SpaceX Wealth Wave’s "Blind Box Shareholders": Nested Structures Upon Nested Structures, Who’s Swimming Naked?

- Core Thesis: The 24-year-long private status of star companies like SpaceX has spawned a massive private secondary market, where numerous SPVs (Special Purpose Vehicles) are layered upon each other. This structure prevents buyers from verifying the authenticity of the underlying assets, creating "blind box" transactions. Meanwhile, to control shareholder count and mitigate regulatory risk, these companies are gradually tightening controls on secondary transfers.

- Key Elements:

- SpaceX's 2026 IPO valuation reaches $1.75 trillion, with its private secondary market swelling to $230 billion. This has spawned at least 170 SPVs around its shares, some with a nesting depth of up to five layers.

- Each layer of SPV incurs fees (e.g., a 6% setup fee plus management fees), causing the actual investment to shrink. Furthermore, end buyers have no right to verify whether their shares correspond to real shares and must rely entirely on intermediaries at the upper levels.

- The prolonged private period of companies (from 6 years in 1980 to 13.5 years in 2024) allows shares to be traded repeatedly. Combined with strict trade controls by SpaceX itself through rights of first refusal and buybacks, this drives up premiums in the external market.

- To circumvent the US regulatory red line requiring public financial reporting once a company has over 2,000 shareholders, and to protect option pricing and operational information security, companies like Anthropic and Figure AI are publicly declaring unauthorized secondary transactions invalid.

- SpaceX’s IPO documents will, for the first time, provide a verifiable shareholder registry. At that point, the legality of years of nested transactions will be tested, potentially exposing the "shell" risk at the bottom of some SPVs.

Two days ago, the Wall Street Journal published a story about a hedge fund almost no one had heard of, named Darsana Capital.

Founded in 2014, the fund was relatively small. In 2019, it made a decision: to bet on a rocket company that hadn't gone public yet. At the time, SpaceX was valued at around $300 billion.

Seven years later, SpaceX is about to go public, with a valuation of $1.75 trillion. Darsana's roughly $600 million invested over those years is now worth about $15 billion. This bet is one of the single most profitable hedge fund trades in Wall Street history. This one holding, SpaceX, accounts for nearly 60% of Darsana's total assets.

SpaceX, the biggest IPO ever, also marks the starting gun for this year's wave of tech public offerings. Stories like Darsana's have been frequently reported recently. Google invested $900 million in 2015, now worth over $100 billion. Founders Fund's $20 million lifeline in 2008 has now ballooned to $19.5 billion.

But flipping to other reports, the picture changes completely.

Around the end of March, both Bloomberg and Reuters reported a strange phenomenon: a group of investors bought SpaceX shares but couldn't confirm whether they actually owned them. One of them, an entrepreneur named Tejpaul Bhatia, believed he held SpaceX stock but had no way to verify if the shares supposedly belonging to him were real or fake.

On one side, there are wealth-creation myths precise to the billions; on the other, people who can't even confirm if they made a purchase. The same company, the same IPO – why is the situation so fragmented?

The Private Secondary Market Under "AI Anxiety"

Over the past two to three years, AI has driven valuations in the primary market to absurd heights.

Companies like OpenAI, Anthropic, xAI, and SpaceX are valued in the hundreds of billions or even trillions of dollars, and these valuations are still rising rapidly. Looking at these numbers, the average investor has only one thought: I want a piece of that too.

There have never been so many people wanting to get on board. The problem is, none of these companies are public. For an ordinary person wanting to buy in before an IPO, there's almost no way in.

