Bidding farewell to traditional bull and bear cycles, the market has entered an era of rotating bubbles

- Core Thesis: The current financial market has shifted from the slow, sustained bull and bear market cycles of the past to a "chain storm" market landscape composed of a series of rapidly rotating, interconnected hot sectors. Investors need to move beyond an obsession with a single trend and identify structural changes and cyclical logic from a higher dimension.

- Key Elements:

- Fundamental Shift in Market Structure: Compared to past decades, eight major changes—including the widespread participation of speculative groups, the formation of perpetual buying pressure, the rise of passive investing, and the dominance of multi-strategy funds and high-frequency trading—have collectively shaped the current market environment, and this trend is irreversible.

- Pattern of Market Movement: Market hotspots are like summer thunderstorms, triggered by specific catalysts and going through stages of "dormancy - ignition - narrative - divergence - collapse." Capital flows out of fading hotspots, acting like a wedge of cold air, igniting a new wave of activity in adjacent areas.

- Key Structural Factors: Low transaction costs, price-insensitive passive index investing, concentrated market fragility from uniform risk control in multi-strategy funds, and zero-delay information dissemination amplify sentiment and trends.

- Investor Segmentation: The market primarily benefits two types of investors: industry experts with deep understanding of technological barriers and profit logic, and trend observers who can perceive the behavior patterns of mainstream capital and market sentiment.

- Continuously Rich Future Themes: Upstream and downstream links in AI infrastructure, robotics, cryptocurrency, nuclear fusion, quantum technology, and other fields will continuously serve as potential hotspots, providing ample fuel for rotation.

Original Author: Smac, Partner at Compound VC

Original Compiled by: Saoirse, Foresight News

Editor's Note: As market hotspots emerge in rapid succession, the AI craze is sweeping the scene, leading some to question whether it will repeat the fate of the metaverse hype cycle. Amidst the noisy market conditions, people are often swept away by the current hotspots, losing sight of long-term trends. To make rational judgments, one must learn to elevate their perspective. In this article, Compound VC Partner Smac uses a meteorological analogy to dissect the market logic behind the rotating bubbles.

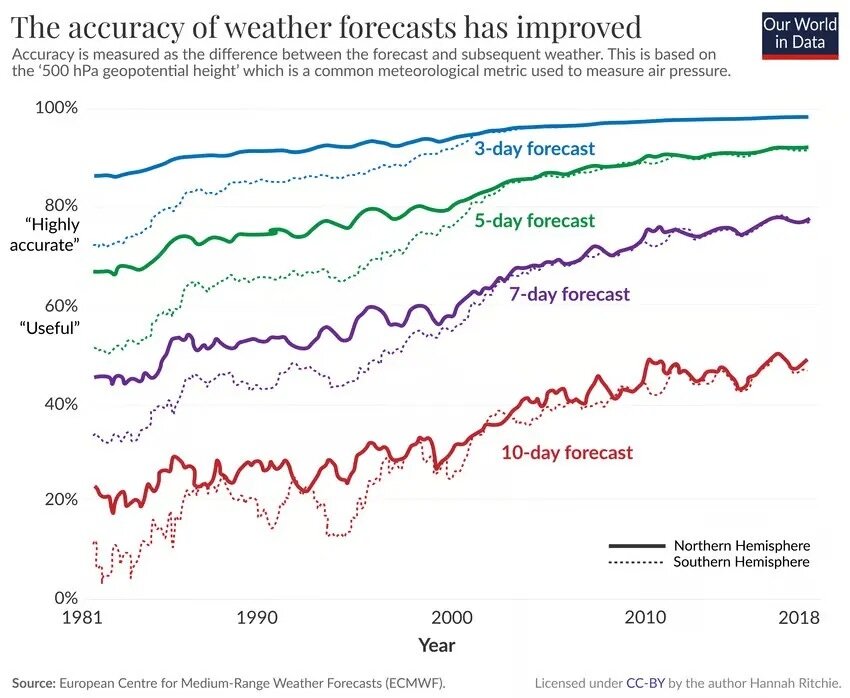

Meteorology is a fascinating field. Over the past fifty years, various weather prediction tools have continuously evolved, and the accuracy of weather forecasts has improved accordingly. Today, a five-day weather forecast is as accurate as a single-day forecast was thirty years ago.

