Coinshares Research: Does Tether Pose Systemic Risk to Cryptocurrency Markets?

Original source:Coinshares

Original source:

Author: Marc Arjoon

Original compilation: GaryMa, Wu said blockchain

We take a look at the reserves of the USDT stablecoin backing Tether and compare it to other similar assets in DeFi and TradFi. The collapse of TerraUSD (UST) has raised doubts about all stablecoins, stable or not, and raised new questions about what reserves are backing the value of these stablecoins. Investors and users as well as politicians and regulators are voicing these concerns. Many believe that stablecoins pose risks to both consumers and the broader economy.

Before the UST crash, all UST in circulation was worth approximately $18.6 billion, of which over $17 billion (90%) was deposited into Anchor. While the value of Terra's ecological loss is enormous (over $40 billion), its impact is relatively limited, accounting for less than 2% of the market. Tether's USDT case is quite different. The current circulating supply of USDT is $74 billion, 4 times that of UST at its peak. Below we show the relative market capitalization of TerraUSD (UST) and Tether (USDT) over the past 180 days.

The market value of UST dropped rapidly with its decoupling. The incident spooked some USDT holders, causing their tokens to be converted into U.S. dollars in amounts as high as $10 billion. For context, Tether has redeemed more than half of UST's entire circulating supply in just over a week and hasn't de-pegged (didn't drop below $0.99). It was the largest batch of redemptions to date without any systemic problems.

