Powell's Farewell Night, Wall Street Hears a Louder Hawkish Tone

- Core Viewpoint: The Federal Reserve kept interest rates unchanged at its April meeting, but internal hawkish divisions have intensified. Coupled with surging oil prices and Powell's term coming to an end, market expectations have shifted from pricing in rate cuts to the risk of rate hikes. The interest rate environment is entering a complex new phase driven by the multi-factorial influences of inflation, energy, employment, and policy communication.

- Key Factors:

- Three dissenting votes within the committee against retaining a dovish bias indicate a loosening consensus on policy direction within the FOMC, and the market is beginning to price in rate hikes rather than cuts.

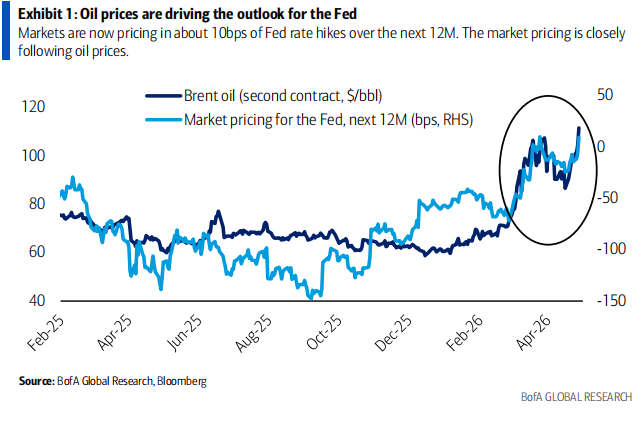

- The Iran situation pushed Brent crude oil to $120 per barrel. On that day, approximately 7 basis points of the 10 basis point increase in the 2-year Treasury yield came from the oil price shock, far exceeding the impact of the Fed's decision itself.

- Powell confirmed this meeting was the last under his chairmanship. The Senate has advanced the nomination of Kevin Warsh as the new chair, increasing uncertainty regarding policy style and communication framework.

- Institutions like Goldman Sachs, Bank of America, and JPMorgan all believe the bar for rate cuts has been raised. HSBC predicts no rate cuts between 2026 and 2027. The market has priced in approximately a 10 bps rate hike, making the hawkish sentiment the highest since June 2025.

- Powell stated that adjustments to policy guidance "could come as early as the next meeting," and the future dovish bias will shift towards a more neutral stance, but on the condition that oil prices stabilize and progress is made on tariff issues.

Original Title: "Powell Steps Aside, Oil Prices Take Center Stage, Hawkish Tone Intensifies Across the Board – Wall Street Reviews the Fed Decision"

Original Author: Zhao Ying

Original Source: Wall Street CN

The Fed held its ground, yet Wall Street heard an even louder hawkish screech. Three dissenting votes against retaining an accommodative bias, the inflationary pressure from surging oil prices, and Chairman Powell's term winding down have collectively pushed the market from pricing in rate cuts to the more complex risk of rate hikes.

According to Zephyr Trading Desk, at the FOMC meeting on April 29, the Fed kept the federal funds rate target range unchanged at 3.50%-3.75%. Post-meeting analyses from Goldman Sachs, Bank of America, JPMorgan Chase, and HSBC all point to the same conclusion: the truly important aspect is not the rate decision itself, but the widening divergence in the statement's language, indicating that the consensus on policy direction within the committee is loosening.

As the situation in Iran deteriorates, oil prices became another major theme of the day. BofA noted that the 2-year Treasury yield rose 10 basis points on the day, with only about 3 basis points occurring after the Fed's decision; the remaining 7 basis points were primarily attributed to Brent crude oil surging 8% to $120/barrel. JPMorgan also believes that the Iran situation and risks in the Strait of Hormuz have pushed up energy prices, directly compressing the Fed's room for easing.

The power transition further amplifies policy uncertainty. Powell confirmed that this would be his last FOMC meeting as Fed Chair, stating he would remain on the FOMC as a regular governor after his term ends, with his tenure duration yet to be determined. Meanwhile, the Senate Banking Committee has advanced Kevin Warsh's nomination for Fed Chair. An era of monetary policy has officially concluded, and the policy style and communication framework of the successor are becoming the new focus of market attention.

