Morgan Stanley: Chi 1,4 nghìn tỷ USD cho Hạ tầng AI, “Bài toán sức mạnh tính toán” của META có thu hồi vốn được không?

- Quan điểm chính: Báo cáo nghiên cứu của Morgan Stanley ước tính, chi tiêu vốn của năm nhà cung cấp dịch vụ đám mây lớn vào năm 2028 có thể lên tới 1,4 nghìn tỷ USD, công suất tính toán khả dụng sẽ mở rộng lên 120GW, nhưng chi phí mỗi GW bị đẩy lên cao do bộ nhớ, điện năng và các yếu tố khác; META được chọn là ưu tiên hàng đầu, liệu họ có thể chuyển đổi sức mạnh tính toán khổng lồ thành doanh thu từ quảng cáo, API, v.v. là chìa khóa để kiểm chứng lợi nhuận.

- Các yếu tố chính:

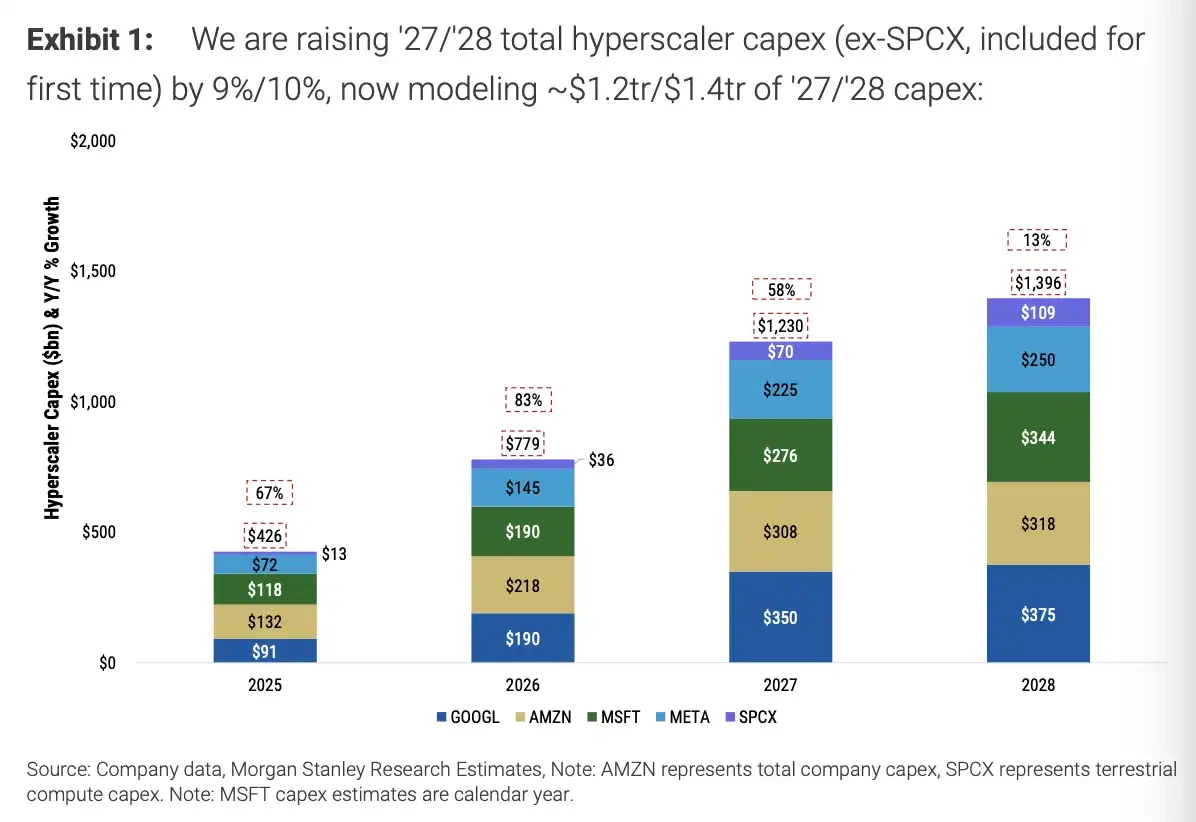

- Dự báo chi tiêu vốn năm 2028 của năm nhà cung cấp dịch vụ đám mây lớn được điều chỉnh tăng lên 1,4 nghìn tỷ USD (năm 2027 là 1,2 nghìn tỷ USD), đầu tư cơ sở hạ tầng AI toàn cầu dự kiến gần 3 nghìn tỷ USD.