Most people see weather as a single, coherent moving system: clouds roll in, rain falls, the rain stops, and it clears up. Imagine a winter front approaching; the image that likely comes to mind is a massive gray cloud cover spanning hundreds of miles, bringing heavy snowfall. Meteorologists call this type of weather stratiform cloudiness. Simply put, it's like a layered cake; all areas within the cloud cover experience the same weather changes.

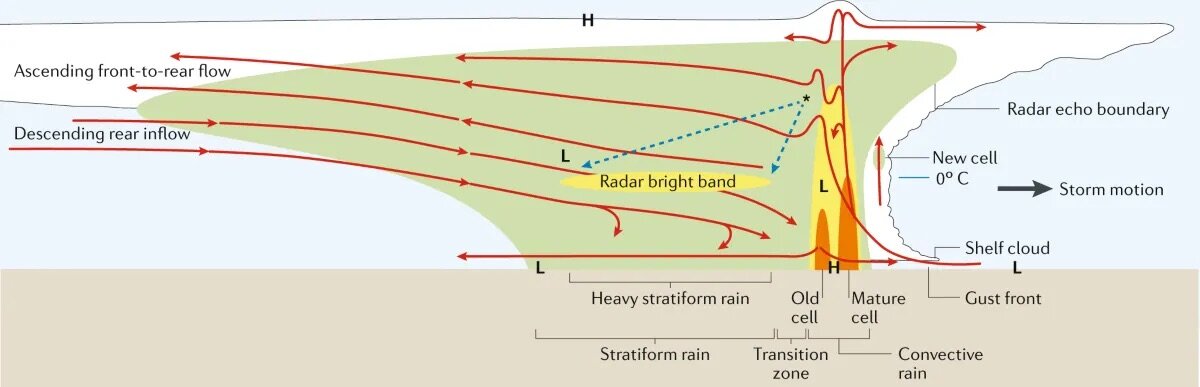

But weather isn't only like this. If you've ever witnessed a summer thunderstorm on the plains, you'll know it operates very differently. First, individual convective clouds form: warm, moist air near the ground rises, meets cold air at higher altitudes, water vapor condenses, and towering local cumulonimbus clouds develop. Within an hour, hail, lightning, and torrential rain arrive, reducing visibility to less than a hundred meters.

After the cloud cluster reaches its peak, it releases all its energy and gradually dissipates. The cold air from the storm's downdraft spreads outward at speeds of up to 40 miles per hour. When this cold air collides with the surrounding warm, moist air that hasn't yet formed storms, it acts like a wedge, once again pushing the warm air upward.

As long as the atmosphere has sufficient instability, this "cold air wedge" will spawn new convective cloud clusters about a dozen miles from the original storm.

This new cloud cluster couldn't form on its own. Although energy was already stored in the atmosphere, it lacked a trigger, which the dissipating storm provided. Subsequently, the new cloud cluster will repeat the evolution process of the previous storm.

When multiple convective cloud clusters form in succession, they constitute a mesoscale convective system. For someone on the ground, they will only encounter each storm individually; each storm feels like the entirety of the weather system. On one side, it's calm, and people are unaware of the impending rain and wind; on the other side, the storm has already passed. But from a satellite's perspective, you can see a line of independent cloud clusters connected, each at a different stage of development, moving forward until they exhaust the warm, moist air along their path.

