Are prediction markets a money tree? An in-depth analysis of their profit model

- Core thesis: The core of the prediction market business model is not simply charging fees for market access. Instead, it transforms market disagreements into trading demand, using a differentiated taker fee mechanism to convert proactive trades into stable platform revenue. Polymarket's success validates the shift from a "traffic narrative" to "systematic revenue validation."

- Key elements:

- The essence of the profit model is "turning disagreement into Fees": The closer the price is to 50/50, the greater the market disagreement, the stronger the trading impulse, and the higher the platform's fee revenue. Conversely, when outcomes are certain, information value is high, but fee contribution is low.

- Major platforms have significantly differentiated fee structures: Polymarket uses vertical-specific pricing (Crypto rate 0.07) and divergence-based pricing (p×(1-p)); Kalshi adopts a model closer to regulated exchanges; Opinion emphasizes a complex discount system and user segmentation; Predict.fun uses a flat 2% fee.

- Polymarket's commercialization timeline and key milestones: Fees were first introduced in the Crypto vertical in January 2026, expanded to Sports in February, and after full-scale fee implementation in March, demonstrated significant revenue generation potential, with 7D Fees reaching $9.27 million.

- Trading volume does not equal actual profit: While the Sports vertical has the highest 7D volume ($401 million), its estimated fees ($3.31 million) are lower than Crypto ($4.39 million). This is because Crypto has a higher market order ratio (75%) and fee rate (0.07) compared to Sports (60% and 0.03).

- The true moat for prediction markets lies in "sustained pricing power": The core capability is not discovering hot topics, but transforming them into markets with depth and trading frequency, making prices a signal that can be referenced externally.

Original authors: Changan, Amelia, Biteye Content Team

In the past, discussions about prediction markets focused on whether they were accurate, had high trading volume, or could become a new type of information market. But when prediction markets become a business, the core question changes: what is the profit model of a prediction market?

In the business world, high trading volume does not necessarily mean the platform is making money. An event market can generate huge buzz, and users can trade frequently. However, if most transactions cannot be monetized through fees, or if activity is purely sustained by subsidies and points, then volume is just a nice-looking number, not a healthy revenue stream.

For prediction markets, the real test of business acumen is not "how many markets were created" or "how popular a particular event is," but whether the platform can seamlessly connect three things:

- The impulse for real transactions;

- Maintaining sufficiently deep order book liquidity;

- Converting aggressive order-taking demand (Taker) into fees.

This is why the business model of prediction markets is far from a simple "tax on opening a market." On the surface, it's just a YES/NO gambling game, but what truly supports the platform's revenue base is the underlying transaction structure, liquidity mechanisms, fee structures, and user behavior.

Especially since the leading platform Polymarket systematically introduced Taker Fees, the narrative for prediction markets has shifted from being "information tools" to entering a "revenue validation" phase.

This article will deeply analyze the underlying mechanics of prediction markets from a business perspective:

- How do prediction market platforms make money?

- Why does the Maker/Taker dynamic determine the survival of a platform?

- What are the fundamental differences in fee structures among mainstream platforms like @Polymarket, Kalshi, @opinionlabsxyz, and @predictdotfun?

- Why are the highest-volume sectors not necessarily the most profitable sectors?

💡Core Conclusion: Prediction markets don't sell answers; they sell disagreement.

The closer the price is to 50/50, the greater the market disagreement, the stronger the trading impulse, and the easier it is for the platform to generate fee revenue from aggressive trades. The closer the price is to 0 or 100, the more certain the outcome. While the information value still exists, the fee contribution significantly decreases.

Therefore, the true business moat for a prediction market is not turning "events" into markets, but turning "disagreement" into trades, and then steadily converting those trades into revenue.

I. How Prediction Markets Make Money: Not by Opening Markets, But by Turning Disagreement into Fees

To deconstruct the cash flow of a prediction market, one must first clarify the four core drivers of its revenue. They are intertwined, forming a closed loop from traffic to monetization.

