MetaMask 聯創走了,留下一隻被裝進 IPO 招股書的小狐狸

- 核心觀點:MetaMask 共同創辦人 Dan Finlay 因職業倦怠離職,而母公司 Consensys 正籌備 IPO。在競爭加劇、產品創新滯後和用戶成長放緩的背景下,MetaMask 正面臨品牌價值高於產品價值的困境,Consensys 或選擇在品牌巔峰期透過 IPO 變現。

- 關鍵要素:

- Dan Finlay 因倦怠離開,標誌 MetaMask 十年發展週期結束,其創辦人幾乎不具個人品牌,產品熱度已被行業 KOL 八卦取代。

- 競品 Phantom 基於 Solana 生態崛起,年化收入約 1.08 億美元,遠超 MetaMask 的 4600 萬美元,用戶增量已被分流。

- MetaMask 慢於支援 Solana 等公鏈,其身份(以太坊親兒子)限制了跨鏈決策,2025 年 5 月才原生支援 Solana,已錯過窗口期。

- Consensys 為衝刺 IPO 已啟動兩輪裁員(2024 年 10 月裁員 20%,2025 年年中又一輪),內部員工士氣因晉升意願被裁等負面評價而低落。

- $MASK 代幣自 2021 年起被宣傳但至今未發,聯創離職後代幣計劃成謎,IPO 被視為將品牌而非產品變現的理性選擇。

Author: Kuri, Shenzhen TechFlow

The person who built this little fox no longer wants to build it.

On April 23rd, MetaMask co-founder Dan Finlay announced his official departure from Consensys, ending a decade-long development career. The reason given was burnout and a desire to spend more time with family.

MetaMask is arguably the most recognizable product application in the crypto world. Almost anyone who has installed a crypto wallet knows the logo of that little orange fox. In 2016, Finlay and co-founder Aaron Davis built this browser extension within Consensys, allowing ordinary people to interact with Ethereum without running a full node.

Over the past decade, according to statistics from various third-party platforms, global installations have exceeded 100 million, with approximately 30 million monthly active users. The swap feature has generated over $325 million in cumulative fee revenue.

Looking through public information, I found that Finlay has rarely given interviews over the past ten years. He previously wrote code at Apple, and at his core, he is likely an engineer, not someone building a public persona.

When someone like that says they're tired, it's usually genuine. However, the timing of his departure makes it hard not to read into things.

Just a few months ago, Consensys hired JPMorgan and Goldman Sachs as IPO advisors. According to Axios, the goal is to go public as early as this year.

The company's last funding round was in 2022, with a valuation of $7 billion. Since then, it has undergone at least two rounds of layoffs. Meanwhile, the $MASK token has been rumored since 2021 but has remained silent for five years.

Issuing a wallet token seems less necessary, and more frighteningly, the little fox seems less necessary for everyone too.

It's the Default Fox, But Not a Must-Have

Many dApp development documents used to start with "Please install MetaMask first." It was the default wallet of the industry, much like how ten years ago, when you installed Windows, the blue IE browser was on your desktop.

The problem is, the default and the preferred choice are no longer the same thing.

