Pre-IPO New Battle: On the Eve of Listing, $SPCX Has Been Pushed to $2.5 Trillion

- Core Thesis: Trade.xyz has launched SpaceX's Pre-IPO perpetual contract $SPCX on Hyperliquid with a starting price of around $150. However, its on-chain trading price has surged to $216, reflecting strong bullish market sentiment towards its IPO. The product incorporates a step-based price control mechanism to limit volatility, while multiple CEXs have also launched similar offerings, marking the pre-IPO trading of US stocks as a new battleground for crypto industry trading volume.

- Key Elements:

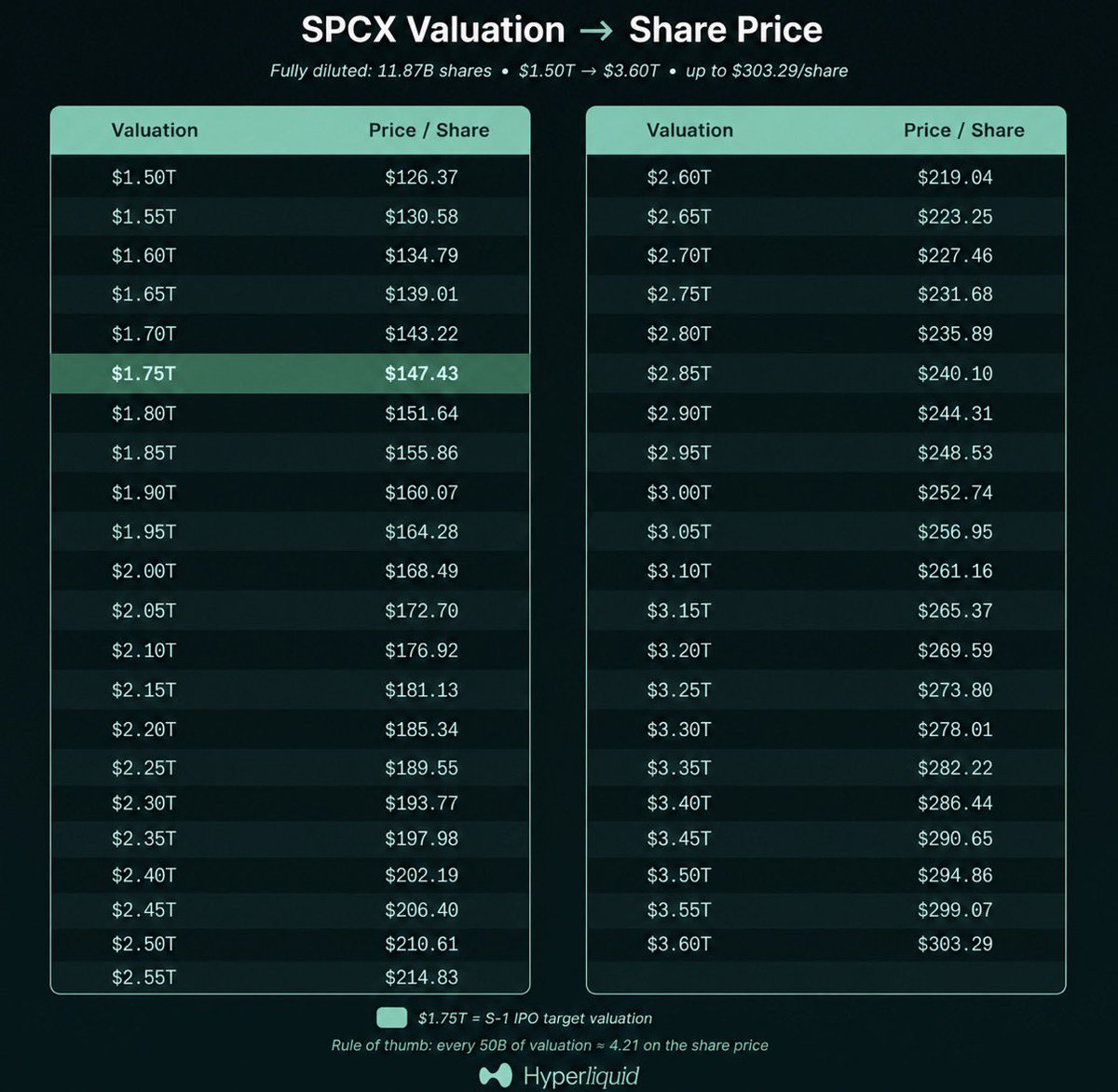

- SpaceX has confidentially filed its S-1 document, targeting a valuation of $1.75 trillion and planning to raise $75 billion. If successful, it would become the largest IPO in history.

