Kelp DAO bảo vệ được khoản nợ xấu 400 triệu USD, nhưng Aave đã phải trả giá 12 tỷ USD

- Quan điểm cốt lõi: Mặc dù Aave đã hoàn tất việc bù đắp tài sản sau sự cố rsETH, nhưng phải đối mặt với ba thách thức lớn: sự sụt giảm hơn 12 tỷ USD TVL, tranh chấp pháp lý đang chờ xét xử tại Tòa án New York và sự suy yếu nội bộ trong quản trị. Tăng trưởng tương lai của nó phụ thuộc vào tính mở cho các trường hợp dị thể của V4 và định hướng tổ chức RWA của Horizon, nhưng cả hai hướng đi này đều bị giới hạn bởi nhịp độ bên ngoài và chính trị nội bộ, khó có thể khôi phục niềm tin thị trường trong ngắn hạn.

- Các yếu tố chính:

- Sau sự cố rsETH, TVL của Aave đã giảm từ 26,396 tỷ USD vào ngày 18 tháng 4 xuống còn 14,181 tỷ USD vào ngày 25 tháng 5, thiệt hại hơn 12 tỷ USD.

- Tòa án Quận phía Nam New York sẽ mở phiên xét xử vào ngày 5 tháng 6 về quyền sở hữu 30.766 ETH bị Ủy ban An ninh Arbitrum đóng băng, Aave phải đối mặt với các vụ kiện pháp lý và tiêu hao thương hiệu.

- DeFi United đã huy động nhiều bên cùng lúc cung cấp hỗ trợ tài chính cho Aave, nhưng cộng đồng đã làm cạn kiệt khả năng ứng phó khẩn cấp và không thể tái tạo quy mô bảo lãnh tương tự.

- Các cá voi như Justin Sun đã rút khoảng 174 triệu USD từ Aave chuyển sang Spark, xu hướng dịch chuyển vốn rõ ràng, giao thức đã mất đi lòng tin của các khách hàng lớn.

- Tăng trưởng tiền gửi sau khi ra mắt V4 rất chậm (đạt 86,13 triệu USD vào ngày 26 tháng 5), và bộ phận quản trị bị suy yếu nội bộ do các đề xuất bỏ phiếu gộp, ảnh hưởng đến tốc độ hiện thực hóa tính mở.

- Phiên bản V3 được cấp phép của Horizon tập trung vào RWA tổ chức, tính đến ngày 26 tháng 5 đã tích lũy hơn 500 triệu USD tiền gửi ròng, với các đối tác bao gồm BlackRock, nhưng tăng trưởng bị hạn chế bởi tốc độ kết nối tài chính truyền thống.

- Các đối thủ cạnh tranh Morpho và Spark đã phục hồi TVL sau sự cố rsETH, giành lấy lưu lượng cho vay bị mất của Aave, tạo ra một cục diện cạnh tranh dài hạn.

Original Author: Sanqing, Foresight News

On May 26, Kelp DAO transferred the final batch of 20,373.72 rsETH to the LayerZero OFT Adapter, and Aave simultaneously announced that rsETH and all affected markets had returned to normal. In 37 days, all 116,500 rsETH had been fully replenished.

However, this only means rsETH has regained its 1:1 backing; it does not mean Aave's books are fully cleared. The 30,766 ETH frozen by the Arbitrum Security Council remains stuck in the U.S. District Court for the Southern District of New York, with ownership still undetermined. Aave's lost TVL cannot simply return along with the rsETH.

The Bill Extends Beyond the TVL Column

According to DefiLlama data, on the day of the incident, April 18, Aave's TVL was $26.396 billion; by May 25, it was $14.181 billion. The funds that hadn't returned after a month amount to over $12 billion.

More challenging issues lie ahead. The U.S. District Court for the Southern District of New York will hold a hearing on June 5 regarding the ownership of the 30,766 ETH frozen by the Arbitrum Security Council. Aave LLC and Gerstein Harrow submitted supplementary briefs before May 22. The judge had previously modified the restraining notice on May 8 to allow fund transfers, but the substantive ruling is still pending the June 5 determination.

Gerstein Harrow represents the families of victims of North Korean terrorism and holds an unsatisfied judgment of $877 million. Regardless of the outcome, this lawsuit is a drain on the Aave brand.

DeFi United was able to materialize this time because multiple parties were willing to step in: Stani Kulechov contributed 5,000 ETH personally, Consensys and Joseph Lubin pledged up to 30,000 ETH, the Aave treasury allocated up to 25,000 ETH, supplemented by a credit line of up to 30,000 ETH from Mantle and support from Lido, Ether.fi, and others.