1️⃣ Trading Fees - Direct Revenue Source

Most prediction markets charge the party that initiates an aggressive trade, i.e., the Taker. This is because the Taker consumes liquidity, while the Maker provides it.

This means that not every trade on a prediction market generates revenue. The trades that truly contribute fees are those where users are willing to trade aggressively, paying for speed and certainty of execution.

2️⃣ Liquidity - Foundation for Sustainable Trading

The hardest part of a prediction market isn't opening the event, but ensuring that event has depth.

If no one places limit orders, users can't buy or sell when they want. Even if the market is a hot topic, it's difficult to form an effective price.

Therefore, many platforms reduce the cost for Makers or even provide incentives for them.

This isn't a direct "revenue source," but it determines whether trading fees can exist in the long run.

Without liquidity, there is no sustained trading, and fee revenue naturally cannot be stable.

3️⃣ Information Value - Mindshare Capture

What differentiates prediction markets from traditional trading platforms is that they aren't just trading tools; they also produce information.

When an event market has sufficient trading volume and liquidity, its price becomes a probabilistic signal. Media outlets cite it, KOLs interpret it, traders monitor it, and average users use it to gauge market sentiment.

This may not directly translate into trading fees, but it brings attention, user mindshare, and external virality to the platform. Over the long term, this information value reinforces trading demand.

4️⃣ User Operations and Discount Systems - Converting Activity into Revenue

Beyond basic trading fees, different platforms also use discounts, referrals, campaigns, points, and rebates to increase trading frequency. While these measures may not directly generate income, they impact the platform's long-term monetization ability. For example, Opinion offers user discounts, trading discounts, and referral discounts; Predict.fun employs a simpler base fee and discount mechanism; Polymarket focuses on differentiated fees across sectors and Maker rebates. The essence of discounts and incentives is not merely subsidization; it involves sacrificing some profit to retain users, gradually converting their activity into revenue.

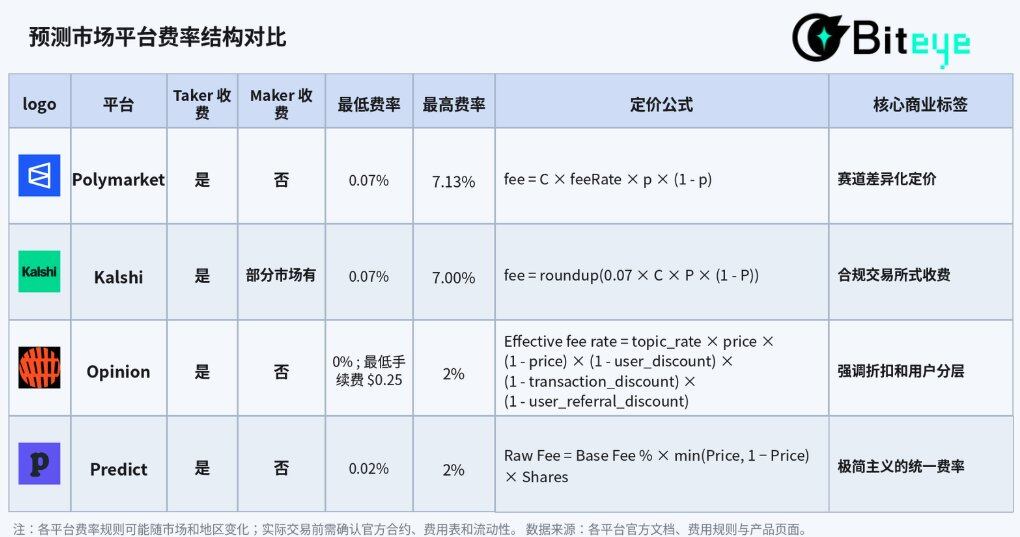

II. Horizontal Comparison of Fee Structures Among Mainstream Prediction Market Platforms

Looking at the fee designs of several mainstream prediction markets, the strategic direction of the industry is highly convergent: encourage limit orders to provide liquidity and convert aggressive trades into revenue. However, in tactical execution, platforms show clear strategic divergence based on their positioning.

