Original author: AARON XIE

Original compilation: Deep Chao TechFlow

Introducing: The beginning of permissionless lending on the chain

The story of on-chain permissionless lending platforms begins with Rari Capital and its Fuse platform. Launching in the first half of 2021, Fuse quickly gained traction after launching during the DeFi Summer Boom, a period that marked DeFi’s explosive growth. The brainchild of Rari Capital, this platform revolutionizes the DeFi space by enabling users to create and manage their own permissionless loan pools, in line with the emerging trend of yield optimization.

During its rise, Rari Capital adopted the (9, 9) narrative popularized by the Olympus DAO, a strategy designed to capitalize on OHM gains. The merger of Rari Capital and Fei Protocol further amplified the growth and community building during this period. The merger of Rari Capital and Fei Protocol in November 2021 revolved around a specific vision: to build a comprehensive DeFi platform that integrates Rari’s lending protocol with Fei’s stablecoin mechanism.

However, everything came crashing down in April 2022, when Fuse fell victim to a reentrancy attack, resulting in staggering financial losses estimated at around $80 million. The incident triggered intense scrutiny of Rari Capital’s security practices and raised broader concerns about the vulnerability of DeFi platforms to such attacks. In the wake of this crisis, Tribe DAO, the governing body formed from the merger of Rari Capital and Fei Protocol, faces difficult decisions. Pressure and challenges from hackers eventually led to the closure of Tribe DAO and Rari Capital later that year. This shutdown marks an important moment for the DeFi space, highlighting how vulnerable even the most innovative platforms are to security threats and underscoring the importance of having safe, robust protocols in decentralized finance.

The resurgence of unlicensed lending

The DeFi industry faces continued doubts about security following the Rari Capital hack in April 2022 and the major Euler hack in 2023, which involved a $200 million loss. Known for its innovative permissionless lending protocol that allows users to borrow and lend a variety of cryptoassets, Euler serves as another stark reminder of the fragility in the DeFi ecosystem. These major security breaches have fueled industry-wide pessimism, raising serious concerns about the security and reliability of decentralized finance platforms.

However, starting from the launch of Ajna in mid-July, the DeFi lending field has quietly recovered in the second half of 2023. This resurgence continues with the release of Morpho Blue on October 10, 2023. What makes these emerging protocols unique in the revitalized DeFi lending space is that their narrative shifts from purely “permissionless” to explicitly “modular.” Platforms such as Ajna and Morpho Blue are beginning to emphasize their “modular” nature, rather than focusing solely on the unrestricted access provided by permissionless systems. This approach presents them as a base layer technology on top of which third-party developers can build and customize lending use cases. This shift toward modularity highlights the flexibility and adaptability of these platforms, encouraging innovation and specialization in lending solutions. Alongside this modular narrative, safety is also emphasized. For example, Ajna differentiates itself by eliminating the need for oracles, eliminating dependence on external price sources, thereby reducing vulnerability. Morpho Blue introduces the concept of “permissionless risk management”, delegating the responsibility to third parties to select loan markets with the highest risk-adjusted returns.

Today’s Situation: DeFi Liquidity Returns

As we enter 2024, there is a clear upsurge across the cryptocurrency and DeFi industries. This resurgence is often attributed to new token distribution mechanisms, a theory championed by Multicoin’s Tushar. His theory is that every cryptocurrency bull run is triggered by innovative methods of token distribution. The concept of “points” has become a significant driver in the current market, with platforms like Eigenlayer leading the way with their restaking ecosystem. This approach not only renewed interest but also shaped the dynamics of the market. At the same time, the diversity of asset types on the chain is expanding, adding to the depth of the DeFi ecosystem.

Having said that, with institutions and “degens” alike seeking on-chain leverage, we must ensure we have the necessary lending systems and infrastructure in place. While established protocols like Compound and Aave have facilitated billions of dollars in transactions, their limited capacity cannot accommodate diverse collateral types, necessitating the emergence of emerging on-chain lending platforms. Over the past year or two, the space has seen the rise of new lending protocols such as Morpho, Ajna, and Euler, each competing for a piece of the on-chain lending market. Additionally, we have witnessed the development of NFT lending protocols such as Metastreet and Blur. This article aims to explore the narratives and functions of these projects, providing readers with an in-depth understanding of their differences and contributions.

