Gate Research: Long Put Options – Options Trading Strategy in a Bear Market

- Core Viewpoint: In a bear market or when a downtrend is expected, buying a put option (Long Put) is a strategy that exchanges a limited premium cost for downside profit elasticity. It is suitable for use in the early stage of an anticipated rapid price decline, rather than during periods of high volatility or when premiums are excessively high.

- Key Elements:

- Core Strategy Advantage: The maximum loss is locked in as the premium paid, avoiding the unlimited loss risk of short selling, making it suitable for investors sensitive to tail risk.

- Profit Structure: Losses are limited (the premium) if the price rises; profit elasticity amplifies on the downside. The break-even point is the "strike price minus the premium paid."

- Time Sensitivity: Options have an expiration date, requiring the price to decline quickly and effectively before expiration. Otherwise, time value erodes gradually, and a loss may occur even if the directional view is correct.

- Impact of Volatility: Market panic increases implied volatility, pushing up put option prices. Entering a position when entry costs are high due to later-stage volatility can offset potential profits.

- Applicable Scenario: Best suited for the stage when the trend has just turned weak but panic has not yet been fully released, not after the market has already crashed and premiums are excessively high. A comprehensive judgment of direction, timing, and volatility is required.

Summary

• In a bear market or when there is a strong expectation of a downturn, a Long Put strategy is a classic approach with limited downside risk and significant upside profit potential.

• Compared to directly shorting the spot asset, the main advantage of a Long Put is that the maximum loss is predetermined, with the investor only bearing the cost of the premium.

• This strategy is suitable not only for expressing a clear bearish view but also for hedging downside risk in a portfolio with existing long positions.

• A Long Put is not simply a bet on direction; its success depends on the magnitude of the price decline, the timing of the decline, and changes in market volatility.

• In a bear market environment, this strategy is more suitable during phases where "prices are expected to fall relatively quickly" rather than when volatility is high and option premiums are excessively inflated.

Introduction

In a bear market, investors often face a real challenge: if you believe the market will continue to fall, how should you participate in this downturn?

The most direct way is, of course, to sell the spot asset, or to short-sell using tools like margin borrowing or perpetual contracts. However, these methods often involve higher capital requirements, more complex risk management demands, and can theoretically lead to unlimited losses in some cases. For investors who do not want to bear excessive tail risk, shorting, while directionally clear, is not necessarily the easiest strategy to execute over the long term.

This is precisely the significance of put options. Buying a put option essentially involves paying a fixed cost (the premium) in exchange for the right, but not the obligation, to sell an underlying asset at a predetermined price (the strike price) within a specific future period (until expiration). While the investor is not obligated to exercise the option, if the market indeed falls, this right becomes more valuable.

Therefore, a Long Put is essentially a strategy of "exchanging a limited cost for upside profit potential from a decline." It has an offensive nature, as profits can amplify rapidly during a market crash, but also a defensive one, as the maximum loss is capped at the initial premium paid, even if the market prediction is wrong.