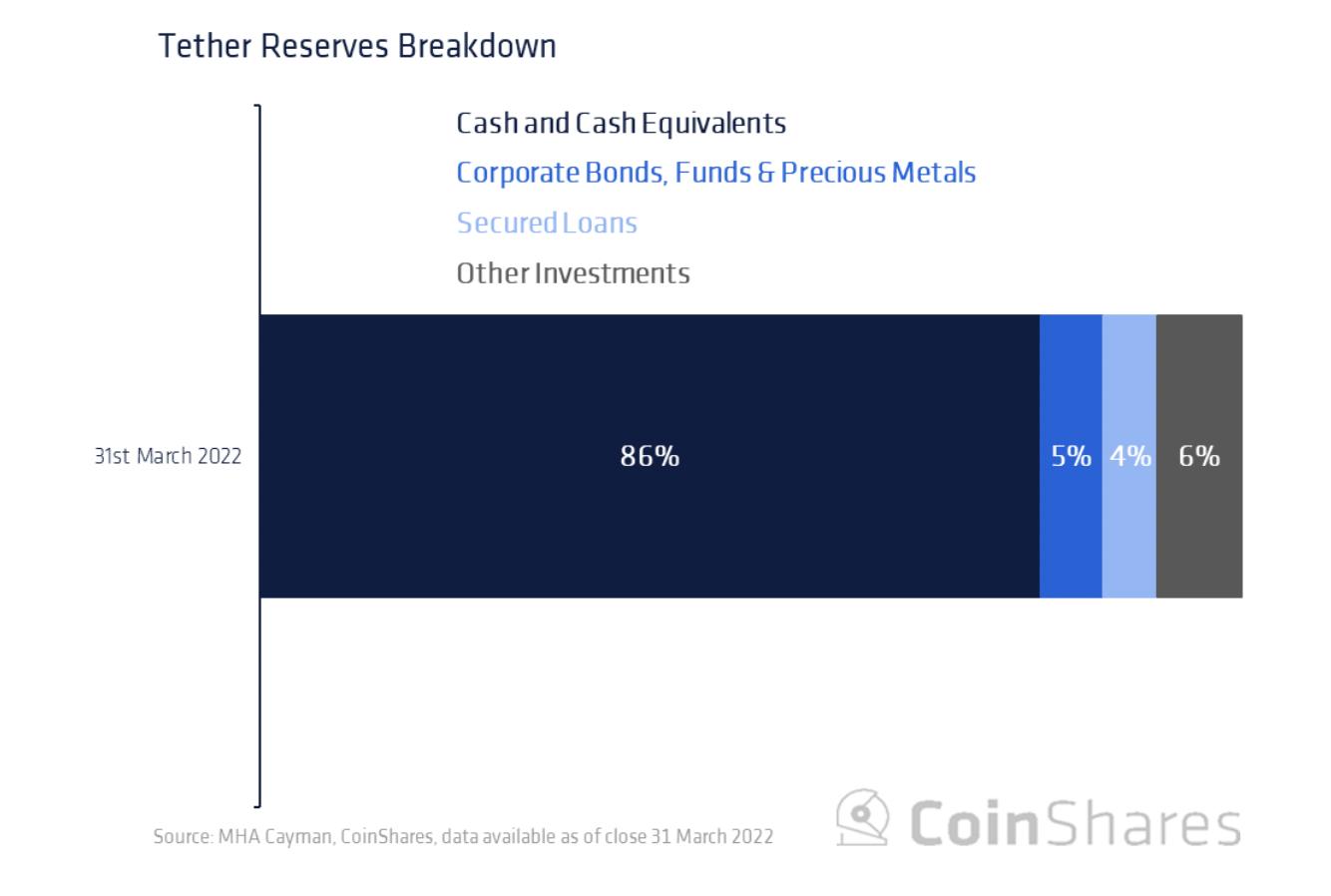

Volatility and redemptions aside, what is USDT's immediate backing and is it safe? Well, those doubts prompted Tether to release an audited quarterly report detailing its reserves. These reserves are currently audited by MHA Cayman, an accounting firm based in the Cayman Islands. We highlight the latest audit breakdown below.

We see that USDT is not financially backed 1:1 by cash (or cash equivalents), but more like 0.85:1. A closer look at cash and cash equivalents shows that just over half is allocated to US Treasuries and about 30% is allocated to commercial paper (CP) and CDs. The remaining 16 percent was allocated to money market funds (about 10 percent), cash and bank deposits (about 6 percent), non-U.S. Treasury bills (about 0.4 percent), and reverse repos (0.15 percent).

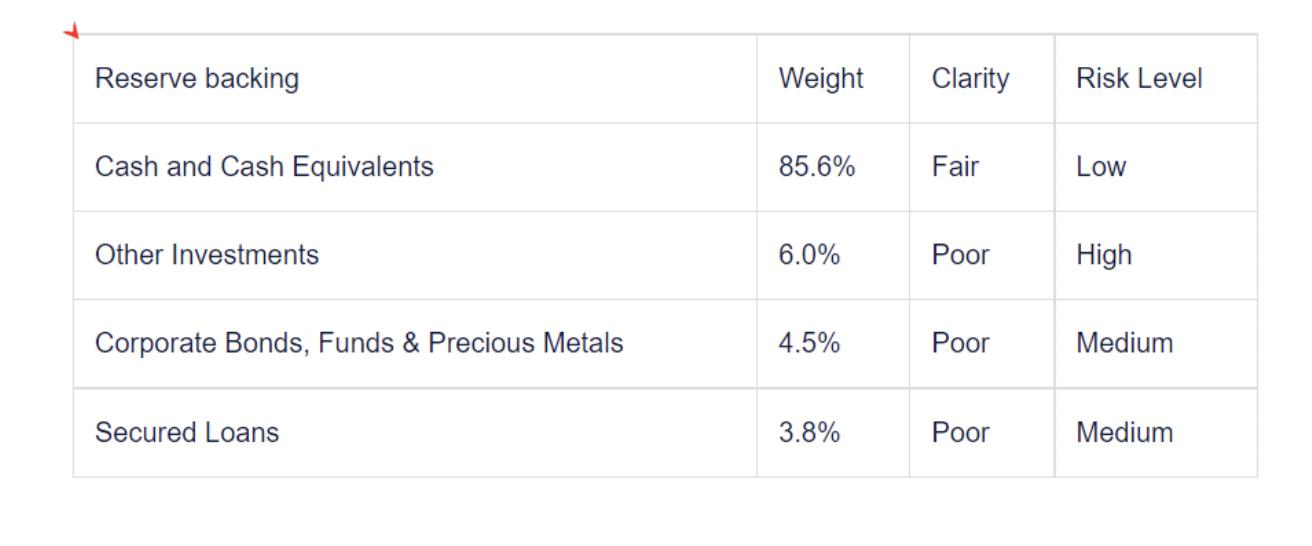

As for the remaining 14.36%, the audit did not provide further explanations. Allocations to corporate bonds, funds and precious metals (4.52%) provide no details on corporate bond types (investment grade, country) and fund types. Types of precious metals are also excluded, and the percentage breakdown of the three categories is also opaque. Secured loans (3.82%) have no disclosures, but references to other investments (6.02%) do include digital assets, but to what extent is also unclear.