A supercell thunderstorm cloud near Amistad, New Mexico, at sunset

This system of successive storms has different formation conditions than a single weather front. It depends on a specific atmospheric environment:

- Warm, moist air near the surface, which acts as the "fuel" for the storms;

- Dry, cold air at high altitudes, which drives the continuous upward movement of warm air, creating atmospheric instability;

- Varying wind directions at different altitudes, which cause the storms to rotate and move laterally, known as wind shear.

When these three conditions are met simultaneously, successive storms will occur one after another.

After all this talk about meteorology, let's get back to the point: The meteorological phenomenon described above is almost identical to the current state of the financial market.

The market of the past was like a stratiform weather system: a bull market and a bear market would alternate, sector trends would rotate slowly, and each cycle would last for years. The long bull market from 1982 to 2000 was followed by the dot-com bubble, and then the real estate and credit cycle from 2003 to 2007. These market cycles were long and clear-cut. Even if investors were off by a few years in timing, as long as they understood the major trends, they could still profit in the end.

But today's market is no longer what it used to be. We are in a chain-reaction convective storm market: individual hotspots are like successive storms, and anyone caught in one feels that this particular trend is unstoppable and all-encompassing.

Capital flows out of themes that have lost their heat, in turn spawning new trends in adjacent areas. The pace of sector rotation has accelerated dramatically: AI infrastructure, GLP-1s (a class of diabetes drugs popular for their weight loss effects, now a hot investment track in capital markets), stablecoins, quantum technology, nuclear energy, distributed autonomous technology, robotics, aerospace... Each track will experience a complete cycle of enthusiasm, have its own loyal participants, go through a full narrative cycle, and inevitably face a downturn. The "cold air" spreading after the previous trend fades will then ignite the next hotspot in a new area.

Refusing to acknowledge that the current market has fundamentally changed is self-deception. People like to joke about "this time is different," but deliberately ignoring the permanent shift in the financial market environment is either lazy thinking or stubbornly living in a fantasy of the old market.