Morpho Protocol

Origin of Morpho

Morpho’s origin story and the decision to develop Morpho Blue is rooted in the protocol’s initial success and a deep understanding of the limitations of the DeFi lending space. Launched by Paul Frambot and his Morpho Labs team, Morpho quickly rose to fame and became the third largest lending platform on Ethereum, with deposit assets exceeding $1 billion within a year. This impressive growth is driven by the Morpho Optimizer, which operates on top of existing protocols such as Compound and Aave, increasing the efficiency of interest rate models. However, Morphos growth was ultimately constrained by the design limitations of these underlying loan pools.

These realizations have led to a rethinking of decentralized lending from the ground up. The Morpho team, with its extensive experience, recognizes the need to look beyond existing models to achieve new autonomy and efficiencies in DeFi lending. This evolution gave birth to Morpho Blue. Morpho Blue is envisioned to solve several key issues in DeFi lending:

Trust Assumptions: The protocol reduces trust assumptions by allowing for more decentralized and dynamic risk management. This solves the problem of a large number of risk parameters that need to be constantly monitored and adjusted, which can be one of the main causes of security breaches.

Scalability and efficiency: By moving away from a DAO-style management model, Morpho Blue aims to increase scalability and efficiency. This includes solving the capital efficiency and interest rate optimization issues inherent in current decentralized lending models.

Decentralized Risk Management: Morpho Blue focuses on permissionless risk management, enabling a more transparent and efficient way of handling risk in lending platforms.

The development of Morpho Blue represents a significant shift towards building more opinion-free and trustless lending primitives in DeFi. This shift is complemented by the potential to build abstraction layers on top of these original capabilities, thereby establishing a more resilient, efficient, and open DeFi ecosystem at its core.