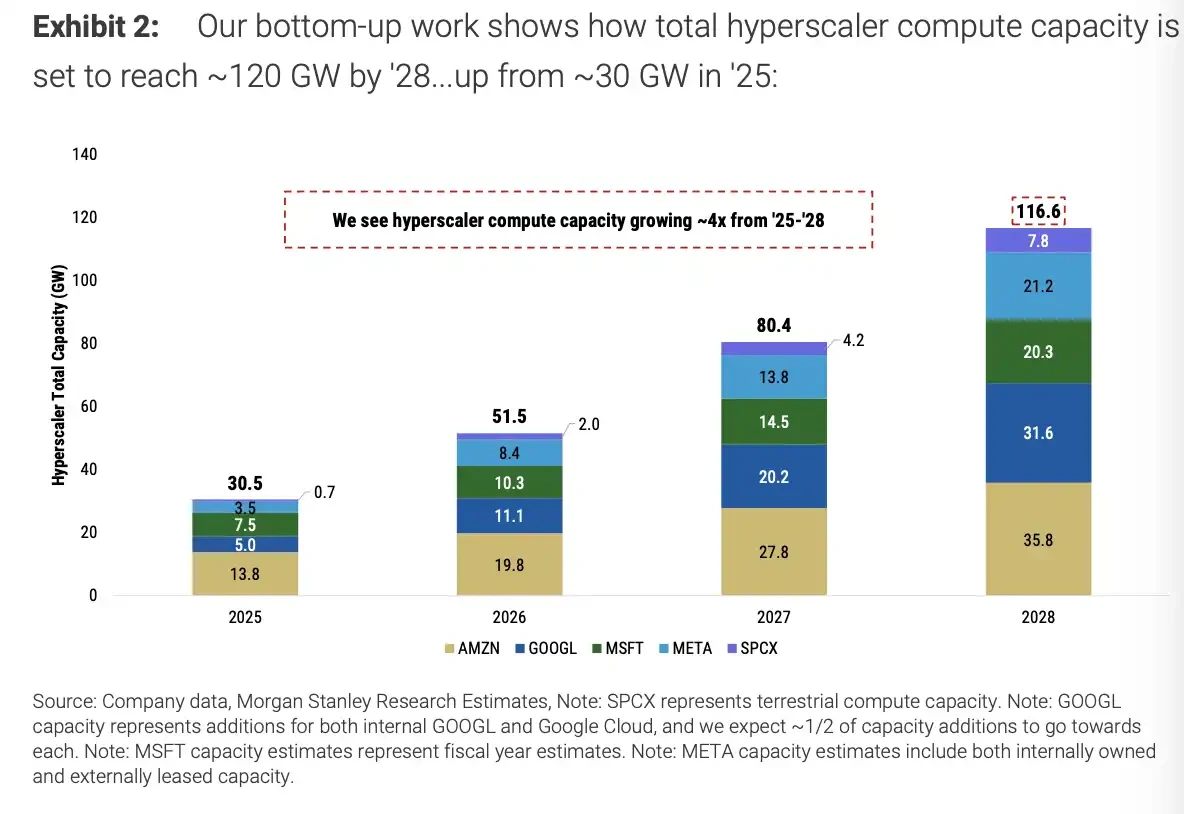

- Công suất tính toán khả dụng dự kiến sẽ tăng từ 30GW vào năm 2025 lên 120GW vào năm 2028, trong đó META tăng lên 21GW, Amazon đạt 35GW.

