Money is flowing into bonds and IPOs, leaving only HYPE rising in the crypto space

- Core Viewpoint: Global capital is currently undergoing a systemic withdrawal from the crypto market, shifting towards the bond market (5% yield) and traditional IPOs ($4 trillion in the queue). This has led to pullbacks in major assets like BTC, ETH, and Solana, while Hyperliquid has bucked the trend by facilitating access to traditional asset Pre-IPO trading.

- Key Factors:

- The yield on 30-year U.S. Treasury bonds has risen to 5.12% (the highest since 2007), and long-term government bond yields in G7 countries are approaching 5%, pushing global capital towards assets with guaranteed returns.

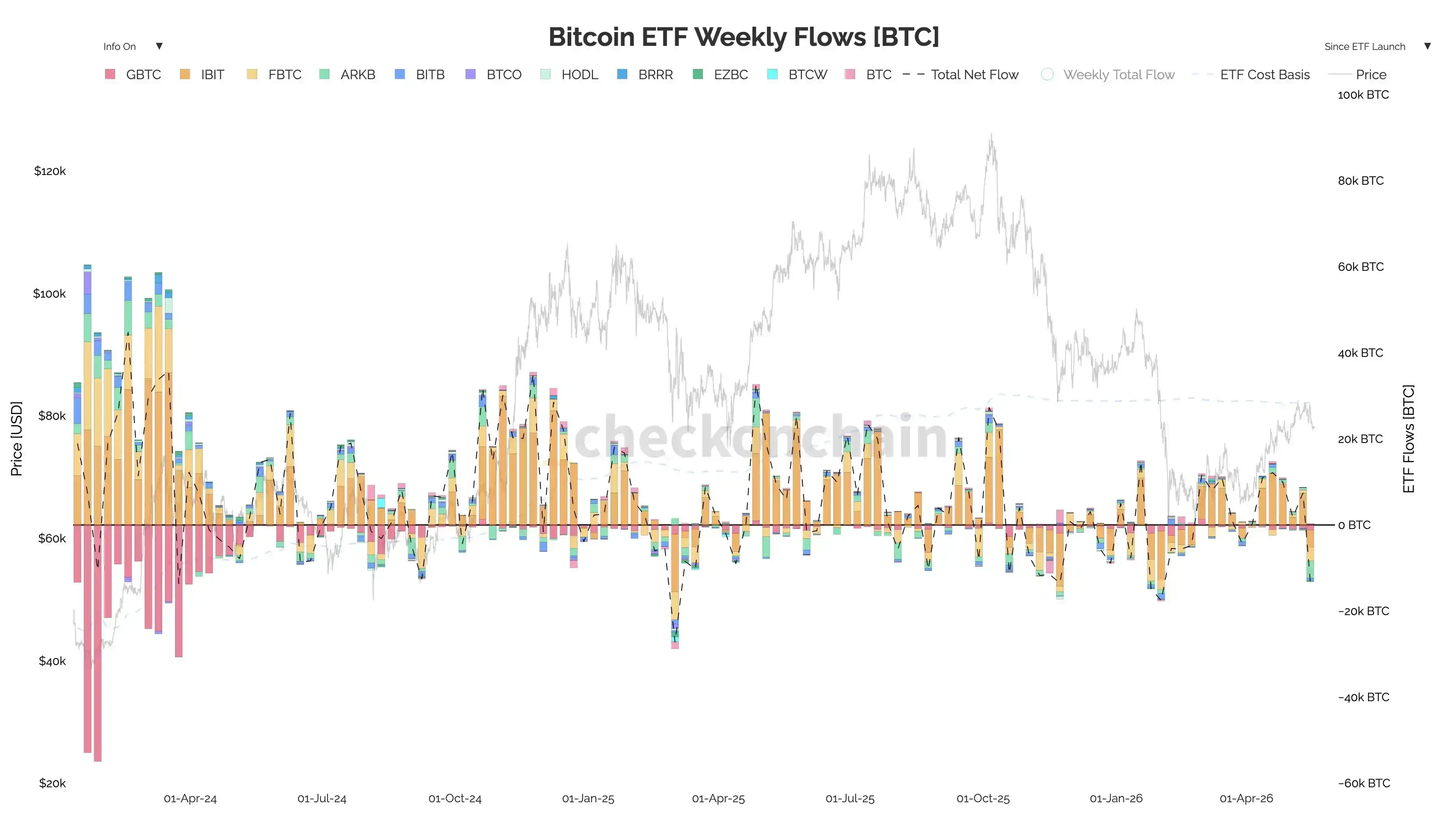

- Bitcoin spot ETFs saw a net outflow of $1.039 billion in the week of May 11-15, ending a six-week streak of net inflows. During this period, ARKB and IBIT experienced outflows of $324 million and $317 million, respectively.