Strategy: Long Put

1.1 Strategy Characteristics

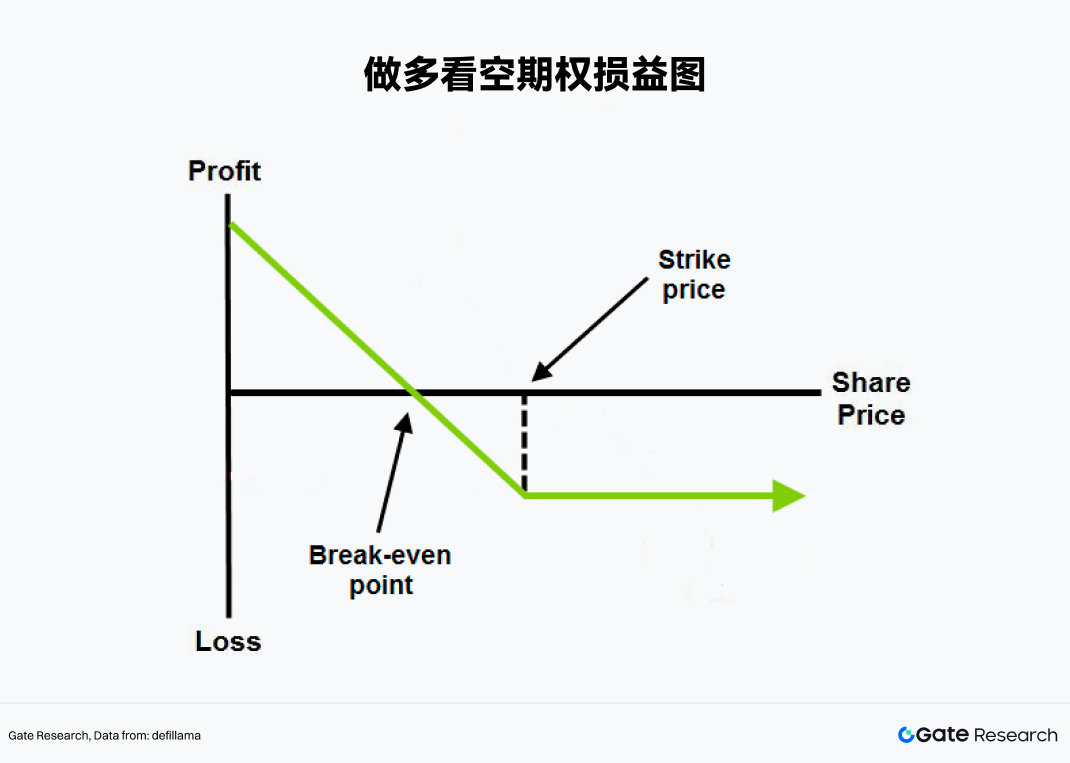

A Put Option grants the buyer the right to sell the underlying asset at the agreed-upon strike price on or before the expiration date. Buying a put option is what the market commonly calls a Long Put.

This strategy is most suitable when the market outlook is very clear: an investor expects the price of a specific underlying asset to fall in the future, ideally a significant decline within a limited timeframe. Unlike spot assets, options are time-bound instruments. When an investor buys an option, they pay a premium, which is like buying an "insurance policy with a limited validity" for their prediction. If the underlying price moves favorably within the effective period, this "insurance policy" increases in value. However, if the market does not fall as expected, or declines too slowly, the time value of the option will erode continuously, potentially rendering it worthless at expiration.

From a profit-and-loss structure perspective, the Long Put strategy has several distinct characteristics.

• Limited Maximum Loss. No matter how much the underlying asset's price rises subsequently, the buyer can only lose the initial premium paid for the option.

• Significant Downside Profit Potential. As long as the underlying price continues to fall, the value of the put option increases correspondingly, with the maximum theoretical profit also being limited.

• Clear Breakeven Point. The trade only starts generating a net profit at expiration when the underlying price falls below the "strike price minus the premium paid."

• Time-Sensitive Strategy. Getting the direction right is not enough; the price decline must occur effectively before the option expires.

It is precisely for this reason that the Long Put, while being a bearish strategy, is not a tool suitable for *every* instance where a decline is anticipated. It requires a comprehensive judgment on the price direction, the timing of the move, and the underlying volatility over the option's lifespan.

1.2 Strategy Advantages

A bear market is not simply about falling prices. It is often accompanied by valuation compression, liquidity contraction, decreased risk appetite, and a significant increase in volatility. In such an environment, the Long Put is considered a classic bear market strategy mainly for three reasons.

First, it amplifies the efficiency of expressing a bearish trend. If an investor directly sells the underlying asset, the profit typically has a one-to-one relationship with the price decline. However, after buying a put option, when the price decline accelerates and volatility rises, the option's value often shows higher elasticity (leverage).

Second, it controls the worst-case scenario. One of the most common occurrences in a bear market is that, despite an overall weakening trend, there are frequent sharp bounces. Many short trades fail not because the direction was wrong, but because they were stopped out or liquidated during these violent intermediate fluctuations. The advantage of a Long Put is that even if the market suddenly rebounds short-term, the buyer will not face unlimited losses like leveraged short positions can.

From a practical perspective, the Long Put strategy is often most suitable not necessarily when "the market has already finished crashing," but rather during the period when "the trend has just turned bearish, but panic hasn't fully been released." This is because when the market is already in extreme panic, the implied volatility of options is typically significantly elevated. Buying puts at this point can be very expensive, making the risk-reward ratio potentially unfavorable.

1.3 Strategy Example

Gate currently supports short put options for several major cryptocurrencies. Taking BTC as an example, suppose at a certain point, the spot price of BTC is 84,000 USDT. An investor believes that the market might enter a further downward phase over the next month due to weakening macroeconomic prospects, risk-off capital flows, and profit-taking by holders from higher levels. Instead of directly shorting a perpetual contract, he chooses to buy one BTC put option contract expiring in one month with a strike price of 80,000 USDT, paying a premium of 4,000 USDT.