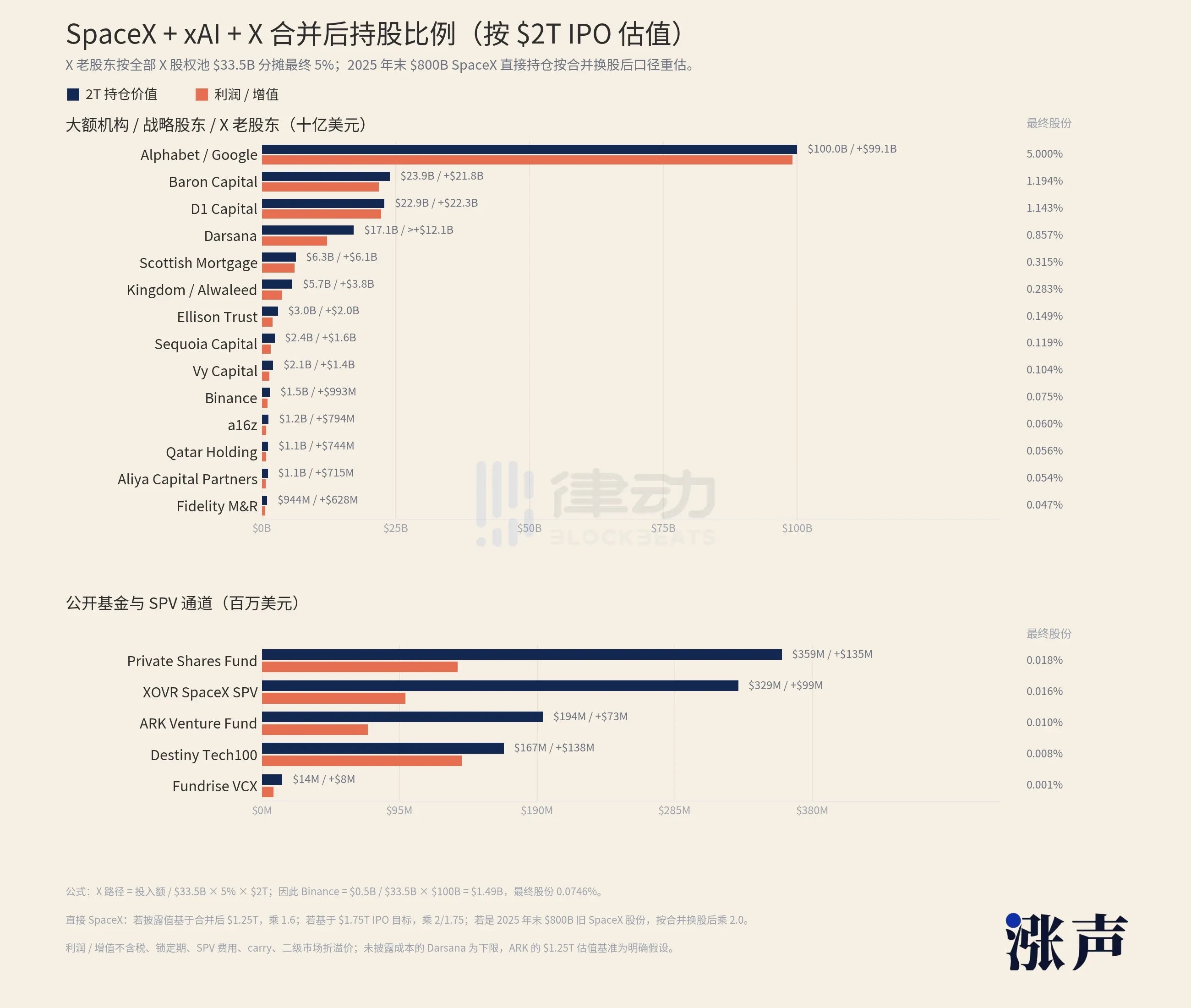

Just look at SpaceX's shareholder list. Major institutions and strategic shareholders hold tens or hundreds of billions of dollars in positions. Alphabet, Google's parent company, holds over a hundred billion alone. Of all the publicly accessible channels available now, a few ETFs and funds holding SpaceX together have an exposure of only about $1 billion.

Based on a $2 trillion valuation, how much could SpaceX's investors make?

Moreover, most channels keep ordinary people out. Most avenues in the private market are only open to accredited investors. In the US, this means having an annual income over $200,000 or having more than $1 million in assets excluding your primary residence. Those who don't meet this threshold might not even get a foot in the door for that meager $1 billion exposure.

With anything else, such a disparity would be enough to discourage people. But FOMO logic works in reverse. The more scarce it is, and the more you see others making money, the more you want to squeeze in.