As for the remaining 14.36%, the audit did not provide further explanations. Allocations to corporate bonds, funds and precious metals (4.52%) provide no details on corporate bond types (investment grade, country) and fund types. Types of precious metals are also excluded, and the percentage breakdown of the three categories is also opaque. Secured loans (3.82%) have no disclosures, but references to other investments (6.02%) do include digital assets, but to what extent is also unclear.

history

Since 2017, Tether has hired the services of several different banks, legal firms and accounting firms to certify the size and validity of its reserves. These companies include MHA Cayman, Moore Cayman, Deltec Bank, FSS and Friedman LLP. Below we turn to a brief history of these relationships."In 2017, as pressure on USDT reserves mounted, Tether invited accounting firm Friedman LLP to conduct a reserve audit, but critics emphasized that the study had methodological flaws and did not represent a complete audit. Shortly after the first audit, Tether Corporation reported that Friedman did not perform as well as they believed"within a reasonable time

Audit work completed and partnership terminated. The Tether company then turned to Washington-based law firm FSS. The FSS report was not a full audit of Tether, but said the law firm had received sworn and notarized statements from two of Tether’s (unnamed) banks. To help build confidence, Tether gave way to Bahamas-based bank Deltec to publish a report confirming the amount of cash Tether had in their accounts there, but again this does not provide the full picture as it is only the cash value from one of its banks . In 2021, the New York Attorney General's Office completed an investigation stating that Tether had exaggerated its reserves and hidden losses of approximately $850 million. This resulted in an $18.5 million fine and was required to release quarterly reports of its holdings within two years. Around the same time, Tether announced a partnership with Moore Cayman, an accounting firm in the Cayman Islands. Moore provided an assurance report attesting to the full backing of USDT, and later provided a more detailed breakdown of reserves. However, from January 2022, MHA MacIntyre Hudson said its Cayman Islands branch, MHA Cayman, will handle Moore Cayman clients. It should be noted that MHA MacIntyre Hudson is currently under investigation by the FRC for a previous audit of an unrelated company.

As mentioned above, the breakdown of reserves will only be available from June 30, 2021 (after other stablecoins start launching). For the most part, the weighting of allocations has remained relatively stable since June 2021, with cash and cash equivalents rising slightly from 85% to 86%, while secured loans remained at 4%. However, other investments (including digital assets) have doubled from 3% to 6%, increasing the risk level of the reserve. Growth in other investments came at the expense of corporate bonds, funds and precious metals, which fell from 8% to 5% over the period. In dollar terms, cash and cash equivalents rose 7% in the most recent quarter, while secured loans fell 24%.