- $SPCX is priced based on 11.87 billion shares, with a starting price of $150, close to SpaceX's target valuation (~$147/share). After launch, it once rose to $216, corresponding to a valuation of approximately $2.56 trillion.

- Past experience with the Cerebras ($CBRS) Pre-IPO contract shows that the on-chain price traded at roughly a 50% premium to the IPO price before listing but still remained below the opening price. However, given SpaceX's massive scale, institutional pricing power may diminish the leading role of on-chain sentiment.

- $SPCX features a step-based price control mechanism. If the oracle price deviates from the market price by more than 20%, trading will be locked, limiting the maximum price movement to 7 steps to manage volatility risk.

- In the private market, Brookfield holds $2 billion worth of SpaceX shares at a valuation exceeding $2 trillion. The on-chain valuation (~$2.56 trillion) still represents approximately a 25% premium to that.

- Multiple CEXs (e.g., OKX, Gate, Bitget) have launched SpaceX derivatives, but the quoted prices vary significantly ($216 to $2000), primarily due to differences in the share count basis. Investors need to be aware of the risks.

- As the heat of crypto-native narratives (e.g., meme coins) wanes, introducing traditional star IPOs (like SpaceX) has become a new direction for the industry, leveraging their inherent attention and real valuation systems to stimulate trading volume.

Original Author: Ku Li, ShenChao TechFlow

Before the hype around $CBRS has fully subsided, Trade.xyz launched its second Pre-IPO perpetual contract on Hyperliquid this morning.

This time, the underlying asset is SpaceX.

According to reports from Bloomberg and Reuters, SpaceX confidentially submitted an S-1 registration document to the SEC on April 1, with a target valuation of $1.75 trillion and plans to raise up to $75 billion. If successful, this would be 2.5 times the size of Saudi Aramco's $29 billion IPO in 2019, making it the largest single public offering in the history of human capital markets.

The whole world is waiting for this stock. Now, on-chain, there's no need to wait.

According to the Trade.xyz announcement, $SPCX is priced based on 11.87 billion fully diluted shares, with a starting price of $150.

Based on the listing application documents SpaceX submitted to the SEC, the target valuation is $1.75 trillion, which translates to approximately $147 per share. This means Trade.xyz set the starting line for $SPCX near SpaceX's own valuation.

However, on-chain sentiment clearly believes this price is too low.

Within hours of its launch, SPCX's price jumped from $150 to $216, a 44% increase. Using the same share count, a price of $216 corresponds to a valuation of approximately $2.56 trillion, almost 50% higher than SpaceX's own target.

Given the current situation, is $SPCX expensive or cheap in pre-market trading?

Stepped Price Control: SPCX On-Chain Volatility is Less Pronounced

The last experience with pricing Pre-IPO contracts came from $CBRS three weeks ago.

According to Hyperliquid News data, CBRS traded on-chain near $277 before its IPO, approximately 50% higher than Cerebras' final issuance price of $185.

At the time, many thought the on-chain price was inflated. Yet, Cerebras opened directly at $350, which was another 26% higher than the on-chain price.

On-chain traders correctly identified the trend and set a more aggressive price than the underwriters, but still underestimated the frenzy of the actual opening.

The situation with SPCX looks familiar. The on-chain price is nearly 50% higher than the target valuation in SpaceX's listing application, almost the same premium as CBRS had on-chain at the time.

However, the author believes directly applying the CBRS experience requires caution. Cerebras raised $5.5 billion; SpaceX plans to raise $75 billion. One is a mid-sized tech IPO, the other is the largest public offering in history. The larger the entity, the heavier the institutional pricing power. How far on-chain retail sentiment can lead institutions is an unknown variable.