This was an unprecedented community mobilization, but Aave has used up its one-time-only card. In the event of another upstream contagion incident, it may not be possible to assemble the same list of supporters again.

For example, after the incident, Justin Sun withdrew approximately $174 million (including 65,854 ETH and some stablecoins) from Aave to Spark, bringing his total deposits on Spark to over $1.3 billion. Whales are voting with their feet, and capital has already migrated.

V4's Openness is Being Slowed by Governance

Aave doesn't only have V4 as its counter-punch, but V4 is the most crucial one.

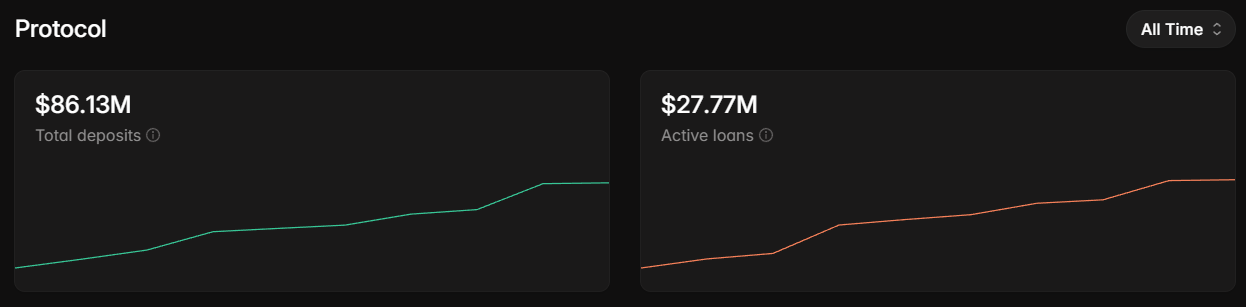

V4 went live on the Ethereum mainnet on March 30, featuring a Hub-and-Spoke architecture with three initial Liquidity Hubs. Aave Labs promised "security-first growth," with deposit limits gradually increasing. It surpassed $10 million in deposits on April 8, crossed $50 million on May 9, and by May 26, total deposits were $86.13 million, with active borrowing positions at $27.77 million.

This cadence was a responsible design choice before the rsETH incident but turned into a stress test afterward. Aave is simultaneously managing a $200 million bad debt on V3 while slowly opening up limits on V4.

The more thorny issue is that V4 also faces internal friction within its own governance layer. In February 2026, Aave Labs submitted a strategic proposal bundling product revenue, service provider incentives, the V4 growth engine, and brand legal custody, requiring delegates to vote on four different risk dimensions at once.

Aave Chan Initiative founder Marc Zeller publicly questioned the appropriateness of bundling a massive fund request with strategic approvals. This governance dispute simmered before and after the V4 launch, and every delay allows competitors to eat into Aave's market share.

V4's advantage lies in the openness of its Spoke design; anyone can build a Spoke, and if it meets the criteria, it can connect to a Liquidity Hub as a credit line. This is why Babylon Labs chose to integrate Trustless Bitcoin Vaults into V4 instead of other platforms. However, the speed at which this openness materializes depends on whether the governance layer can keep pace.

More Than Just V4: Aave is Fighting Three Battles

Aave V3 remains the cash cow. It generates over $100 million in annualized revenue, and the bulk of its $14.1 billion TVL resides on V3. The "Aave will win" proposal positions V3 in a "stable maintenance" phase, with Stani publicly committing that there is no forced migration and no deadline.

V4 and V3 will run in parallel for at least 24 to 36 months. V4 acts as an additive layer, catering to heterogeneous use cases that V3 cannot handle. Horizon, on the other hand, is an independent permissioned fork of V3, specifically designed to serve institutional RWA.

Each of these three layers captures different incremental growth. V4 targets new scenarios beyond V3's risk framework. Post-rsETH, it also has the added task of providing a reason for funds that migrated to Morpho and Spark to return to Aave. Horizon targets RWA flows from traditional finance, operating in a completely separate pool from V3 and V4.