1️⃣ Polymarket: Refined Pricing by Sector

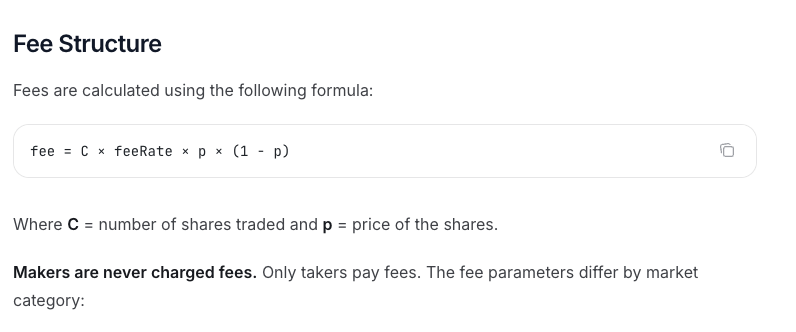

Polymarket's Taker fee logic combines "sector differentiation" and "disagreement-based pricing" to the extreme. Its official core formula is:

fee = C × feeRate × p × (1 - p)

Where C is the number of shares traded, p is the trade price, and feeRate is determined by the market sector.

This mechanism involves two core variables:

- Sector Refinement: Based on current confirmed fee rates, the Crypto sector has a feeRate of 0.07, Sports is 0.03, Politics/Finance/Tech is 0.04, Culture/Weather is 0.05, and some Geopolitics markets have a rate of 0. This means Polymarket doesn't charge uniformly across all markets but uses differentiated rates based on each sector's trading frequency, sensitivity, and user willingness to pay.

- Disagreement-Based Pricing: It perfectly follows the mathematical curve of p × (1 - p). The closer the price is to 50/50 (maximum disagreement), the higher the fee. The more certain the outcome (closer to 0 or 100), the lower the fee.

https://docs.polymarket.com/trading/fees

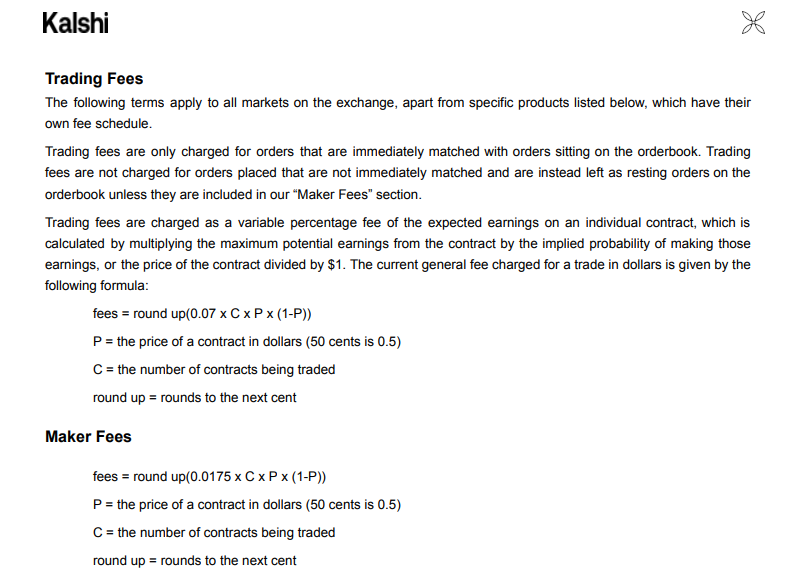

2️⃣ Kalshi: Closer to the Compliant Exchange Model

Kalshi's fee design, within a compliance framework, is closer to traditional financial derivatives exchanges. Its standard Taker fee formula is also linked to price disagreement:

fee = round up(0.07 × C × P × (1 - P))

Where C is the number of contracts and P is the contract price. Fees are rounded up to the nearest cent. This structure is very similar to Polymarket's C × feeRate × p × (1-p).

