vote bribes per week, which alone could lead to an immediate $156 million valuation for Conic. The risks are high, but so are the opportunities, which help reinforce crvUSD's potential.

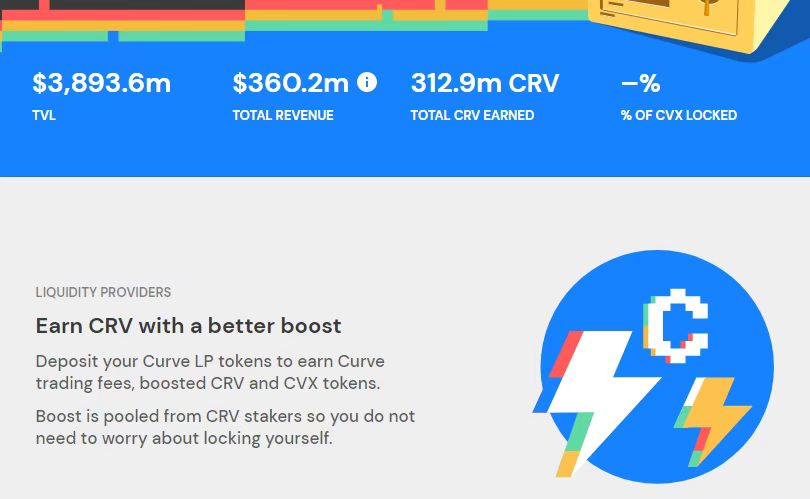

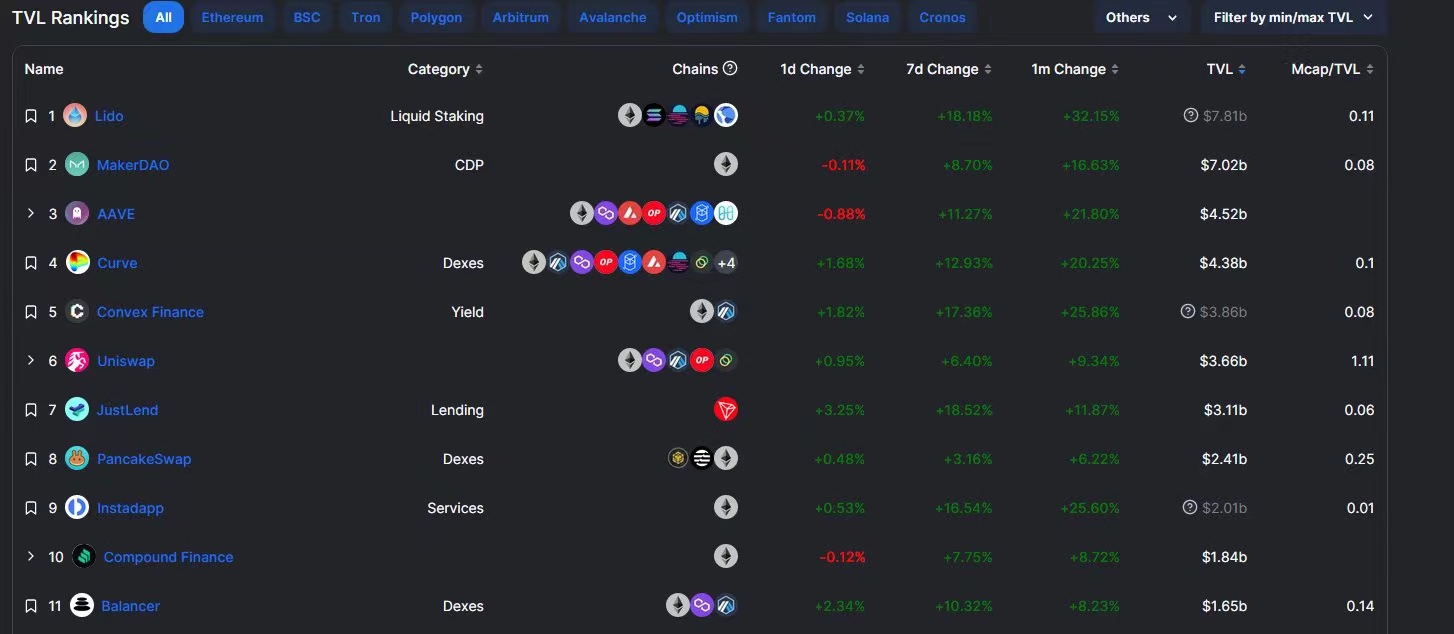

(1) Convex is the overlord in the pool. From what I've seen about Conic, I think Curve is one of the most important protocols in the space and its value will only continue to grow. That means Convex will stand with it.

(2) While I think Yearn and Conic will continue to threaten Convex's dominance, there is one thing that cannot be ignored. That is, Convex has 288.5 million locked CRV, which no one can shake.

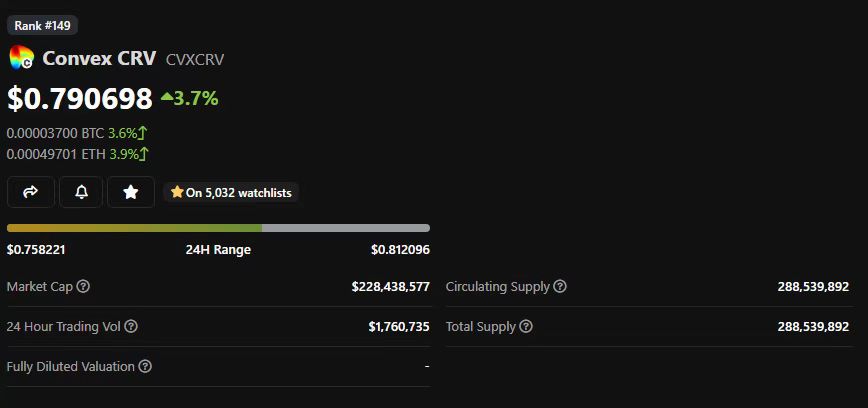

(3) Even if Convex stops issuing new rewards, or is robbed of market share by new entrants, this voting right will never be taken away and will continue to be rewarded. cvxCRV is also currently trading at over 20% less than CRV.

(4) As crvUSD grows, people want to cash out their locked cvxCRV for CRV, which creates this gap.

(5) My personal prediction is that the CVX team will push their crvUSD rewards to cvxUSD to help close this gap. This means that at the current price, by buying cvxCRV (instead of CRV), you will get 20% more rewards.

7. Frax Finance(FXS)

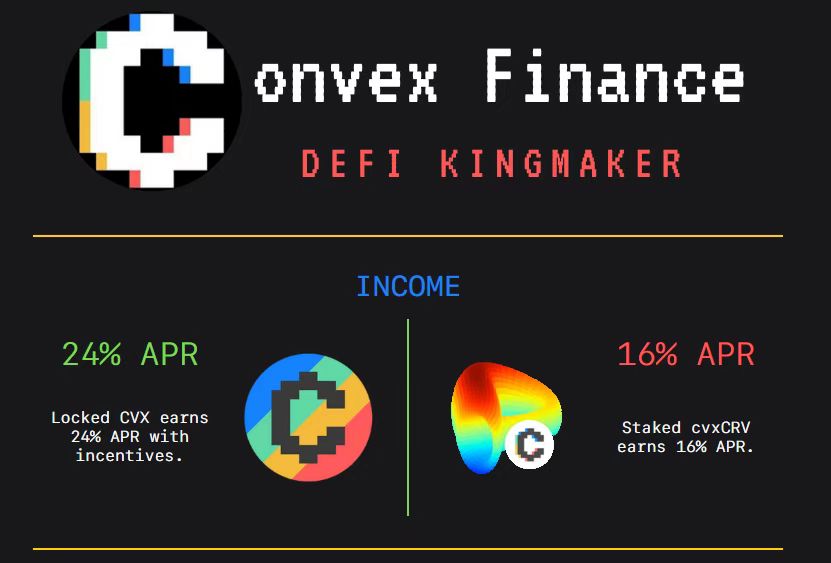

(6) Right now, buying CVX and locking vlCVX gets more votes per dollar than raw CRV and earns 24% APY from bribes.