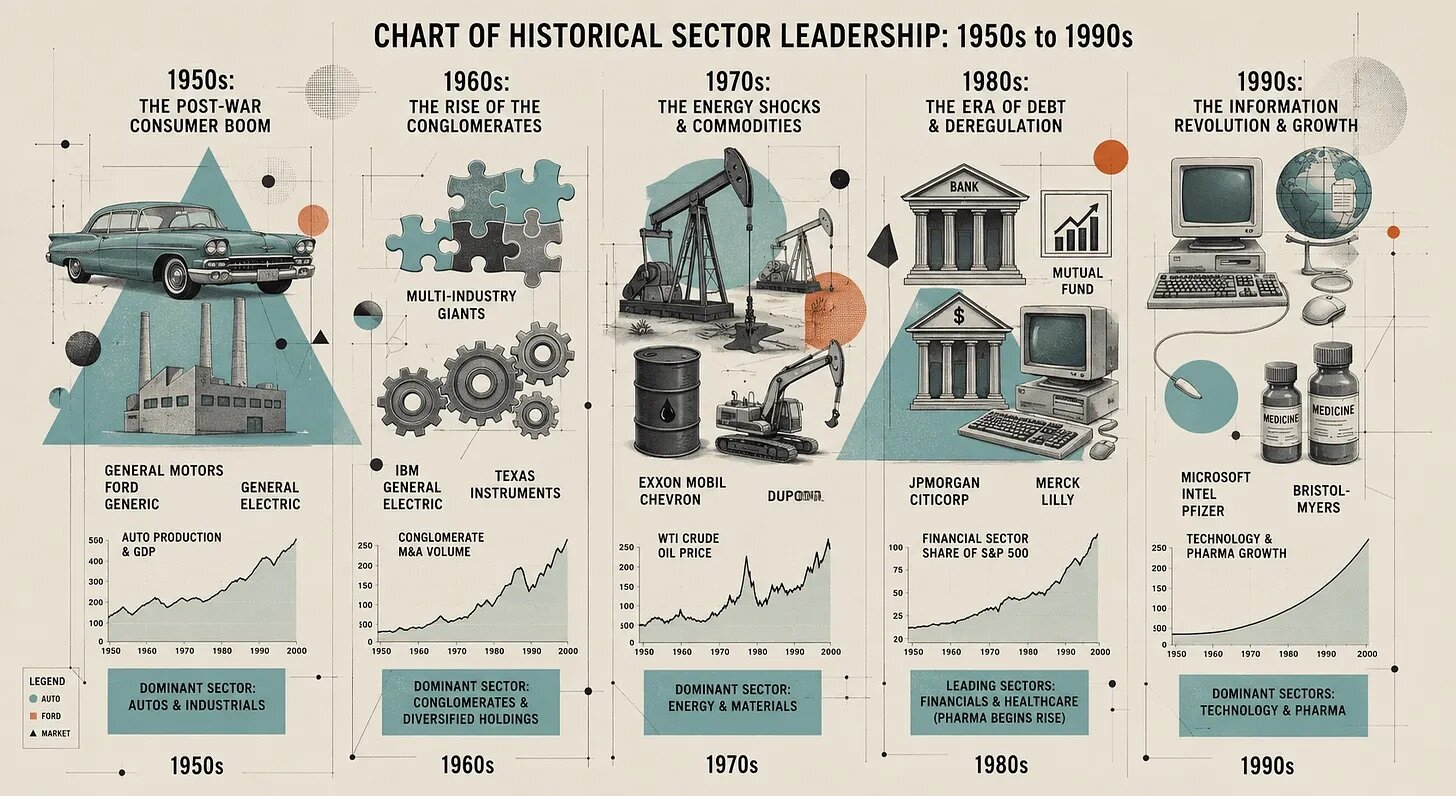

A Market Landscape Unlike the Past

For a long time after World War II, the pace of the financial market resembled that of a slow-moving weather system. A bull market could last ten, fifteen, or even twenty years, and sector rotation always revolved around long-term megatrends.

Approximate timeline of industry themes and leading sectors

Back then, sector shifts occurred within a unified macro-environment. It only took landmark era-defining turning points, like the collapse of the Bretton Woods system, Volcker's anti-inflation policies, the peak of the dot-com bubble, or the global financial crisis, to completely overturn the market structure.

This market form arose from numerous structural factors: high transaction costs in the past kept retail participation extremely low, forcing long-term holding habits; pensions were the main vehicle for retirement assets; the S&P 500 was dominated by manufacturing, energy, banking, and retail companies, whose profit growth was roughly in sync with the broader economy, making their trends stable and predictable. At the same time, information spread slowly; after an annual report was released, most investors might not learn its contents for weeks.

Market volatility in the past was also relatively balanced. A bull market would be followed by a deep correction, a gradual deleveraging process, and a long adjustment period; rebounds in a bear market were also gradual. The market would linger in different emotional zones for extended periods, and overall structural shifts often took quarters or years.

Using the meteorological analogy: The old market had moderate fuel, high atmospheric stability, and weak wind shear, leading to long, stable trends that allowed investors to plan calmly. Today, all environmental conditions have changed; some have even reversed completely, leading to a fundamental transformation of the market structure.

Where Did the Change Come From?

Many changes intertwine and amplify each other, and each one alone would be enough to reshape the entire market. In summary, there are eight core shifts:

- Democratization of the Speculative Class

- Formation of Perpetual Bid

- Passive Investing Creates Inelastic Counterparties

- Rise of Multi-Strategy Funds and HFT, Disappearance of Market Intermediaries

- Volatility Artificially Suppressed

- Fundamental Change in Index Composition

- Complete Elimination of Information Delay

- Shift in Fiscal and Monetary Environment

Democratization of the Speculative Class

The participants in today's market have visibly changed. In the 1990s, retail trading volume accounted for only 10% of total US stock market turnover. Due to high commissions, most retail investors held stocks for the long term, and active speculation was rare.