- An estimated $4 trillion in IPOs are queued for 2026 (e.g., SpaceX), coupled with a surge in AI capital expenditure, diverting risk capital away from crypto asset allocations.

- The first day of trading for SpaceX's Pre-IPO contract on Hyperliquid saw a volume of $40 million. The HIP-3 platform directs on-chain liquidity towards traditional stock pricing rather than native crypto assets.

- Newly appointed Federal Reserve Chair Kevin Warsh faces the contradiction between political pressure to cut interest rates and high inflation expectations in the bond market (five-year inflation expectations at 2.7%), meaning market bets on rate cuts could be invalidated.

Where did the money go?

The S&P 500 was hitting record highs just last week, while the Nasdaq ended a seven-week winning streak. The 30-year US Treasury yield surged to 5.12%, the highest since 2007. SpaceX's Pre-IPO contract on Hyperliquid recorded $40 million in trading volume on its first day.

Money is flowing everywhere except crypto. BTC only reclaimed the $82,000 level on May 14th, but has since fallen through $77,000 in the past couple of days. ETH hasn't fared much better, dropping nearly 10% for the week, falling from the $2,300 range to $2,110. Solana has given back all its recent gains, sliding from highs near $100 back to $84. It seems like no one in the broader crypto industry is holding up, except for HYPE.

Both are considered risk assets, so why is crypto the only one lagging behind?

30-Year Bond Yields Hit Nearly 20-Year High

The bond market is re-emerging as the center of gravity for global capital.

The 30-year US Treasury yield reached its highest level since June 2007, climbing from 4.63% at the end of February to 5.12%. Meanwhile, the 10-year yield touched 4.6%, and the 2-year yield rose to 4.08%.

This isn't just a US phenomenon. Apollo Global Management Chief Economist Torsten Slok stated in his Sunday report on May 17th that government bond yields for 10-year maturities or longer in G7 countries have reached their highest levels since 2004, collectively approaching 5%.

Governments worldwide are facing expanding fiscal deficits, requiring them to borrow more and issue more bonds. The US fiscal deficit still hovers around 6% of GDP. Rising borrowing costs make it harder for governments to navigate crises through fiscal spending, precisely at a time when many countries face challenges due to global conflicts.

Deutsche Bank's Jim Reid noted in a May 18th report that bond issues were likely to be on the agenda of the two-day G7 finance ministers' meeting that opened in Paris that day. However, the structural problems in the bond market cannot be resolved by any single ministerial meeting.

In times of heightened geopolitical tension, global capital increasingly favors assets offering predictable returns.

Outflows from Bitcoin ETFs corroborate this trend.

According to SoSoValue data, spot Bitcoin ETFs saw net outflows of $1.039 billion for the week of May 11th to May 15th, ending a six-week streak of net inflows. This also marks the largest single-week outflow since the end of January.

At the product level, ARKB saw net outflows of $324 million for the week, while IBIT saw $317 million, with both leading products bleeding capital simultaneously. Daily data paints an even sharper picture. Outflows were $233 million on May 12th, $635 million on May 13th alone, and the 11 Bitcoin ETFs collectively saw another $290 million outflow on Friday, May 15th, indicating an orderly retreat of institutional funds.

The magnitude of this shift becomes clearer when compared to previous weeks. The week of April 17th saw net inflows of nearly $1 billion, April 24th saw $824 million, and the week of May 8th still recorded $623 million in inflows. The capital flow underwent a complete reversal within just one week, from "sustained inflows" to "single-week outflows of $1 billion."

During the same period, Ethereum ETFs also recorded net outflows of $255 million, marking five consecutive days of negative flows. The entire crypto ETF asset class experienced a collective turnaround in mid-May.

As the bond market becomes more attractive, crypto's relative appeal naturally diminishes.

The $4 Trillion IPO Pipeline: How Can Crypto Compete?

Bonds absorb risk-free capital. IPOs, on the other hand, compete for risk capital, representing the most direct drain on crypto liquidity.

In 2026, there's a $4 trillion IPO pipeline waiting to absorb capital. This is a figure capable of reshaping the global capital allocation landscape.

SpaceX has become the next focal point. In this environment, Pre-IPO and new issue strategies offer an appeal that bonds cannot provide: non-linear wealth effects.