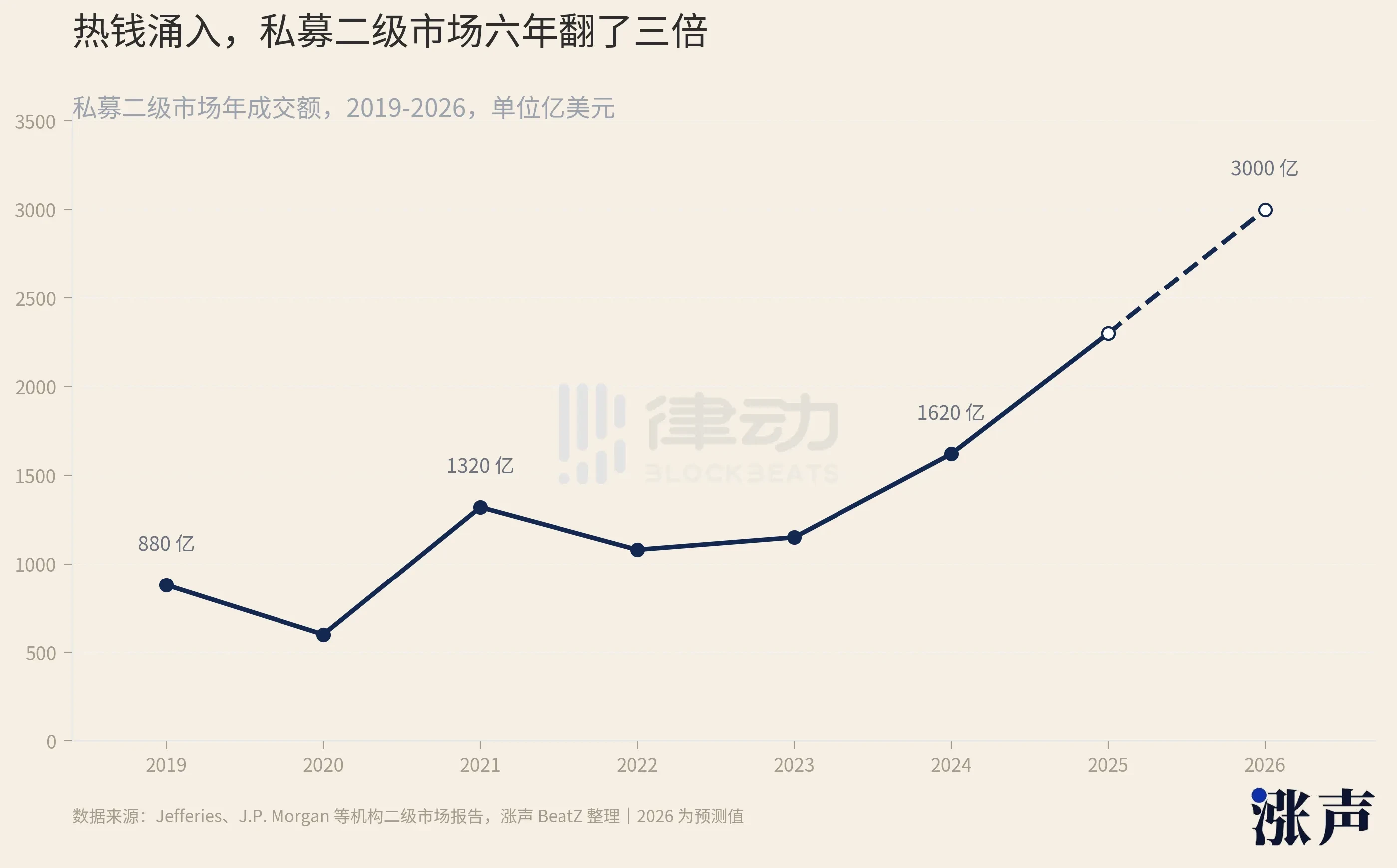

The money didn't retreat. It flooded into a place called the private secondary market.

This market specifically trades shares of private companies. Early investors and employees wanting to cash out, and those who missed the early boat wanting to get in – the platforms, funds, and various vehicles that facilitate these transactions constitute this market.

In recent years, it has expanded incredibly. From 2019 to now, its size has tripled. Total transaction volume was about $162 billion in 2024, rose to around $230 billion in 2025, and is expected to reach $250 billion in 2026. The number of companies willing to open their shares for secondary transfers went from 12 to 31 in just one year.