Kalshi's fee structure shares similarities with Polymarket: its trading fee also depends on the contract price. The closer to 50¢, the higher the fee; the closer to 1¢ / 99¢, the lower the fee. Kalshi's fee schedule shows that for 100 contracts, the taker fee ranges roughly from $0.07 to $1.75.

However, a key difference is that some markets on Kalshi also have a Maker fee, charged only when those limit orders are eventually filled. Cancelling a limit order is free. This indicates Kalshi's fee structure is more akin to a compliant exchange: not a simple permanent free Maker model, but more complex bilateral fee rules depending on the market.

https://kalshi.com/docs/kalshi-fee-schedule.pdf

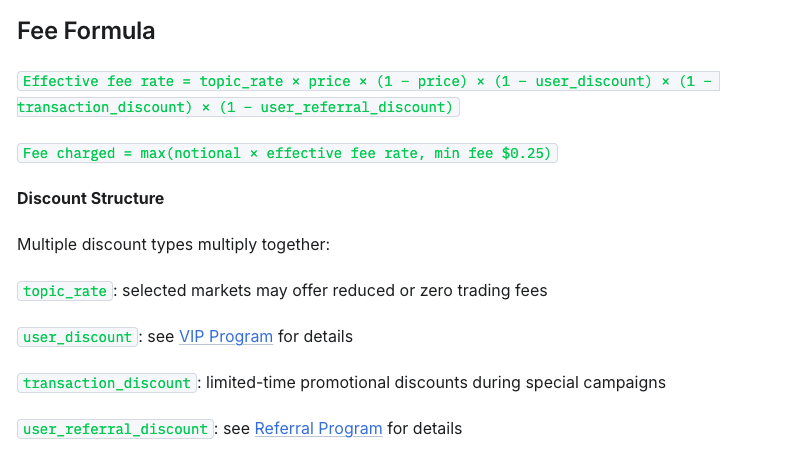

3️⃣ Opinion: Greater Emphasis on Discounts and User Tiers

Opinion introduces an extremely complex "multi-dimensional discount system." Its effective fee rate formula is:

Effective fee rate = topic_rate × price × (1 − price) × (1 − user_discount) × (1 − transaction_discount) × (1 − user_referral_discount)

This means Opinion's fee depends not only on the market price and topic_rate but also on user discounts, transaction discounts, referral discounts, and other factors.

Opinion also sets a minimum order of $5 and a minimum fee of $0.25 to prevent small trades from generating excessively low fees.

This shows Opinion's fee design leans more towards user operations:

- topic_rate differentiates markets

- user_discount creates user tiers

Therefore, compared to Polymarket's "sector-differentiated pricing," Opinion treats fees more as an operational tool: on one hand, using a discount system to guide user trading, retention, and acquisition; on the other hand, using free Maker orders to lower the barrier for placing limit orders and maintaining market liquidity.

https://docs.opinion.trade/trade-on-opinion.trade/fees

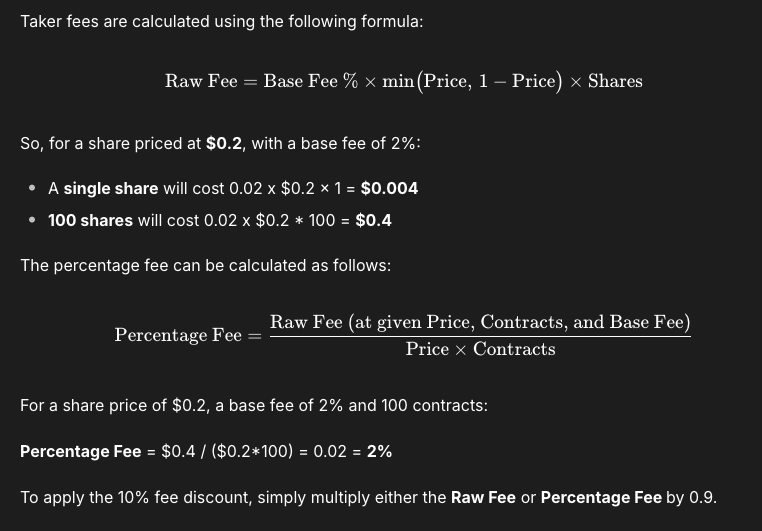

4️⃣ Predict.fun: Minimalist Flat Fee Structure

Predict.fun's fee structure is relatively simpler, suitable for reducing user understanding costs.