The key parameters for this trade are as follows:

• Underlying Price: 84,000 USDT

• Strike Price: 80,000 USDT

• Premium Paid: 4,000 USDT

• Time to Expiration: 30 days

• Breakeven Point: 76,000 USDT

This means that at expiration, the trade only starts generating a net profit if BTC falls below 76,000 USDT.

If one month later, BTC drops to 70,000 USDT, the intrinsic value of this put option is:

80,000 - 70,000 = 10,000 USDT

After deducting the initial premium of 4,000 USDT paid, the net profit would be:

10,000 - 4,000 = 6,000 USDT

Conversely, if at expiration the price of BTC is still above 80,000 USDT, then this put option has no intrinsic value. The investor's maximum loss is the initial premium paid of 4,000 USDT.

Long Put: Returns, Risks, and Key Variables

To truly understand this strategy, the key is not just remembering "puts make money when the market falls," but understanding *why* they make money and under what circumstances they might fail.

2.1 Source of Profit: Price Decline

The most direct source of profit for a Long Put is a decline in the underlying asset's price. Suppose an asset currently trades at $36.25. An investor buys a put option with a strike price of $35, paying a premium of $2, with 90 days remaining until expiration. The breakeven point for this trade is $33, calculated as:

Breakeven = Strike Price - Premium = 35 - 2 = 33

If the price falls to $30 at expiration, the put option's intrinsic value is $5. After deducting the initial $2 premium, the net profit is $3. If the price is still at $35 or higher at expiration, the option is worthless, and the maximum loss is the initial $2 premium paid. This illustrates the core structure of a Long Put: limited loss if the price rises, and increasing profit potential if the price falls.

2.2 Time Decay: Getting the Direction Right Might Not Be Enough

The biggest difference between options and spot assets is the "time" dimension.

For a put option buyer, time is often not an ally. If the market does not decline immediately as expected, the time value embedded in the option will gradually erode (time decay / theta). Even if the directional bet is ultimately correct, if the decline is too slow or occurs too late, the trade outcome could be unfavorable (e.g., the loss from time decay offsets the profit from the price drop).

This means that a Long Put involves not just predicting *if* the market will fall, but also *when* it will fall.

2.3 Volatility Impact: Another Layer in a Bear Market

Besides price and time, volatility is another critical variable in options trading.

Generally, the more panicked the market, the more expensive options become, especially puts. This is because investors are more willing to pay a premium for protection or speculative bets during downturns. Therefore, a Long Put typically benefits from a rise in implied volatility (vega positive). However, this also presents a challenge. If an investor buys puts *after* the market has already crashed significantly and panic is extreme, resulting in very high option prices, a subsequent decline in volatility (even if the price continues to fall slowly) could offset some of the potential profit. In essence, a Long Put is not just a bet on the price falling; it can also be seen as a bet that "the decline is not yet fully priced in" by the volatility market.

Conclusion

The Long Put is one of the most classic directional option strategies in a bear market. Its appeal lies in using a limited loss (the premium) to gain high profit potential from a price drop. Compared to directly shorting the asset, it's easier to control tail risk. Compared to simply selling the spot asset, it retains a more offensive, leveraged characteristic.

However, it is not a tool that guarantees easy profit just because you are bearish. The difficulty of the Long Put lies in the fact that it requires the investor to have a reasonable assessment of the direction, timing, speed of the move, and volatility expectations. If the market doesn't fall fast enough, deep enough, or if the entry point is too crowded (with high implied volatility), the actual performance of the trade can be significantly diminished.

Cryptocurrencies, being a typical high-volatility asset class, provide a natural environment for the Long Put strategy. Once the market enters a phase of declining risk appetite, weakening price trends, and increased event-driven volatility, buying put options can become a strategic choice that combines both defensive and offensive attributes. But fundamentally, it remains a trading method that requires discipline, timing, and an understanding of the Greek risks, not a simple "copy-trading" tool.

References

• Gate, https://www.gate.com/help/other/options/28363/introductions-of-gate.io-s-options

• Investopedia, https://www.investopedia.com/terms/l/long_put.asp

• InteractiveBroker, https://www.interactivebrokers.com/campus/trading-lessons/bear-market-long-put/

• Optionclue, https://optionclue.com/en/tradinglossary/long-put/

Gate Research is a comprehensive blockchain and cryptocurrency research platform that provides readers with in-depth content, including technical analysis, hot topic insights, market reviews, industry research, trend forecasts, and macroeconomic policy analysis.

Disclaimer

Investment in the cryptocurrency market involves high risk. Users are advised to conduct their own independent research and fully understand the nature of the assets and products being purchased before making any investment decisions. Gate is not responsible for any losses or damages arising from such investment decisions.