As money poured in, sellers of SpaceX shares also poured out.

How many poured out? According to the New York Times, there are at least 170 Special Purpose Vehicles, or SPVs, that have bought SpaceX shares. An SPV is a shell: someone gets a bit of SpaceX stock, puts it into this shell, and then sells shares of the shell to subsequent investors. 170 shells, all circling the same company.

These shells come from all sorts of backgrounds.

In October 2025, an institution called Witz Ventures launched an SPV on the fundraising platform Republic. Named The Cashmere Fund, the shell packaged three of the hottest targets – xAI, SpaceX, and Perplexity – and sold them to retail investors. About 150 listeners of a financial podcast called Rich Habits also jumped the queue into SpaceX through a group purchase. Rapper 2 Chainz and SkyBridge founder Anthony Scaramucci have both publicly claimed to hold SpaceX shares.

Retired NBA player Tristan Thompson said on a show that he invested in SpaceX when its valuation was $300 billion.

The problem is, this swarm of intermediaries is a mixed bag of good and bad.

One institution, Vika Ventures, collected $5.9 million from investors, promising to buy SpaceX shares. It was later discovered that the founder used the money to buy luxury watches and private jets. In 2023, another financial broker was sentenced to eight years for defrauding over 50 investors of nearly $6 million, selling pre-IPO shares including SpaceX.

There's also Linqto, a once-popular platform specializing in star targets like SpaceX, which went bankrupt in 2025. The SEC is investigating whether it properly verified investors' accredited status, affecting over 13,000 investors.

Even if you don't encounter a scammer, things aren't necessarily clear.

DataPower Capital is an institution dealing in SpaceX shares. Its founder, David Yakobovitch, told the New York Times that he only accepts transactions one layer removed from SpaceX. "Once you go a few layers down," he said, "things start to get murky."

Nested to the Fifth Layer

Back to those 150 podcast listeners from Rich Habits. They didn't buy SpaceX.

They bought shares in Witz Ventures, and Witz Ventures bought a share of DataPower Capital. DataPower is the one that directly obtained stock from a SpaceX registered shareholder. In other words, an ordinary person ordering from a podcast is separated from actual SpaceX stock by at least two or three layers of shells.

With each extra layer, two things happen simultaneously.