There is also a variable that didn't exist with CBRS. According to Trade.xyz documentation, the SPCX pre-market now includes a stepped price control mechanism:

The deviation between the oracle price and the market price cannot exceed 20%. Once triggered, trading is locked until the oracle catches up before the next round opens. There are a maximum of 7 steps for both upward and downward movements. After 7 upward steps, the price hits a ceiling; after 7 downward steps, it hits a floor. This continues until the official IPO listing or the contract expires on August 29.

This design means SPCX's price is confined within a calculable range. Unlike CBRS, which was completely free pricing, SPCX has a ceiling above and a floor below.

For traders, the nature of the game has changed. Both the upside potential and downside risk are limited.

Is there an off-chain reference point to check if the on-chain pricing is unreasonable? According to Bloomberg, Brookfield disclosed on May 14 that it holds $2 billion in SpaceX Pre-IPO shares, corresponding to a valuation exceeding $2 trillion.

This means that the price offered by institutional investors in the private market is already significantly higher than the $1.75 trillion stated in the listing application. The current on-chain valuation of around $2.5 trillion is about 25% higher than the private market.

No one can definitively say whether this premium is reasonable. But at least two reference points exist: the private market has already valued SpaceX above $2 trillion; and the CBRS experience shows that a 50% on-chain premium ultimately proved insufficient.

Everything might only become clear when $SPCX actually opens on June 12.

CEXs Enter the Fray, Competing for US Stock Pre-Market

When CBRS launched three weeks ago, Pre-IPO perpetual contracts were essentially Hyperliquid's exclusive business.

SpaceX is different; major platforms have all joined. According to BitMart statistics, OKX's SpaceX perpetual contract is quoted around $2,000, Gate around $1,908, Bitget's preSPAX around $680, and Binance Wallet around $720. Hyperliquid's SPCX is quoted at $216...

The same SpaceX, with prices ranging from $216 to $2,000 – a difference of nearly 10 times?

This isn't because someone priced it incorrectly. The platforms use completely different share bases. Hyperliquid's SPCX is priced based on 11.87 billion shares post-stock split. Many CEXs use the pre-split share count, naturally resulting in a higher unit price.

According to a Bitget announcement, preSPAX claims to be backed by real equity issued by Republic. Most other platforms use purely synthetic derivatives. Even the underlying asset types are different.

For those unfamiliar with the mechanics, there is a common pitfall. Seeing $216 on Hyperliquid and $2,000 on OKX, one might initially think Hyperliquid is ten times cheaper. However, when converted to valuation, they might be similar. The difference lies only in the share base and product structure.

Trading without calculating the valuation is clearly the fastest way to lose money.

The fragmentation of prices itself indicates something. When CBRS launched, only Hyperliquid offered Pre-IPO contracts. Less than a month later, Pre-IPO products for SpaceX are available across all major exchanges. This category is evolving from a single-platform experiment into industry-wide infrastructure.

For Hyperliquid, the good news is that it personally validated a product category. The bad news is that anyone can participate in this category.

Everyone is racing into this category, and the reason behind it might be more noteworthy than the category itself.

Over the past year or so, the crypto market's own narrative has weakened. The hype cycles for meme coins are getting shorter. Altcoins lack new stories. On-chain trading volumes are shrinking. Active user counts on many platforms have started to decline. Everyone is searching for the next thing that can generate real trading volume.

Star US stock IPOs perfectly fill this gap. Companies like SpaceX, OpenAI, and Anthropic command global attention without any platform needing to create buzz. The attention is naturally there.

More importantly, unlike meme coins, these assets have real revenue, referenceable valuation frameworks, and clear listing timelines. Traders are not gambling on an illusory narrative. Although emotional factors play a role, the underlying assets themselves are real and verifiable.

This kind of certainty is a scarce commodity in today's crypto market.

So, when platforms scramble to list SpaceX Pre-IPO, they are not just competing for one product. They are vying for the entry point to the next phase of trading activity. When the native crypto narrative runs out of steam, importing the world's most popular traditional assets, allowing them to be priced, traded, and speculated upon on-chain – this might be the new path the entire industry is groping towards.

US stock Pre-IPO is becoming the new battleground for the crypto industry. Embracing the change is the more pragmatic choice.