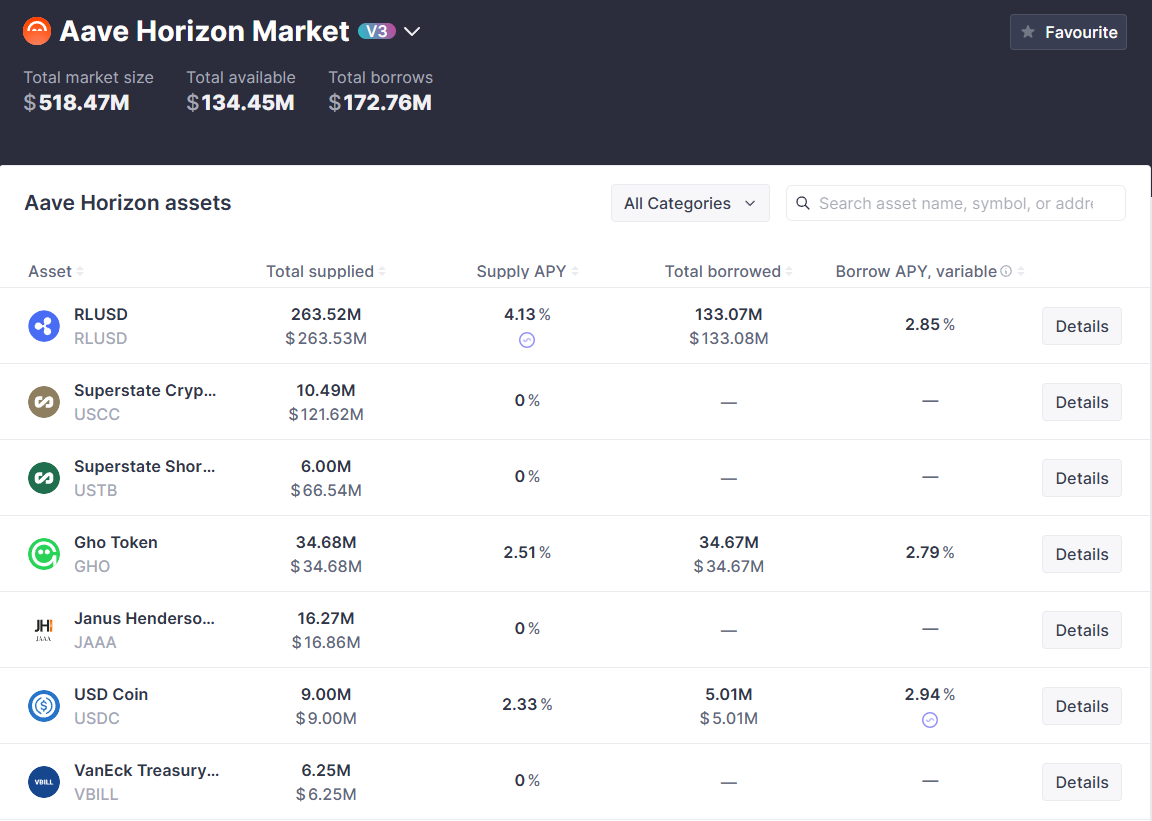

The Horizon Market officially launched in August 2025. It is a permissioned V3 instance deployed by Aave, specifically allowing institutions to use tokenized treasuries, corporate bonds, and money market funds as collateral to borrow stablecoins like USDC, GHO, and RLUSD.

As of May 26, it has accumulated over $500 million in net deposits, with a target of surpassing $1 billion by the end of 2026. Partners include BlackRock, Franklin Templeton, Circle, Ripple, and VanEck.

This route diverges from Morpho's vault management model. Morpho uses third-party curators like Steakhouse and Gauntlet to curate vaults that capture lending flows from retail institutions like Coinbase. Aave, through Horizon, directly connects with asset managers in traditional finance to capture RWA.

These two approaches target different institutional client profiles. Morpho serves fintech companies that use on-chain lending as a tool, while Aave serves asset managers who view the blockchain as a venue for issuance.

The capital migration following the rsETH incident primarily impacted the first type of client. The migration cost for the second type of client is higher, and their reaction is slower. The compliance framework, KYC processes, and asset admission audits that Aave has built in Horizon are things Morpho cannot replicate quickly in the short term following the incident.

This is the only incremental growth line for Aave that was not directly impacted by the rsETH incident, but its growth depends on the pace at which traditional finance integrates with DeFi.

There Won't Be a Second DeFi United

Aave remains the largest protocol in the lending market. Its TVL of $14.1 billion is still nearly double that of Morpho, and the deep deployment breadth accumulated over the years is something no one can catch up with in the short term.

But the bill from rsETH is not on the balance sheet; it's in the column of institutional default preference for lending protocols. Spark's TVL rose from $3.727 billion to $5.3 billion in one month. Morpho bottomed out on April 21 and slowly climbed back to pre-incident levels. These numbers will not automatically reverse direction just because Aave's market has recovered.

The speed at which V4 delivers on heterogeneous use cases, combined with the progress of Horizon in institutional RWA, will determine whether Aave can win back the lost market share. However, the former is hampered by governance internal friction, and the latter is constrained by the pace of traditional finance's own integration timeline. And for both of these, Aave can only wait.

DeFi United was not a permanent institution; it was a one-time mobilization.