Robinhood pioneered zero-commission trading and the payment for order flow model; in the fall of 2019, Schwab followed suit by eliminating trading commissions, with Fidelity, TD Ameritrade, E*Trade, and others quickly doing the same, completely rewriting the industry rules.

The COVID-19 pandemic further accelerated this trend: with stimulus checks distributed, people stuck at home, and mobile trading apps deliberately gamifying trading, retail trading volume share surged to 25% from 2020 to 2021. Many thought this was a short-term phenomenon, but high retail participation has persisted. On April 29, 2025, during significant market volatility triggered by tariff policies, JPMorgan data showed that the share of retail order flow hit an all-time high of 48%. On regular trading days, retail volume is more than double pre-pandemic levels; during major market swings, this ratio can reach up to 35%.

A deeper change lies in what retail investors are trading. Single-stock options have become a mainstream choice for retail investors, and zero-days-to-expiry (0DTE) options have exploded. Newer participants are predominantly younger, hold highly concentrated portfolios, and trade based on market narratives. Crucially, these investors often use special methods to leverage (leverage that doesn't show up in conventional margin data), their trading decisions follow price action rather than fundamentals, and they are highly susceptible to following others.

In meteorological terms: Today, the "warm, moist air" near the market's surface is more abundant than ever, with potential energy stored at historic highs.

Formation of Perpetual Bid

I have written about this before. In short, the US retirement security system has shifted from defined-benefit pensions to defined-contribution plans. Now, individuals must plan their own retirement finances. On the market level, this means that every pay cycle, a massive, price-inelastic, passive inflow of capital buys stocks, creating an automated perpetual bid.

The logic of traditional pensions was completely different: defined-benefit plans needed to manage duration risk against liabilities. Managers would actively assess market valuations; if they thought stocks were too expensive, they would adjust asset allocation and increase bond holdings. Even if their rebalancing was slow, it was far more active than today's purely passive perpetual bid.

This is crucial: The marginal trading capital in the market has a much greater impact on prices than before.

Passive Investing Creates Inelastic Counterparties

The essence of passive index investing is to buy and sell strictly according to index weights, regardless of price. The higher a stock's market cap, the more passive capital flows into it, and vice versa. This mechanism embeds momentum effects into the market's underlying logic: the stronger the trend of an asset, the more passive capital it attracts. The strong performance of the Magnificent Seven tech stocks in the US is largely attributed to this.

For years, much has been written about the concentration of index weights towards top companies. Of course, these top companies also have strong profitability and growth, so the concentration isn't entirely baseless. But the core issue is that passive capital has no natural "take-profit switch."

Rise of Multi-Strategy Funds and HFT, Disappearance of Market Intermediaries

Alongside the formation of perpetual passive bid, the active trading landscape has also undergone a massive transformation, marked by the rise of multi-strategy portfolio trading firms. Institutions like Citadel, Millennium, Point72, and Balyasny aggregate hundreds of independent portfolio managers, each responsible for a specific trading strategy, all under strict risk constraints. The assets under management of these firms have exploded, with capital concentrating towards the top, mirroring the concentration trend in stock indices.

Simultaneously, high-frequency trading now accounts for 50%-60% of US stock market volume and up to 75% in futures markets. This combination creates a highly fragile market environment: firms trade against each other, weakening the market's price discovery function. A significant portion of the volume on the tape is simply capital circulating within the market itself.

Under normal conditions, bid-ask spreads are very tight, which is good. But once a narrative breaks, market positioning becomes extremely imbalanced, or the risk limits of multiple firms are triggered simultaneously, the market microstructure can break down instantly. The risk exposures of all these portfolio managers are highly correlated, and their stop-loss rules are largely similar. When one firm is forced to deleverage, the others follow suit. The market crashes in February 2018, August 2019, March 2020, and August 2024 are classic examples. The market structure that breeds these crashes is now deeply entrenched and will repeat itself.