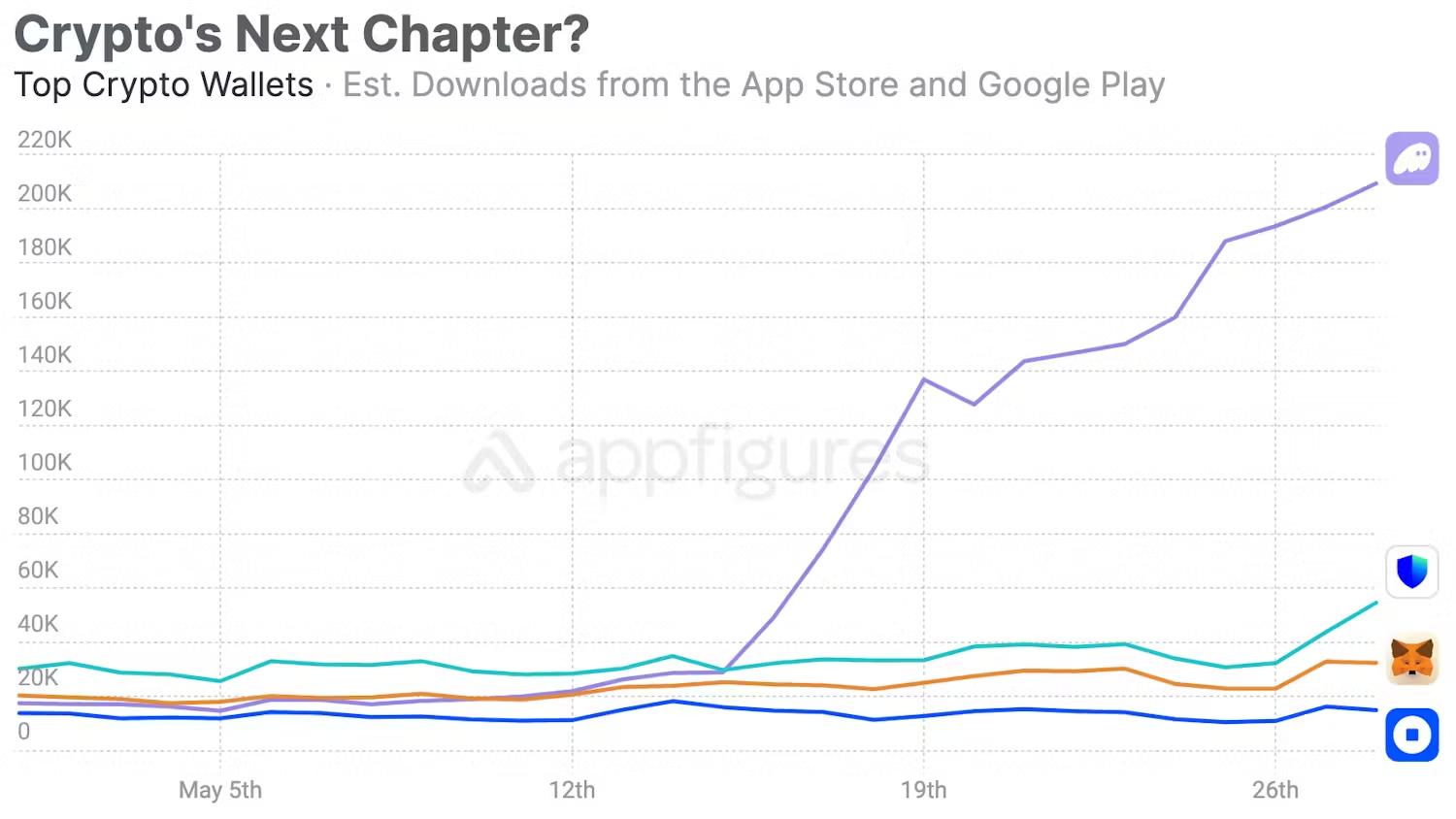

Phantom started as a Solana-only wallet and later expanded to Ethereum and Bitcoin. In January 2025, it raised $150 million in a Series C round, valuing it at $3 billion.

According to estimates from whales.market citing on-chain data, Phantom's annualized revenue is approximately $108 million. In comparison, MetaMask's is around $46 million. That's more than double, and Phantom was born five years after MetaMask.

Phantom started on Solana in 2021 and rode the wave of the Solana ecosystem's recovery and explosion. According to Helius, in 2024, Solana's DEX trading volume surpassed Ethereum's, and in 2025, on-chain application total revenue reached $2.39 billion, a 46% year-over-year increase. 725 million new wallets completed their first Solana transaction in 2025. When these users came in, Phantom was waiting at the door.

What about MetaMask? It only launched native Solana support in May 2025. Before that, users who wanted to use Solana through MetaMask had to install a third-party plugin called Snaps, an experience akin to running a Chrome kernel inside IE...

During these five years, Solana went from a chain that nearly died due to the FTX collapse to becoming, for a time, the chain with the highest trading volume. Phantom's valuation grew along with it, securing a $150 million Series C funding round in early 2025 at a $3 billion valuation.

I believe MetaMask's slowness isn't due to technical limitations; there's also an identity issue. MetaMask is the 'child' of Ethereum. The founder of its parent company, Consensys, is Ethereum co-founder Joe Lubin.

Supporting Solana is expansion for Phantom, but for MetaMask, it's betrayal. By the time the Ethereum ecosystem's growth rate undeniably slowed and cross-chain support became necessary, the window of opportunity had already passed.

Of course, MetaMask still has the strongest compatibility within the Ethereum ecosystem. Almost all dApps on EVM chains test with it as the default option. Its 30 million monthly active users are real.