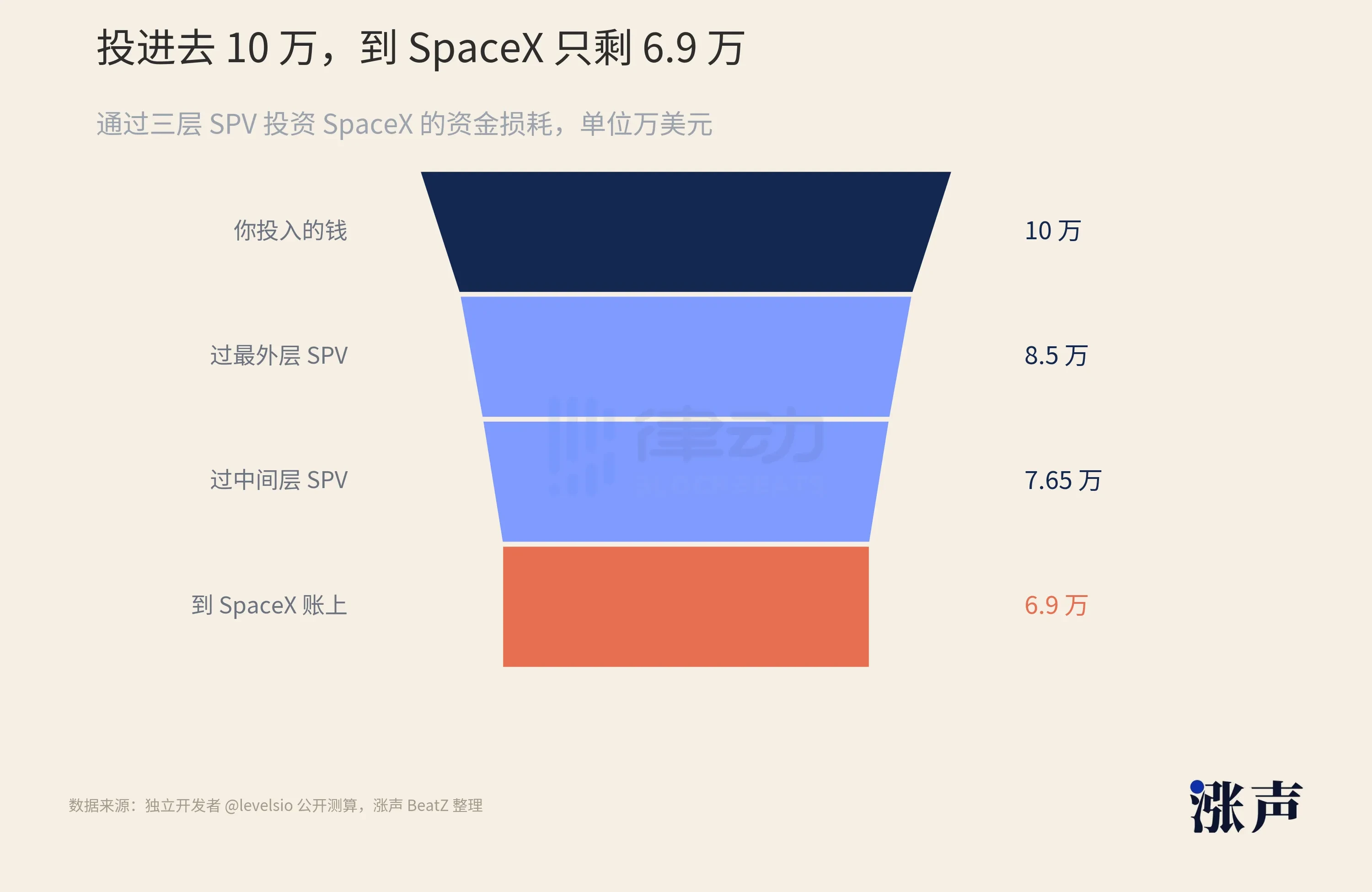

First, the money shrinks. Independent developer levelsio calculated this on social media: Suppose you invest $100,000 into SpaceX through three layers of SPV. The outermost layer charges a 6% setup fee, and the inner two layers each take management fees and profit shares. The money actually reaching the underlying SpaceX shares is only about $69,000. Before even making a profit, 30% is gone.

Second, the truth gets distorted. A fatal characteristic of this SPV structure is that investors at each layer can only see the layer directly above them. You buy the outermost shell. The shell's manager tells you it holds shares of the next shell. Is that next shell real? Are there truly SpaceX shares at the bottom? You can't see it, and you have no right to check.

Among those 170 shells, the deepest nesting reaches five layers. This is why Bhatia and others can't confirm their holdings. It's not because they aren't careful; it's because the structure from the start was designed to prevent those outside the shell from seeing inside.

Why could the SpaceX nesting doll go so deep?