(1) Frax is the king of sniping retail investors. Frax is becoming increasingly difficult to fit into any one category, it is becoming a DeFi monster trying to attack all verticals.

(2) Frax was originally an algorithmic stable currency, and it is currently one of the few coins that can survive multiple ups and downs. Being a battle-tested algorithm stable is impressive in itself, but Frax doesn't stop there. Instead, Frax decided to aggressively try all new territories.

(3) From its transaction AMM to the lending market, Frax has slowly expanded its field to other DeFi markets.

Most projects that have tried this approach, like Sushiswap, have backfired and spread themselves too thin. But Frax has done a great job of retying everything back to the core market.

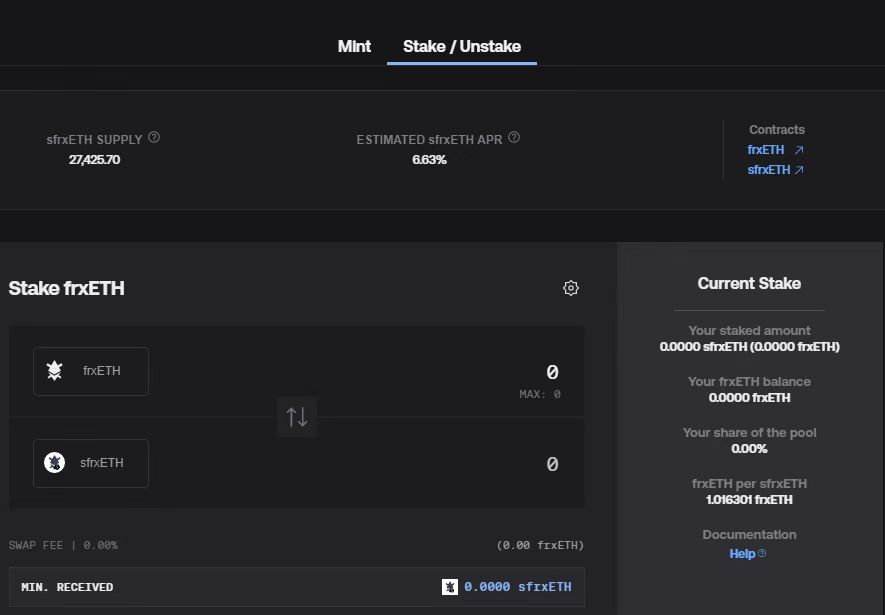

(4) Frax is also the majority shareholder of Curve's voting rights, which you'll notice is a trend this year. They intend to use this Curve voting power to increase the APY yield of their liquid collateralized ETH product - frxETH.

(5) Like competing with cbETH and stETH, they can only provide base ETH yield minus fees. By redirecting their rewards (even short-term rewards) to frxETH, Frax should be able to capture a significant portion of the market share in liquid staking over time.

(6) Unlike some of the other projects profiled here, Frax’s valuation is already quite high, and due to the narrative surrounding the liquidity staking protocol, the valuation has increased significantly in the past few weeks.

8. Curve Finance(CRV)

(7) I bought on the last dip and may wait for a "cooling off period" before continuing to buy, but I think there is still a market with huge potential for Frax to offer the best of both worlds by creating an interconnect protocol Similar products.

(1) The fluctuation of DeFi is driven by Curve. CRV voting can change the trend of any project in a single instance, breathing life into a project or defeating it outright. Curve started as perhaps the most efficient trading protocol of its kind for trading pairs, but it quickly grew into an industry powerhouse, providing incentivized liquidity to fledgling projects.

(2) This model creates "Curve Wars", where other protocols compete to collect as much CRV as possible to incentivize their own pools. Curve then launched a V2 pool to trade regular pairs with AMMs like Uniswap. Even though the V2 pools have grown a lot, my hunch is that these pools can still grow further to provide higher traffic.

(3) However, I think the current catalyst for Curve is twofold. First, Curve and 1 inch collaborated to integrate Synthetix’s atomic swap protocol, allowing them to create synthetic assets and swap them in and out of the Curve pool for better virtual liquidity that doesn’t currently exist. This opens up opportunities for "new market" routes where conventional AMMs cannot compete.

(4) Curve V2 pools will benefit as Synthetix scales up assets in this product, allowing users to trade large amounts of liquidity across complex routes.

(5) Second, Curve is finally on track to release their long-awaited stablecoin "crvUSD" sometime this month. Instead of an agreement based on regular liquidation, the system uses an automated liquidation method called LLAMA. This self-clearing AMM runs through Curve's pool, meaning liquidation fees will automatically accrue to individual LPs on Curve, while borrowing fees will flow to veCRV holders (which in turn benefits Convex, Conic, Yearn, and Frax ).

(6) So why is the Curve stablecoin more interesting than other stablecoins? This is partly due to Curve driving the largest demand for stablecoins in the space. Every stablecoin pair on Curve is paired with Curve's 3 Pool.

(7) Even in a down market, 3 Pool has driven nearly $600 million in stablecoin demand. However, there is no reason that 3 Pool must own these assets, or that the underlying trading pair must be the current 3 Pool.

(8) Curve DAO voters can vote to convert 3 Pool from holding DAI to holding crvUSD, or a better way to vote is to vote to decide that the basic trading pair for measuring qualified stablecoins is crvUSD instead of 3 Pool, which will immediately Generate crvUSD demand of $600 million.

(9) While it looks like Curve will only start with ETH as collateral, the LLAMA system is a way to secure diverse collateral. As long as Curve has a V2 asset pool backed by the Conic omnipool, they can liquidate most assets with confidence.

9. Balancer(BAL)

(10) More importantly, the value here is reflexive - as demand for crvUSD increases, more rewards flow to veCRV holders, which makes CRV more valuable, which means more projects Wants to control CRV voting, which increases demand for crvUSD, and so on.

(1) Balancer has been a leader in novel mechanisms, and it has two key features that I think will grow in value. Balancers are often overlooked. Balancer's unique model makes it the foundation of DeFi, and I think the development we're seeing is that the 80/20 pool will be the core value underpinning the next wave of DeFi.

(2) Many teams realize that their locked-token models (like xSushi or veCRV) are problematic. Because while locked tokens create scarcity and upward liquidity, they also create illiquidity for new big buyers, and weak bottoms in bear markets.

(3) At the same time, you can't ask users to stake regular AMM trading pairs, because impermanent losses will destroy returns, or positions will become so concentrated that your assets will never really go up or down, and it will become a Useless assets.