According to its publicly available information, its fee calculation formula is:

Raw Fee = Base Fee % × min(Price, 1 − Price) × Shares

The Base Fee is currently 2%. The actual effective rate changes with the trade price: below 50%, the rate is fixed at 2%; above 50%, the closer the price is to 1, the lower the effective rate.

Additionally, Predict.fun supports fee discounts, which further reduce the fee.

The characteristic of this design is its intuitiveness: users don't need to determine which side of the event they are on; they only need to look at the trade price itself to understand the fee change.

https://docs.predict.fun/the-basics/predict-fees-and-limits#limits

It's clear that the commonality among prediction market platforms is that they all attempt to convert aggressive trading behavior into revenue.

This also shows there isn't just one path to commercialization for prediction markets. They all ultimately answer the same question: are users willing to pay for trading?

III. Deep Dive into Polymarket: Volume Doesn't Equal Real Revenue

While different platforms employ various tactics, Polymarket remains the most suitable sample for validating the true monetization efficiency of prediction markets.

There are two main reasons:

- Its fee implementation path is the clearest: from a trial in Crypto to an expansion in Sports, and now almost universal charging across more categories.

- Its data is the most comprehensive: official feeRates, 7D/30D Fees can all be used to further break down the revenue structure.

So next, using Polymarket as an example, we answer a more specific question: Are the highest-volume sectors also the most profitable?

