零资金费率?老外都在聊的HyperEVM新合约设计

- 核心观点:加密交易员Jez在HyperEVM上推出新型永续合约协议PaperTrade,采用无手续费、无滑点、无资金费率模式,但本质上是一种用户与LP池对赌的机制,并通过代币PAPER将交易亏损转化为平台股份。

- 关键要素:

- PaperTrade读取Hyperliquid报价但不撮合订单,交易在用户和公共LP池之间直接结算,类似历史上的“bucket shop”对赌模式。

- LP池不接受外部存款,仅依赖用户亏损的保证金;用户盈利部分通过链上债权队列排队,等待后续亏损单填补。

- 代币PAPER根据用户亏损数量按曲线铸造,LP余额低于200万美元时每亏损1美元铸造100枚PAPER,超过后铸造速率衰减。

- PAPER质押者可获得协议抽水收入和LP池超过500万美元后的所有超额部分,形成“输家获得股份、赢家取走输家钱”的闭环。

- 参与策略建议在LP池TVL低位时亏损铸造PAPER,TVL高位时质押PAPER坐收分红。

Crypto trader Jez today announced PaperTrade, a new protocol developed on HyperEVM, sparking lively discussions within the English crypto community.

Jez, a long-time advocate of perpetual contracts, went all-in on Hyperliquid in its early days. His wallet address ranks highly on the airdrop leaderboards for both Lighter and Variational. This time, he's building the product himself — a Perp DEX with no trading fees, no slippage, and no funding rates.

The Old-School Bucket Shop Goes On-Chain

The mechanics of PaperTrade have an infamous historical predecessor. In early 1900s American towns, "bucket shops" operated under the guise of brokerage firms. They would chalk up real-time stock prices from the NYSE on a blackboard, but customer orders never left the shop owner's drawer. Essentially, customers were betting against the shop owner. This practice was outlawed by New York state in 1909 and had mostly vanished by the 1920s.

When a user opens or closes a position on PaperTrade, the platform directly reads the order book price from Hyperliquid and settles the difference in P&L against a public LP pool. Throughout this process, no order ever enters Hyperliquid's matching engine, and no actual perpetual contract changes hands. The trade is always between the user and the LP pool, with no third-party counterparty.

Perpetual Futures + P2P + DeFi Ponzi

PaperTrade also borrows models from DeFi yield farming and P2P lending.

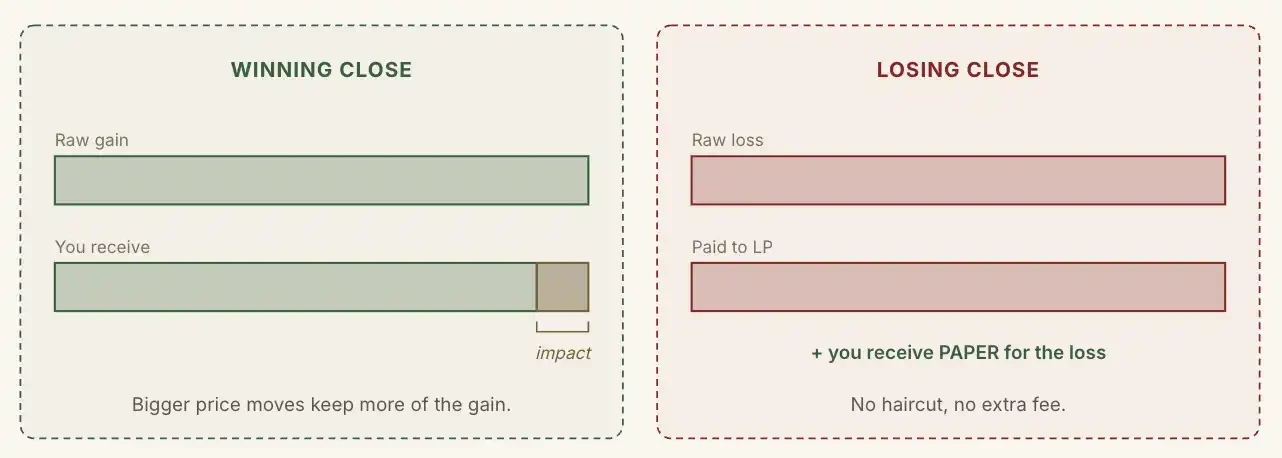

A user's losses on PaperTrade are added to the protocol's LP pool in full. Meanwhile, the protocol takes a cut from a user's profits. The smaller the price movement, the larger this profit cut. In other words, the more a user wins, the smaller the protocol's take.

Unlike HLP, PaperTrade's LP pool has no pre-deposit from the team, no VC backing, and does not accept external deposits of any kind. Its sole source of funds is the margin from user losses.