(4) So what to do? This requires a balanced 80/20 pool, which is what Balancer uses. By letting users hold their own tokens and 20% of ETH, they ensure strong liquidity, but lower impermanence losses for users.

(5) Of the teams I've talked to recently, about a dozen are redesigning the token economy, and 8 of them are talking about using an 80/20 pool - something only Balancer really offers right now.

(6) I mentioned in last year's 2022 wealth code article that I think Balancer is a B2B protocol that can provide unique liquidity products to other partners, and they are really better at it.

Balancer already has nearly 20 new partners and is growing in market share. This is the first time they have come close to TVL's top 10 in DeFi. Even during the crash, they controlled their TVL better than most projects, as Balancer added new partners, not just new users.

(7) But as I said last year, I think Balancer is the project that brings you unexpected wealth when you use it without your knowledge, because it is a core infrastructure.

10. Cosmos(ATOM)

(8) Balancer is a long-term game, it will either become the core pillar of DeFi, or fail. But right now, they're doing a great job slowly weeding out new partners and unique integrations, so I'm still a Balancer buyer this year.

(1) Cosmos is a network of interconnected blockchains that make it easy to design custom interoperability. When it comes to other L1s, I'm skeptical. It takes a high standard of innovation and bringing a unique product to pass mine. Cosmos achieves this with a simple, modular SDK that allows anyone to build small custom blockchains using interconnected standards around communication and tooling.

(2) This means you can create a niche blockchain that is designed to be a dedicated AMM like Osmosis, or a cross-chain bridge like Gravity Well, or a custodian like Akash, all of these blocks Chains have standard ways to communicate and interact locally.

(3) I personally believe that the race for a monolithic blockchain as the core settlement layer is over. Ethereum has won this race.

The next games are:

1) Who wins on L2;

2) Who wins in the niche application chain.

(4) Many competitors in the application chain field (such as Avax, Polygon, and BSC) are building application chains in a standard way. In fact, they are called "micro-chains" rather than application chains. Polkadot's Parachains were in the early days Significant challenges were encountered, and it hurt them.

(5) Cosmos, on the other hand, focuses on building simple tools and standard ways of connecting, but beyond that, tries to keep components modular rather than restricting the creativity of builders.

(6) Outside of the Ethereum ecosystem, we don't see a lot of innovation, we often only see incremental improvements. But Cosmos is one of the few projects where we see exciting experimentation and innovative implementation.

11. Keep3r(KP3R)

(7) So I think Cosmos is very likely to be one of the non-Ethereum winner projects that finally stand out, which is also an ecosystem full of opportunities.

(1) Keep3r with the aura of the AC project is an important automation tool that supports most of DeFi. KP3R has had a rough year. That's part of the reason why it's a bit lower on my list this year, but I still believe it's in the hands of talented builders and will continue to be the core infrastructure of The DAO. The main reason remains that they are the only ones that operate in large-scale automated protocols.

(2) My prediction is that in this cycle we will see a lot of old DeFi teams disappear and their applications will grind to a halt because no one is running regular functions anymore.

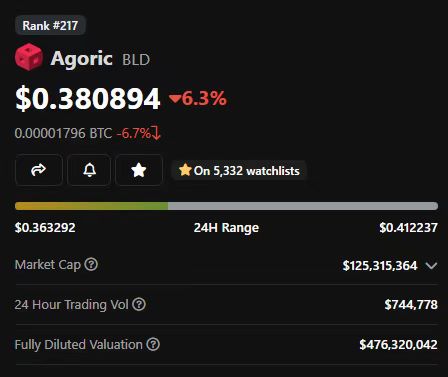

12. Agoric(BLD)

(3) Keep3r will play a key role as we continue to build more advanced cross-chain products and improve decentralization. Others like Chainlink and OZ Defender have their own automation tools. But so far, no tool has the adoption and broad decentralized participation of the Keeper network, so I still think Keep3r will be a long-term winner.

(1) Agoric is a Cosmos-based chain that implements a unique security and accessibility design pattern. Unlike most protocols in the space, which rely on smart contracts to hold your assets, Agoric was built from the ground up to allow users to interact with DeFi while keeping assets in their own wallets.

13. ZCash(ZEC)

(2) Agoric currently has a market cap of $125 million (FDV of $476 million). Agoric has a lot of room to run and could be a unique and competitive L1 product.

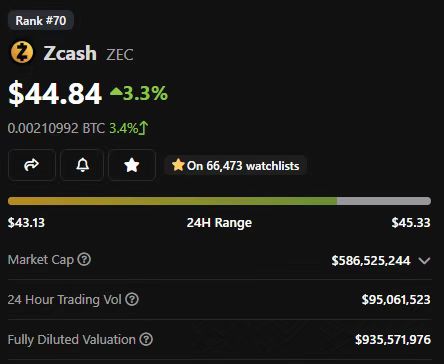

(1) ZCash has received a lot of criticism in the past due to people confusing transparent and shielded addresses, arguing that they are privacy optional. ZCash also took a hit because:

A) Acquired by Digital Currency Group;

B) There are high continuous mining rewards;

C) is an independent currency, not a platform. And, everything is about to change.

(2) ZCash is moving to PoS, like Ethereum, and while the timeline is still changing, my guess is that it will happen sometime late this year/early next year and dramatically change ZCash supply and demand.

(3) The ZCash community is also deeply exploring the issue of other tokens on ZCash and using ZEC as gas. Once users are able to migrate tokens to Zcash, new DeFi opportunities are quickly unlocked.

(4) While the Ethereum community is racing to perfect L2 zero-knowledge proofs, this is what the Zcash community has been doing since day one. Their current transaction speed can run on a mobile phone in seconds. In contrast, zkEVM like Polygon currently requires a proof program with 1 TB of RAM and 128 CPU cores. This is a completely different game.

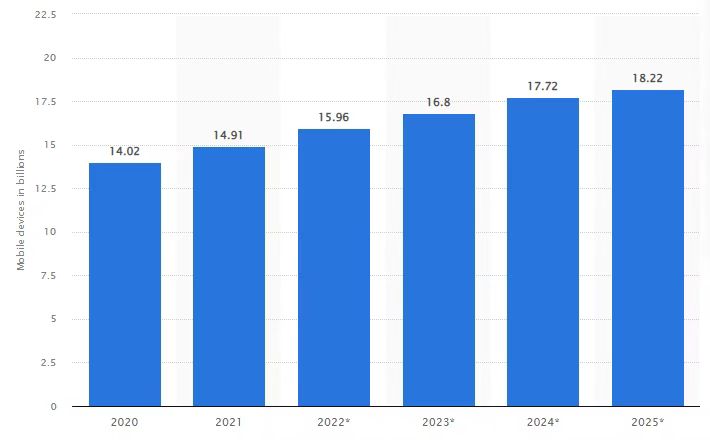

(5) It is estimated that by 2025, the number of mobile devices (phones, ipads, smart watches, etc.) will exceed 2.5:1. Someone is going to be the mobile encryption winner. I think ZEC's fast payment has a chance to be done offline by proving and supporting DeFi.

(6) Imagine that no matter where you are in the world, even with limited connectivity, you can transfer money and transact in seconds with a simple low-end device, all done privately. This is a dream many cryptocurrencies have been chasing, and ZCash is well on its way to making it happen. Market cap is just $586 million ($935 million FDV).