Three Dissenting Votes: The Easing Bias Is No Longer Secure

The most closely watched signal from this meeting was the split within the FOMC over the statement's language.

Goldman Sachs economist David Mericle noted that Governors Hammack, Kashkari, and Logan opposed the language implying an accommodative bias in the statement. This outcome caught Goldman Sachs by surprise. Meanwhile, Governor Miran supported a rate cut, consistent with Goldman's earlier assessment.

The dispute centers on the statement's wording regarding the "timing of additional adjustments." In the market context, this phrase is seen as a signal retaining the possibility of further rate cuts. The opposition of three members to retaining this language means some policymakers are no longer willing to signal a one-sided easing stance to the market.

In his press conference, Powell acknowledged "vigorous debate" within the committee regarding the policy guidance. He stated that the number of members supporting a move to more neutral guidance had increased compared to March. The FOMC's central tendency is moving towards a 'more neutral' interest rate outlook, but most members believe the current timing is premature. He even suggested that adjustments to the wording "could come as soon as the next meeting" – scheduled for June 16-17.

HSBC also emphasized that the essence of this division is that the policy direction is no longer one-sided. While the three members supported keeping rates unchanged, their explicit opposition to retaining the easing bias sends a signal to the market: the next move could be either a rate cut or a rate hike.

"Rate Hikes" Back in Pricing, Bar for Cuts Raised

The consensus on Wall Street is that the Fed hasn't officially pivoted to rate hikes, but the long-dormant concept of "rate hikes" has formally re-entered the market's field of vision.

BofA stated that following a slightly hawkish FOMC meeting, compounded by record-high oil prices, the market has now priced in approximately 10 basis points of rate hikes over the next 12 months. The bank also noted that this is different from the 2022 rate hiking cycle because the current energy shock also puts downward pressure on growth, a point Powell highlighted in his press conference.

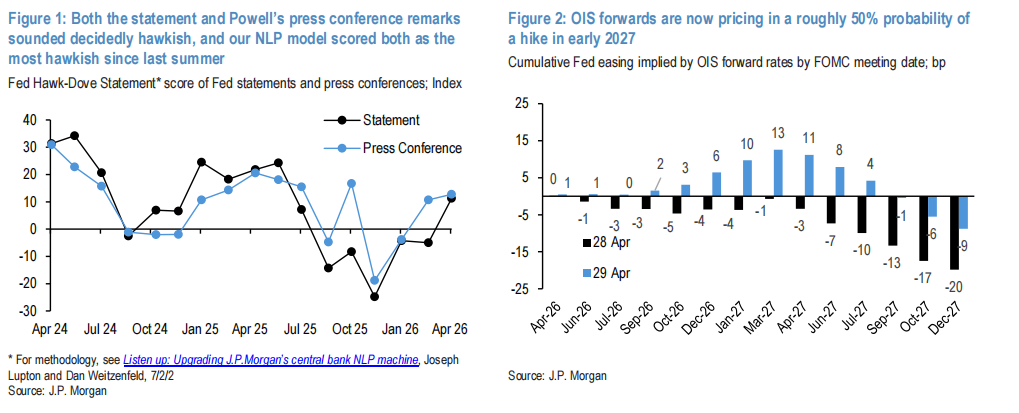

JPMorgan's interpretation was more hawkish. Its natural language processing model showed that the hawkishness scores for both the statement and Powell's press conference hit their highest levels since June 2025. The bank stated that money market pricing has rapidly shifted from "pricing in nearly one full rate cut by end-2027" to "pricing in nearly a 50% probability of a rate hike by early-2027."

Goldman Sachs maintained a more cautious view. The bank still predicts the Fed could cut rates in September and December, but believes the bar for cuts has been raised significantly in the absence of a clear weakening in the labor market. Goldman stated that the risk of a prolonged pause in rates is rising, but remains highly skeptical about the possibility of rate hikes.