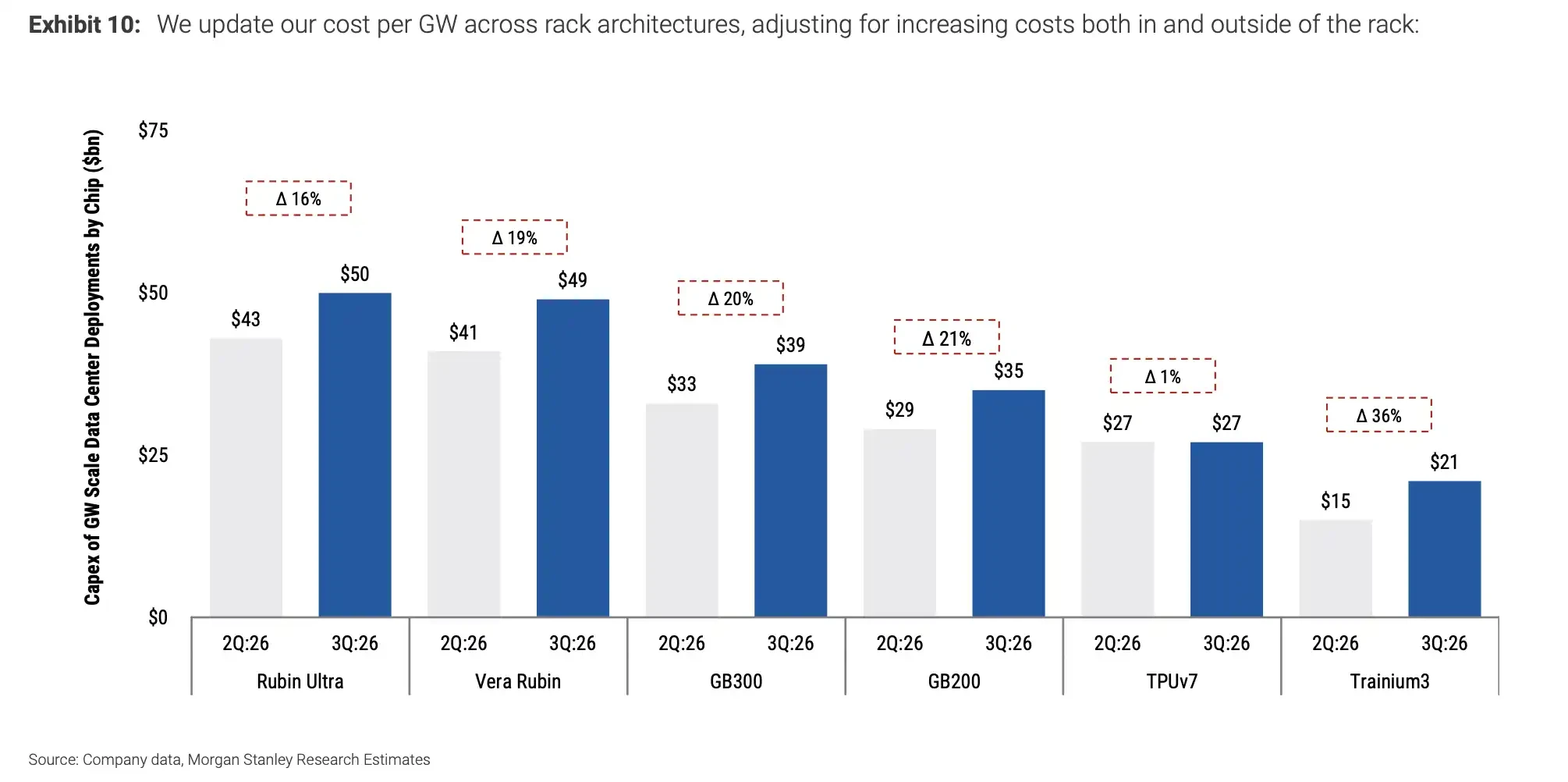

- Chi phí xây dựng mỗi GW tăng cao do chi phí bộ nhớ, điện năng và các chi phí bên ngoài trung tâm dữ liệu tăng, ví dụ chi phí GB200 khoảng 35 tỷ USD, Vera Rubin khoảng 49 tỷ USD.