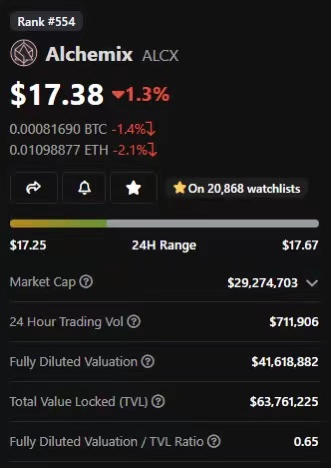

14. Alchemix Finance(ALCX)

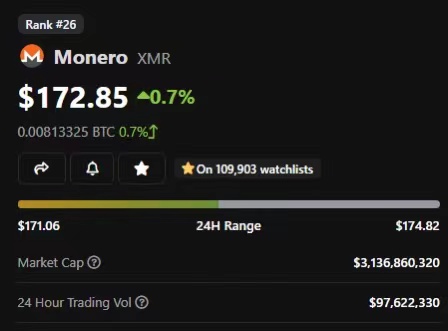

(7) Compared to the largest privacy coin, Monero, which has a market cap of $3.1 billion, it has the potential to gain 6x market share even if the market does not rise. Monero is not a platform either. Therefore, considering the L1 value, ZCash has a higher potential.

(1) Alchemix broke the mold by designing the first self-repaying loan. But then the market plummeted, yields plummeted, the loans would never be repaid, and they started to struggle. However, Alchemix has done a good job of redesigning the V2, gaining decent traction even in the bear market.

(2) Their V2 now allows self-repaying, non-liquidating loans with up to 50% collateral. That is, if I have $100,000 in ETH, I can borrow $50,000 in ETH without worrying about liquidation.

(3) In a large market environment, your entire position can easily be liquidated. But on Alchemix, if the market goes down, you won't get liquidated, it just takes longer to get your money back. This means that Alchemix allows me to take on up to 50% of the loan's value with minimal risk. And, as the value of the collateral goes up, the annual return on the treasury strategy goes up again, and my loan repayments will be faster.

(4) Alchemix has a market cap of only $30M ($40M FDV), and even in a bear market, its TVL is more than 3x its market cap. My hunch is that when regular users use self-paying loans in a bull market, smart buyers use it to buy discounted assets in a bear market.

(5) I think that as the APY treasury rate continues to rise, Alchemix expands to other chains, and integrates continuous new strategies, this team has strong long-term potential. Especially if they expand the number of assets they cover.

They will be deployed on each chain in anticipation of the future, providing an easy way to leverage native assets on that chain as collateral. If they can do it, I can see the potential for 20x+ long term.

15. Canto(CANTO)

(6) It is undeniable that Alchemix is uniquely positioned to deliver a new value proposition and scale it rapidly to capture capital locked on multiple chains.

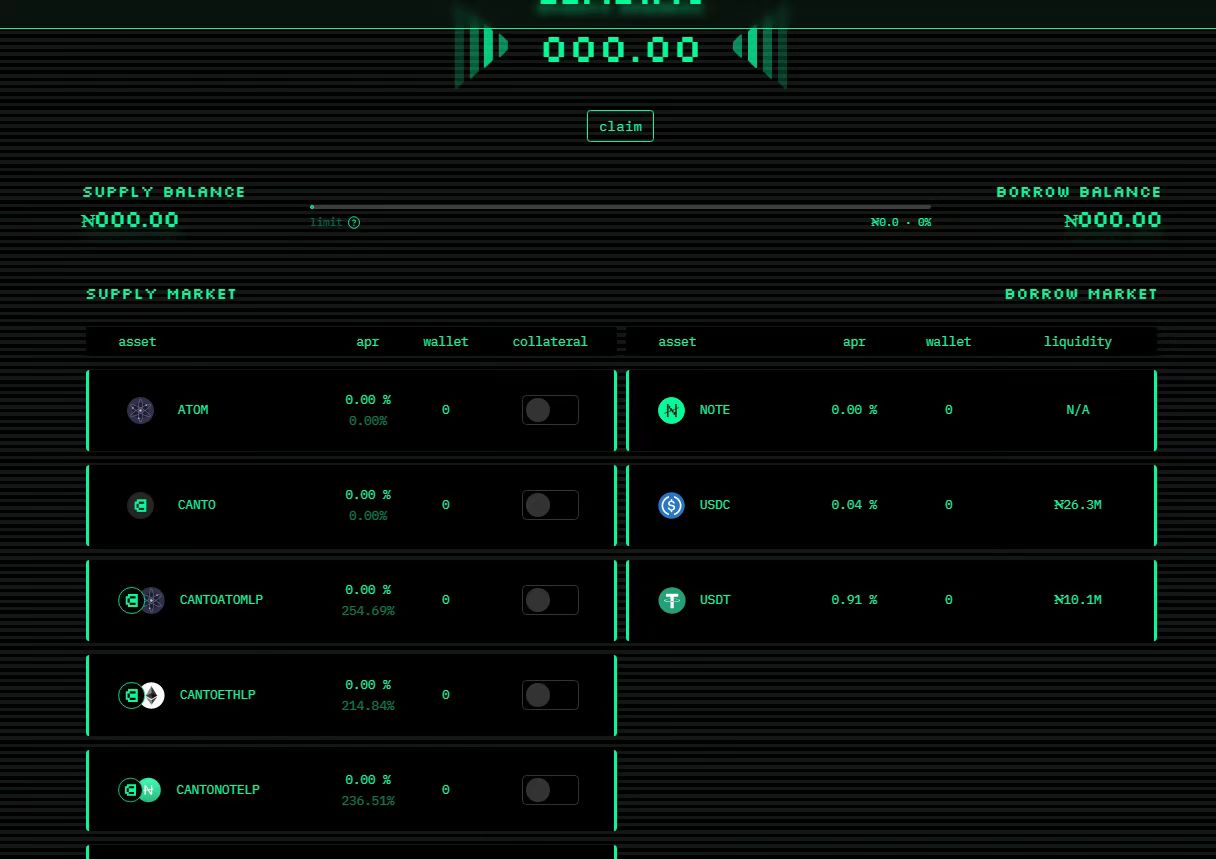

(1) Canto is an EVM chain based on Cosmos. Canto aims to replace fee-charging infrastructure with a design that helps reward decentralized public goods. Such as having its own built-in native lending protocol and AMM.

(2) There are no fees for these built-in systems other than the basic incentives for LPs. It also has its own native stablecoin (NOTE) built into the lending market and managed with interest rate controls.

(3) But I think the really unique design principle of Canto's success is its model around fee rewards. In a future release, when you deploy a smart contract, the contract will have a unique NFT attached to it.

(4) This NFT will receive a portion of all CANTO used for gas rewards associated with your contract. This means the protocol will make money based on its usage rather than a fixed fee model. This encourages developers to design protocols and systems that serve the public good, not just those that can extract the most fees.