But this stickiness doesn't come from product strength; it comes from switching costs. Switching costs only prevent old users from leaving; they don't prevent new users from coming.

Someone who started playing on-chain in 2025 is very unlikely to have MetaMask recommended by friends when installing a wallet.

The Little Fox on the Shelf

The product is falling behind, people are leaving, yet Consensys is preparing for an IPO.

According to Axios, in October 2025, Consensys hired JPMorgan and Goldman Sachs as IPO advisors, targeting an IPO as early as this year. If successful, it would be the first company deeply tied to Ethereum's core infrastructure to list on the US stock market.

But in the same year it hired investment banks, Consensys went through at least two rounds of layoffs.

In October 2024, it cut 20% of its staff, about 160 people. CEO Joe Lubin cited macroeconomic pressures and regulatory uncertainty. Another round of layoffs occurred in mid-2025, this time justified by the need to "drive profitability."

On Glassdoor, the well-known job community, employee reviews are uglier than the layoffs themselves.

One person wrote that the company lays off people at least twice a year, always front-line contributors, never management. Another said that after sharing their promotion aspirations with their superior, their name appeared on the next layoff list.

I don't know how much of these reviews is emotion versus fact. But a company aggressively cutting costs and seeing employee morale hit rock bottom right before an IPO is a signal in itself.

Then there's the story of the MASK token.

In 2021, Lubin tweeted "Wen $MASK?" and the community buzzed with excitement. In 2022, he elaborated on plans for a token plus DAO to drive "progressive decentralization." In May 2025, when The Block asked Finlay about the token's timeline, his answer became just maybe.

For users, the MASK token is a carrot dangled in front, encouraging continued use, interaction, and contributing on-chain data to MetaMask. For Consensys, the token is a card yet to be played before the IPO.

Issue it too early and dilute the valuation narrative. Issue it too late and lose the community's patience. Now the co-founder is gone, the token hasn't been issued, but the IPO is coming.

MetaMask's product competitiveness is declining, a trend hard to reverse quickly. However, MetaMask's brand recognition remains. That little orange fox is still the most recognizable crypto logo worldwide.

Brand value and product value decay at different speeds. Brand decays more slowly.

For crypto companies, an IPO often sells not the product itself, but the brand plus the narrative. "Ethereum infrastructure," "Web3 gateway," "world's largest self-custody wallet"... these labels still sound great on pitch decks. Lubin himself, as an Ethereum co-founder, carries an aura for traditional investors.

So, Consensys's choice is to package MetaMask into a publicly-traded shell and let the secondary market price it, while the brand still holds value, the regulatory window is still open, and Wall Street still has enthusiasm for crypto infrastructure.

Silence Isn't Golden

The reaction to co-founder Finlay's departure has been very muted within the crypto circles. No flood of long farewell posts, no laments about "the end of an era." Most people don't even care about this news.

The departure of a MetaMask co-founder generates less buzz than some KOL complaining about swag shrinkage at a conference in Hong Kong.

That in itself says something.

MetaMask is a rare case in the crypto industry. It possesses the industry's biggest brand, yet its founders have virtually no personal brand.

In an industry where the founder is the biggest marketing resource, MetaMask's two founders chose to remain invisible. The product spoke for them, until it could no longer.

I believe MetaMask's story is, at its core, a story about the "default."

In the tech industry, being the default option is the most powerful competitive advantage and also the most dangerous anesthetic. When you are the default, user growth happens without you needing to do anything. It comes on its own.

But this growth masks the product's own aging. By the time you notice users leaving, the exodus has often been happening for a long time.

IE was the default browser, lost to Chrome. Nokia was the default phone, lost to iPhone.

Windows Media Player was the default player, lost to everyone else. When these products lost, they still had high market share and strong brand recognition, but new users had simply stopped choosing them.

MetaMask is now standing at that exact point. Existing users are still there, the brand is still strong, but the incremental growth has gone elsewhere. Consensys's IPO plan is, ultimately, about monetizing the existing user base.

At a stage where brand value exceeds product value, selling out is indeed the rational choice.

On the day Finlay left, MetaMask had just launched an advanced permission feature called ERC-7715. He said he looked forward to experiencing it as a regular user.

A product's creator becoming its ordinary user is perhaps the most sincere and quiet farewell in the crypto industry.

But for MetaMask, how many ordinary users will still click on that little fox every day next year? Are you still using it?