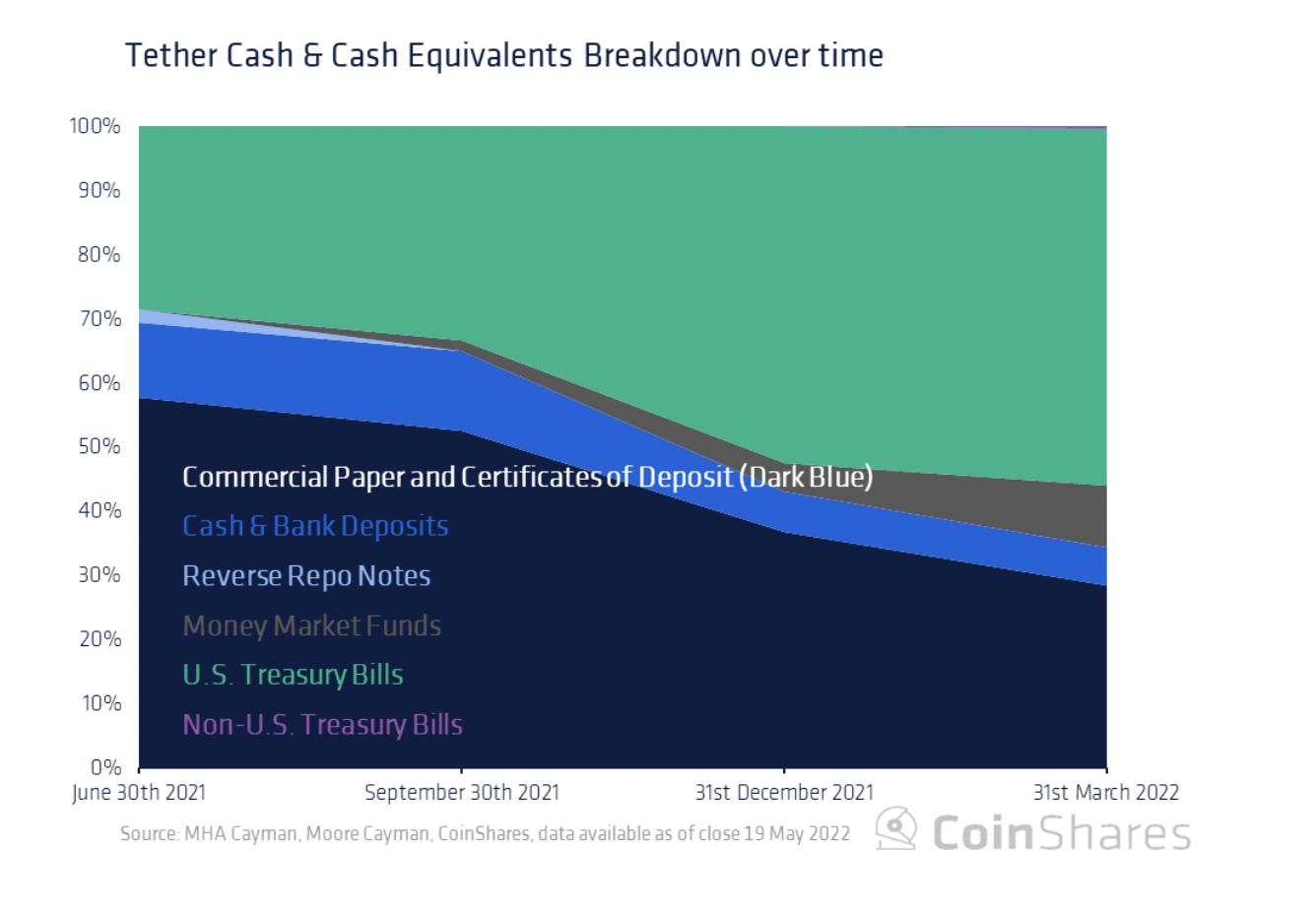

Digging deeper into cash and cash equivalents, we show below that US Treasuries have begun to form a larger portion of reserves (24% to 48%), displacing the dominance of commercial paper and CDs (49% to 24%). Concerns about the riskiness of these instruments have been somewhat eased by the reduction in commercial paper holdings. Cash and bank deposits were reduced from 10% to 5%, and reverse repurchase notes were reduced from 2% to 0.1%. There was also an increase in money market funds, which now account for 8%, and in the most recent quarter, non-US Treasuries also increased (0.3%).

Digging deeper into cash and cash equivalents, we show below that US Treasuries have begun to form a larger portion of reserves (24% to 48%), displacing the dominance of commercial paper and CDs (49% to 24%). Concerns about the riskiness of these instruments have been somewhat eased by the reduction in commercial paper holdings. Cash and bank deposits were reduced from 10% to 5%, and reverse repurchase notes were reduced from 2% to 0.1%. There was also an increase in money market funds, which now account for 8%, and in the most recent quarter, non-US Treasuries also increased (0.3%).

The quality of Tether's commercial paper continues to be questioned, even as its distribution is reduced. Below we show the rating breakdown for Tether's commercial paper as of March 2022.

However, since March 31, 2022, there have been approximately $10 billion in redemptions (down from approximately $84 billion to $74 billion in size) without any adverse effects. The redemption process involves a one-time $150 verification process and a 0.1% fee, and the current minimum redemption amount is $100,000. Those limits could slow things down in the event of a run on assets, but evidence suggests Tether has been able to process billion-dollar redemptions in just over a week.