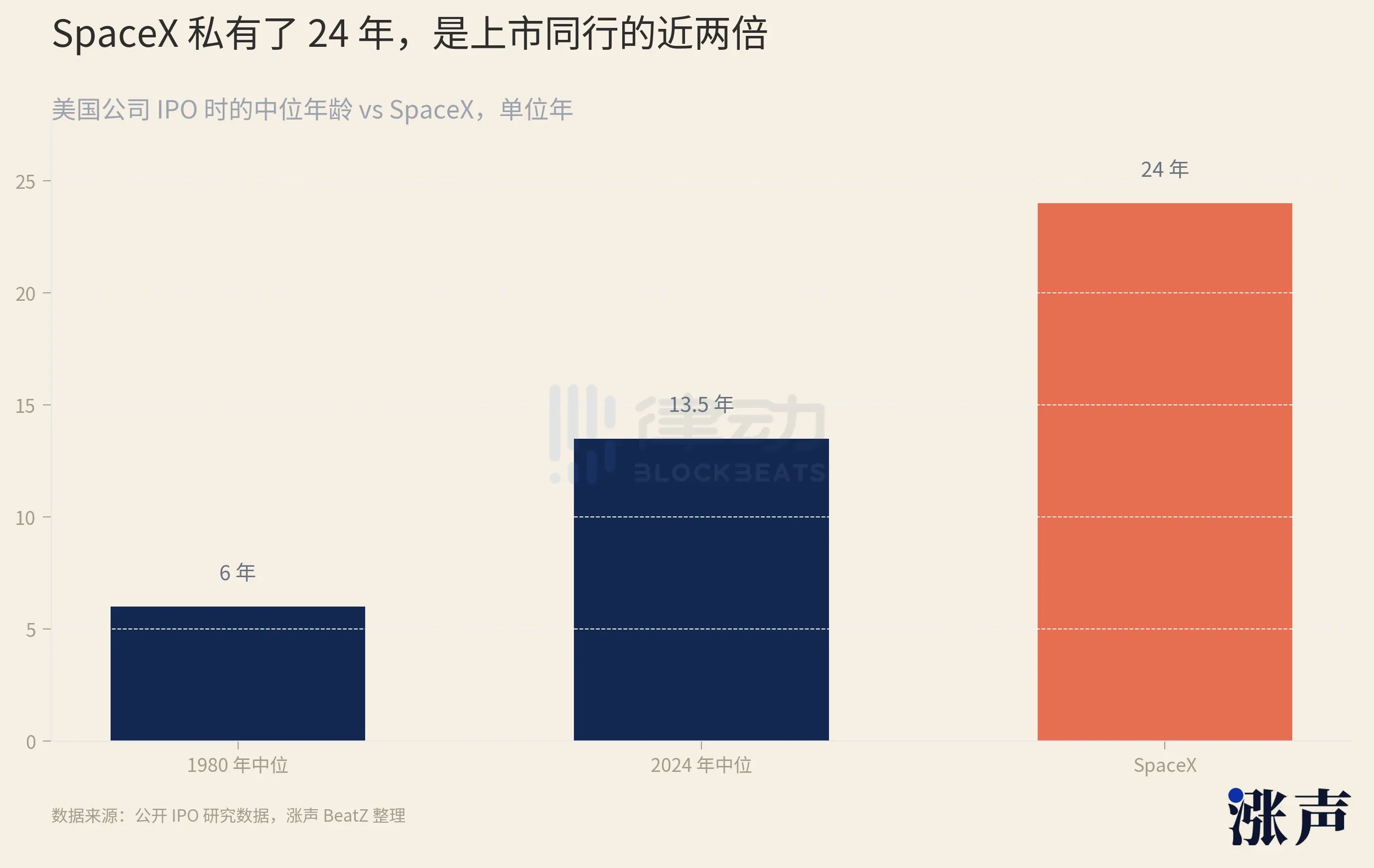

It depends on how long it has remained in the private market. Founded in 2002 and going public only in 2026, it remained private for a full 24 years.

What does 24 years mean? The average tech company going public in 1999 was only 4 years old. In 2014, the average was 11 years. More recently, the median age for US companies going public has stretched to 14 years. SpaceX's 24 years, on top of this already lengthening curve, is extreme.

The longer a company stays in the private market, the longer its shares are bought, sold, and re-shelled. SpaceX's shares have been traded over-the-counter for over two decades, resulting in layer upon layer of shells.

The lengthening private period is not unique to SpaceX.

In recent years, the median age for a US company going public has risen from 6 years in 1980 to 13.5 years in 2024. The reason is simple: there is simply too much money in the private market.

As of 2023, global venture capital still held over $650 billion in dry powder. Companies don't lack funding, so they are in no rush to go public and face the earnings pressure and regulatory oversight of the public markets. Consequently, the number of unicorns (companies valued over $1 billion) keeps piling up. There are now over 1,500 globally, worth a combined $6 trillion, and most haven't raised a round of funding based on a public valuation in over three years.

The longer a company stays in the private market, the longer its employees and early investors have their stock locked up. For these people wanting to cash out, the secondary market is the only exit. The demand is there, and SPVs specifically designed to meet this demand appear in droves.

During the venture capital boom of 2021, the number of newly created SPVs in the US surged 235% year-over-year. By the third quarter of 2024, there were over 2,400 active and identifiable SPVs. When a tool is used so extensively and repeatedly for over twenty years, nesting dolls reaching the fifth layer is almost an inevitable outcome.