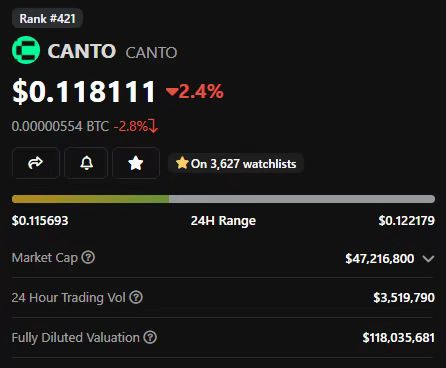

(5) CANTO has more TVL than many other larger chains, far ahead of Near, Cardano, Gnosis, and Aptos, all of which have multi-billion dollar market caps. Canto has a market cap of $47 million ($118 million FDV).

(6) Constructing a new L1 is difficult. Maintaining user interest in various new protocols is difficult (especially when these protocols compete with free built-in protocols) and Canto will need to rely heavily on its gas rewards program to maintain this momentum. If Canto can carve out some novel use cases that are hard to monetize elsewhere, it could be a real win. Consider royalty-free NFT projects, or royalty-free AMMs.

(7) My prediction is that in the next few months we'll see some innovative experimentation with Canto, and if they can start capturing some of the market, there's a lot of potential for growth. On top of that, the current staking ROI is 21%, which acts as a great buffer against downside volatility.

16. API3 DAO(API3)

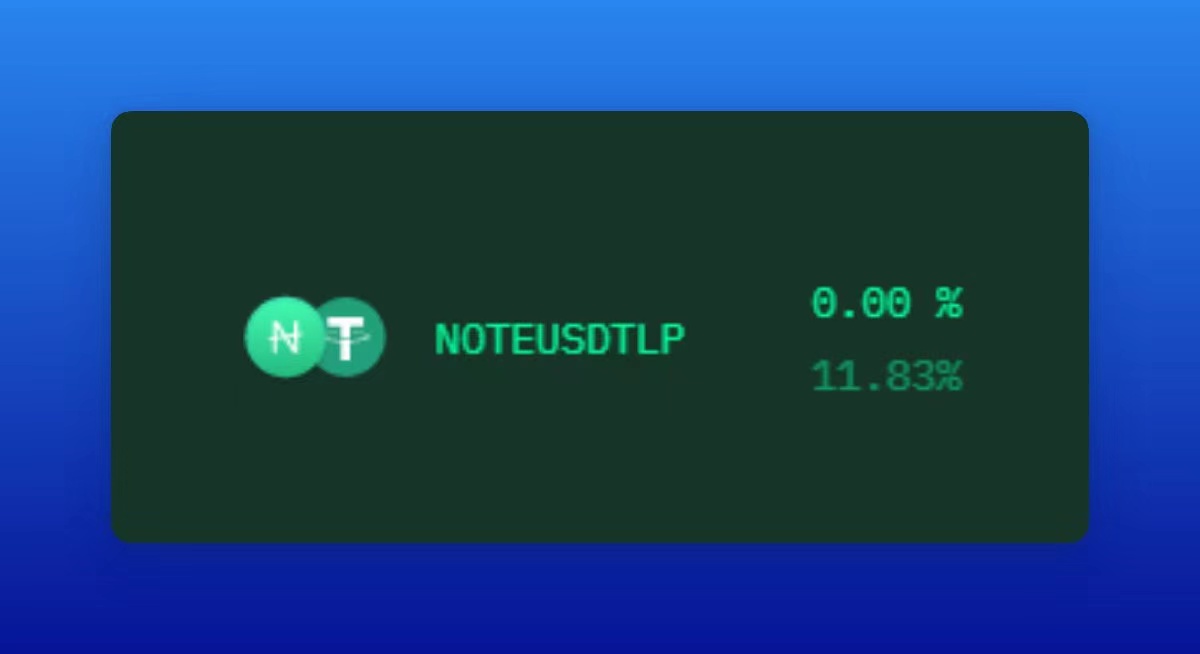

(8) And loan on the stablecoin pair of NOTE/USDT or NOTE/USDC, the APY of the stablecoin is 11% -12%. This is one of the best scaled stablecoin yields I've found on a reliable network.

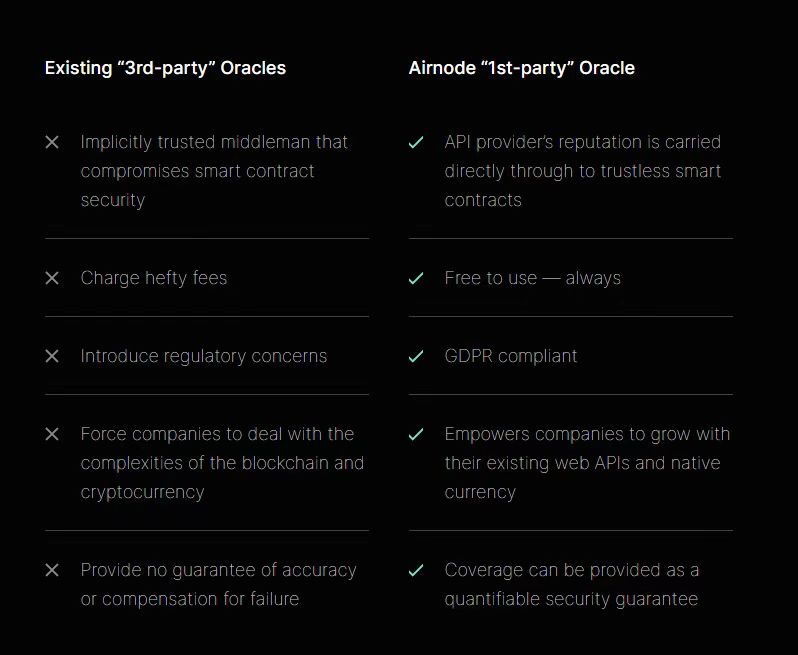

(1) Oracle in encryption has several core issues:

1) Free feeds are standard, but don't last forever;

2) Feed payment is unstable.

3) Can't easily use multiple API sources.

(2) API3 aims to solve these challenges in a novel way. Its "Airnode" design allows you to connect any API to Web3 in a trustless way, allowing you to run it in a cost-free third-party way. I would like to see API3 built in a more open way.

17. AngleProtocol(ANGLE)

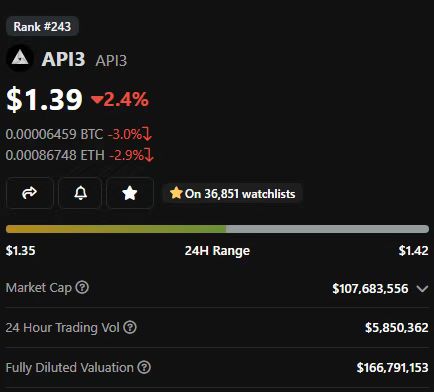

(3) This does not mean that I think API3 will be the default oracle provider for all DeFi. But in terms of risk versus reward, they have clear opportunities for growth.

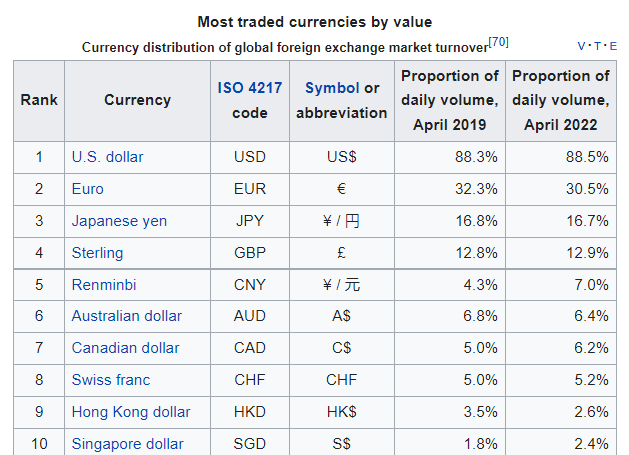

(1) So far, cryptocurrencies have been US-centric, and the stability of the US dollar is very important.