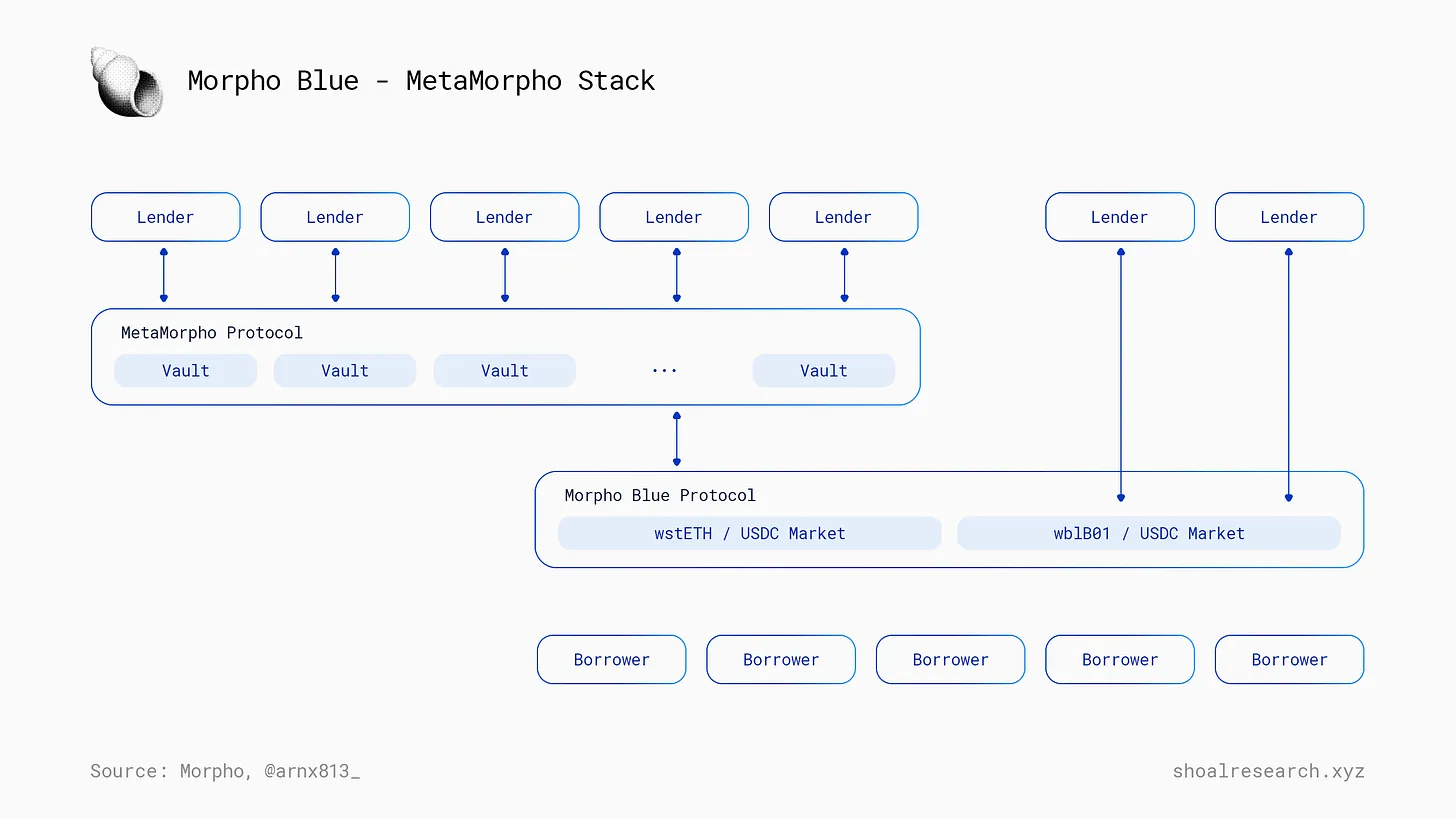

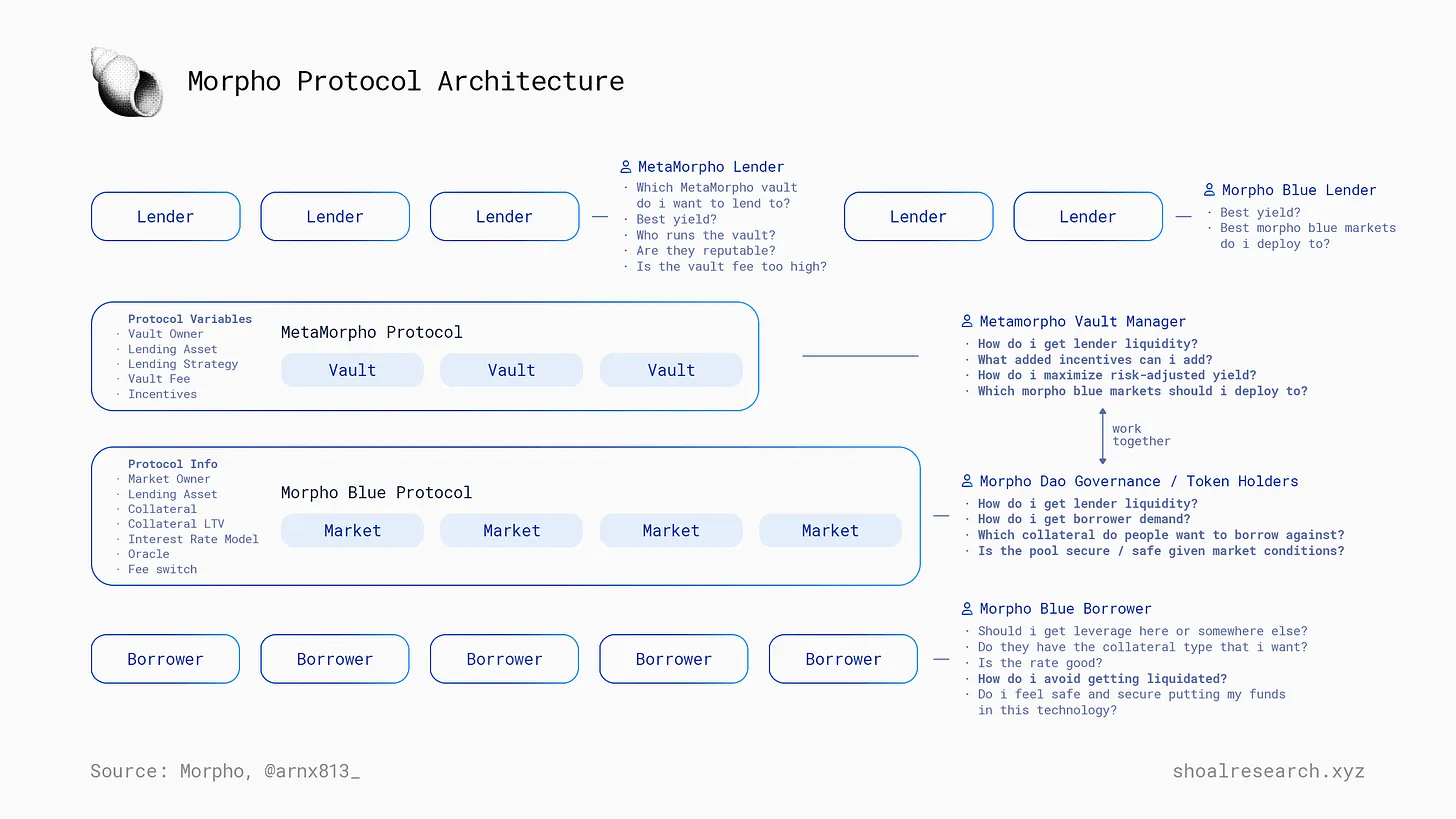

Morpho Blue (and MetaMorpho) Protocol Analysis

The Morpho protocol is divided into two different layers: Morpho Blue and MetaMorpho, each layer plays a unique role within the ecosystem.

Morpho Blue is designed to allow anyone to deploy and manage their own lending marketplace without permission. A key feature of every Morpho Blue Market is its simplicity and specificity: it supports only one mortgage asset and one loan asset, as well as an oracle with a defined loan-to-value ratio (LTV) and a specified price source. The framework ensures that each marketplace is simple and focused, making it accessible to a wide range of users. Morpho Blue also implements minimalist governance, with a concise and efficient code base of only 650 lines of Solidity, improving its security and reliability. Additionally, Morpho Blue includes a fee switch managed by $MORPHO token holders, which adds a layer of community-driven oversight to the protocol.

MetaMorpho, on the other hand, introduces the concept of loan vaults managed by third-party “risk experts.” In this layer, lenders deposit funds into vaults, and vault administrators are responsible for allocating this liquidity into the various Morpho Blue markets. This approach allows for more complex and dynamic management of funds, leveraging the expertise of professional managers to optimize returns and manage risk. MetaMorphos core innovation lies in its product stance and developer-friendliness. It creates a platform where third-party developers can build on Morpho Blue infrastructure, adding another level of diversity and innovation to the Morpho ecosystem.

Steakhouse Financial Case Study

Steakhouse Financial, led by Sebventures, is an example of effective utilization of the Morpho Blue ecosystem. This crypto-native DAO’s financial advisory services have made significant progress in the DeFi space, and its innovative lending methods are eye-catching. Since January 3, Steakhouse Financial has been managing a USDC MetaMorpho vault with a total locked value of $12.8 million. The vault is primarily focused on stETH and wBTC. In the future, Steakhouse Financial has expressed interest in supporting real world assets (RWA) as collateral.

Four roles in the Morpho ecosystem