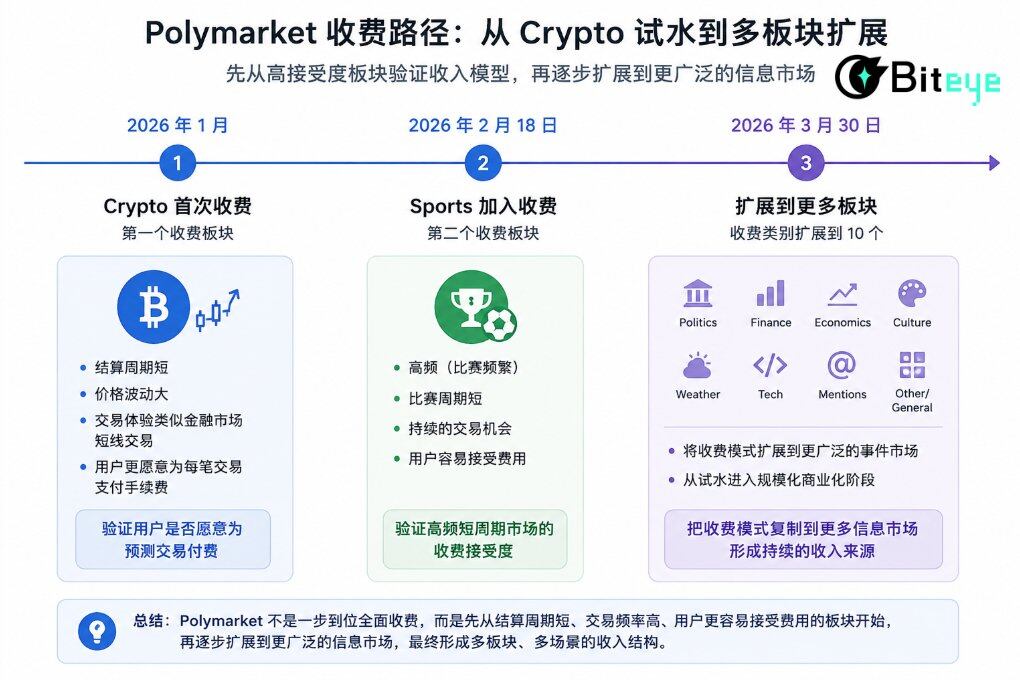

3.1 From Free to Paid: Polymarket's Commercialization Timeline

January 2026: Crypto Becomes the First Paid Sector

After returning to US users, Polymarket pioneered the introduction of Taker Fees in the Crypto sector. Crypto events have short settlement cycles, high price volatility, and trading behavior similar to short-term secondary trading. Users prioritize execution speed over friction cost sensitivity, making it an ideal testing ground for fees.

February 18, 2026: Sports Becomes the Second Paid Sector

Following closely, on February 18, 2026, the Sports sector became the second paid sector. Sports events are inherently high-frequency and short-cycle, providing a continuous stream of trading scenarios. Therefore, Sports was a natural extension for charging fees.

So, Polymarket's initial charge on Crypto and Sports was essentially validating its revenue model using two sectors with higher user acceptance first.

March 30, 2026: Fee Expansion to More Sectors

On March 30, 2026, Polymarket extended taker fees to more categories, including Politics, Finance, Economics, Culture, Weather, Tech, Mentions, Other/General, bringing the total charged categories to 10.

After universal charging, Polymarket didn't simply impose a uniform fee across all sectors but adopted a more granular fee structure. This step can be seen as a key milestone in Polymarket's commercialization, where it began extending its fee model to a broader range of markets.

The results of universal charging have been remarkably impressive. According to the latest data, Polymarket has demonstrated immense revenue-generating power: 7D Fees reached $9.27M, and 30D Fees reached $36.3M. Its 7-day revenue jumped into the top six among all crypto projects, officially entering the ranks of revenue-generating projects.

3.2 Decomposition of Core Sector Order Types and Price Distributions

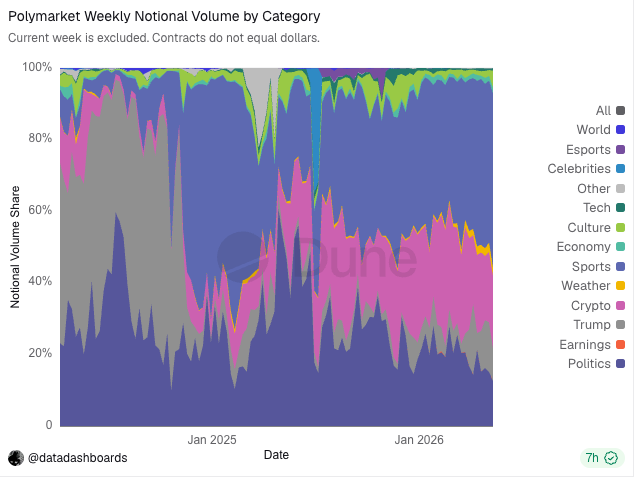

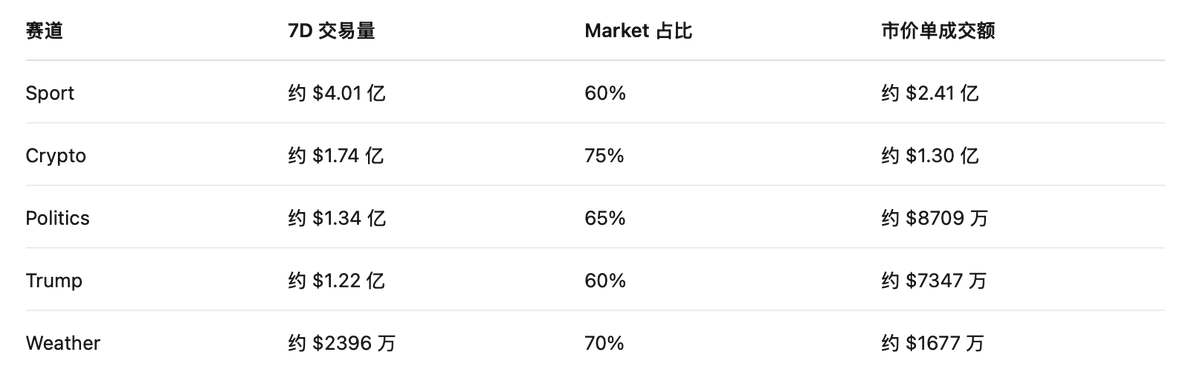

To estimate the real revenue of each Polymarket sector as accurately as possible, we used Polymarket trading data from 2021 to February 2026 to estimate fees for five major sectors.