HSBC offered the most hawkish forecast. The bank expects the Fed will not cut rates in either 2026 or 2027. HSBC believes that unless core PCE inflation falls below 3%, or even 2.5%, rate cuts are nearly impossible to discuss. Their own forecasts show core PCE inflation staying above 3% through end-2026 and above 2.5% through end-2027.

Oil Prices Take Starring Role, Iran Situation Dominates Pricing Logic

Unlike past meetings where the Fed's statement drove market reaction, energy prices became the core variable for interest rate markets on the day of this meeting.

BofA noted that of the 10 basis point rise in the 2-year Treasury yield, only about 3 basis points could be attributed to the Fed's decision itself, with the majority of the increase stemming from Brent crude oil rising to $120/barrel. The bank believes the main driver of the Fed's outlook currently is the Iran situation and oil prices, rather than a simple policy reaction function.

JPMorgan also attributed the rise in front-end yields and the flattening of the yield curve to the deteriorating situation in the Middle East and risks in the Strait of Hormuz. Rising oil prices not only boost inflation expectations but also make it harder for the Fed to signal easing.

In his press conference, Powell explicitly stated that amid high uncertainty regarding the war and energy prices, most members saw no need to adjust policy guidance at this time. JPMorgan stated that Powell set a prerequisite for potential rate cuts: needing to see stabilization in energy prices and progress on tariff issues.

Goldman Sachs believes that even if the geopolitical conflict ends, some FOMC members might remain hesitant to cut rates with inflation still closer to 3% than 2%. Even if the inflation overshoot stems primarily from tariff and energy price pass-through, policy easing may not arrive quickly.

Powell's Final Curtain Call, Warsh Takes the Baton Introduces New Variables

This meeting also marks the end of Chairman Powell's term.

BofA stated this was the last FOMC meeting chaired by Powell. The Goldman Sachs report also mentioned that Powell indicated he would remain on the FOMC as a regular governor after his chair term ends on May 15, with the duration to be determined.

Regarding the reason for staying, Goldman stated Powell said he is waiting for certain investigations to conclude in a transparent and final manner and will leave when he deems it appropriate. JPMorgan and HSBC also noted that Powell intends to maintain a low profile and will not obstruct the functioning of the FOMC under Warsh's leadership.

The progress of Warsh's nomination has become a focal point for markets. JPMorgan stated the Senate Banking Committee voted along party lines to advance his nomination. HSBC pointed out that the full Senate vote has not yet occurred, but if it proceeds smoothly, Warsh could take office officially before the June meeting.

HSBC believes Warsh could bring about systematic changes in the policy communication framework. The bank's rates strategist noted that Warsh has expressed skepticism about the Fed's "dot plot" rate projection mechanism. If forward guidance is weakened in the future, bond market volatility could increase, and long-end term premiums could face upward pressure.

Coexisting Rate Volatility and Policy Uncertainty

For fixed-income investors, the message from this meeting is not singular. Front-end yields are suppressed by oil prices and hawkish pricing, pushing back rate cut expectations, but rate hikes are not yet the consensus base case across investment banks.

BofA believes that in the investment-grade bond market, the current rise in yields partly offsets the impact of rate volatility. As implied rate volatility remains below its peak from March this year, investment-grade bonds still have periodic technical support.

JPMorgan suggests that the combination of pressure on front-end yields, expensive valuations for intermediate-term Treasuries, and policy uncertainty from the leadership change means the rates market is entering a more complex phase of strategic positioning.

HSBC maintains a "maximum bullish" stance across multi-assets, focusing on U.S. stocks. The bank stated that despite the hawkish repricing of rate expectations, risk assets performed strongly in April. Optimism surrounding the profitability of the AI supply chain remains a key narrative for multi-asset markets.

Overall, Wall Street's conclusion on this FOMC meeting is: The Fed didn't change rates, but it changed the market's probability distribution for the next move. With Powell stepping aside, oil prices taking center stage, and Warsh set to take over, investors are no longer facing a simple rate cut timeline, but a new interest rate environment driven by the interplay of inflation, energy, employment, and policy communication.