Given current developments, there are four main roles in the Morpho ecosystem: MetaMorpho Lenders, Morpho Blue Lenders, Borrowers, MetaMorpho Vault Administrators and Morpho Governance/Morpho Labs

Below is a diagram of the complete Morpho protocol architecture, annotating the participants and their goals/thought processes.

Morphos growth

MMorpho differentiates itself through a combination of strong branding and superior business development execution. While other lending projects have emerged, including Ajna, Midas, Frax Lend, and Silo Finance, Morpho comes out on top in terms of total value locked. The protocol, while inherently permissionless, abstracts it through a permissioned Morpho UI. This curated UI is a testament to the team’s commitment to maintaining brand and trust, by carefully showcasing only the best lending marketplaces and partners. This subtle approach: the appeal of selling a permissionless protocol while effectively connecting its front-end to a reputable entity has ensured that Morpho Blue is a benchmark for quality and reliability in the DeFi space, despite what the DeFi space may seem like. Risky and unstable.

Building on the above sentiments, Morpho invests a lot of time and effort into the end-user experience. Morpho has developed a clean and intuitive UI/UX that simplifies interaction for end users and lending operators. This is not common among many DeFi lending protocols as they still have a gimmicky feel to them. Furthermore, the development of abstraction layers, such as MetaMorpho, simplifies the appeal. Morpho Blue’s subtle strategy of balancing permissionless innovation with a permissioned, brand-focused front end is impressive. This approach not only emphasizes Morpho’s adaptability and flexibility as a platform, but also positions it as a leader in promoting professional and secure lending solutions in the DeFi space.

What does Morpho do well? What areas need improvement?

The following are the advantages:

Strong personal brands of team members, such as Paul and Merlin, enhance credibility and visibility.

Efficiently build the ecosystem by selling simplicity, building abstraction layers like MetaMorpho, and locking in third-party lending operators like Steakhouse, B Protocol, Block Analitica, and Re 7, as well as locking in token incentives like stETH.