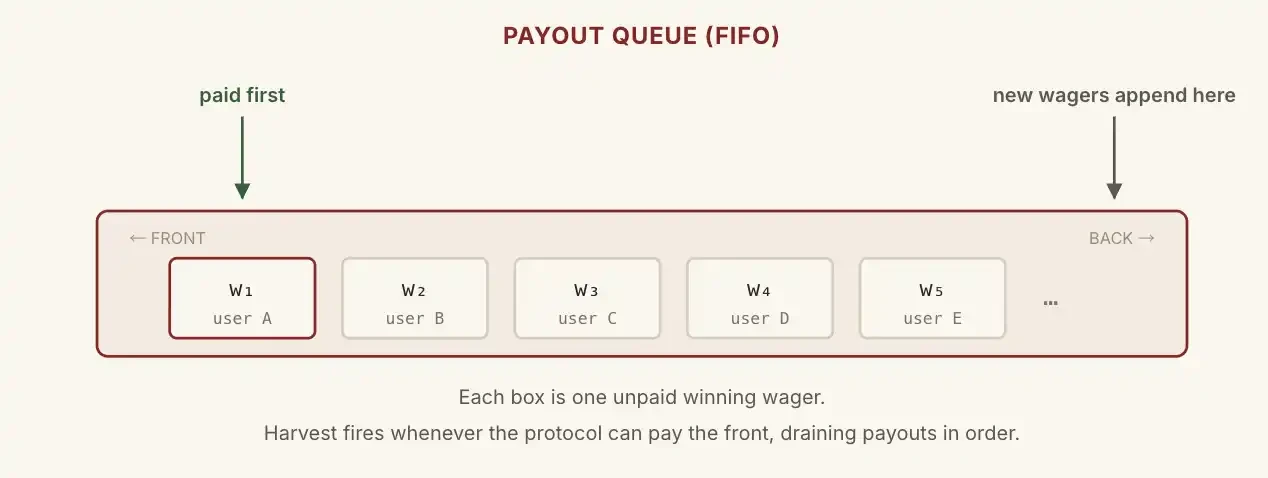

The question arises: What if the LP pool only has $100, but a user wins $5,000? How does the protocol pay out?

PaperTrade implements a queue system similar to the debt queue in traditional P2P lending, but on-chain.

This $5,000 winning enters an ordered on-chain queue, waiting for subsequent losing trades to fill the gap. The queue pays out sequentially from the start. A user's principal is always returned first, with only the profit portion being queued.

Theoretically, the LP can become temporarily "insolvent," but every winner will eventually be paid in full, provided that the losses from losers can cover the protocol's debt to winners.

If this were the whole story, the project would be destined for failure. An empty LP pool would mean winners might wait indefinitely to receive their profits in the queue, removing their incentive to trade. Traders would leave, and without losers, the protocol's debt to winners would become bad debt.

The true genius of PaperTrade lies in its token, PAPER.

For every dollar a user loses, the protocol mints a certain amount of PAPER according to a bonding curve.

When the LP balance is below $2 million, the minting rate is fixed at 100 PAPER per $1 lost. Once the LP exceeds $2 million, the rate begins to decay. The higher the LP balance, the fewer PAPER tokens are minted for each dollar lost.

X-axis: PAPER minted per unit of loss; Y-axis: LP balance (in millions)

Staking PAPER entitles holders to two streams of dividends: first, the protocol's profit-sharing revenue; second, any LP balance exceeding $5 million is entirely distributed to stakers.

In other words, the LP pool size is capped at $5 million. Beyond this threshold, all user losses are channeled back to PAPER holders. This creates a closed-loop system: "Losers get platform equity, winners take the losers' money, and the platform taxes winners to subsidize losers."

Therefore, a rational participation strategy can be summarized as: bet to lose money (and mint PAPER) when the LP pool's TVL is low, and stake PAPER to collect dividends when the LP pool's TVL is high.

A Stress Test for HyperEVM

In my opinion, the biggest uncertainty for PaperTrade lies in the HyperEVM network it's deployed on.

PaperTrade essentially uses Hyperliquid's price feed as a free, native oracle. All other logic runs within the smart contracts on HyperEVM.

This means any other high-performance blockchain with similar capabilities can replicate PaperTrade's entire mechanism on their own chain, as long as they integrate an external price oracle. A copycat could even offer things HyperEVM currently cannot: lower gas fees, higher TPS, more generous early subsidies, and more aggressive token incentives.

During the HyperEVM meme season in Q1 of last year, the network experienced a period of slow transaction speeds and high gas fees. The launch of PaperTrade represents another significant test for HyperEVM.