Traditional fundamental long/short hedge funds are being squeezed out: these funds rely on deep research to pick stocks, hold 20 to 40 names, and have investment horizons of several quarters. Today, such firms are either absorbed by large asset management platforms or move into private markets, family offices, or single-strategy funds. In my view, significant alpha can still be found by understanding the logic of rotation and maintaining patience amidst short-term capital flows.

Volatility Artificially Suppressed

Given the above four points, the current volatility trend is not hard to understand. Data shows that since 1990, the VIX has closed below 20 on two-thirds of all trading days; the day-to-day correlation of volatility is as high as 85%, meaning today's level largely continues yesterday's.

But the pattern of volatility switching has become extreme and unbalanced: a large body of research shows that once chronically suppressed volatility breaks a critical point, it explodes violently within just a few days; the process of volatility falling back, however, is very slow, often taking weeks.

There are multiple structural reasons: the market has spawned a massive "short volatility" industry. The prevalence of 0DTE options further suppresses intraday volatility through dealer hedging. The market remains in a low-volatility calm state for long periods, allowing risk to accumulate; when tail risk hits, all participants flee collectively.

Simply put, today's volatility distribution is increasingly skewed: long periods of low volatility build up energy, ultimately leading to a much more violent release of risk.

Fundamental Change in Index Composition

The sixth change is the composition of the stock indices themselves. In 1980, the S&P 500 was dominated by manufacturing companies; industrials, materials, energy, financials, and consumer staples were predominant. The earnings growth of these companies roughly tracked GDP, with smooth growth curves and valuation multiples that mean-reverted around a reasonable center. Even forecasting Procter & Gamble's earnings five years out wasn't subject to huge errors.

That situation is long gone. Today, Information Technology, Communication Services, plus tech-heavy Consumer Discretionary companies like Amazon and Tesla, collectively account for over 40% of the S&P 500's weight. The business models of these companies are no longer linear: the marginal cost of distributing software is near zero; and the AI track is full of uncertainty — opinions are deeply divided on whether AI labs will become the most critical infrastructure of the next half-century or money-burning black holes.

For such companies, estimating short-term earnings is difficult enough, and long-term value is even more volatile, causing valuation multiples to swing wildly. Company valuations no longer rely solely on financial statements; market narratives have become a core influencing factor. For investors who can anticipate the direction of frontier technology, understand competitive moats, and identify emerging markets, there is a wealth of alpha opportunities here.

Traditional manufacturing companies expand capacity gradually, their discounted cash flow models yield relatively stable results, and valuation multiples revert to the mean more easily. Today, a company's valuation depends heavily on the market's acceptance of its growth story. I am not saying traditional valuation frameworks are obsolete; this is simply the objective reality of today's new types of companies.

Today's mainstream indices are filled with these long-duration, narrative-driven companies. Steeper atmospheric temperature gradients store more energy; similarly, the more such companies there are, the greater the potential kinetic energy stored in the market, and once a trigger appears, market fluctuations will be even more violent.

Complete Elimination of Information Delay

Everyone can intuitively feel this, but its impact is often underestimated. For most of financial history, the dissemination of market-relevant information was restricted by distribution channels. Today, information spreads with virtually zero delay.

Position information, in particular, spreads much faster than ever. Investors can see in real time how well-known figures react to news, and more and more people proactively disclose their holdings. A deluge of real-time information constantly fosters comparison, profit screenshots are everywhere, stories of "turning a thousand dollars into millions" go viral regularly, and the anxiety of missing out is continually fanned.

Shift in Fiscal and Monetary Environment

This point doesn't need much elaboration, summarized as follows:

- US monetary policy has been persistently loose, with real interest rates staying low;

- Quantitative easing has continuously expanded the Fed's balance sheet;

- Low discount rates inflate the prices