Its optimizer product has a strong existing product and brand, which provides Morpho Blue with significant leverage for success.

What needs improvement: The unit economics of third-party risk managers need to improve. Without taking into account engineering, legal and risk management costs, Block Analitica, which has $45 million in assets under management, would have earned $70,000 in revenue.

Ajna, the oracle-less market

Origin of Ajna

Ajna was founded by several former MakerDAO team members who recognized scalability and risk issues in previous generation lending protocols. Oracle dependencies and governance are factors that limit growth and are major sources of risk. The key idea is to outsource the Oracle functionality to the lenders and liquidators themselves. Their vision is to create Lending Uniswap, an immutable protocol that can scale to support almost any asset, including long-tail assets and NFTs. This original and innovative design was arrived at through a development process of more than two years, including more than ten code audits.

Ajna Finance’s origin story is closely tied to the DeFi ecosystem’s broader desire for security and robustness in 2023. This Dan Elizter article on the need for oracle-less protocols in DeFi highlights this (Please read here). Elitzer, founder of Nascent VC and a well-known figure in the DeFi community, outlined the ongoing security challenges plaguing DeFi and the billions of dollars in losses caused by hacker attacks, emphasizing fundamental changes in DeFi protocol design and security. The need for sexual rethinking.

Against this backdrop, the Ajna protocol emerges as a compelling solution. Launched in mid-July 2023, Ajna’s design philosophy aligns with what Elitzer describes as a vision for DeFi: a protocol that operates with zero dependencies and therefore no trust, including a lack of governance, upgradeability, and oracles. This approach reduces the theoretical attack surface and inherent risks within the protocol.

Ajna protocol analysis

In the world of DeFi lending, Ajna stands out with its unique approach to lending. It is a non-custodial, permissionless system that requires no oracles or governance, ensuring a high degree of decentralization and autonomy. Ajna allows the creation of marketplaces with specific collateral and loan assets, simplifying the process and enhancing user accessibility. The platform supports a variety of assets, including fungible and non-fungible tokens, expanding the scope beyond the types of collateral typically seen in DeFi. Ajna’s features include facilitating lending cases such as NFT lending and shorting the market without being subject to limitations common to other platforms.

Three players in the Ajna ecosystem

Given current developments, there are three main actors in the Morpho ecosystem: Ajna Lenders, Ajna Borrowers, and Ajna Governance/Token Holders.

Ajnas growth

Ajna has taken a definite hit to its security-oriented brand after suffering a major security breach in the second half of 2023. After the relaunch, the project began pursuing complete decentralization, severing all ties with centralized laboratory companies. Now, they are a fully decentralized DAO and protocol.

Rebooting a DeFi protocol is difficult and is never a good thing. While Ajna experienced setbacks, they are back with a re-audited protocol with two clear selling points: full decentralization and no oracles. Ajna’s strategy relies entirely on DeFi local brands.

Now, the long-term questions are as follows:

What lending use cases does Ajna uniquely unlock that differentiates it from Morpho and other competitors?

How effective is decentralized DAO coordination as Ajna attempts to execute its growth and commerce growth strategy?

Euler, rising from the shadows

Origin of Euler

The emergence of the Euler Protocol as a next-generation DeFi lending platform represents a significant evolution from first-generation protocols such as Compound and Aave. As a decentralized service, Euler addresses a critical gap in the DeFi market: the lack of support for non-mainstream tokens in lending services. Recognizing the unmet need for lending and borrowing long-tail crypto assets, Euler offers a permissionless platform that can list almost any token as long as it is paired with WETH on Uniswap v3.

The Euler protocol stands out in the DeFi lending space with several key innovations:

It adopts a unique risk assessment method that takes into account the collateral and lending factors of the asset, enhancing the accuracy of risk assessment.

Euler also integrates Uniswap v3’s decentralized TWAP oracle for asset valuation, supporting its permissionless ethos by supporting diverse asset listings.

Additionally, the protocol introduces a new clearing mechanism that is resistant to MEV attacks, as well as a reactive interest rate model that automatically adjusts to market conditions.

These features, coupled with the implementation of sub-accounts for user convenience, make Euler a sophisticated and flexible platform for DeFi lending.