And SpaceX happens to be the company that manages its stock most tightly in the entire private market. Externally, SpaceX exercises its right of first refusal on almost every share transfer, effectively intercepting sales before they happen. It conducts share buybacks every six months, buying up employee shares and bringing them back under its controlled pool.

The tighter the door is welded shut, the more expensive the tickets outside become.

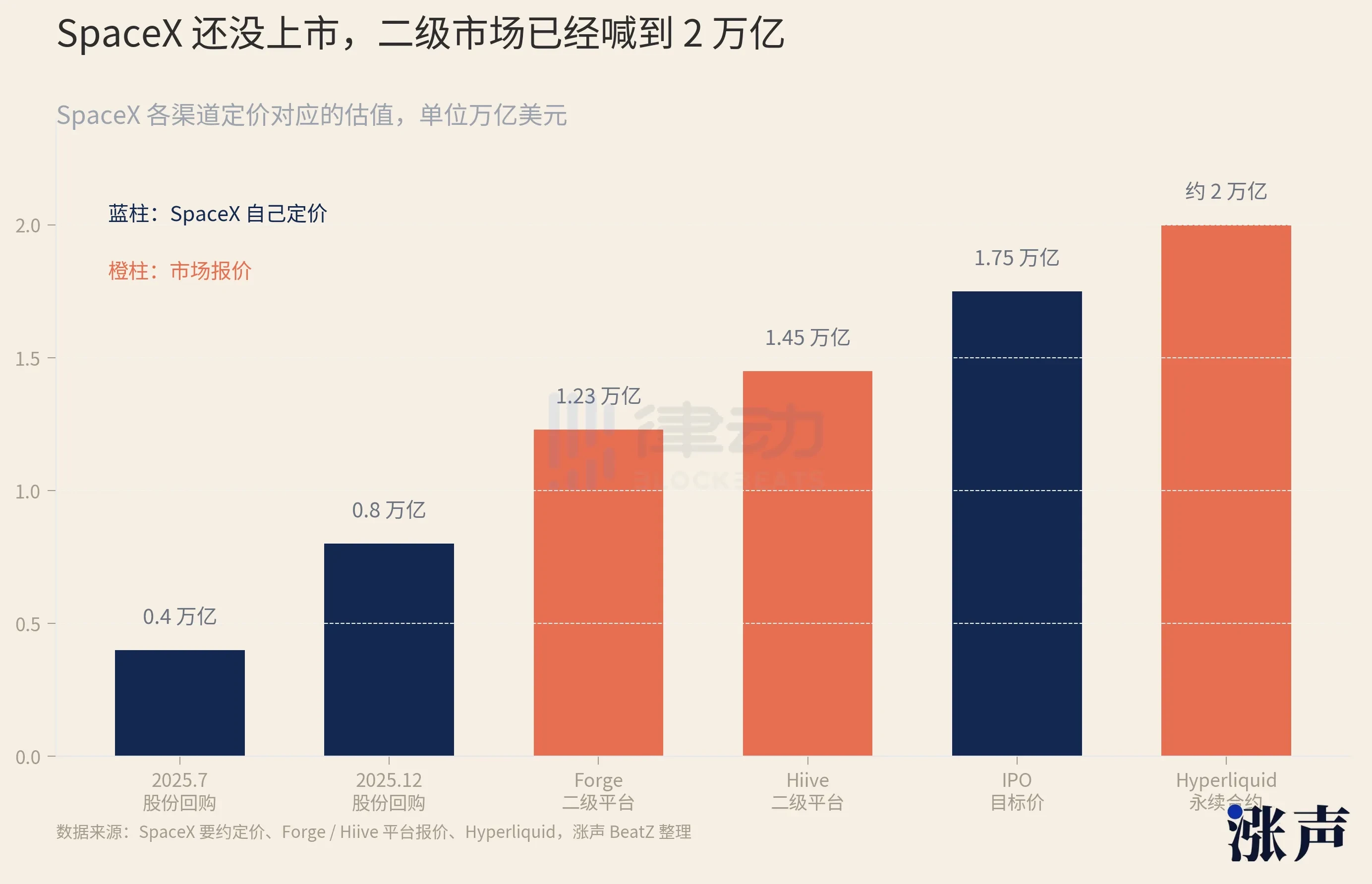

SpaceX's own pricing is quantifiable: its July 2025 share buyback was priced at a $400 billion valuation; six months later in December, it doubled to $800 billion. But secondary market quotes had already run far ahead. The Forge platform quoted around $1.23 trillion, Hiive at $1.45 trillion, and the crypto exchange Hyperliquid had futures contracts corresponding to over $2 trillion – higher than even SpaceX's own target IPO valuation.