Looking at the proportion of market orders, there are clear differences among the five sectors:

Crypto has the highest market order share at 75%, which perfectly aligns with the characteristic of crypto assets being "highly volatile and fast-changing." Users prefer to use market orders to lock in gains or losses quickly. The Weather sector, driven by real-time sudden meteorological events, also sees users placing extreme importance on reaction speed.

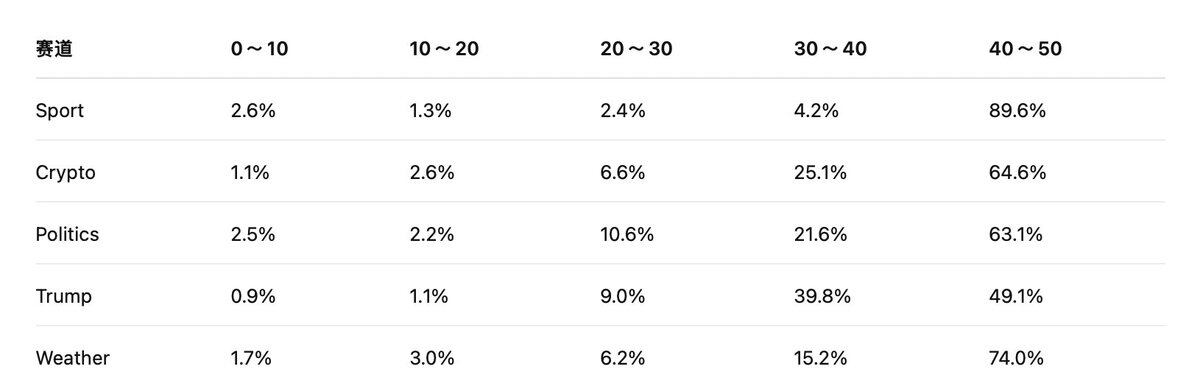

Secondly, the amount of fees heavily depends on the price range of the trades.

This is because not all trades entering the fee-charging channel generate the same fee. Polymarket's fee is related to p × (1 - p). The closer the price is to 50/50, the greater the market disagreement, and the higher the fee weight. The closer the price is to 0% or 100%, the more certain the outcome, and the lower the fee weight.

Based on data from the five major sectors, most trades are concentrated in the 30-50 range, especially the 40-50 range:

This data indicates that Polymarket's primary trading activity doesn't occur when outcomes are already close to certain, but rather when there is still significant disagreement in the market.

3.3 Revenue Estimation: Which Sector is the Cash Cow?

We roughly estimate Polymarket's fee revenue across the five sectors by taking the market order volume for each sector, combining it with the corresponding feeRate, and applying the p × (1-p) weight for different price ranges. We also consider that after fees are introduced, some fee-sensitive users may shift from Taker to Limit orders. Users engaging in end-of-trading, low-odds arbitrage, or high-frequency short-term trading will calculate their returns more carefully.

Therefore, we can make a more conservative assumption on top of our initial estimate: assume that after fees are implemented, market order volume in each sector decreases by 20%.

The adjusted formula becomes:

Adjusted Estimated Fee ≈ Market Order Volume × 80% × feeRate × p × (1 - p)

Based on the total 7D trading volume and each sector's volume share, we estimate the 7D market order volume for the five major sectors.

Having calculated the market order volume for each sector, we then combine the sector's feeRate and price range weights to estimate the fees. To make the calculation