(2) As global economic uncertainty begins to recede and we see emerging markets start to become viable investments again, there will be growing interest in holding and trading other currencies.

(3) The currency foreign exchange market is actually the largest market in the world, with trillions of dollars in capital transactions every day, and so far, none of them are on-chain because there are no viable non-USD stablecoins.

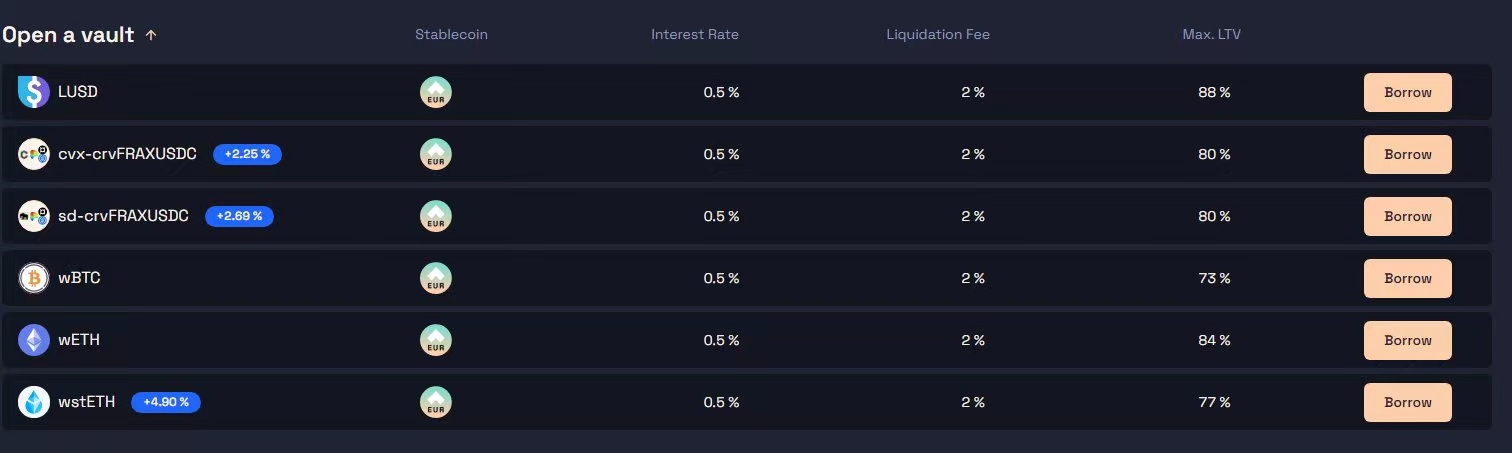

(4) Angle wants to change that, using their agEUR as a MakerDAO for Euros, letting you open a treasury on a variety of collateral at low interest rates.

(5) Currently, users can borrow agEUR at a fixed rate of 0.5%, collateralized by wstETH, wETH, wBTC and other stablecoins. Given the low interest rates, this is the lowest cost stable ETH loan that exists, even if you immediately exchange agEUR for USDC.

(6) To borrow DAI on MakerDAO, you either pay an annual interest rate as high as 3%, or get a lower loan-to-value ratio.