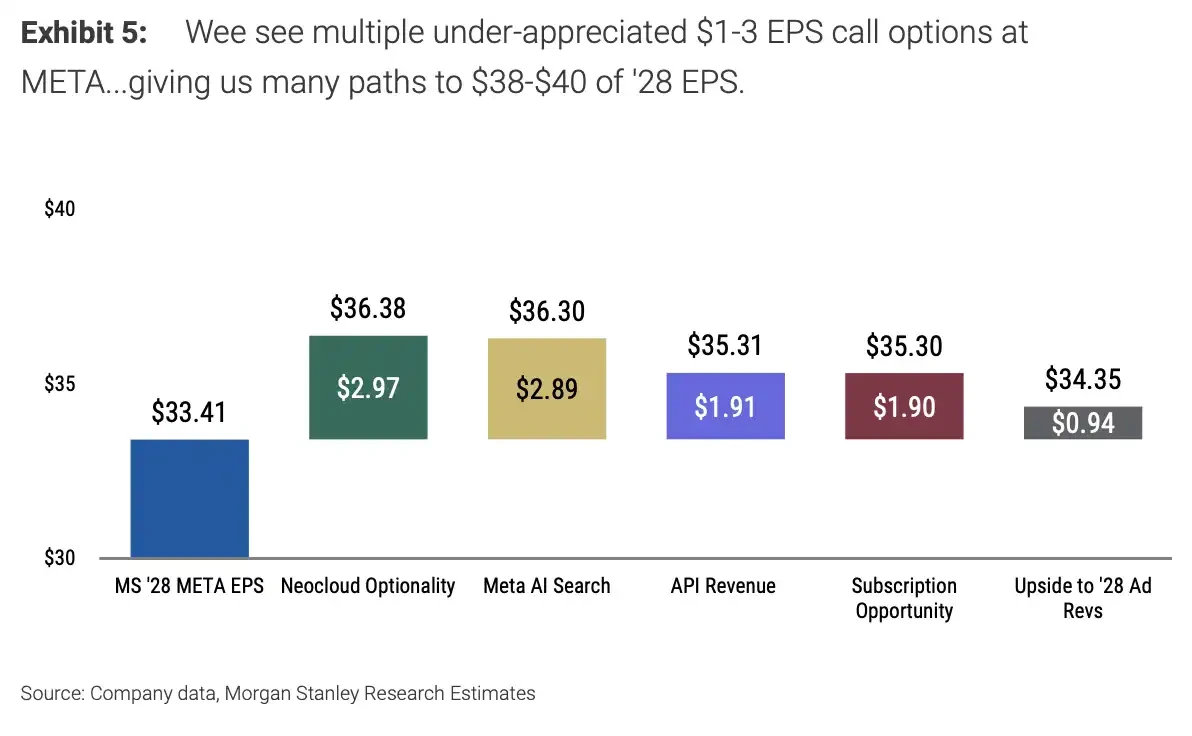

- META được chọn là ưu tiên hàng đầu cho Internet AI, các con đường kiếm tiền từ AI của họ (như API, nâng cấp quảng cáo, đăng ký) dự kiến có thể đóng góp khoảng 10 USD cho EPS năm 2028.

- Trong giả định mô hình kinh doanh API của META, mỗi 100MW công suất GB300 có thể tạo ra khoảng 8,59 tỷ USD doanh thu và 1,91 USD tăng thêm cho EPS, nhưng phụ thuộc vào tỷ lệ sử dụng cao.

- Amazon và Google cũng được hưởng lợi từ chu kỳ chi tiêu vốn, trong đó doanh thu của AWS dự kiến tăng 40% vào năm 2027 và 36% vào năm 2028, Google có thêm công suất mới nhiều nhất.

- Việc triển khai chi tiêu vốn phải đối mặt với ba ràng buộc: nguồn cung (chip, phê duyệt), quy định (chính sách năng lượng) và nhu cầu (sự sẵn lòng chi trả của khách hàng), kiểm chứng doanh thu là thách thức cốt lõi.

TL;DR

- Morgan Stanley's research report estimates that the capital expenditure of the five major hyperscale cloud providers could reach $1.4 trillion by 2028.

- Construction costs per GW are being pushed up by memory, power, and construction, with compute capacity potentially expanding from 30GW to 120GW.

- META is listed as the top pick in AI internet, with a $775 price target contingent on the monetization of API, advertising, and subscriptions.