Compared

Compared

So, how do Tether's reserves compare to leading money market funds? As stated in the audit report, 8% of Tether’s reserves are made up of money market funds, although details of these funds were not disclosed. We looked at the portfolios of several top money market funds by AUM and compared their holdings as of the previous quarter. We see that mutual funds can vary widely in their fixed income holdings, although commercial paper repurchase agreements and certificates of deposit appear to be popular choices.

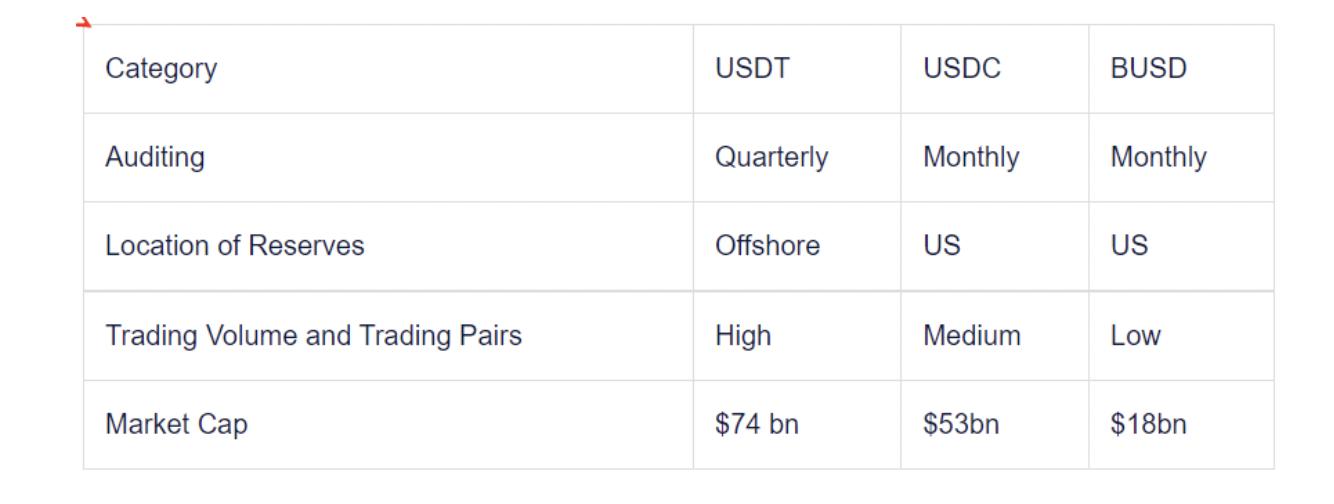

While it's useful to contrast the differences between money market funds and stablecoin reserves, it's not exactly a like-for-like comparison. Below we highlight the reserve breakdown of the last two largest stablecoins by market capitalization, Circle’s USDC and Binance’s BUSD.

BUSD, which was created by Binance and Paxos, does not break down the weighting between cash and US-backed debt. BUSD reserves are audited by Withum (which also audits other stablecoins).

Tether was the first mainstream stablecoin and had market dominance for several years. In recent times, however, Circle's USDC and Binance's BUSD have gained significant market share among the mainstream stablecoins (~37% and ~13%, respectively).