Meanwhile, the AI narrative is the dominant theme of 2026. Evercore analysts noted in a May 15th report that US economic data suggests demand remains strong, particularly with a surge in AI-related capital expenditures. The flip side of this AI spending boom is the life-changing wealth effect created by leading AI companies in the secondary market.

The return efficiency of names like Nvidia and Cerebras makes any crypto narrative seem less compelling.

More strikingly, even on-chain activity is helping traditional markets compete for capital.

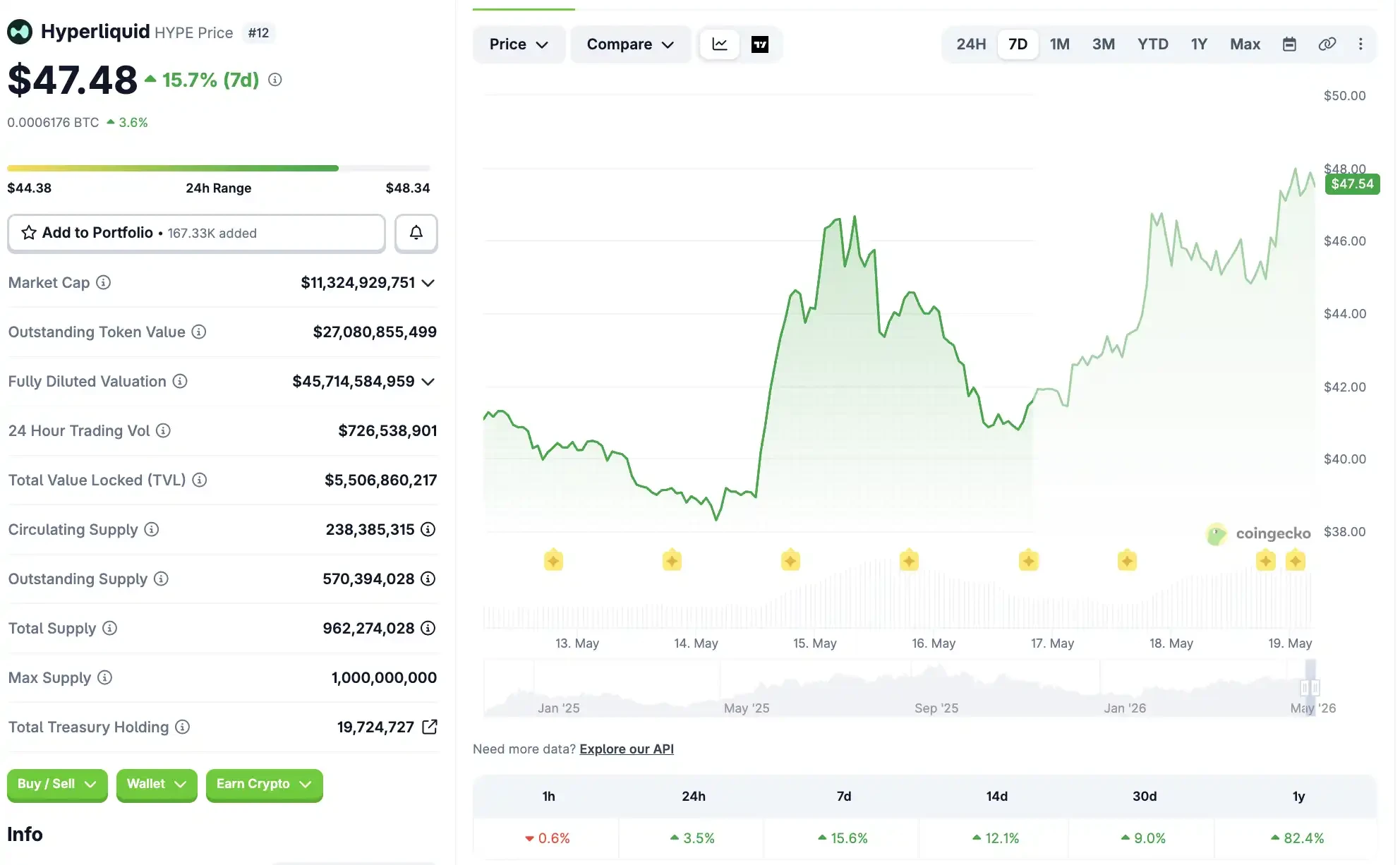

The night SpaceX launched on Trade.xyz, Hyperliquid's Pre-IPO contract saw $40 million in trading volume on its first day. The HIP-3 platform is using perpetuals for price discovery on traditional stocks. Hyperliquid itself gained 10% for the week, reaching $45, making it the only mainstream crypto asset to buck the downtrend. Related reading: 'The Biggest Winner from the SpaceX IPO Might Be Trade.xyz'.