And there's another tangled web from mergers. In March 2025, Musk merged X (formerly Twitter) into his AI company, xAI. In February 2026, SpaceX then acquired xAI entirely. Those who bought Twitter or xAI in the past, along with their entire system of shells, were all transferred onto SpaceX's shareholder register through these stock swaps.

Opening a Mystery Box

When it gets nested to this extreme, the companies themselves can no longer sit by idly.

In May 2026, Anthropic and OpenAI both publicly stated, clearly telling the market that any share transfers not approved by the board of directors are void and will not be recorded on the company's books. They named eight platforms, including Forge and Hiive, as unauthorized. Upon the news, related tokens on on-chain secondary markets specializing in pre-IPO shares crashed, losing 30% to 40% of their value in a single day.

This public stance against secondary market trading isn't just a passing whim of one or two companies.

Recently, the robotics company Figure AI, while reportedly seeking a $39.5 billion valuation, also intervened to block secondary trading of its own shares. Almost all of the hottest targets in the private market – Anthropic, SpaceX, Anduril, Stripe, Databricks – are doing the same thing: turning their tolerance for secondary trading down to zero.

Why did they collectively turn hostile?

This brings up a rarely noticed "red line" related to going public. Under US rules, if a company's shareholder count exceeds 2,000, it must regularly disclose its finances, just like a public company, even before an IPO. Nesting doll SPVs make it impossible for companies to know their actual shareholder count. One SPV counts as a single shareholder on the register but might hold shares for hundreds of people behind it. If a company inadvertently crosses the 2,000 threshold, it is forced to open its books.

There is also the issue of pricing employee stock options. If a company's shares are freely traded on the secondary market at inflated prices, the company cannot ignore that high figure when setting the exercise price for employee options. The crazier the secondary market, the less valuable the employees' options become.

More critically, it's about information. Shareholders have the legal right to access company operating information. For AI companies, model architecture, training data, and compute power arrangements are the most confidential assets. When a company doesn't even know its own shareholder count, it can't control who has access to this information.

Cleaning up the countless shareholders, protecting option pricing, and sealing information leaks – none of these are new issues individually. But when the secondary market has ballooned to $230 billion and nesting dolls reach five layers, companies find they can no longer manage it privately. So they come out in the open, stating in their first public announcements: "Your shares are invalid." SpaceX didn't issue a similar statement, but its right of first refusal system effectively does the same thing.

This pronouncement of "invalidity" leaves those mult-layered shells hanging completely in the air. You bought an SPV, paid your money. Whether those underlying SpaceX shares were ever approved or even exist – no one can give you an answer until the company publicly reconciles its books.

So buying a SpaceX SPV increasingly feels like opening a mystery box.

The day the box is opened is fixed. On June 12th, when SpaceX rings the bell on Nasdaq, its IPO filing will contain, for the first time ever, a public, verifiable shareholder register. Every single layer of shells wrapped around its stock for the past 20-plus years will have to be checked against this list at that moment. If they match, the box contains real stock. If not, it's worthless paper. On that day, Bhatia will find out which kind he got.

But after SpaceX, there is OpenAI, Anthropic, and a long line of companies waiting. Just scroll through your social media feed, and you'll see countless posts about "agency subscriptions" for these hottest AI companies.

The hot money created by AI in recent years has nowhere to go. There are only a few targets truly worth buying, and they are all locked up tight. Too much money, too narrow a doorway, and a countless number of shells grow in the middle.

As long as this imbalance persists, the private secondary market will remain what it is now: a mystery box that everyone wants to open, but no one can truly say what they've drawn.