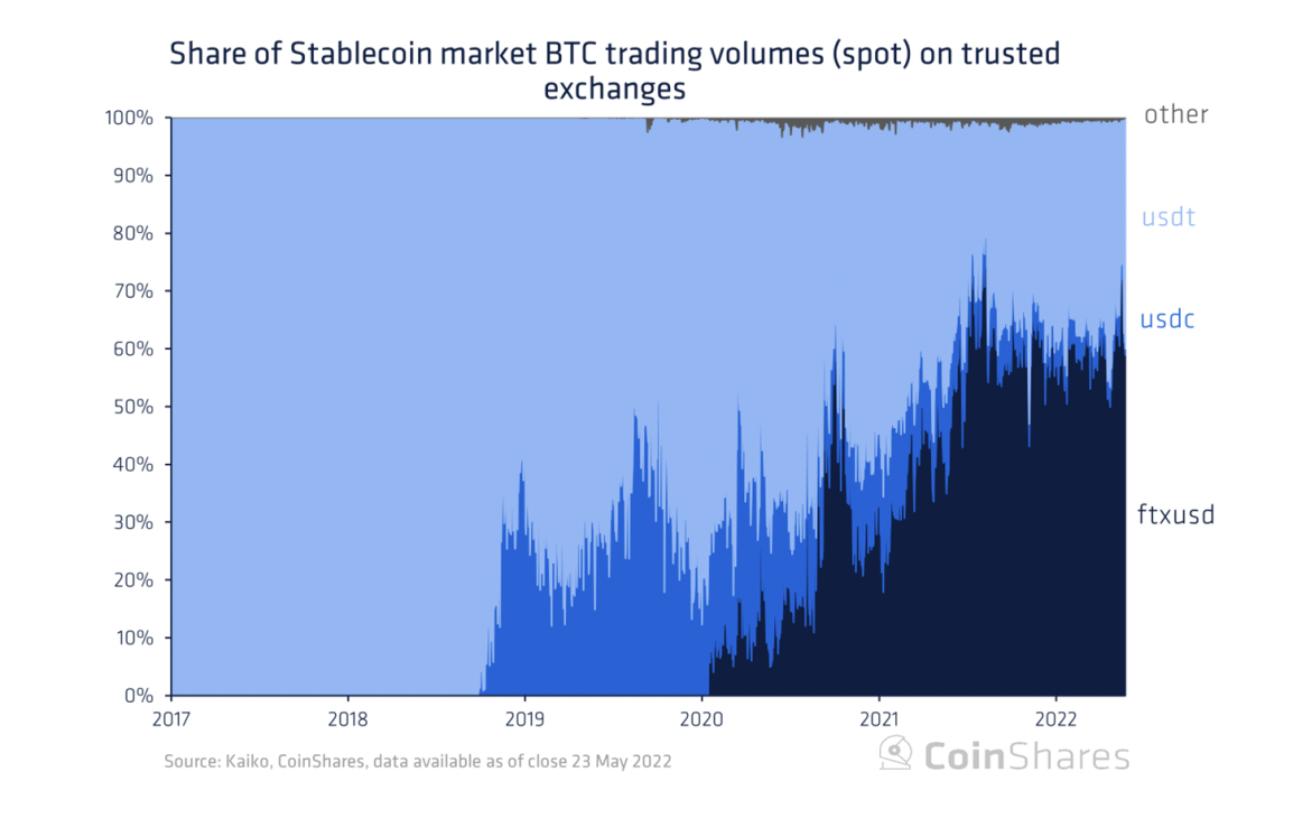

Additionally, Tether has a ~33% market share of all stablecoin/BTC trading volume on trusted exchanges, although this is also waning. The relative importance of USDT is clearly declining.

Additionally, Tether has a ~33% market share of all stablecoin/BTC trading volume on trusted exchanges, although this is also waning. The relative importance of USDT is clearly declining.

All three stablecoins are pegged 1:1 to the US dollar, Circle and Binance/Paxos are subject to and publish monthly audits, while Tether is quarterly. While USDT always shows its reserves, it does not provide public information about audits, which may be a concern for investors. Despite differences in transparency reporting, there are some differences in reserves between these stablecoins. We highlight some more differences between these three stablecoins below.The world's most popular stablecoin, Tether, has withstood many tests and some black swan events since its launch in early 2015. The first-mover advantage combined with real-world testing has increased people's confidence in USDT, as evidenced by the growth in circulating supply.

However, the real test may be yet to come, with renewed focus on stablecoin reserves already resulting in a 12% reduction in USDT circulating supply through recent redemptions.

Plus, competitors like Circle have more transparent reporting in a more trustworthy regulatory environment. This sense of security in USDC (and other stablecoins) has continued to cause Tether’s market share to decline.

As seen before, this trend may lead Tether to adopt stronger reserves, greater transparency, and more diligent auditing practices.

Of course, Tether can also lie flat and don’t care about the reduction of credible transparency, market share and supply scale, but this will cause Tether’s market influence to be greatly reduced."If it's going the first way, that reduces the risk for everyone, but if it's going the second way, then"This question becomes less important.