Morgan Stanley raised its capital expenditure estimates for major hyperscale cloud providers in a sell-side research report, projecting total capital expenditure for the five major platforms to reach $1.2 trillion in 2027 and $1.4 trillion in 2028. The firm continues to list META as the top pick in AI internet, maintaining a $775 price target.

These figures are based on the report's model estimates and do not equate to official company guidance. Publicly available Morgan Stanley materials have already mentioned that global AI-related infrastructure investment could approach $3 trillion by 2028, with data center capital expenditure around $2.9 trillion. The $1.4 trillion figure for the five major platforms is primarily derived from the sell-side's breakdown estimates for major cloud and internet platforms.

The most newsworthy change in this report is the continued upward revision of AI infrastructure spending. By 2028, the model posits that the available compute capacity of major platforms will reach nearly 120GW, approximately four times the 30GW expected in 2025. The construction cost per GW has also been revised upwards, as next-generation platforms like GB200, GB300, and Vera Rubin require more memory, power, racks, and engineering investment.

For investors, the question has shifted from "Will AI giants spend money?" to "How quickly will this spending translate into revenue?" META is positioned at the forefront because it faces higher AI capital expenditure pressures while possessing more direct monetization avenues such as advertising, consumer applications, model APIs, and subscription tools.

$1.4 Trillion in Spending Betting on 120GW of Compute Power

The report raises its capital expenditure expectations for the five major hyperscale cloud providers by 9% and 10% for 2027 and 2028 respectively, bringing them to $1.2 trillion and $1.4 trillion. This scope covers AI infrastructure spending for Amazon, Google, Microsoft, META, and related SPCX entities.

Capacity expansion is a primary driver of the spending increase. In this model, the available compute capacity of major platforms rises from approximately 30GW in 2025 to nearly 120GW by 2028. Amazon is expected to total around 35GW by 2028, Google sees the largest capacity additions in 2027 and 2028, and META increases from roughly 3.5GW at the end of 2025 to 14GW in 2027 and 21GW in 2028.

Capital expenditure forecasts for the five major hyperscale cloud providers, totaling $1.4 trillion in 2028, with upward revisions of 9% and 10% for 2027 and 2028 compared to previous estimates.

Available compute capacity rises from approximately 30GW in 2025 to nearly 120GW by 2028, META grows to 21GW, and Amazon totals around 35GW.

META's capital expenditure estimates require noting definitional differences. In the report's model, META's capital expenditure for 2027 and 2028 is raised to $225 billion and $250 billion respectively. Some public secondary reports citing Morgan Stanley's figures suggest META's total for 2027-2028 is around $380 billion, which may involve different definitions such as total capex, AI infrastructure, gross amounts, or inclusion of off-balance-sheet financing.

These differences do not change the main narrative: AI data center spending continues to pressure free cash flow, depreciation, and near-term EPS, and will determine whether future revenue from cloud, advertising, search, API, and enterprise tools can materialize. Those who can convert more compute power into billable products will find it easier to justify today's capital expenditure.

Cost Per GW Rises, Memory and Power Infrastructure Raise the Bar

The upward revision in spending is not solely due to "building more data centers," but also because "each GW is more expensive."

In the report's bottom-up cost model, the construction cost per GW for GB200 is approximately $35 billion, a 16% increase from previous assumptions. For GB300, it's about $39 billion, a 19% increase. Vera Rubin stands at roughly $49 billion, a 20% increase. Google TPU v7 is around $27 billion, and Amazon Trainium3 is about $21 billion.

Updated deployment costs for GPU and ASIC GW-scale data centers: GB200 around $35 billion, GB300 around $39 billion, Vera Rubin around $49 billion.

Cost pressures come primarily from two areas. The memory component in high-end AI systems continues to increase. Costs related to the data center shell, including power, land, cooling, power distribution, and construction, are also rising. The report assumes these costs increase from roughly $10 million/MW to between $11 million and $19 million/MW.

This is why the expenditure curve for AI giants is unlikely to decline in the short term. While improved chip supply can alleviate some pressure, power access, rack integration, construction, skilled labor, and local permitting will continue to lengthen build-out timelines. Some project timelines could extend to around three years. The larger the capital expenditure, the faster the revenue side needs to demonstrate returns.