Unfortunately, on March 13, 2023, Euler Finance will experience one of the largest DeFi hacks ever. The flash loan attack on March 13 caused losses of more than $195 million and triggered a ripple effect that affected numerous decentralized finance (DeFi) protocols. In addition to Euler, at least 11 other protocols have suffered losses due to the attack.

After the Hack: Euler V2

After a year of silence, Euler launched its v2 on February 22, 2024. Euler v2 is a modular lending platform consisting mainly of two components: Euler Vault Kit (EVK) and Ethereum Vault Connector (EVC). EVK enables developers to create their own custom lending vaults; it can be described as a vault development kit that makes it easier to build vaults using Eulers technology framework. EVC is an interoperability protocol that enables vault creators to connect their vaults together so that developers can more efficiently link vaults together to pass information and interact with each other. Together, these two technologies act as a base layer lending infrastructure.

There will be two main types of Euler vaults:

Core: A managed lending market similar to Euler v1, managed by DAO.

Edge: A permissionless lending market with greater parameter flexibility. A pooled lending experience, not a 1:1 like Morpho Blue or Ajna.

Euler’s brand strategy

Similar to Ajna and Morpo, Euler is a strong advocate of a “modular” lending narrative that aims to build a permissionless base-layer lending protocol that third parties can leverage. However, Euler differs significantly in its public-facing marketing and branding strategies. Unlike Morpho, which takes an extremely abstract and simplified approach, Euler prefers to use its feature-rich technology as a key selling point of its brand and technology. Some of the features it highlights are advanced risk management tools such as sub-accounts, PL simulator, limit order types, new liquidation mechanism (fee process), and more.

Who are the end users of Euler and what is their end product?

Euler offers a powerful and novel feature set that goes beyond Morpho Blue (e.g. sub-accounts, expense streams, PL simulator, etc.). The question remains: is Euler selling its lending infrastructure to third-party lending operators, or are they building their own lending marketplace? These two opportunities have different customer bases. If Euler is competing with Morpho to attract third-party lending operators, how easy is it to build abstractions on Euler v2? Euler misses the idea of a pool manager abstract primitive equivalent to MetaMorpho, but they seem to want to replicate what Morpho does with 3rd party pool operators.

Is it a good idea to charge a 1% agreement fee at launch?

At launch, Euler enforces a minimum 1% protocol fee derived from the repository manager. This can be an important psychological barrier because during the growth phase, expense is a stumbling block to development. Morpho, on the other hand, has a protocol where their business source licensing terms are tied to a fee mechanism: if a fee is charged, the code becomes open source (and therefore freely forkable).

at last

Relative to other, more novel aspects of DeFi (such as liquid staking and re-collateralization), the lending space seems to have matured, and one may question where the innovation lies and what the future of one of DeFis more mature industries might be. However, it’s a fair and reasonable argument to make that lending is one of the only areas in DeFi that achieves true product-market fit and largely avoids Ponzi economies. That said, innovation will almost inevitably follow where product-market fit occurs, so if the past is any indicator of the future, DeFi lending will certainly see evolution and evolution in future cycles.

In this article, we discuss several projects in the lending space, including Ajna, Morpho, and Euler, among others. The overarching theme of all three lending projects is not only the creation of permissionless marketplaces, but the creation of permissionless marketplaces in a user-friendly, user-centric way. Yes, before these three protocols, one could start ones own lending pool/protocol, but that was not user friendly. In the next DeFi lending cycle, we are not only focusing on the permissionless side (which seems to be the obvious direction of protocol trends), but also on the user experience side. Companies like Summer.fi are creating new lending experiences (and the overall DeFi experience) for a more streamlined DeFi experience. As their integrations increase and their experience is simpler than directly accessing the front-end hosted by the creators of various lending protocols, they will likely continue to gain popularity. With the focus on intent-based protocols rising, intent-based lending or borrowing (similar to how Morpho aggregates between Aave and Compound) may prove to be another narrative for the future of lending: just enter what you want Borrowing things, this new narrative will find the best, risk-adjusted opportunities.

To some extent, creating marketplaces in a permissionless manner will certainly become simpler as well. Currently, Morpho is working with three complex groups (B Protocol, Block Analitica, and Steakhouse Finance) to operate their new permissionless marketplace, but soon, this will also become more user-friendly, just like the already permissionless lending experience The same as itself can be done by any user. The ability for any user to create a market will allow for a Cambrian explosion of innovation in the lending market, from new asset types as collateral (e.g. LRT, RWAs) to new structured products focused on various income opportunities .