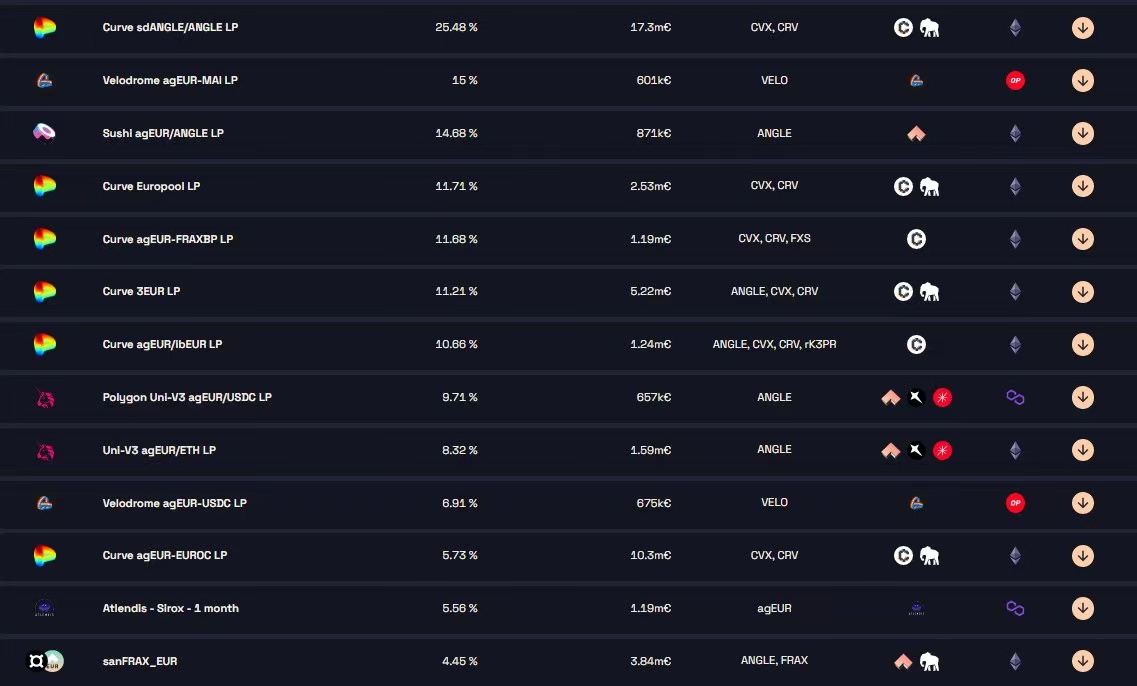

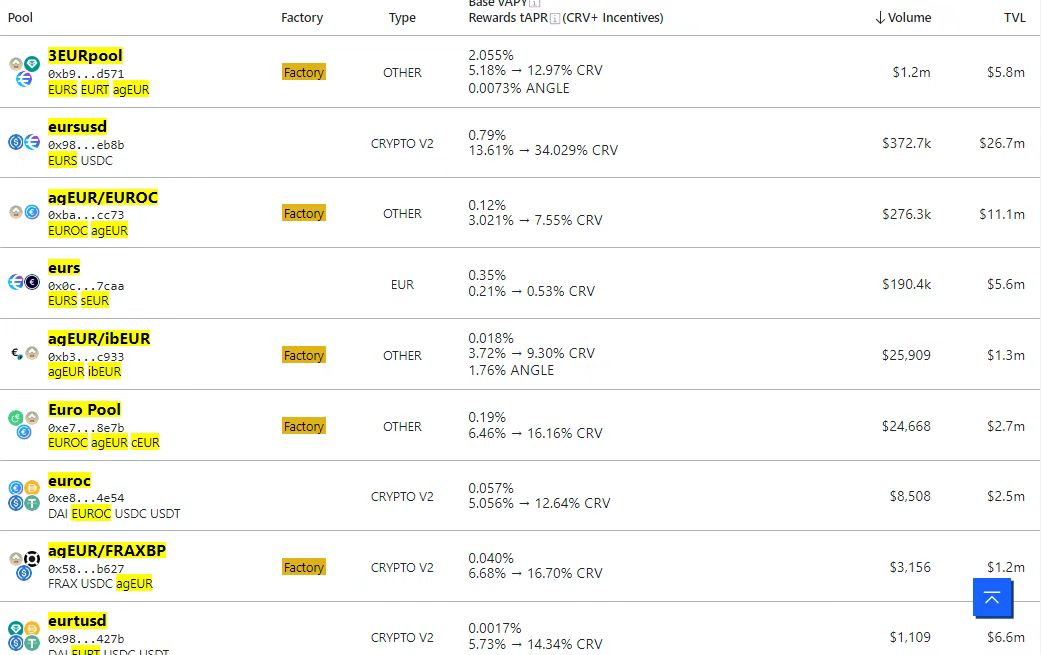

But if you borrow in euros, you can still get rich returns through its incentive pool, which covers multiple chains and pays 4%-25% fees on the stablecoin EUR/EUR trading pair.

(7) This means that, unless you think the USD/EUR exchange rate will fall by another 25%+ this year, at popular farms like Convex Finance or Velodrome Finance, you may choose to invest in the EUR pair rather than the USD pair.

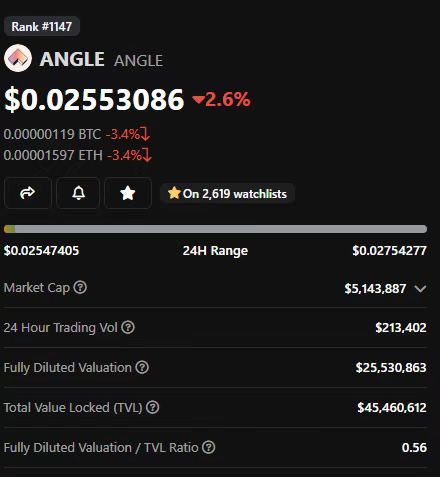

(8) Meanwhile, ANGLE has a market cap of just $5m and an FDV of $25m, with a lot of potential upside considering the euro is the second most traded currency in the world.

(8) One of the ironies of cryptocurrencies is that it is difficult to create stablecoins alone, since much of the liquidity in stablecoins comes from stablecoin trading pairs on Curve. On-chain EUR liquidity is slowly growing with the launch of Circle’s EUROC and Synthetix’s sEUR.

(9) My prediction is that it will take a few more years for Angle to gain a foothold, and as liquidity grows, they will need some large OTC desk to help them settle actual Euros. But as the eurozone recovers, many Europeans will want to hold euros on-chain, and as on-chain transactions become faster and cheaper, more foreign exchange transactions will move on-chain, and the euro will be one of them a big part.

18. Aura Finance(AURA)

(10) If Angle is to succeed, they need to maintain diverse but safe collateral, actively seek incentive partners, and start using agEUR as collateral on other platforms. But given the euro's outstanding global demand, and its low market cap, its risk-reward is still a good opportunity for me.

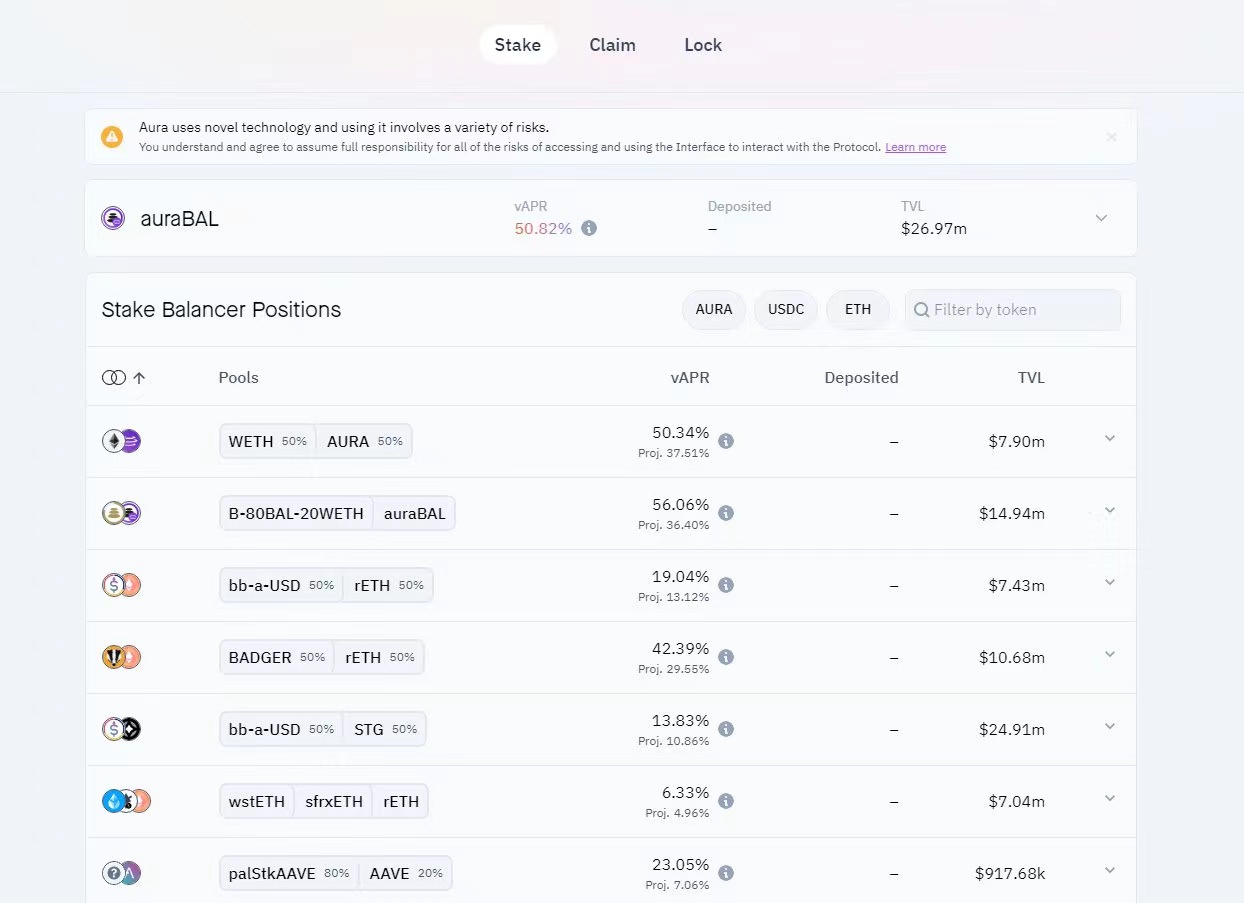

(1) The relationship between Aura and Balance is like Convex is to Curve. This is a locked liquid staking market that helps boost Balancer pool rewards.(2) If you believe in Balancer's theory, it's easy to get started with Aura. I love these locked token games because they really reward people who can patiently buy in and hold for 3-5 years.

The market is all about moving money from the impatient to the patient.

(3) Aura does this while letting you earn 50% APY on staked tokens, and if Balancer does grow in continued demand, there could eventually be a Balancer voting bribery protocol (similar to the Votium protocol ).