META's Focus Shifts to How AI is Monetized

META is listed as the top pick primarily because its AI revenue optionality is more concentrated than that of most internet companies.

The report breaks down META's potential upside from areas like Meta AI search, new cloud services, API revenue, subscription tools, and advertising upgrades, which together could contribute roughly $10 to its 2028 EPS. In the base case scenario, META's 2028 EPS is $33.41. If some of these options materialize, EPS could have further upside.

Cumulative contribution of META's five AI upside options to 2028 EPS. Base EPS is $33.41, with total upside estimated at around $10.

This estimate is not entirely consistent with figures from some public secondary reports, such as "four products or catalysts" or "2028 EPS upside of $1 to $3," and is better viewed as a scenario analysis within this specific report. What ultimately translates to the financial statements depends on product adoption rates, pricing power, and compute utilization.

API is the most direct avenue. Meta announced the public preview of its Meta Model API on July 9th. Third-party information from pricing trackers like Artificial Analysis indicates that the input and output prices for Muse Spark 1.1 API are $1.25 and $4.25 per million tokens, respectively, lower than some leading competitors.

The report's model further assumes that 100MW of GB300 capacity used for APIs corresponds to approximately 53,300 GPUs at 75% utilization. This could generate around $8.59 billion in revenue, $640 million in incremental EBIT, and contribute roughly $1.91 to 2028 EPS. This estimate relies on high utilization and sustained demand; low pricing alone helps attract customers but cannot guarantee profitability.

Subscription tools are another potential avenue. The model assumes that 25% of META's 15 million advertisers pay roughly $200 per month for tools like business agents and coding assistants. This could contribute around $8 billion in revenue and about $2 to 2028 EPS. Whether advertisers will continue to pay ultimately hinges on whether these tools deliver higher conversion rates, lower production costs, or stronger automation capabilities.

Amazon and Google Benefit, But Revenue Validation Must Follow

Amazon and Google are also significant entities in this round of capital expenditure increases, but they serve more as context within this main narrative.

For Amazon, the report raises its AWS revenue growth outlook, projecting 40% and 36% growth in 2027 and 2028 respectively. It also estimates that AWS's backlog increased by approximately $110 billion quarter-over-quarter in Q2, reaching around $475 billion. Since Amazon has not yet released its corresponding official Q2 financial report, this backlog figure should be considered a sell-side forecast. Official documents have confirmed that AWS sales grew 28% year-over-year in Q1 2026, OpenAI added a $100 billion multi-year commitment, and cash capital expenditure continues to rise.

Google's advantage lies in its full-stack capabilities including the Gemini model, TPU, and cloud business. The report's model shows that Google adds the most new capacity among major platforms in 2027 and 2028. A near-term pressure point is that compute resources may still constrain product scaling, especially when search, cloud services, and model APIs compete for compute power simultaneously.

These threads point to the same practical issue: AI spending has entered the trillion-dollar level, and the market will increasingly directly ask "how much revenue does each dollar of capital expenditure generate?" Cloud services, AI search, APIs, advertising tools, and enterprise subscriptions will all be avenues for validating the return on expenditure.

Massive Spending Must Navigate Power, Approvals, and Real Demand

This round of capital expenditure increases has clear boundaries.

The first constraint is supply. Chips, HBM memory, racks, power access, and skilled labor all impact the construction pace. AI data centers must navigate local approvals, grid upgrades, and construction cycles from planning to operation, and cannot be deployed linearly according to model assumptions.

The second constraint is politics and regulation. The large-scale occupation of power, water resources, and land by data centers may face local resistance. Energy policies and local permitting processes could also shift around the 2026 US midterm elections and the November 2028 presidential election.

The third constraint is demand. META's API, subscription, and advertising upgrades remain upside scenarios; revenue realization requires actual customer payments and sustained usage. Lower prices than competitors help attract customers, but long-term profitability depends on usage volume, gross margins, and tool ROI.

The $1.4 trillion capital expenditure paints a picture of a high-cost growth curve. Giants are pre-emptively locking in AI compute power, and the market will continue to ask when this compute power will translate into revenue and profit. META's $775 price target is built on the gradual realization of AI monetization, but the hardest step is converting the EPS upside in the model into cash flow on the financial statements.