In the short term, this is not necessarily good news for native crypto assets.

On-chain liquidity is being directed to price traditional stock targets like SpaceX, rather than flowing back into Bitcoin, ETH, or Solana. Even Hyperliquid's gains are fundamentally driven by the narrative surrounding traditional assets, not purely by crypto narratives.

Warsh Takes Office, but Rate Cuts Could Be Thwarted

The bond market and the IPO market are draining liquidity from the crypto space. Looking at the Fed, the expected new liquidity might also fail to materialize.

Powell's term ended on May 15th. Warsh was confirmed by the Senate as the new Fed Chair last week and is currently awaiting approval from the President's formal appointment committee and completing asset liquidation to comply with ethics rules.

Before even being officially sworn in, Warsh is already facing some difficult challenges.

Trump nominated Warsh partly in hopes he would be more aligned with the White House's cost-reduction agenda than Powell. Treasury Secretary Bessent has spent recent months making the reduction of government borrowing costs a core part of the White House's cost-cutting pledges. In his speech at the New York Fed last fall, he articulated clearly that lowering government borrowing costs means lowering corporate borrowing costs, mortgage rates, and car loan payments, thereby improving affordability for all Americans.

However, as mentioned earlier, the current reality is that the bond market has pushed the five-year inflation expectation to 2.7%, the highest since 2023. A May 17th report from Yardeni Research explicitly pointed out that the 2-year Treasury yield of 4.08% is the market's way of telling the Fed that the current target range of 3.50%-3.75% is set too low.

According to Warsh's own logic, he should be inclined to continue raising rates, or at least not cut them. But the White House, especially Trump himself, has an almost public political desire for rate cuts.

On the other hand, if you listened to Warsh's testimony before his confirmation, you would know he spent considerable time discussing AI. He believes AI will boost productivity and suppress inflation, thus supporting rate cuts. The problem is that short-term data shows no signs of this happening.

Interactive Brokers Senior Economist José Torres, whose view likely represents a significant portion of the market, wrote in his May 15th report that due to a lack of progress on geopolitical conflicts, the market has abandoned bets on the space for rate tightening.

If Warsh chooses to succumb to Trump's political pressure and force a rate cut, the bond market would likely respond with higher long-term yields, making things even harder for all duration-sensitive assets. If Warsh chooses a hawkish stance, expectations for rate cuts this year would be dashed, and all market bets on liquidity easing would need to be repriced.

This implies that the market's betting over the past few months on rate cuts following Warsh's assumption of office might be completely overturned.

HYPE Leads Crypto's Gainers

After the leverage blowout in the crypto market around October 10th, the recovery phase should have relied on the return of new capital.

With a $4 trillion IPO pipeline in 2026 and AI names continuing to generate wealth effects, the appeal of altcoin trades is being continuously diluted. Even Bitcoin, the crypto asset with the most institutional attributes, is beginning to cede ground to traditional markets. The $1 billion weekly ETF outflow is the most direct evidence.

High bond market interest rates are leading to Bitcoin ETF outflows. The recovery phase is being stretched indefinitely, preventing crypto from catching up with the overall rally in risk assets.

However, it's worth noting that some divergence is emerging within the broader crypto market.

Hyperliquid rose 15% for the week to $48, with year-to-date gains reaching 69%, driven precisely by the Pre-IPO price discovery narrative on HIP-3. Assets that can tell new stories and capture the gateway to traditional markets are still rising, while assets relying purely on beta are having their valuations compressed. Even Bitcoin is being sidelined.

Zooming out to view the overall financial market reveals three forces simultaneously draining liquidity from the crypto ecosystem over the past few weeks. The bond market is pulling back risk-free capital with 5% yields, the IPO pipeline is capturing incremental risk budgets with its $4 trillion scale, and the new Fed Chair Warsh may be unable to deliver on expected rate cuts for this year.

However, favorable catalysts for Bitcoin's next phase do exist.

The upside catalyst is the CLARITY Act taking effect in August. This is the biggest policy positive window for crypto this year, and increased regulatory clarity could directly release some pent-up institutional demand.

The downside risk is that before this catalyst materializes, Bitcoin might need to retest the $70,000 level. If the current $77,000 level fails to hold, the next significant support is likely around $70,000.