(4) In addition, this is a good farming opportunity, even if you don't have a large amount of pledged BAL positions, you can get higher rewards in the pool.

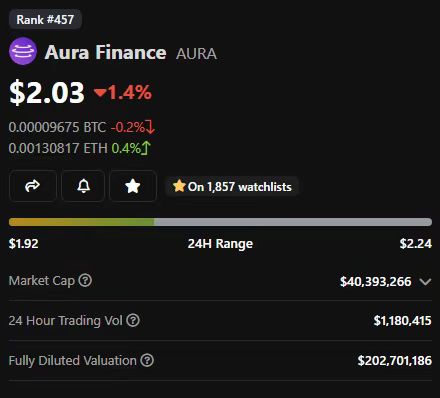

(5) Aura has a market cap of $40M ($202M FDV), which is very attractive considering they hold $27M of BAL permanently locked and only release Aura when new BAL is acquired force ratio.

(6) As we have seen with Convex, they can be extended to other chains, and even use Frax's other products like Convex, thus expanding the scope of application.

19. Gearbox Protocol(GEAR)

(7) Potential catalysts exist under current market conditions. But I think these coins are more likely to go down than up, but if they go up, the rewards are huge.

(1) Gearbox is one of the most interesting new use cases in DeFi, creating a money market for leveraged lending for DeFi applications, eventually allowing users to participate in on-chain leveraged farming.

It's a powerful mechanism, and it generates some pretty strong yields for those who provide the asset. Gaining more than 5% of the stablecoins in the one-sided non-impermanent loss pool of the mainnet is now basically gone, except for Gear.

(2) Their pre-built strategies allow you to enter easy one-click farming positions and earn more APY. However, currently, as it scales, it is limited to a set of whitelisted users.

(3) Gearbox's development is slow, but the emphasis is on its quality. If teams and communities want to scale, they need to continue to leverage new assets and new strategies.

20. CapDot Finance

(4) But in general, the opportunity to be the only source of true leverage without overcollateralization is enormous. This is a market worth tens of billions, if you can seize the opportunity and cash it out safely.

(1) Cap is a community built, owned and operated DEX that allows perpetual futures and margin trading. Its V3.1 was a huge hit on Arbitrum, and their V4 promises to add hundreds of new assets to their perpetual product engine.

(2) Rewards are given to users who pool assets to provide liquidity to the exchange, and then the remainder is used to buy back CAP tokens. This makes the project quite lucrative for small retail investors.

21. LooksRare(LOOKS)

(3) CapDot Finance still has a long way to go, but it's a young, vibrant project that continues to deliver at breakneck speed and is on its way to a giant like DyDdoxx.

(1) I think the NFT market will continue to expand. And I don't think OpenSea will be up for supremacy, Blur will be overpriced and will be more focused on professional traders, and I like rewards.

(2) In the existing attractive NFT market, LooksRare is the only platform that has rewards, is not expensive, and is not like OpenSea. 22% APY is paid out in LOOKS and wETH, and the commission is pretty stable.

22. Pickle Finance(PICKLE)

(3) LooksRare will have to fight back against Blur to regain market share, but I think they can do that by focusing on Polygon and L2, and targeting consumers who are put off by Blur's interface.

(1) Pickle is sort of like the Yearn treasury, but for automatic compounding of rewards. It was a huge hit when it launched, but died in the previous bear cycle. However, the team is still running and their V2 supports almost all chains and thousands of farms.

(2) Nevertheless, you can still use Pickle Jars (fund pool) to earn lucrative APY, and will pledge Pickle, vote to decide which treasury gets the reward, and get a share of the fee. The current reward APY is 19%, which is Pretty impressive for a market cap with low usage. Pickle has a market cap of $643,000 and an FDV of $2.4 million. The market cap is small.

(3) Pickle was on my buy list last year before they came out with the V2 and is on my list now, but I don't own it because I can't actually buy enough to make it worthwhile. I've been waiting for it to develop so I can buy reasonable quantities.

23. Sideshift(XAI)

(4) I hope that Pickle can solve some liquidity challenges, such as incentivizing the Pickel/Weth pool of 80/20 pool, so that the liquidity on the chain is better, and I hope they continue to work hard to create a useful, effective and yield high product.

(1) Sideshift is a non-custodial exchange that requires no registration and no KYC, and can perform cross-chain and cross-asset transactions with instant delivery. You do not need to register or share personal information, you can use multiple chain transactions.

(2) Competitors like ChangeNow offer fiat currency transactions, so they require KYC under certain thresholds. Sideshift only works with cryptocurrencies and stablecoins and is therefore not considered a money services business for most jurisdictions.

(3) Most competitors also don't allow you to transact with privacy coins, while Sideshift supports both Monero and ZCash, including ZCash shielded addresses. It has a wide range of assets in various chains.

(4) It supports Ethereum, Optimm, Polygon, Fantom, Tron, Cosmos, Avalanche, and Arbitrrum for EVM chains. As well as native chains of Bitcoin, BSC, Cronos, Dash, Dogecoi, Litecoin, Tezos, Ripple, Stellar, Solana, Polkadot and Kava.

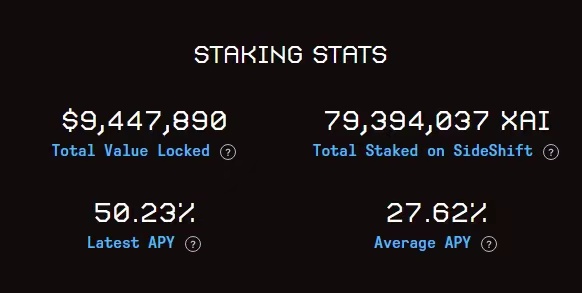

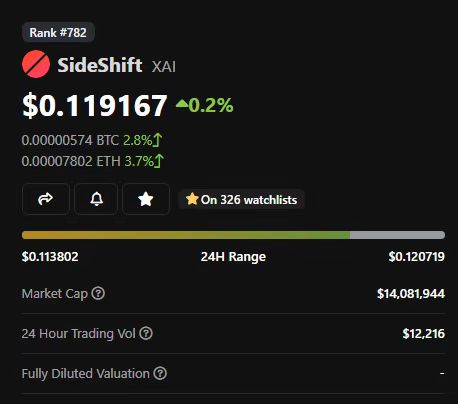

(5) Their native token XAI, like their transactions, is available to individuals who are not on US IP addresses. Earn 50% of Sideshift’s daily transaction fees when staking XAI, currently 50% APY. Sideshift is valued at $14 million.

(6) Before Ethereum’s EVM field was strong, services like Sideshift used to be more popular because they were the key to cross-chain transactions. Projects like Shapeshift used to be one of the biggest and most profitable.

(7) When EVM took over and everything moved to ETH Delta and Uniswap, they both suffered heavy policy hits and reduced interest in cross-chain transactions.

(8) My prediction is that as the transaction chain becomes more and more fragmented, there will be more and more transaction services of this kind. After all, they are essentially just acting as bridges, and there are actually more options.

Finally Clipper, Polymarkets, Llama Airforce, Polynomial are also on my watch list.Hopefully the market will eventually turn around this year, we're all up and not down.

While 2022 will be a challenging year for cryptocurrencies, it will also be a very interesting one.